Trying to figure out if the 2D payment gateway fits your business? According to recent data, digital payment transactions jumped from 2,071 crore in FY 2017-18 to 18,737 crore in FY 2023-24, growing at a rate of 44% annually. This growth indicates more businesses are accepting online payments, and customers expect smooth, secure checkout experiences everywhere.

As you set up payment acceptance for your business, you come across 2D payment gateways that are faster and simpler to use. But they can also be riskier. So what exactly is it, and how does it work?

In this guide, we break down 2D payment gateways in detail, including their benefits and their challenges. Plus, we’ll also cover how they compare to 3D gateways so that you can choose the right solution for your business. Let’s get into it.

A 2D payment gateway is a payment processing system that authenticates online transactions using two layers of information: card details and CVV code. The term "2D" refers to these two dimensions of verification.

When a customer makes a payment through a 2D gateway, they enter their card number, expiration date, and CVV. Once the gateway verifies these details with the issuing bank, the transaction is approved. There's no additional step like entering an OTP or completing biometric authentication.

For example, if you're buying a subscription service online and you only need to enter your card information to complete the purchase, you're likely using a 2D payment gateway. The process is quick because there's no waiting for SMS codes or app notifications.

This simplicity is why some businesses prefer 2D gateways. However, the lack of additional authentication also means the merchant assumes more responsibility if fraud occurs. The issuing bank has less assurance that the real cardholder made the purchase, which can lead to disputes and chargebacks.

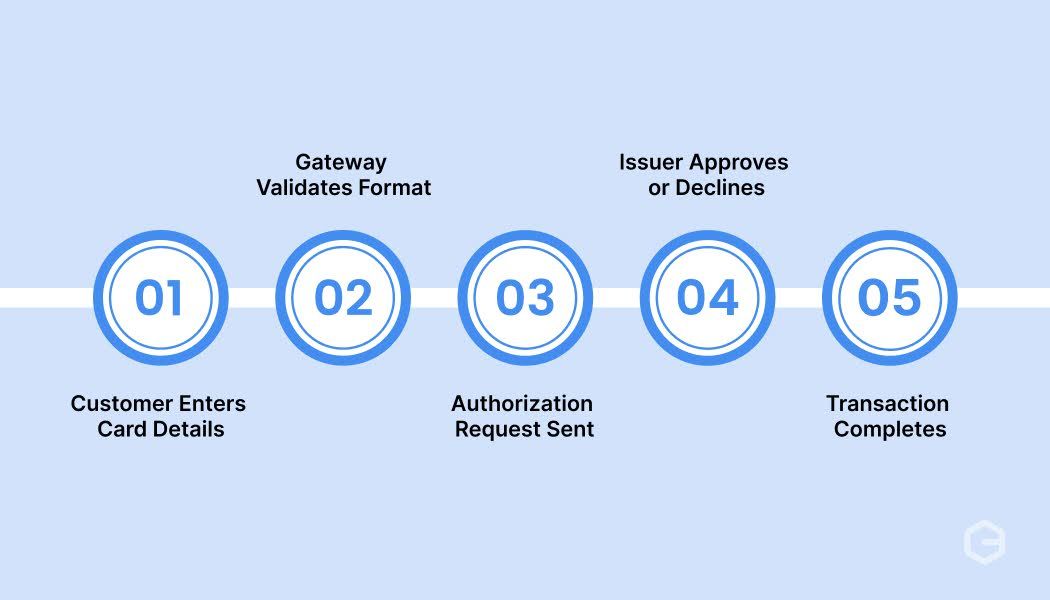

A 2D payment gateway follows a basic flow that prioritizes speed over layered security checks. Here's how the process works:

The entire process happens in seconds. Since there's no pause for OTP entry or fingerprint verification, checkout feels instant. However, this speed comes at a cost. Without strong customer authentication, the merchant bears full liability if the transaction turns out to be fraudulent.

2D payment gateways offer specific advantages that make them appealing in certain scenarios. Some of the benefits they offer include:

While these benefits are real, they only apply in specific situations. For most businesses dealing with high-value transactions or international customers, the risks outweigh the speed gains.

The simplicity of 2D gateways comes with notable downsides that businesses need to weigh carefully.

Choosing the right gateway depends on your business model, target market, transaction value, and risk tolerance. Here's how to think through the decision.

For instance, a small e-commerce store selling within India might initially consider a 2D gateway for speed. But if they plan to expand to international markets or scale their operations, they'll quickly hit limits and need to upgrade to a more secure solution.

