According to recent data, India’s services exports have grown rapidly, from around USD 158 billion in 2013-14 to close to USD 387 billion in 2024-25. This rise shows how often Indian companies now work with partners abroad. However, to transfer these funds securely and without delay, it’s essential to understand the rules for sending money abroad from India.

The Liberalized Remittance Scheme (LRS) sets clear guidelines for how much money you can transfer, what purposes are allowed, and what taxes apply. Getting this right helps you avoid penalties and ensure your money reaches its destination smoothly.

In this guide, we break down everything you need to know about sending funds abroad from India. Find out the exact limits, required documents, tax implications, and how to choose the right transfer method for your needs.

Tax implications: TCS applies to amounts above ₹10 lakh, with rates varying from 5% to 20% based on purpose.

The rules for sending money abroad from India are governed by the Liberalized Remittance Scheme (LRS). This framework allows resident individuals to send money overseas for specific permitted purposes without requiring prior approval from authorities.

Under LRS, you can send up to $250,000 per financial year (April to March) for various current and capital account transactions. This limit includes the transfer amount plus all associated fees, charges, and foreign exchange conversion costs.

For example, if you're a freelancer receiving payments from a US client and need to pay for software licenses abroad, all costs, including the payment amount, transfer charges, and currency conversion fees, count toward your annual $250,000 limit. The scheme covers most legitimate business and personal needs, including service payments, business expenses, travel costs, and professional fees.

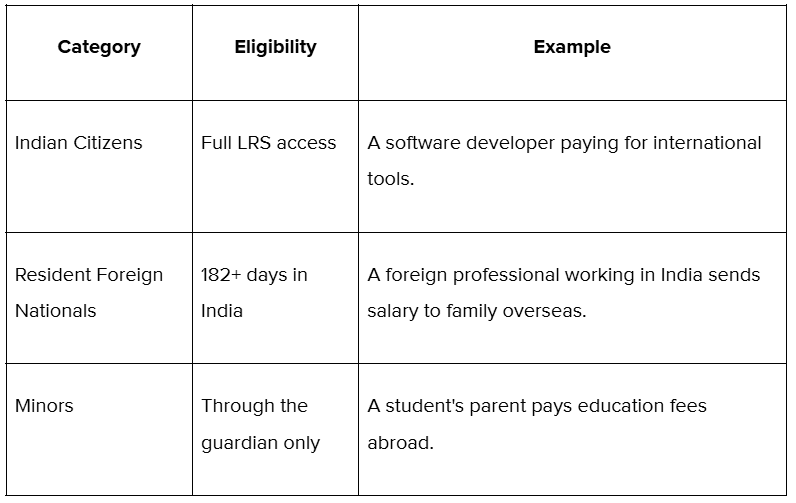

Only resident individuals, as per the Foreign Exchange Management Act (FEMA) can use the LRS. This includes Indian citizens, people of Indian origin, and foreign nationals residing in India for more than 182 days in the preceding financial year.

Some examples of who qualifies and can send money abroad include:

For instance, a freelance graphic designer who's an Indian citizen can use LRS to pay for Adobe subscriptions or send money to international contractors. Similarly, an export business owner can use their personal LRS limit for business-related international payments like attending conferences or purchasing software.

It’s worth noting that Non-Resident Indians (NRIs) follow different rules and have separate regulations for sending money abroad. They can use their NRE or NRO accounts with different limits and documentation requirements based on their account type and residency status.

Minors can also send money abroad, but only through their legal guardians who complete the necessary documentation. The guardian must provide additional proof of their relationship with the minor.

More importantly, LRS is not available to entities such as corporations, partnership firms, or trusts. These entities must follow different regulations for outward remittances based on their specific business needs and transaction purposes.

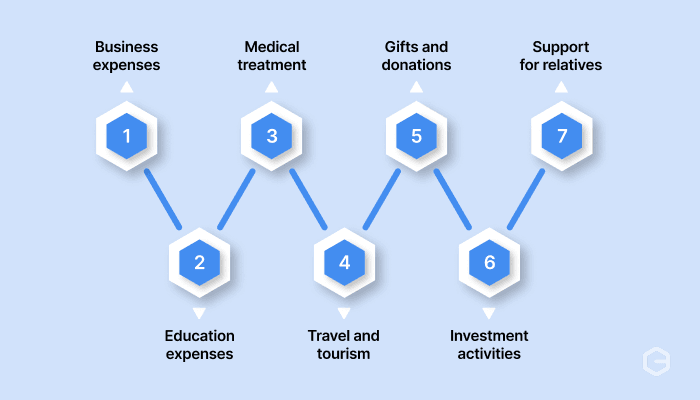

LRS permits money transfers for specific purposes only. Here are the key permitted purposes:

Business expenses: Software licenses, subscription fees, contractor payments.

