Did you know that India is the world’s top recipient of international remittances? In fiscal year 2025 alone, the country received a record-breaking $135.46 billion. From families relying on funds sent by relatives abroad to freelancers and businesses serving global clients, receiving money from abroad has become a key part of everyday financial life in India.

As remote work and cross-border trade continue to expand, the demand for swift, cost-effective, and compliant payment solutions has never been greater. Yet, challenges like high transaction fees, exchange rate markups, bank delays, and regulatory roadblocks can create unnecessary friction.

This blog will help you understand how to receive money from abroad in India safely and efficiently. We’ll break down different transfer methods, highlight key service providers, explain required documents and timelines, and cover hidden costs and tax implications so you can choose the best option for your personal or business needs.

Tired of getting lost in the maze of international payment options? Whether it’s a freelance gig payout, help from family overseas, or a business transaction, how you receive money from abroad can make or break the experience. The good news? You’ve got options.

1. Bank transfers: Bank transfers are one of the most secure and standard methods for receiving money from abroad. You’ll need to provide your bank account details along with your SWIFT or IBAN code. This method is ideal for large sums but may take a few business days, depending on the sender's location and the bank's processing times.

2. Cash pickup: Cash pickup services are popular for those who don’t have bank accounts. With a transaction number and a valid ID, you can collect cash from designated locations. Services like Western Union and MoneyGram offer this option, making it a fast and convenient way to send money.

3. eWallets: Digital wallets, such as PayPal and Payoneer, enable users to receive funds quickly. After receiving money in your eWallet, you can transfer it to your bank account or use it for digital transactions.

4. Money orders and cheques: Although considered old-school, money orders and cheques remain viable methods, especially for those who prefer traditional mail. However, they take longer due to postal delays and bank clearing times.

When it comes to receiving money from abroad in India, multiple service providers offer a range of features to cater to different needs.

From multi-currency accounts to flexible payment options, choosing the right provider depends on factors like transfer fees, exchange rates, and convenience.

Whether you’re a freelancer juggling international clients or a business collecting payments from overseas, choosing the right service provider makes all the difference.

The wrong choice could mean high fees, currency conversion losses, and delayed payouts. The right one? Faster payments, better rates, and peace of mind.

So, which providers deliver on speed, transparency, and support in the real world? Let’s break it down.

PayGlocal streamlines the process of receiving money from abroad, offering simplified solutions for freelancers, businesses, and individuals with international clients. Here’s what makes PayGlocal a top choice:

Wise is one of the best choices for those who need flexibility with multiple currencies. It offers:

PayPal is widely known and convenient, but it comes with higher fees compared to some alternatives. Key points include:

Instamojo is a versatile platform popular for domestic payments, with limited but flexible options for international transactions:

Payoneer is favored by freelancers, businesses, and marketplace sellers who need to manage payments in multiple currencies. Key features include:

As a service under PayPal, Xoom specializes in fast money transfers but comes with higher costs:

There’s no one-size-fits-all here. Your ideal payment gateway depends on what you value most, including speed, fees, flexibility, or ease of use. Some platforms give you total control over currencies, while others shine with seamless integrations or payout support. What matters is that you choose a service that aligns with your specific needs.

Now that you know about the various payment providers, let’s list out the mandatory information a payee needs to be ready with, for receiving money from abroad:

To ensure a smooth transaction across borders, you’ll need the following details:

This information is crucial for tracking transfers and ensuring regulatory compliance.

Speed matters, especially when payments are tied to deadlines or cash flow. Different methods come with varying times of wait, and knowing what to expect can save you stress (and follow-up emails). Here’s how long it takes to receive money from abroad, depending on the method of transfer:

1. Bank transfers

Timeframe: 1–5 business days.

International bank transfers generally take a few days due to processing times, currency conversion, and the clearing systems in both the sending and receiving countries. Factors like weekends, bank holidays, and intermediary banks can also affect the speed.

2. eWallets

Timeframe: Often instantaneous or within a few hours.