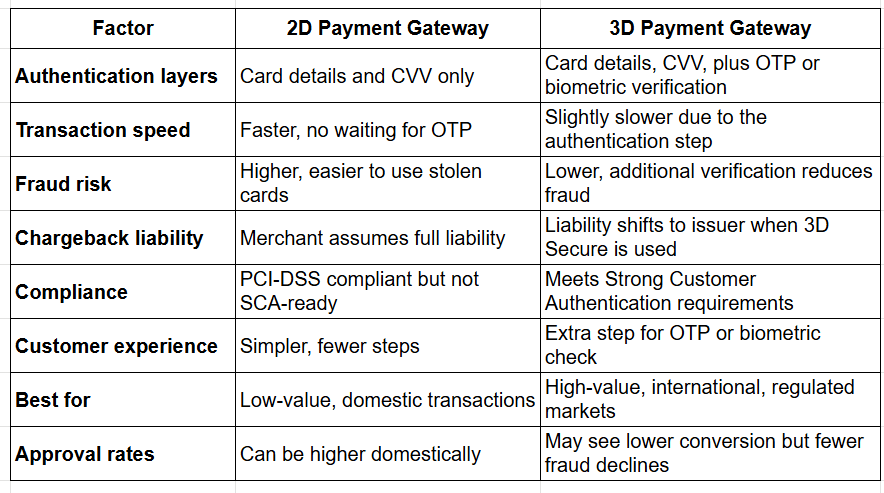

The main difference is in how each gateway verifies the customer's identity during a transaction. Here's a complete breakdown of how they compare:

The important thing is knowing which model fits your customer base and growth plans. If you're building for scale and want to accept payments from anywhere, 3D Secure is the safer, more future-proof choice.

2D payment gateways can seem appealing because of their simplicity, but they create friction when you're dealing with international customers, regulatory compliance, or fraud risk. You need an advanced payment solution that can efficiently handle international payments while meeting all security requirements and maintaining speed.

PayGlocal is specifically built for businesses that want to scale globally and want a secure payment solution. Whether you're a SaaS company, exporter, or e-commerce brand, PayGlocal helps you collect payments from 180+ countries with the reliability and compliance modern businesses demand.

Here's what you get:

PayGlocal helps you accept payments confidently, scale globally, and avoid the trade-offs that come with outdated gateway models. You get security, speed, and support designed for businesses that are serious about growth.

2D payment gateways offer speed and simplicity, but they come with higher risk, chargeback liability, and limited compliance for international markets. The better approach is choosing a payment platform that gives you security, compliance, and global reach without forcing compromises.

Modern payment solutions handle authentication intelligently while keeping checkout smooth and conversions high. If you're serious about accepting international payments and scaling your business, don't settle for outdated models. Choose a platform built for growth, compliance, and customer trust.

Get started with PayGlocal today and start accepting global payments with better speed and security.

As you set up payment acceptance for your business, you come across 2D payment gateways that are faster and simpler to use. But they can also be riskier. So what exactly is it, and how does it work?

In this guide, we break down 2D payment gateways in detail, including their benefits and their challenges. Plus, we’ll also cover how they compare to 3D gateways so that you can choose the right solution for your business. Let’s get into it.

Key takeaways

- What it processes: A 2D payment gateway authenticates transactions using card details and CVV only, without OTP or additional security steps.

- Speed advantage: Checkout is faster because customers don't wait for OTP verification, which can reduce cart abandonment.

- Security concerns: Without extra authentication layers, 2D gateways carry a higher fraud risk and chargeback liability for merchants.

- Use case fit: Works for low-value transactions, certain markets with low fraud rates, or businesses prioritizing speed over security.

- Global payment solution: Modern payment platforms like PayGlocal combine security, speed, and global reach without forcing you to choose between safety and convenience.

What is a 2D payment gateway?

A 2D payment gateway is a payment processing system that authenticates online transactions using two layers of information: card details and CVV code. The term "2D" refers to these two dimensions of verification.

When a customer makes a payment through a 2D gateway, they enter their card number, expiration date, and CVV. Once the gateway verifies these details with the issuing bank, the transaction is approved. There's no additional step like entering an OTP or completing biometric authentication.

For example, if you're buying a subscription service online and you only need to enter your card information to complete the purchase, you're likely using a 2D payment gateway. The process is quick because there's no waiting for SMS codes or app notifications.

This simplicity is why some businesses prefer 2D gateways. However, the lack of additional authentication also means the merchant assumes more responsibility if fraud occurs. The issuing bank has less assurance that the real cardholder made the purchase, which can lead to disputes and chargebacks.

How does a 2D payment gateway work?

A 2D payment gateway follows a basic flow that prioritizes speed over layered security checks. Here's how the process works:

- Customer enters card details: The buyer provides their card number, expiry date, and CVV at checkout.

- Gateway validates format: The payment gateway checks if the card details are formatted correctly and match the card network rules.

- Authorization request sent: The gateway sends the transaction details to the card issuer for approval.

- Issuer approves or declines: The bank verifies if the card is valid, has sufficient funds, and isn't flagged for fraud. If everything checks out, it approves the transaction.

- Transaction completes: The gateway confirms the payment, and the merchant receives the funds after settlement.

The entire process happens in seconds. Since there's no pause for OTP entry or fingerprint verification, checkout feels instant. However, this speed comes at a cost. Without strong customer authentication, the merchant bears full liability if the transaction turns out to be fraudulent.

What are the benefits of 2D payment gateways?

2D payment gateways offer specific advantages that make them appealing in certain scenarios. Some of the benefits they offer include:

- Faster checkout experience: Customers complete payments in seconds without waiting for OTP messages or authentication prompts. This reduces friction and keeps the buying process smooth.

