India’s digital payment growth has been significant in recent years. Data shows that over the last 6 financial years, there have been more than 65,000 crore digital transactions. In fact, 49% of all worldwide real-time transactions happened in India.

If you've ever sent money internationally or received digital payments from overseas clients, you've probably also come across the term SWIFT. So, what exactly does SWIFT stand for, and how does it impact your business transactions?

In this guide, we break down everything you need to know about SWIFT, from its full form to how it works, along with an effective global payment solution. Let’s get started!

SWIFT stands for Society for Worldwide Interbank Financial Telecommunications. It's a global messaging network that banks use to communicate securely when processing international money transfers.

Let’s say you’re sending money from your bank in India to a supplier in the US. The SWIFT system carries secure messages between these banks with all the transaction details.

For example, if you're a freelancer receiving payment from a US client, your client's bank uses SWIFT to send a message to HDFC Bank in India with details like the amount, your account information, and transfer instructions. HDFC Bank then credits your account based on these SWIFT messages.

SWIFT was established in 1973 by 239 banks from 15 countries to replace the Telex system that banks were using for international communications. Before SWIFT, banks relied on different methods to send payment instructions across borders.

The cooperative officially launched its services in 1977, processing 10 million messages in its first year. By the 1980s, SWIFT had expanded globally and introduced standardized messaging formats that banks use today.

SWIFT has continued to evolve with enhanced security measures and expanded membership. Today, SWIFT processes over 42 million messages daily, connecting financial institutions worldwide and facilitating trillions of dollars in international transactions.

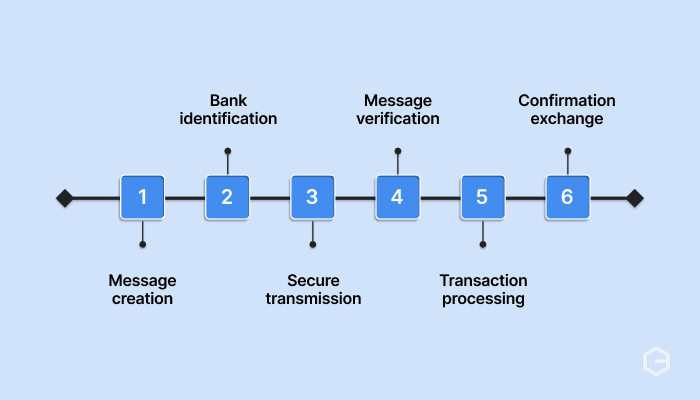

SWIFT operates through a secure network that processes millions of financial messages daily. Here's how the entire process works step by step:

1. Message creation: Your bank creates a detailed message with your transaction information, including the amount, recipient details, and transfer instructions.

2. Bank identification: Your bank uses the recipient bank's SWIFT code to make sure the message goes to the correct financial institution.

3. Secure transmission: The message travels through SWIFT's protected network, keeping all transaction details safe from unauthorized access.

4. Message verification: The receiving bank gets the SWIFT message and checks all the details to make sure everything is correct.

5. Transaction processing: The receiving bank processes the payment according to the instructions in the SWIFT message.

6. Confirmation exchange: Both banks send confirmation messages back and forth through SWIFT to complete the transaction record.

SWIFT codes are unique identifiers that help banks locate each other in the global financial network. These codes contain either 8 or 11 characters and follow a specific format.

In a SWIFT code, the first four characters identify the specific bank, followed by two characters showing which country the bank operates in. The next two characters indicate the region, and a three-character branch code specifies a particular branch.

For instance, in the SWIFT code example format HDFCINBBABC, HDFC is the bank code, IN indicates India, BB represents the location code, and ABC denotes the specific branch details.

SWIFT transfer times vary significantly based on several factors, but most international transfers take 1-5 business days to complete. Several factors affect how quickly your SWIFT transfer processes:

Weekend and holiday delays: Banks don't process transfers on non-business days.

SWIFT transfer fees typically include multiple charges that add up quickly. Different types of fees apply at various stages of the SWIFT transfer process:

For instance, sending $10,000 from India to the US might cost ₹1,500 in sending fees, $25 in intermediary charges, $15 in receiving fees, plus 3% currency markup, totaling over $400 in various charges.

