In India, card payments are growing rapidly alongside other popular payment methods like UPI. In fact, the latest data shows that there are around 100 million credit cards in India. Majorly because of the cashbacks, benefits, and offers.

But even though card payments power modern business, swipe machine charges can affect a business's profit margins.

Every time a customer swipes their card at your store, you pay fees that range from 1% to 3% of the transaction value.

These charges, known as Merchant Discount Rates (MDR) or swipe fees, are unavoidable costs of accepting card payments. But choosing the right payment partner can help you minimize these costs while expanding your reach globally.

In this guide, we break down everything about swipe machine charges and show you how to make smarter payment decisions for your business.

Swipe machine charges are fees that merchants pay to payment processors when customers use credit or debit cards for transactions. These charges cover the costs of processing payments, fraud prevention, and maintaining secure payment infrastructure.

The primary component is the Merchant Discount Rate (MDR), which is a percentage of each transaction value. For example, if you process a ₹1,000 transaction with a 2% MDR, you pay ₹20 as swipe machine charges.

Card networks like Visa and Mastercard set baseline interchange fees, but your actual charges depend on your payment processor bank, business type, and transaction volume.

Swipe charges are applied automatically every time a customer uses their card at your business. Here's how swipe charges work in practice:

Most merchants focus only on transaction fees, but swipe machine costs include several components that can impact your total profit margins.

Many banks often don’t charge monthly rental fees or have lower rental charges if you maintain high-volume transactions.

Several factors determine the actual rates you pay for card processing, giving you opportunities to negotiate better terms with your provider. Here are the main factors that influence your swipe machine charges:

Smart merchants can significantly lower their payment processing costs through strategic approaches and negotiations.

Traditional payment processors focus on domestic transactions with complex fee structures and hidden charges. Modern businesses need solutions that work globally while keeping costs low.

PayGlocal changes how businesses handle payments by combining competitive rates with powerful international capabilities. Instead of handling multiple providers for local and global payments, you get everything through one clear platform.

Whether you're processing domestic card payments or expanding globally, PayGlocal provides the infrastructure and cost efficiency to grow your business confidently.

Swipe machine charges are an essential cost that modern businesses have to pay to ensure smooth payment processes. But knowing about the fee structure helps you make smarter business decisions. From basic MDR rates of 1% to 3% to additional costs like GST and compliance fees, every component affects your profitability.

Smart merchants focus on negotiating better rates, choosing the right payment mix, and partnering with providers that offer transparency and growth opportunities. PayGlocal offers competitive rates, zero setup fees, and the tools to accept payments from customers worldwide.

Ready to reduce your payment processing costs while expanding globally? Get started with PayGlocal today.

But even though card payments power modern business, swipe machine charges can affect a business's profit margins.

Every time a customer swipes their card at your store, you pay fees that range from 1% to 3% of the transaction value.

These charges, known as Merchant Discount Rates (MDR) or swipe fees, are unavoidable costs of accepting card payments. But choosing the right payment partner can help you minimize these costs while expanding your reach globally.

In this guide, we break down everything about swipe machine charges and show you how to make smarter payment decisions for your business.

Key Takeaways:

- Swipe machine charges typically range from 1% to 3%: Transaction value varies by card type and business volume.

- Different swipe machine fee components: Swipe machine charges include MDR (Merchant Discount Rate), setup costs, and monthly rental charges.

- Smart negotiation and volume discounts: They can significantly reduce your overall payment processing costs.

- Global Payments: PayGlocal offers transparent pricing with no setup fees and competitive international rates for global businesses.

What are swipe machine charges?

Swipe machine charges are fees that merchants pay to payment processors when customers use credit or debit cards for transactions. These charges cover the costs of processing payments, fraud prevention, and maintaining secure payment infrastructure.

The primary component is the Merchant Discount Rate (MDR), which is a percentage of each transaction value. For example, if you process a ₹1,000 transaction with a 2% MDR, you pay ₹20 as swipe machine charges.

Card networks like Visa and Mastercard set baseline interchange fees, but your actual charges depend on your payment processor bank, business type, and transaction volume.