- Lower cart abandonment: The fewer steps a customer has to take, the less likely they are to leave before paying. For impulse purchases or low-value transactions, speed can directly impact conversion rates.

- Simpler integration: 2D gateways often require less complex setup compared to 3D Secure systems. Businesses can get up and running faster without extensive technical configuration.

- Better for repeat customers: If you're charging returning customers who trust your platform, a streamlined process feels more convenient and keeps them engaged.

- Works in low-risk environments: In markets or industries with historically low fraud rates, the trade-off between speed and security can make sense.

While these benefits are real, they only apply in specific situations. For most businesses dealing with high-value transactions or international customers, the risks outweigh the speed gains.

What are the risks of 2D payment gateways?

The simplicity of 2D gateways comes with notable downsides that businesses need to weigh carefully.

- Higher fraud exposure: Without OTP or biometric checks, stolen card details can be used more easily. The merchant has no way to verify that the person entering the card is the actual cardholder.

- Chargeback liability falls on you: When fraud happens on a 2D gateway, the merchant is responsible for the loss. Unlike 3D Secure, there's no liability shift to the card issuer, which means you absorb the cost of fraudulent transactions.

- Compliance challenges: While 2D gateways can be PCI-DSS compliant, they don't meet the Strong Customer Authentication requirements mandated in regions like Europe. This limits where you can operate.

- Lower trust for high-value sales: Customers making expensive purchases often expect extra security steps. A 2D gateway might feel too casual for transactions involving significant amounts.

- Issuer declines: Some card issuers automatically decline transactions that don't include 3D Secure authentication, especially for international payments. This can hurt your success rates.

How do you choose between 2D and 3D payment gateways?

Choosing the right gateway depends on your business model, target market, transaction value, and risk tolerance. Here's how to think through the decision.

- Your industry and transaction type: If you're selling low-value digital goods or services where speed matters most, a 2D gateway might work. For high-value purchases, physical goods, or subscription services, 3D Secure is safer and often required.

- Where your customers are located: International transactions, especially in Europe, require 3D Secure authentication by law. If you're accepting payments from global customers, a 2D gateway will limit your reach and create compliance issues.

- Your fraud risk tolerance: Can you afford to absorb chargebacks and fraud-related losses? If not, 3D Secure offers liability protection that 2D gateways don't. The issuer takes responsibility for fraud when proper authentication is used.

- Conversion rates vs. security: Yes, adding an OTP step can slow checkout and potentially lower conversion slightly. But the trade-off is fewer fraud disputes, chargebacks, and operational headaches. For most businesses, this balance favors security.

- Card issuer requirements: Many banks now require 3D Secure for international card transactions. If you use a 2D gateway, you'll see higher decline rates from issuers who won't approve without additional authentication.

For instance, a small e-commerce store selling within India might initially consider a 2D gateway for speed. But if they plan to expand to international markets or scale their operations, they'll quickly hit limits and need to upgrade to a more secure solution.

What is the difference between 2D and 3D payment gateways?

The main difference is in how each gateway verifies the customer's identity during a transaction. Here's a complete breakdown of how they compare:

The important thing is knowing which model fits your customer base and growth plans. If you're building for scale and want to accept payments from anywhere, 3D Secure is the safer, more future-proof choice.

Accept global payments with strong security and better speed

2D payment gateways can seem appealing because of their simplicity, but they create friction when you're dealing with international customers, regulatory compliance, or fraud risk. You need an advanced payment solution that can efficiently handle international payments while meeting all security requirements and maintaining speed.

PayGlocal is specifically built for businesses that want to scale globally and want a secure payment solution. Whether you're a SaaS company, exporter, or e-commerce brand, PayGlocal helps you collect payments from 180+ countries with the reliability and compliance modern businesses demand.

Here's what you get:

- Multi-Currency Accounts: Collect payments in 33+ currencies and settle in INR, with transparent pricing.

- Sanction Screening: Stay compliant with global regulations through automated sanction screening powered by zero-knowledge-proof technology.

- Global Payment Methods: Go beyond cards and offer 40+ local payment methods your customers trust, increasing conversions across markets.

- One Platform: Manage all your payments, view transaction reports, track fund status, and handle compliance from a single dashboard.

- Instant compliance: Auto-generated FIRC (Foreign Inward remittance Certificate) documents and regulatory compliance built into the platform, so you stay compliant without extra work.

PayGlocal helps you accept payments confidently, scale globally, and avoid the trade-offs that come with outdated gateway models. You get security, speed, and support designed for businesses that are serious about growth.

Final thoughts

2D payment gateways offer speed and simplicity, but they come with higher risk, chargeback liability, and limited compliance for international markets. The better approach is choosing a payment platform that gives you security, compliance, and global reach without forcing compromises.

Modern payment solutions handle authentication intelligently while keeping checkout smooth and conversions high. If you're serious about accepting international payments and scaling your business, don't settle for outdated models. Choose a platform built for growth, compliance, and customer trust.

Get started with PayGlocal today and start accepting global payments with better speed and security.