The way people send and receive money keeps changing. According to recent data, India recorded over 18,000 crore digital payment transactions in 2024-25, reflecting a major shift toward digital financial services. This growth in digital payments has created new expectations for speed and convenience in all types of money transfers, including international ones.

An international money order is a prepaid payment method that lets you send money to another country without a bank account. It works like a secure check that the recipient can cash at their local bank or post office. While popular for decades, the process involves paperwork, waiting periods, and limited tracking.

In this guide, we break down everything about international money orders and how they work. Let’s get started.

International money order: It is a prepaid financial instrument that allows you to securely send money to recipients in other countries.

How it works: You purchase the money order from providers like India Post, Western Union, or MoneyGram by paying the amount plus fees upfront.

Processing time: Delivery typically takes 7-15 business days, depending on the destination country and local processing times.

For businesses: If you're receiving payments regularly from international clients, digital payment solutions provide better speed, lower costs, and automatic compliance documentation.

Global payment solution: Modern platforms like PayGlocal offer faster transfers, transparent pricing, real-time tracking, and direct account settlement for accepting international payments.

An international money order is a secure payment method that allows you to send money to recipients in other countries. It functions like a prepaid check issued by a financial institution or postal service.

The sender pays the full amount plus service fees upfront. The money order is then sent to the recipient, who can cash it at their local bank, post office, or designated payment center. Unlike regular checks, money orders are guaranteed because the funds are prepaid.

International money orders are commonly used for personal remittances, paying bills abroad, or sending money when bank transfers aren't convenient. For example, if you need to send money to family in the Philippines, you can purchase an international money order from India Post, and your recipient can cash it at their local bank.

However, they come with limitations. Processing takes several days, tracking is often limited, and fees can add up. For businesses that receive regular international payments, modern payment alternatives offer greater speed.

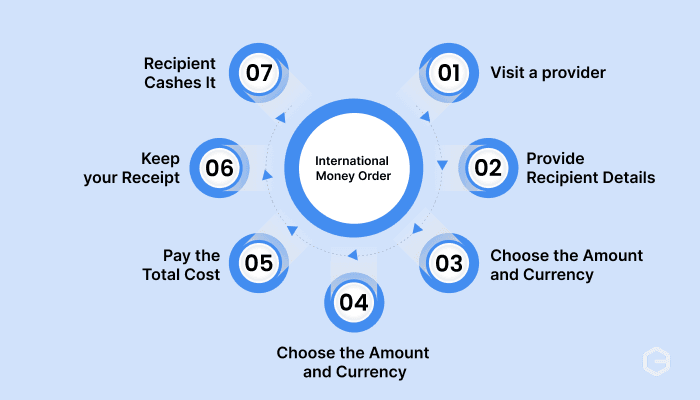

Sending an international money order is straightforward, though it requires visiting a physical location and completing some paperwork. Here's how the process typically works:

Visit a provider: Go to India Post, a bank, or a money transfer service like Western Union that offers international money orders.

Provide recipient details: You'll need the recipient's full name, address, and sometimes additional identification or contact information.

Choose the amount and currency: Specify how much you want to send. The provider will show you the exchange rate and total fees.

Complete the forms: Fill out the required paperwork with accurate information. Any errors can delay the process or cause the money order to be rejected.

Pay the total cost: This includes the money order value plus service fees and any currency conversion charges.

Keep your receipt: You'll receive a receipt with tracking information. Store this safely as proof of payment.

Recipient cashes it: The recipient receives the money order by mail or picks it up. They present it at their bank or post office along with valid identification to receive the funds.

The entire process can take 7-15 business days from purchase to the recipient receiving the money, depending on the destination country and local processing systems.