These fees make SWIFT transfers expensive for regular business use, especially for smaller amounts, where charges can represent 5-10% of the transfer value.

SWIFT is owned by its member financial institutions as a cooperative society. No single bank or government controls SWIFT. Instead, it operates under the collective ownership of over 2,400 financial organizations and shareholders worldwide.

The organization is headquartered in Belgium and governed by a 25-member Board of Directors representing different regions and types of financial institutions.

While SWIFT operates independently, it must comply with regulations from multiple jurisdictions, including the guidelines of the US, EU, and other major economies. This cooperative structure means no single entity can unilaterally control SWIFT's operations or policies.

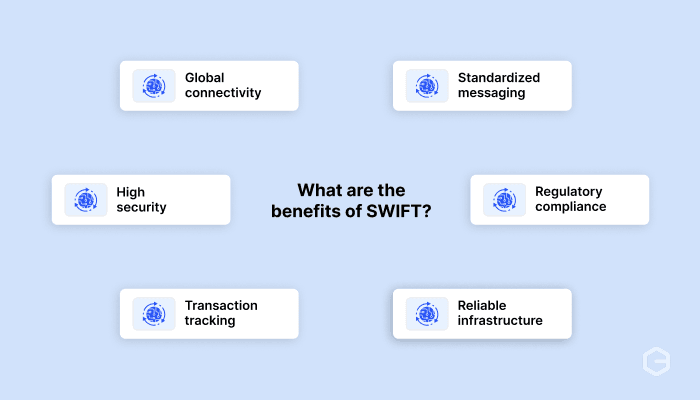

SWIFT offers several advantages for international banking. The system provides a reliable infrastructure that enables global financial communications with high security standards. Here are SWIFT's main benefits:

SWIFT serves various participants in the global financial ecosystem. Different types of organizations rely on SWIFT for different purposes. Here's how different entities use SWIFT:

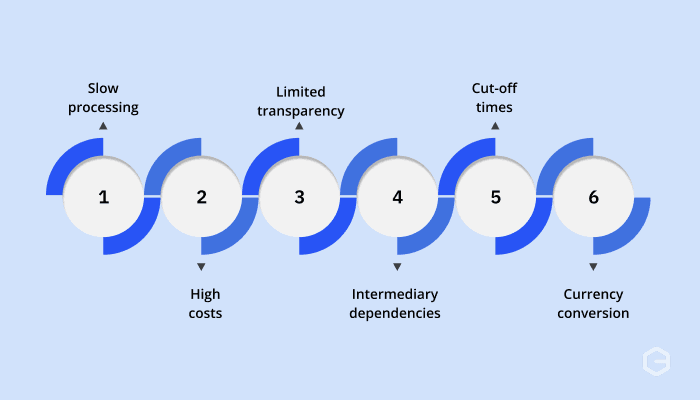

Despite its global reach, SWIFT has several limitations that affect businesses. SWIFT's main limitations include:

SWIFT works for traditional banking, but modern businesses need payment solutions that match their pace and transparency requirements. If you're handling international transactions regularly, relying solely on SWIFT can slow down your operations and eat into your profits.

PayGlocal offers a complete payment processing platform that offers facilities like multi-currency payment collection and transparent pricing with faster payment settlements. Here’s how PayGlocal can help you:

PayGlocal combines global connectivity with modern speed, transparency, and user experience that growing businesses need to scale globally.

While SWIFT enables global financial communication, its limitations around speed, cost, and transparency can be limiting for modern business operations.

For businesses that prioritize efficiency and customer experience, modern payment platforms offer significant advantages over traditional SWIFT-based transfers. PayGlocal provides the global reach you need with the speed and transparency your business deserves.

Ready to collect international payments faster with better rates? Get started with PayGlocal today and experience the difference modern payment infrastructure can make for your business.

If you've ever sent money internationally or received digital payments from overseas clients, you've probably also come across the term SWIFT. So, what exactly does SWIFT stand for, and how does it impact your business transactions?

In this guide, we break down everything you need to know about SWIFT, from its full form to how it works, along with an effective global payment solution. Let’s get started!

Key Takeaways:

- SWIFT full form: Society for Worldwide Interbank Financial Telecommunications - the global messaging network for banks.

- Payment transfer processing: Most international wire transfers use SWIFT codes to reach the right bank.