Digital wallets, such as PayPal or Payoneer, are designed for fast and convenient transfers. As long as both sender and recipient have accounts, transfers for receiving money from abroad can be completed almost immediately.

3. Cash pickups

Timeframe: Available within minutes.

Services like Western Union and MoneyGram offer rapid transfers where recipients can collect cash within minutes of the transfer being initiated for receiving money from abroad. However, this speed may come at a higher cost.

4. Money orders and cheques:

Timeframe: Several weeks.

This is one of the slowest methods, as it involves mailing physical documents. Delivery delays due to postal services, coupled with the time it takes to process the cheque or money order once received, can extend the waiting period by weeks.

For a deeper understanding of what slows down international payments and what you can do about it, it’s worth exploring the common challenges businesses face with cross-border transfers and the solutions that are helping them move money faster.

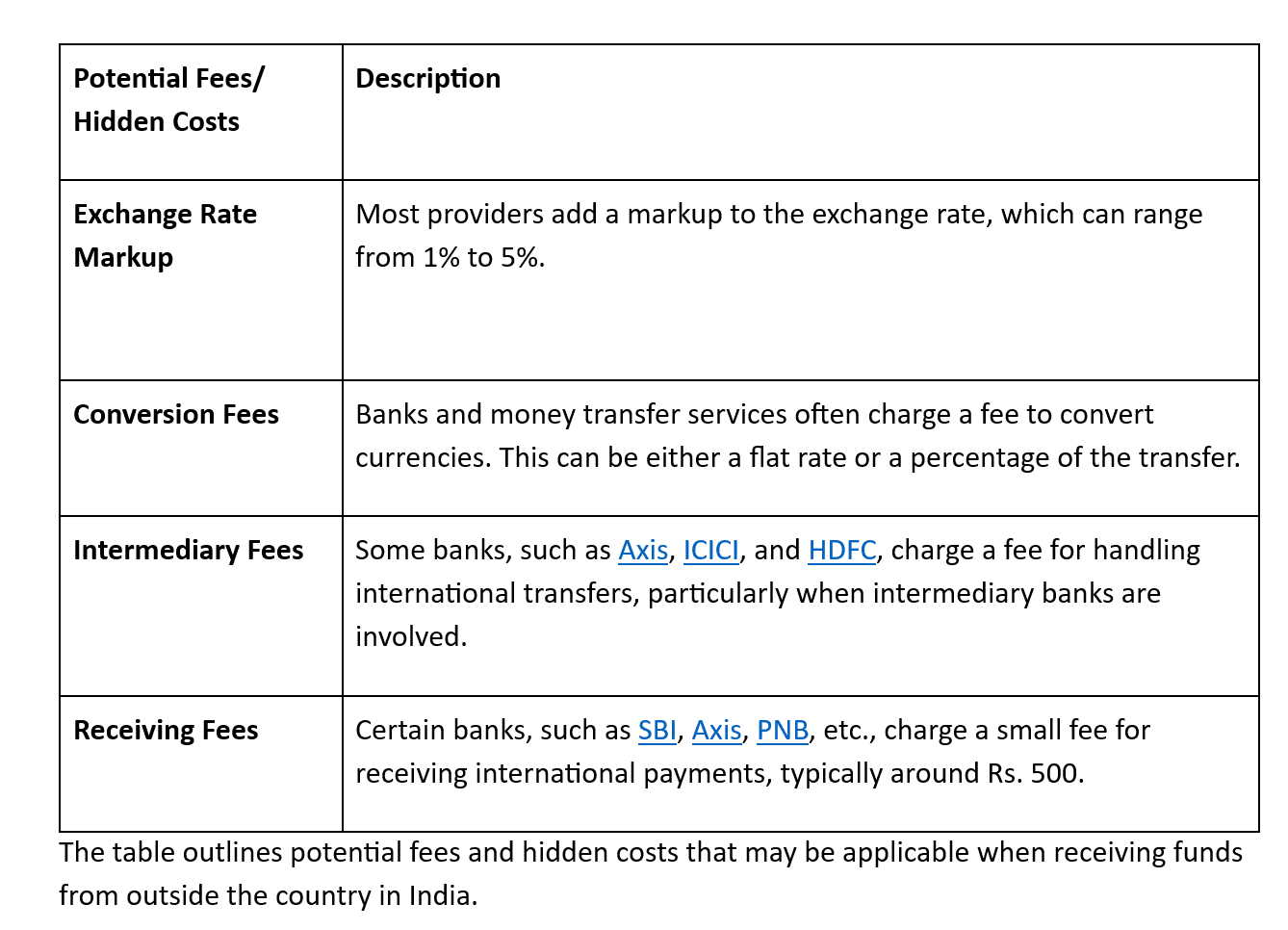

When receiving money from abroad, you may encounter various fees, such as:

NOTE: It is advisable to always compare the mid-market exchange rate to the rate offered by your provider to avoid overpaying.

Receiving money from abroad? Don’t let paperwork slow you down. Indian regulations are clear, but banks won’t process your transfer unless all documents are in order. Whether you're a freelancer, a business, or an NRI, here's what you need to stay compliant and keep your funds moving without delay:

Now that you’ve understood various regulations in compliance with Indian laws, it’s clear that receiving money from abroad has different tax implications depending on the purpose and amount, as listed below:

Is receiving money from abroad always tax-free? Not quite. Whether you’re freelancing for overseas clients or getting support from family abroad, the taxman wants his due. The rules are straightforward, but missing the fine print can cost you. We break down exactly what’s taxable, what’s not, and what you need to report so you stay compliant without the confusion.

Whether you’re a freelancer earning income or someone receiving funds from family overseas, knowing what’s taxable and what’s not can help you avoid surprises during tax season. And if you're curious about how these incoming transfers work behind the scenes, it’s worth exploring how payment transaction processing operates.

NOTE:

It’s essential to keep records of all transfers and consult with a tax advisor to ensure compliance with Indian tax laws.