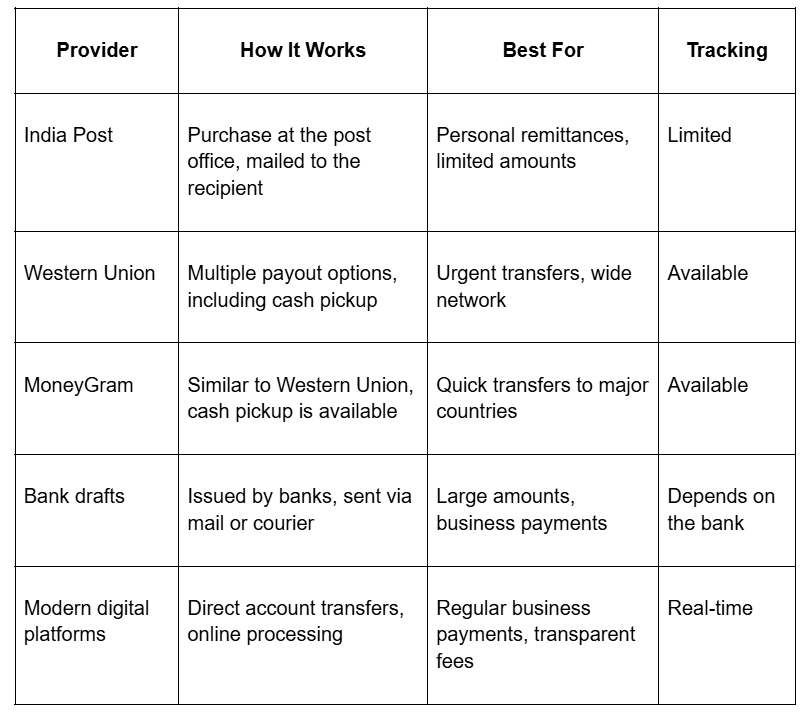

Different providers offer international money order services with varying features, costs, and delivery networks. Here's a quick comparison of the main options:

Each option has different use cases depending on your needs.

1. India Post international money orders

India Post offers international money orders for personal remittances to select countries. You visit your local post office, fill out the required forms, pay the amount plus fees, and the money order is mailed to the recipient.

The service is available to limited destinations and has a transfer limit per money order. Processing typically takes 10-15 business days. For instance, if you're sending money to support a family in Canada, India Post provides a simple option.

2. Western Union and MoneyGram

These global money transfer companies offer international money orders with faster processing and wider networks. Recipients can often collect cash at a wide range of agent locations instead of waiting for mail delivery.

Fees vary based on the amount sent, destination country, and payout method. While faster, costs can be higher.

3. Bank drafts and wire transfers

Banks issue demand drafts for international payments or process SWIFT wire transfers. These are better suited for larger amounts or business transactions.

Bank drafts must be physically mailed to the recipient, taking 7-10 days. Wire transfers are electronic and arrive in 1-3 business days, but come with higher fees, often $20-$50 per transaction plus exchange rate margins.

4. Digital payment platforms

Modern platforms like PayGlocal have changed how businesses and freelancers handle international payments. Instead of physical money orders, you receive payments directly into multi-currency accounts.

These platforms offer transparent pricing, real-time tracking, automatic compliance documents, and settlement in your preferred currency. For example, a freelancer receiving payments from US clients can collect in USD and settle in INR without paperwork or delays.

Sending an international money order through India Post requires a few specific steps and documents. Here’s how it works:

1. Locate your nearest post office: Find a post office that offers international money order services. Not all branches provide this service.

2. Bring required documents: Carry your valid ID proof (Aadhaar, PAN card, passport), the recipient's complete address and name, and the exact amount you want to send.

3. Fill out the application form: Complete the international money order form with accurate recipient details. Double-check spelling and address information.

4. Pay the amount and fees: The total cost includes the transfer amount, service charges, and any currency conversion fees. India Post charges vary by destination.

5. Verify transfer limits: India Post allows a maximum of ₹50,000 per international money order. For larger amounts, you'll need multiple transactions or alternative methods.

6. Get your receipt and tracking number: Keep the receipt safe. It contains the tracking number and serves as proof of payment.