Education expenses: Tuition, accommodation, books, and living costs.

Medical treatment: Hospital bills, treatment costs, travel for medical care.

Travel and tourism: Holiday expenses, business travel, emergency costs.

Gifts and donations: Money for relatives, charitable contributions.

Investment activities: Foreign securities, bank deposits, and real estate.

Support for relatives: Regular support for family members abroad.

The basic documentation includes a valid passport and PAN (Permanent Account Number). These are mandatory for all LRS transactions and verify your identity and tax status.

Form A2 is the standard application form for retail outward remittances. You'll need to complete this accurately, specifying the purpose of your transfer, recipient details, and source of funds.

Here are the essential documents you'll typically need:

Valid passport: Required as primary identity proof for foreign exchange transactions.

Depending on your transfer amount and purpose, you might also need additional documentation. For larger remittances, a chartered accountant's certificate (Form 15CB) is typically required to confirm tax compliance.

Supporting documents vary by purpose:

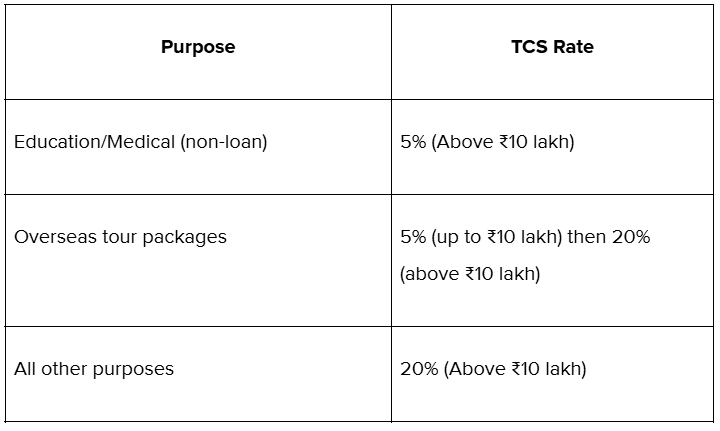

Tax Collected at Source (TCS) applies to outward remittances under LRS. The current threshold is ₹10 lakh (approximately $12,000) per financial year. Amounts below this threshold don't attract TCS.

TCS rates vary depending on the purpose of your transfer:

For education and medical expenses not financed by loans, the rate is 5% on amounts exceeding ₹10 lakh. For overseas tour packages, it's 5% on the first ₹10 lakh above the threshold, then 20% on higher amounts.

For all other purposes, including investments, gifts, and general business remittances, the TCS rate is 20% on amounts exceeding ₹10 lakh. This collected tax can be claimed as a refund when filing your income tax return if you have sufficient tax liability.

Banks are the most traditional option for sending money abroad. All major Indian banks offer international transfer services through wire transfers, demand drafts, or online platforms. They handle compliance and documentation, but often charge higher fees.

Another option includes authorized foreign exchange dealers, providing competitive rates and specialized services. These licensed entities often offer better exchange rates than banks and more personalized service for regular customers.

Also, online money transfer platforms have gained popularity for their convenience and transparency. Licensed platforms provide real-time tracking, competitive rates, and simplified documentation processes while ensuring full regulatory compliance.

Consider the transfer amount, urgency, and recipient location when choosing your method. For large amounts or first-time transfers, banks provide additional security and extensive documentation support.

Here's what to evaluate when selecting your transfer method:

Check the provider's licensing status with authorized entities. Only licensed services can facilitate outward remittances under LRS, and using unlicensed services can result in penalties and transaction failures.

International transfer rules don't have to be complicated. While knowing regulations is important, you also need a reliable partner who handles compliance seamlessly while offering competitive rates and excellent service.

PayGlocal specializes in helping Indian businesses and individuals send money abroad within regulatory frameworks. Our platform combines regulatory expertise with modern technology to make international transfers straightforward and cost-effective.

Here’s how PayGlocal can help you:

Whether you're a freelancer receiving international payments, running an export business, or making business payments overseas, PayGlocal ensures your transfers are compliant, cost-effective, and hassle-free.

The rules for sending money abroad from India are designed to ensure transparency and prevent misuse while allowing legitimate international transfers. Knowing the $250,000 annual limit, required documentation, and tax implications helps you plan transfers effectively.