For large or frequent transfers, it’s wise to consult with a financial advisor to navigate potential legal and tax implications.

Are you still chasing payments weeks after you’ve done the work? Still stuck paying fees you didn’t agree to? You’re not alone, and you shouldn’t have to settle for it.

Here’s the problem: most cross-border payment systems are slow, fragmented, and designed for banks, not businesses like yours. We’ve seen the mess first-hand. So we built a better way.

Here’s how PayGlocal helps you get paid faster, in full, and without the drama:

PayGlocal cuts through the chaos and gives you control. We’ve helped thousands of freelancers, startups, and growth-stage companies skip delays and take control of their international payments.

India offers a range of secure and flexible options for receiving money from abroad. Are you considering your next financial deposit from overseas? By selecting the correct transfer method and staying informed on fees and regulations, you can save both time and money.

Why get bogged down by hefty fees and sluggish transfers? Instead, prioritize speed, simplicity, and cost-efficiency while keeping tax obligations in mind for a seamless international payment experience. That’s precisely where PayGlocal steps in, making it easier for you to receive global payments without delays, confusion, or hidden charges.

Ready to receive your next international payment? Sign up with PayGlocal now and experience innovative payment solutions that put you in control. Simplify your global payments and enjoy the best support for your recurring transfers, all with complete transparency.

As remote work and cross-border trade continue to expand, the demand for swift, cost-effective, and compliant payment solutions has never been greater. Yet, challenges like high transaction fees, exchange rate markups, bank delays, and regulatory roadblocks can create unnecessary friction.

This blog will help you understand how to receive money from abroad in India safely and efficiently. We’ll break down different transfer methods, highlight key service providers, explain required documents and timelines, and cover hidden costs and tax implications so you can choose the best option for your personal or business needs.

Key Takeaways

- You can receive international payments through bank transfers, eWallets, cash pickups, and services like PayGlocal, Wise, and PayPal.

- Key details, such as your SWIFT code, account information, and the purpose of the transfer, are essential for smooth processing.