- SWIFT codes: 8-11 character codes that identify specific banks for international transfers.

- Modern payment solution: PayGlocal offers faster, more transparent international payment solutions with better rates and instant compliance.

What is SWIFT?

SWIFT stands for Society for Worldwide Interbank Financial Telecommunications. It's a global messaging network that banks use to communicate securely when processing international money transfers.

Let’s say you’re sending money from your bank in India to a supplier in the US. The SWIFT system carries secure messages between these banks with all the transaction details.

For example, if you're a freelancer receiving payment from a US client, your client's bank uses SWIFT to send a message to HDFC Bank in India with details like the amount, your account information, and transfer instructions. HDFC Bank then credits your account based on these SWIFT messages.

What is the history of SWIFT?

SWIFT was established in 1973 by 239 banks from 15 countries to replace the Telex system that banks were using for international communications. Before SWIFT, banks relied on different methods to send payment instructions across borders.

The cooperative officially launched its services in 1977, processing 10 million messages in its first year. By the 1980s, SWIFT had expanded globally and introduced standardized messaging formats that banks use today.

SWIFT has continued to evolve with enhanced security measures and expanded membership. Today, SWIFT processes over 42 million messages daily, connecting financial institutions worldwide and facilitating trillions of dollars in international transactions.

How does SWIFT work?

SWIFT operates through a secure network that processes millions of financial messages daily. Here's how the entire process works step by step:

1. Message creation: Your bank creates a detailed message with your transaction information, including the amount, recipient details, and transfer instructions.

2. Bank identification: Your bank uses the recipient bank's SWIFT code to make sure the message goes to the correct financial institution.

3. Secure transmission: The message travels through SWIFT's protected network, keeping all transaction details safe from unauthorized access.

4. Message verification: The receiving bank gets the SWIFT message and checks all the details to make sure everything is correct.

5. Transaction processing: The receiving bank processes the payment according to the instructions in the SWIFT message.

6. Confirmation exchange: Both banks send confirmation messages back and forth through SWIFT to complete the transaction record.

What is the structure of a SWIFT code?

SWIFT codes are unique identifiers that help banks locate each other in the global financial network. These codes contain either 8 or 11 characters and follow a specific format.

In a SWIFT code, the first four characters identify the specific bank, followed by two characters showing which country the bank operates in. The next two characters indicate the region, and a three-character branch code specifies a particular branch.

For instance, in the SWIFT code example format HDFCINBBABC, HDFC is the bank code, IN indicates India, BB represents the location code, and ABC denotes the specific branch details.

How long do SWIFT transfers take?

SWIFT transfer times vary significantly based on several factors, but most international transfers take 1-5 business days to complete. Several factors affect how quickly your SWIFT transfer processes:

- Time zones and banking hours: Banks only process transfers during business hours, creating delays across time zones.

- Intermediary bank requirements: Multiple banks in the transfer chain each add processing time.

- Compliance checks: Sanctions screening and anti-money laundering verification can slow transfers.

- Currency conversion: Converting between currencies adds processing steps.

Weekend and holiday delays: Banks don't process transfers on non-business days.

What are SWIFT transfer fees?

SWIFT transfer fees typically include multiple charges that add up quickly. Different types of fees apply at various stages of the SWIFT transfer process:

- Sending bank fees: Your bank charges ₹500-2,000 for initiating a SWIFT transfer, plus additional fees for urgent processing.

- Intermediary bank charges: Correspondent banks deduct $15-50 from your transfer amount, and you might not know this until after the transaction.

- Receiving bank fees: The destination bank often charges the recipient $10-30 to process incoming SWIFT transfers.

- Currency conversion costs: Banks apply exchange rate markups of 2-4%, which can cost hundreds or thousands on large transfers.

- SWIFT network charges: Banks pay SWIFT directly for message transmission, and they pass these costs to customers.

For instance, sending $10,000 from India to the US might cost ₹1,500 in sending fees, $25 in intermediary charges, $15 in receiving fees, plus 3% currency markup, totaling over $400 in various charges.

These fees make SWIFT transfers expensive for regular business use, especially for smaller amounts, where charges can represent 5-10% of the transfer value.

Who owns the SWIFT banking system?