Choosing the right transfer method depends on your specific needs, but compliance should never be compromised. Working with authorized, reliable service providers ensures your money reaches its destination safely while meeting all regulatory requirements.

Ready to manage all your global payments in one platform? PayGlocal makes international transfers simple, compliant, and cost-effective.

Get started with PayGlocal today and experience faster international payment processes.

The Liberalized Remittance Scheme (LRS) sets clear guidelines for how much money you can transfer, what purposes are allowed, and what taxes apply. Getting this right helps you avoid penalties and ensure your money reaches its destination smoothly.

In this guide, we break down everything you need to know about sending funds abroad from India. Find out the exact limits, required documents, tax implications, and how to choose the right transfer method for your needs.

Key takeaways:

- Annual limit of $250,000: Indian residents can send up to $250,000 per financial year under LRS for permitted purposes.

- Required documentation: You need a PAN card, passport, and Form A2 for most international transfers.

Tax implications: TCS applies to amounts above ₹10 lakh, with rates varying from 5% to 20% based on purpose.

- Global payment solution: With PayGlocal, you can access multi-currency accounts and global payment methods with transparent pricing and payment status tracking.

- Permitted purposes only: Transfers are allowed only for education, medical expenses, travel, gifts, and investment activities.

What are the rules for sending money abroad from India?

The rules for sending money abroad from India are governed by the Liberalized Remittance Scheme (LRS). This framework allows resident individuals to send money overseas for specific permitted purposes without requiring prior approval from authorities.

Under LRS, you can send up to $250,000 per financial year (April to March) for various current and capital account transactions. This limit includes the transfer amount plus all associated fees, charges, and foreign exchange conversion costs.

For example, if you're a freelancer receiving payments from a US client and need to pay for software licenses abroad, all costs, including the payment amount, transfer charges, and currency conversion fees, count toward your annual $250,000 limit. The scheme covers most legitimate business and personal needs, including service payments, business expenses, travel costs, and professional fees.

Who can send money abroad under these rules?

Only resident individuals, as per the Foreign Exchange Management Act (FEMA) can use the LRS. This includes Indian citizens, people of Indian origin, and foreign nationals residing in India for more than 182 days in the preceding financial year.

Some examples of who qualifies and can send money abroad include:

For instance, a freelance graphic designer who's an Indian citizen can use LRS to pay for Adobe subscriptions or send money to international contractors. Similarly, an export business owner can use their personal LRS limit for business-related international payments like attending conferences or purchasing software.

It’s worth noting that Non-Resident Indians (NRIs) follow different rules and have separate regulations for sending money abroad. They can use their NRE or NRO accounts with different limits and documentation requirements based on their account type and residency status.

Minors can also send money abroad, but only through their legal guardians who complete the necessary documentation. The guardian must provide additional proof of their relationship with the minor.

More importantly, LRS is not available to entities such as corporations, partnership firms, or trusts. These entities must follow different regulations for outward remittances based on their specific business needs and transaction purposes.

What purposes are allowed for international transfers?

LRS permits money transfers for specific purposes only. Here are the key permitted purposes:

Business expenses: Software licenses, subscription fees, contractor payments.

Education expenses: Tuition, accommodation, books, and living costs.

Medical treatment: Hospital bills, treatment costs, travel for medical care.

Travel and tourism: Holiday expenses, business travel, emergency costs.

Gifts and donations: Money for relatives, charitable contributions.

Investment activities: Foreign securities, bank deposits, and real estate.

Support for relatives: Regular support for family members abroad.

What documents do you need to send money abroad?

The basic documentation includes a valid passport and PAN (Permanent Account Number). These are mandatory for all LRS transactions and verify your identity and tax status.

Form A2 is the standard application form for retail outward remittances. You'll need to complete this accurately, specifying the purpose of your transfer, recipient details, and source of funds.

Here are the essential documents you'll typically need:

- PAN card: Mandatory for all international transfers to verify your tax identification.

Valid passport: Required as primary identity proof for foreign exchange transactions.

- Form A2: Standard application form declaring transfer purpose and recipient details.

- Bank statements: Recent statements showing the source of funds for the transfer amount.

- Form 15CA: Self-declaration form required for certain transfer amounts and purposes.

- Form 15CB: A chartered accountant certificate is needed for larger transfers or specific purposes.

Depending on your transfer amount and purpose, you might also need additional documentation. For larger remittances, a chartered accountant's certificate (Form 15CB) is typically required to confirm tax compliance.

Supporting documents vary by purpose:

- Business expenses: Invoice, contract, service agreement.

- Education: Admission letter, fee receipt, and course details.