- Transfer speed varies: bank transfers take 1–5 days, while eWallets and cash pickups can be near-instant.

- Watch out for hidden fees. Check exchange rate markups, conversion charges, and intermediary bank costs.

- Income from abroad may be taxable based on the amount and purpose. Consult a tax advisor for large or frequent transfers.

What are the different ways to receive money from abroad?

Tired of getting lost in the maze of international payment options? Whether it’s a freelance gig payout, help from family overseas, or a business transaction, how you receive money from abroad can make or break the experience. The good news? You’ve got options.

1. Bank transfers: Bank transfers are one of the most secure and standard methods for receiving money from abroad. You’ll need to provide your bank account details along with your SWIFT or IBAN code. This method is ideal for large sums but may take a few business days, depending on the sender's location and the bank's processing times.

2. Cash pickup: Cash pickup services are popular for those who don’t have bank accounts. With a transaction number and a valid ID, you can collect cash from designated locations. Services like Western Union and MoneyGram offer this option, making it a fast and convenient way to send money.

3. eWallets: Digital wallets, such as PayPal and Payoneer, enable users to receive funds quickly. After receiving money in your eWallet, you can transfer it to your bank account or use it for digital transactions.

4. Money orders and cheques: Although considered old-school, money orders and cheques remain viable methods, especially for those who prefer traditional mail. However, they take longer due to postal delays and bank clearing times.

When it comes to receiving money from abroad in India, multiple service providers offer a range of features to cater to different needs.

From multi-currency accounts to flexible payment options, choosing the right provider depends on factors like transfer fees, exchange rates, and convenience.

Which service providers are best for receiving money in India?

Whether you’re a freelancer juggling international clients or a business collecting payments from overseas, choosing the right service provider makes all the difference.

The wrong choice could mean high fees, currency conversion losses, and delayed payouts. The right one? Faster payments, better rates, and peace of mind.

So, which providers deliver on speed, transparency, and support in the real world? Let’s break it down.

PayGlocal streamlines the process of receiving money from abroad, offering simplified solutions for freelancers, businesses, and individuals with international clients. Here’s what makes PayGlocal a top choice:

- Multi-Currency Accounts: Manage and receive payments in multiple currencies for greater flexibility.

- Global Payment Methods: Seamlessly collect payments via a variety of international options.

- Low-Cost Payment Collection: Minimize fees while maximizing the value of each transaction.

- Unparalleled Payment Success Rate: Fast onboarding, local accounts in 4 countries, and easy integration with freelance platforms, all while tracking payments in real-time.

2. Wise

Wise is one of the best choices for those who need flexibility with multiple currencies. It offers:

- Multi-Currency Accounts: You can hold and manage account details in up to 8 different currencies, making it ideal for freelancers or businesses that deal with international clients.

- Mid-Market Exchange Rate: Wise stands out by offering the mid-market exchange rate, with no hidden markups, ensuring that you get a fair deal when converting currencies.

- Low-Cost Transfer Fees: Ideal for large payments, Wise charges a minimal, transparent fee, making it one of the most cost-effective options for sending and receiving international transfers.

3. PayPal

PayPal is widely known and convenient, but it comes with higher fees compared to some alternatives. Key points include:

- Account Setup: Both the sender and receiver must have PayPal accounts, adding an extra layer of complexity if one party is unfamiliar with the platform.

- Bank Withdrawal Fees: PayPal charges fees for withdrawing money to your bank account, typically around 2.5% of the transferred amount, which can add up for larger payments.

- Convenience vs. Cost: While PayPal is user-friendly and supports a wide range of currencies, its fees make it less appealing for frequent international transfers.

4. Instamojo

Instamojo is a versatile platform popular for domestic payments, with limited but flexible options for international transactions:

- Payment Links for Domestic Use: This feature enables users to generate payment links for seamless domestic transactions, simplifying the process of requesting payments within India.

- International Payments via Contact: Instamojo supports international payments, but you’ll need to reach out to their team to enable this feature, which makes it less straightforward than other providers.