7. Wait for confirmation: The money order is processed and mailed to the recipient. Delivery takes 10-15 business days, depending on the destination country.

The process works well for occasional personal transfers but becomes impractical for regular business payments or when speed matters.

Receiving an international money order in India is simpler than sending one, but still requires visiting a bank or post office. Here's what you need to do:

1. Wait for notification: You'll typically receive a notification when the money order arrives at your local post office or designated bank.

2. Visit the location: Go to the post office or bank with valid identification documents (passport, Aadhaar card, or other government-issued ID).

3. Present the money order: Show the money order along with your ID proof. The teller will verify your identity and the money order details.

4. Sign and collect: Sign the money order in the designated space. The funds will be paid to you in cash or deposited into your account, depending on the amount and local policies.

5. Keep records: Retain the receipt and any documentation for your records, especially if the payment is for business purposes.

International money orders served their purpose for decades, but they come with significant limitations in the current fast-paced business environment. Some of the common challenges include:

Slow processing: Waiting 7-15 days for funds to clear makes cash flow planning difficult for businesses.

Limited tracking: Once sent, tracking is minimal. You often can't confirm if the recipient received payment until they contact you.

Low transfer limits: India Post's ₹50,000 cap means multiple transactions for larger payments, multiplying fees and delays.

High total costs: Between service fees, currency conversion margins, and opportunity costs from delays, the real cost is often 4-6% of the transfer amount.

Paperwork burden: Every transaction requires physical forms, making it impractical for businesses with regular international payments.

No digital records: Physical receipts and money orders make accounting and tax compliance more difficult.

Currency restrictions: Limited currency options and poor exchange rates reduce the amount your recipient actually receives.

Risk of loss: Physical money orders can be lost in the mail, requiring a lengthy replacement process.

For businesses receiving payments from international clients, these challenges directly impact revenue and customer experience. Slow payments mean delayed project starts. Poor tracking creates confusion. High fees reduce profit margins.

International money orders work for occasional personal transfers, but they can't support a growing business. If you're a freelancer, exporter, or business receiving regular international payments, you need a solution built for speed, transparency, and scale.

PayGlocal helps you collect payments from global customers and settle in INR without the delays, paperwork, or hidden costs of traditional money orders.

Here's how PayGlocal solves your international payment challenges:

Multi-currency accounts: Collect payments in USD, GBP, EUR, and CAD with local account details.

Card payments: Process international credit and debit cards with excellent approval rates.

Global payment methods: Offer 40+ local payment methods that your international customers prefer and trust.

Recurring payments: Set up subscription billing for ongoing services with automated collections.

One platform: Manage all your international payments from a single dashboard with transparent reporting and instant notifications.

PayGlocal helps you get paid faster, track every transaction clearly, and maintain complete compliance without the hassle. Whether you're billing a client in New York or receiving marketplace payouts from Europe, your payments arrive on time and in your preferred currency.

International money orders still serve a purpose for occasional personal remittances when you need a prepaid payment method. They offer security and work in situations where digital alternatives aren't available.

But for businesses and freelancers dealing with regular international transactions, traditional money orders come with their own set of challenges.

Modern solutions like PayGlocal give you the speed, transparency, and control you need to manage international payments confidently. Your clients get a smooth payment experience, and you get funds faster with complete visibility.

Get started with PayGlocal today and start managing your international payment processes easily from one platform.

An international money order is a prepaid payment method that lets you send money to another country without a bank account. It works like a secure check that the recipient can cash at their local bank or post office. While popular for decades, the process involves paperwork, waiting periods, and limited tracking.

In this guide, we break down everything about international money orders and how they work. Let’s get started.

Key takeaways

International money order: It is a prepaid financial instrument that allows you to securely send money to recipients in other countries.

How it works: You purchase the money order from providers like India Post, Western Union, or MoneyGram by paying the amount plus fees upfront.