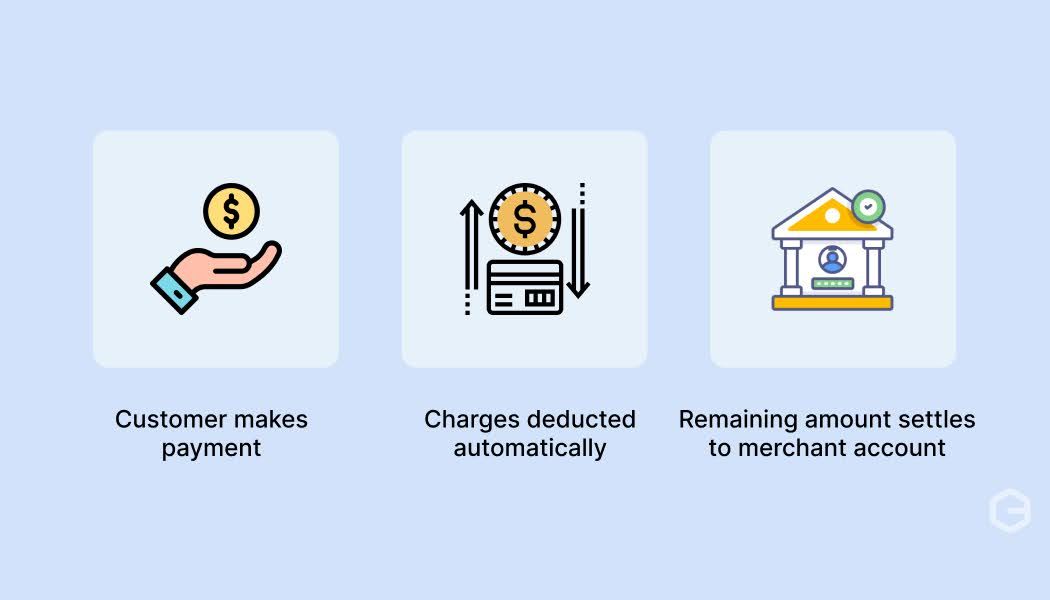

How do swipe machine charges work?

Swipe charges are applied automatically every time a customer uses their card at your business. Here's how swipe charges work in practice:

- Customer makes payment: When a customer swipes or taps their card, the transaction amount goes through your POS machine to the payment processor.

- The merchant pays the charges: If you are a merchant, you will be responsible for paying all swipe charges, not the customer, although some businesses may add convenience fees.

- Automatic deduction system: Swipe charges are deducted automatically from each transaction before the money reaches your bank account within 1-3 business days.

- Multiple parties involved: The charges are split between the bank, card networks like Visa or Mastercard, and payment processors involved in the process.

- Daily settlement process: All transactions from the day are processed together, with net amounts (after deducting charges) credited to your business account.

What are the different types of swipe machine charges?

Most merchants focus only on transaction fees, but swipe machine costs include several components that can impact your total profit margins.

- Security deposit: Ranges from ₹5,000 to ₹15,000 for traditional POS machines.

- Installation charges: Usually ₹500 to ₹1,500 for technician setup and training.

- Monthly rental fees: Monthly fees between ₹300 and ₹800 for maintenance.

- MDR for regular cards (Visa/Mastercard): Typically 1.5% to 2% of transaction value.

- MDR for premium cards (American Express): Typically 2% to 3% of transaction value.

Many banks often don’t charge monthly rental fees or have lower rental charges if you maintain high-volume transactions.

What factors affect swipe machine charges?

Several factors determine the actual rates you pay for card processing, giving you opportunities to negotiate better terms with your provider. Here are the main factors that influence your swipe machine charges:

- Payment processing bank: Different banks set their own rate structures and policies, with charges varying significantly from one bank to another based on their business models.

- Transaction volume: Higher monthly processing volumes typically qualify you for reduced rates, with larger businesses often getting better deals than smaller merchants.

- Card type and network: Visa and Mastercard usually have standard rates, while premium cards like Amex or corporate cards cost more to process than regular debit cards.

- POS machine type: Traditional countertop machines, mobile POS devices, and contactless terminals have different rate structures, with some advanced machines commanding higher fees.

How can you reduce swipe machine charges?

Smart merchants can significantly lower their payment processing costs through strategic approaches and negotiations.

- Negotiate Based on Volume: If you process ₹1 to ₹5 lakhs monthly or more, you have leverage to negotiate lower MDR rates. Present your transaction history and growth projections to payment processors. For high-volume transactions, many banks offer lower rates closer to 1%, which is much lower than the standard rate of 1.5% to 2%.

- Choose the Right Payment Mix: Encourage customers to use lower-cost payment methods like UPI or debit cards when possible.

- Review and Compare Providers: Annual reviews of your payment processor can reveal better options. For instance, switching from a traditional bank to a modern payment platform can reduce costs while adding features like global payment acceptance.

Accept payments globally and reduce costs with PayGlocal

Traditional payment processors focus on domestic transactions with complex fee structures and hidden charges. Modern businesses need solutions that work globally while keeping costs low.

PayGlocal changes how businesses handle payments by combining competitive rates with powerful international capabilities. Instead of handling multiple providers for local and global payments, you get everything through one clear platform.

- Zero setup fees: Start accepting payments immediately without any monthly fixed rental fees or installation charges typical of traditional POS providers. You pay only when you do transactions.

- Global payment acceptance: Accept payments in 33+ currencies from 180+ countries, expanding your market reach beyond domestic customers.

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD while settling in INR, removing complex currency conversion hassles.

- Instant compliance documentation: Automatic FIRC generation and compliance paperwork, saving time and reducing regulatory headaches.

- One platform management: Monitor all transactions, domestic and international, through a single dashboard with real-time tracking and notifications.

Whether you're processing domestic card payments or expanding globally, PayGlocal provides the infrastructure and cost efficiency to grow your business confidently.

Final thoughts

Swipe machine charges are an essential cost that modern businesses have to pay to ensure smooth payment processes. But knowing about the fee structure helps you make smarter business decisions. From basic MDR rates of 1% to 3% to additional costs like GST and compliance fees, every component affects your profitability.

Smart merchants focus on negotiating better rates, choosing the right payment mix, and partnering with providers that offer transparency and growth opportunities. PayGlocal offers competitive rates, zero setup fees, and the tools to accept payments from customers worldwide.

Ready to reduce your payment processing costs while expanding globally? Get started with PayGlocal today.