- Flexible but Limited: While great for domestic use, Instamojo's international capabilities are more restricted and require manual setup.

5. Payoneer

Payoneer is favored by freelancers, businesses, and marketplace sellers who need to manage payments in multiple currencies. Key features include:

- Multiple Currency Accounts: Payoneer supports various currencies, allowing users to receive payments globally without the hassle of currency conversion.

- 2% Above Mid-Market Rate: While Payoneer offers convenience, it charges a 2% markup above the mid-market rate for currency conversions, which may reduce the value of your transfers.

- Business-Friendly: It’s beneficial for receiving payments from international marketplaces or clients, offering a wide range of integrations and payout options.

6. Xoom

As a service under PayPal, Xoom specializes in fast money transfers but comes with higher costs:

- Bank Transfers or Cash Pickups: Xoom offers flexibility for recipients in India, allowing for both bank transfers and cash pickups.

- High Fees for Card Payments: Using a credit card to send money incurs higher fees, and the exchange rate is often marked up, making Xoom one of the more expensive options for receiving funds.

- Best for Speed: If speed is your priority, Xoom is a solid choice; however, convenience comes at a cost, especially for card-based transfers.

There’s no one-size-fits-all here. Your ideal payment gateway depends on what you value most, including speed, fees, flexibility, or ease of use. Some platforms give you total control over currencies, while others shine with seamless integrations or payout support. What matters is that you choose a service that aligns with your specific needs.

Now that you know about the various payment providers, let’s list out the mandatory information a payee needs to be ready with, for receiving money from abroad:

What information do you need to receive money from abroad?

To ensure a smooth transaction across borders, you’ll need the following details:

- Full Name

- Bank Account Number and Bank Details

- SWIFT or IBAN Code

- Purpose of the Transfer

- Sender’s Name and Address

This information is crucial for tracking transfers and ensuring regulatory compliance.

How long does it take to receive money from abroad?

Speed matters, especially when payments are tied to deadlines or cash flow. Different methods come with varying times of wait, and knowing what to expect can save you stress (and follow-up emails). Here’s how long it takes to receive money from abroad, depending on the method of transfer:

1. Bank transfers

Timeframe: 1–5 business days.

International bank transfers generally take a few days due to processing times, currency conversion, and the clearing systems in both the sending and receiving countries. Factors like weekends, bank holidays, and intermediary banks can also affect the speed.

2. eWallets

Timeframe: Often instantaneous or within a few hours.

Digital wallets, such as PayPal or Payoneer, are designed for fast and convenient transfers. As long as both sender and recipient have accounts, transfers for receiving money from abroad can be completed almost immediately.

3. Cash pickups

Timeframe: Available within minutes.

Services like Western Union and MoneyGram offer rapid transfers where recipients can collect cash within minutes of the transfer being initiated for receiving money from abroad. However, this speed may come at a higher cost.

4. Money orders and cheques:

Timeframe: Several weeks.

This is one of the slowest methods, as it involves mailing physical documents. Delivery delays due to postal services, coupled with the time it takes to process the cheque or money order once received, can extend the waiting period by weeks.

For a deeper understanding of what slows down international payments and what you can do about it, it’s worth exploring the common challenges businesses face with cross-border transfers and the solutions that are helping them move money faster.

What fees and hidden costs should you be aware of?

When receiving money from abroad, you may encounter various fees, such as:

NOTE: It is advisable to always compare the mid-market exchange rate to the rate offered by your provider to avoid overpaying.

What documents are required to comply with Indian regulations?

Receiving money from abroad? Don’t let paperwork slow you down. Indian regulations are clear, but banks won’t process your transfer unless all documents are in order. Whether you're a freelancer, a business, or an NRI, here's what you need to stay compliant and keep your funds moving without delay:

- Foreign Inward Remittance Certificate (FIRC): This certificate is issued by the receiving bank to confirm the receipt of foreign currency. Businesses must demonstrate that the money was obtained legally.