Processing time: Delivery typically takes 7-15 business days, depending on the destination country and local processing times.

For businesses: If you're receiving payments regularly from international clients, digital payment solutions provide better speed, lower costs, and automatic compliance documentation.

Global payment solution: Modern platforms like PayGlocal offer faster transfers, transparent pricing, real-time tracking, and direct account settlement for accepting international payments.

What is an international money order?

An international money order is a secure payment method that allows you to send money to recipients in other countries. It functions like a prepaid check issued by a financial institution or postal service.

The sender pays the full amount plus service fees upfront. The money order is then sent to the recipient, who can cash it at their local bank, post office, or designated payment center. Unlike regular checks, money orders are guaranteed because the funds are prepaid.

International money orders are commonly used for personal remittances, paying bills abroad, or sending money when bank transfers aren't convenient. For example, if you need to send money to family in the Philippines, you can purchase an international money order from India Post, and your recipient can cash it at their local bank.

However, they come with limitations. Processing takes several days, tracking is often limited, and fees can add up. For businesses that receive regular international payments, modern payment alternatives offer greater speed.

How does an international money order work?

Sending an international money order is straightforward, though it requires visiting a physical location and completing some paperwork. Here's how the process typically works:

Visit a provider: Go to India Post, a bank, or a money transfer service like Western Union that offers international money orders.

Provide recipient details: You'll need the recipient's full name, address, and sometimes additional identification or contact information.

Choose the amount and currency: Specify how much you want to send. The provider will show you the exchange rate and total fees.

Complete the forms: Fill out the required paperwork with accurate information. Any errors can delay the process or cause the money order to be rejected.

Pay the total cost: This includes the money order value plus service fees and any currency conversion charges.

Keep your receipt: You'll receive a receipt with tracking information. Store this safely as proof of payment.

Recipient cashes it: The recipient receives the money order by mail or picks it up. They present it at their bank or post office along with valid identification to receive the funds.

The entire process can take 7-15 business days from purchase to the recipient receiving the money, depending on the destination country and local processing systems.

What are the types of international money order services?

Different providers offer international money order services with varying features, costs, and delivery networks. Here's a quick comparison of the main options:

Each option has different use cases depending on your needs.

1. India Post international money orders

India Post offers international money orders for personal remittances to select countries. You visit your local post office, fill out the required forms, pay the amount plus fees, and the money order is mailed to the recipient.

The service is available to limited destinations and has a transfer limit per money order. Processing typically takes 10-15 business days. For instance, if you're sending money to support a family in Canada, India Post provides a simple option.

2. Western Union and MoneyGram

These global money transfer companies offer international money orders with faster processing and wider networks. Recipients can often collect cash at a wide range of agent locations instead of waiting for mail delivery.

Fees vary based on the amount sent, destination country, and payout method. While faster, costs can be higher.

3. Bank drafts and wire transfers

Banks issue demand drafts for international payments or process SWIFT wire transfers. These are better suited for larger amounts or business transactions.

Bank drafts must be physically mailed to the recipient, taking 7-10 days. Wire transfers are electronic and arrive in 1-3 business days, but come with higher fees, often $20-$50 per transaction plus exchange rate margins.

4. Digital payment platforms

Modern platforms like PayGlocal have changed how businesses and freelancers handle international payments. Instead of physical money orders, you receive payments directly into multi-currency accounts.

These platforms offer transparent pricing, real-time tracking, automatic compliance documents, and settlement in your preferred currency. For example, a freelancer receiving payments from US clients can collect in USD and settle in INR without paperwork or delays.

How to send an international money order from India?

Sending an international money order through India Post requires a few specific steps and documents. Here’s how it works:

1. Locate your nearest post office: Find a post office that offers international money order services. Not all branches provide this service.

2. Bring required documents: Carry your valid ID proof (Aadhaar, PAN card, passport), the recipient's complete address and name, and the exact amount you want to send.