- Medical: Doctor's recommendation, hospital estimates, treatment plan.

- Investment: Portfolio statements, investment declarations.

- Travel: Visa, ticket bookings, hotel confirmations.

- Gift: Relationship proof, recipient identification.

What are the tax implications when sending money abroad?

Tax Collected at Source (TCS) applies to outward remittances under LRS. The current threshold is ₹10 lakh (approximately $12,000) per financial year. Amounts below this threshold don't attract TCS.

TCS rates vary depending on the purpose of your transfer:

For education and medical expenses not financed by loans, the rate is 5% on amounts exceeding ₹10 lakh. For overseas tour packages, it's 5% on the first ₹10 lakh above the threshold, then 20% on higher amounts.

For all other purposes, including investments, gifts, and general business remittances, the TCS rate is 20% on amounts exceeding ₹10 lakh. This collected tax can be claimed as a refund when filing your income tax return if you have sufficient tax liability.

How can you send money abroad?

Banks are the most traditional option for sending money abroad. All major Indian banks offer international transfer services through wire transfers, demand drafts, or online platforms. They handle compliance and documentation, but often charge higher fees.

Another option includes authorized foreign exchange dealers, providing competitive rates and specialized services. These licensed entities often offer better exchange rates than banks and more personalized service for regular customers.

Also, online money transfer platforms have gained popularity for their convenience and transparency. Licensed platforms provide real-time tracking, competitive rates, and simplified documentation processes while ensuring full regulatory compliance.

How do you choose the right transfer method?

Consider the transfer amount, urgency, and recipient location when choosing your method. For large amounts or first-time transfers, banks provide additional security and extensive documentation support.

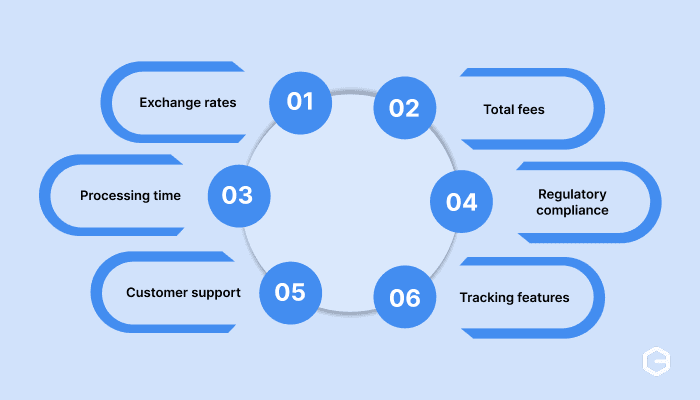

Here's what to evaluate when selecting your transfer method:

- Exchange rates: Compare real-time rates across providers for the best value.

- Total fees: Include transfer charges, conversion fees, and receiving costs.

- Processing time: Match urgency with provider capabilities.

- Regulatory compliance: Ensure proper licensing and documentation support.

- Customer support: Access to help when you need assistance.

- Tracking features: Real-time updates on transfer status.

Check the provider's licensing status with authorized entities. Only licensed services can facilitate outward remittances under LRS, and using unlicensed services can result in penalties and transaction failures.

Manage international payments easily with PayGlocal

International transfer rules don't have to be complicated. While knowing regulations is important, you also need a reliable partner who handles compliance seamlessly while offering competitive rates and excellent service.

PayGlocal specializes in helping Indian businesses and individuals send money abroad within regulatory frameworks. Our platform combines regulatory expertise with modern technology to make international transfers straightforward and cost-effective.

Here’s how PayGlocal can help you:

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD while staying compliant with regulations.

- Transparent pricing: No hidden fees with a clear breakdown of all costs upfront.

- Global payment methods: Accept payments from 180+ countries with local payment options.

- Real-time tracking: Monitor your transfer status at every step with instant notifications.

- One platform management: Handle all international payments from a single dashboard.

Whether you're a freelancer receiving international payments, running an export business, or making business payments overseas, PayGlocal ensures your transfers are compliant, cost-effective, and hassle-free.

Final thoughts

The rules for sending money abroad from India are designed to ensure transparency and prevent misuse while allowing legitimate international transfers. Knowing the $250,000 annual limit, required documentation, and tax implications helps you plan transfers effectively.

Choosing the right transfer method depends on your specific needs, but compliance should never be compromised. Working with authorized, reliable service providers ensures your money reaches its destination safely while meeting all regulatory requirements.

Ready to manage all your global payments in one platform? PayGlocal makes international transfers simple, compliant, and cost-effective.

Get started with PayGlocal today and experience faster international payment processes.