SWIFT is owned by its member financial institutions as a cooperative society. No single bank or government controls SWIFT. Instead, it operates under the collective ownership of over 2,400 financial organizations and shareholders worldwide.

The organization is headquartered in Belgium and governed by a 25-member Board of Directors representing different regions and types of financial institutions.

While SWIFT operates independently, it must comply with regulations from multiple jurisdictions, including the guidelines of the US, EU, and other major economies. This cooperative structure means no single entity can unilaterally control SWIFT's operations or policies.

What are the benefits of SWIFT

SWIFT offers several advantages for international banking. The system provides a reliable infrastructure that enables global financial communications with high security standards. Here are SWIFT's main benefits:

- Global connectivity: Links over 11,000 financial institutions worldwide, making international transfers possible to virtually any country.

- Standardized messaging: Creates uniform communication protocols that all member banks understand and follow.

- High security: Uses advanced encryption and authentication to protect sensitive financial information during transmission.

- Regulatory compliance: Helps banks meet international compliance requirements and fund processing regulations.

- Transaction tracking: Provides detailed records and tracking capabilities for audit trails and reconciliation.

- Reliable infrastructure: Maintains high uptime with strong systems and disaster recovery capabilities.

Who uses SWIFT payments?

SWIFT serves various participants in the global financial ecosystem. Different types of organizations rely on SWIFT for different purposes. Here's how different entities use SWIFT:

- Commercial banks: Use SWIFT for customer wire transfers, trade finance, and interbank lending. Most international transfers you send or receive go through SWIFT messaging.

- Investment firms: Rely on SWIFT for securities trading, fund transfers between accounts, and settlement of investment transactions across borders.

- Corporations: Use SWIFT indirectly when paying overseas suppliers, receiving payments from international customers, or managing multi-currency accounts.

- Government agencies: Use SWIFT for official payments, foreign aid distributions, and international monetary transactions.

- Small businesses and freelancers: Use SWIFT when clients pay them internationally or when they need to pay foreign vendors and contractors.

What are the challenges with SWIFT?

Despite its global reach, SWIFT has several limitations that affect businesses. SWIFT's main limitations include:

- Slow processing times: SWIFT transfers typically take 1-5 business days to complete, which can disrupt cash flow for time-sensitive transactions.

- High costs: Banks add multiple fees, including SWIFT charges, intermediary bank fees, and currency conversion markups that can total 3-5% of the transfer amount.

- Limited transparency: You often don't know the exact fees upfront, or can't track your payment's status in real-time.

- Intermediary bank dependencies: Many transfers require correspondent banks, adding delays and additional fees you might not expect.

- Cut-off times: Banks have daily cut-off times for SWIFT transfers, meaning late submissions get processed the next business day.

- Currency conversion: Poor exchange rates from banks can significantly impact the final amount received.

Get paid faster globally at affordable rates with PayGlocal

SWIFT works for traditional banking, but modern businesses need payment solutions that match their pace and transparency requirements. If you're handling international transactions regularly, relying solely on SWIFT can slow down your operations and eat into your profits.

PayGlocal offers a complete payment processing platform that offers facilities like multi-currency payment collection and transparent pricing with faster payment settlements. Here’s how PayGlocal can help you:

- Multi-currency collection: Accept payments in 33+ currencies from 180+ countries without waiting for slow SWIFT processing.

- Local payment methods: Offer 40+ global payment methods, including cards, digital wallets, and regional preferences your customers trust.

- Instant compliance: Get automatic FIRC (Foreign Inward Remittance Certificate) documentation without manual paperwork or delays.

- Real-time tracking: Monitor every payment with transparent status updates and notifications throughout the process.

- Competitive rates: Pay only per transaction with clear, transparent pricing and no hidden fees or monthly charges.

PayGlocal combines global connectivity with modern speed, transparency, and user experience that growing businesses need to scale globally.

Final thoughts

While SWIFT enables global financial communication, its limitations around speed, cost, and transparency can be limiting for modern business operations.

For businesses that prioritize efficiency and customer experience, modern payment platforms offer significant advantages over traditional SWIFT-based transfers. PayGlocal provides the global reach you need with the speed and transparency your business deserves.

Ready to collect international payments faster with better rates? Get started with PayGlocal today and experience the difference modern payment infrastructure can make for your business.