3. Fill out the application form: Complete the international money order form with accurate recipient details. Double-check spelling and address information.

4. Pay the amount and fees: The total cost includes the transfer amount, service charges, and any currency conversion fees. India Post charges vary by destination.

5. Verify transfer limits: India Post allows a maximum of ₹50,000 per international money order. For larger amounts, you'll need multiple transactions or alternative methods.

6. Get your receipt and tracking number: Keep the receipt safe. It contains the tracking number and serves as proof of payment.

7. Wait for confirmation: The money order is processed and mailed to the recipient. Delivery takes 10-15 business days, depending on the destination country.

The process works well for occasional personal transfers but becomes impractical for regular business payments or when speed matters.

How to receive an international money order in India?

Receiving an international money order in India is simpler than sending one, but still requires visiting a bank or post office. Here's what you need to do:

1. Wait for notification: You'll typically receive a notification when the money order arrives at your local post office or designated bank.

2. Visit the location: Go to the post office or bank with valid identification documents (passport, Aadhaar card, or other government-issued ID).

3. Present the money order: Show the money order along with your ID proof. The teller will verify your identity and the money order details.

4. Sign and collect: Sign the money order in the designated space. The funds will be paid to you in cash or deposited into your account, depending on the amount and local policies.

5. Keep records: Retain the receipt and any documentation for your records, especially if the payment is for business purposes.

What are the challenges with international money orders?

International money orders served their purpose for decades, but they come with significant limitations in the current fast-paced business environment. Some of the common challenges include:

Slow processing: Waiting 7-15 days for funds to clear makes cash flow planning difficult for businesses.

Limited tracking: Once sent, tracking is minimal. You often can't confirm if the recipient received payment until they contact you.

Low transfer limits: India Post's ₹50,000 cap means multiple transactions for larger payments, multiplying fees and delays.

High total costs: Between service fees, currency conversion margins, and opportunity costs from delays, the real cost is often 4-6% of the transfer amount.

Paperwork burden: Every transaction requires physical forms, making it impractical for businesses with regular international payments.

No digital records: Physical receipts and money orders make accounting and tax compliance more difficult.

Currency restrictions: Limited currency options and poor exchange rates reduce the amount your recipient actually receives.

Risk of loss: Physical money orders can be lost in the mail, requiring a lengthy replacement process.

For businesses receiving payments from international clients, these challenges directly impact revenue and customer experience. Slow payments mean delayed project starts. Poor tracking creates confusion. High fees reduce profit margins.

Accept international payments faster with PayGlocal

International money orders work for occasional personal transfers, but they can't support a growing business. If you're a freelancer, exporter, or business receiving regular international payments, you need a solution built for speed, transparency, and scale.

PayGlocal helps you collect payments from global customers and settle in INR without the delays, paperwork, or hidden costs of traditional money orders.

Here's how PayGlocal solves your international payment challenges:

Multi-currency accounts: Collect payments in USD, GBP, EUR, and CAD with local account details.

Card payments: Process international credit and debit cards with excellent approval rates.

Global payment methods: Offer 40+ local payment methods that your international customers prefer and trust.

Recurring payments: Set up subscription billing for ongoing services with automated collections.

One platform: Manage all your international payments from a single dashboard with transparent reporting and instant notifications.

PayGlocal helps you get paid faster, track every transaction clearly, and maintain complete compliance without the hassle. Whether you're billing a client in New York or receiving marketplace payouts from Europe, your payments arrive on time and in your preferred currency.

Final thoughts

International money orders still serve a purpose for occasional personal remittances when you need a prepaid payment method. They offer security and work in situations where digital alternatives aren't available.

But for businesses and freelancers dealing with regular international transactions, traditional money orders come with their own set of challenges.

Modern solutions like PayGlocal give you the speed, transparency, and control you need to manage international payments confidently. Your clients get a smooth payment experience, and you get funds faster with complete visibility.

Get started with PayGlocal today and start managing your international payment processes easily from one platform.