- Document requirements: For large transactions, banks may ask for your PAN card, identity proof, and details of the transfer.

- NRE accounts for NRIs: NRIs should use NRE (Non-Resident External) accounts to receive money in India. Funds in these accounts are repatriable, and interest earned is tax-free.

Now that you’ve understood various regulations in compliance with Indian laws, it’s clear that receiving money from abroad has different tax implications depending on the purpose and amount, as listed below:

What are the tax implications of receiving foreign funds in India?

Is receiving money from abroad always tax-free? Not quite. Whether you’re freelancing for overseas clients or getting support from family abroad, the taxman wants his due. The rules are straightforward, but missing the fine print can cost you. We break down exactly what’s taxable, what’s not, and what you need to report so you stay compliant without the confusion.

- 1. Income Tax for Freelancers and Businesses: Payments received for services rendered are taxable under income tax rules. Make sure to report these amounts as part of your annual income.

- 2. Personal transfers: Transfers from relatives abroad that exceed Rs. 50,000 are subject to taxation unless they fall under non-taxable categories, such as gifts.

- 3. Non-taxable amounts: Transfers from family members such as parents, children, or siblings are non-taxable, regardless of the amount.

Whether you’re a freelancer earning income or someone receiving funds from family overseas, knowing what’s taxable and what’s not can help you avoid surprises during tax season. And if you're curious about how these incoming transfers work behind the scenes, it’s worth exploring how payment transaction processing operates.

NOTE:

It’s essential to keep records of all transfers and consult with a tax advisor to ensure compliance with Indian tax laws.

For large or frequent transfers, it’s wise to consult with a financial advisor to navigate potential legal and tax implications.

PayGlocal: A wise choice for global payment collections

Are you still chasing payments weeks after you’ve done the work? Still stuck paying fees you didn’t agree to? You’re not alone, and you shouldn’t have to settle for it.

Here’s the problem: most cross-border payment systems are slow, fragmented, and designed for banks, not businesses like yours. We’ve seen the mess first-hand. So we built a better way.

Here’s how PayGlocal helps you get paid faster, in full, and without the drama:

- Dynamic checkout that converts: We provide your international customers with what they want. Localized payment options that enhance success rates and minimize drop-offs. You close more sales. Simple.

- Card payments that work: No more failed authorizations. We process Visa, Mastercard, and local cards with high success rates, because your cash flow shouldn’t depend on backend glitches.

- Global methods, zero complications: Bank transfers in the US. Wallet payments in the UAE. Whatever your customer prefers, we handle it, so you don’t lose business to payment friction.

- Recurring payments, minus the manual work: Set it, forget it. Perfect for subscriptions, retainers, or repeat clients. You get predictable revenue, and they get seamless billing.

- Multi-currency account, one dashboard: Receive USD, EUR, GBP, and more, without opening multiple foreign accounts. Track everything in INR. There is no toggling between systems. No confusion.

- One platform for everything: No silos. There is no third-party juggling. Just a single dashboard where you track collections, manage compliance, and move faster.

- Built-in sanction screening: We handle the backend checks so you stay compliant, without slowing down your payments or adding red tape.

PayGlocal cuts through the chaos and gives you control. We’ve helped thousands of freelancers, startups, and growth-stage companies skip delays and take control of their international payments.

Conclusion

India offers a range of secure and flexible options for receiving money from abroad. Are you considering your next financial deposit from overseas? By selecting the correct transfer method and staying informed on fees and regulations, you can save both time and money.

Why get bogged down by hefty fees and sluggish transfers? Instead, prioritize speed, simplicity, and cost-efficiency while keeping tax obligations in mind for a seamless international payment experience. That’s precisely where PayGlocal steps in, making it easier for you to receive global payments without delays, confusion, or hidden charges.

Ready to receive your next international payment? Sign up with PayGlocal now and experience innovative payment solutions that put you in control. Simplify your global payments and enjoy the best support for your recurring transfers, all with complete transparency.