Ever had a customer drop off just because their preferred payment option wasn’t available? In fact, around 55% of merchants consider this to be the main reason why customers leave their shopping carts, resulting in lost sales.

Multi-channel payments solve this issue by letting you accept payments across all customer touchpoints through one unified system. Instead of managing separate platforms for website cards, email payment links, and mobile wallets, you get complete visibility and control from a single dashboard.

In this guide, we break down how multi-channel payments work and how to set them up without the operational chaos. We also cover the main types, key benefits, and all the steps you need to take to get started effectively.

Multi-channel payments definition: Accept payments from customers across different platforms and methods through one unified system instead of managing separate tools.

Main types: Online payments (cards, net banking), offline payments (POS, QR codes), and mobile payments (UPI, payment links, wallets) serve different customer preferences.

Business benefits: Higher conversion rates, better cash flow, simplified operations, and improved customer experience when payment methods match customer preferences.

PayGlocal simplifies implementation: One platform to accept 40+ payment methods across channels with multi-currency support and instant compliance documentation.

Multi-channel payments allow you to accept money from customers across different platforms and methods while managing everything from one centralized system. Rather than running separate payment systems for your website, mobile app, and offline store, you create a unified approach that handles all transactions seamlessly.

This approach is also known as omnichannel payments when it creates connected experiences across all customer touchpoints. The main difference lies in how integrated the experience becomes for both you and your customers.

For instance, an Indian software exporter might receive payments through credit cards on their website, international money transfers to their USD account, and payment links sent via email. Instead of logging into three different systems to track these payments, multi-channel solutions connect all methods to one dashboard where you can monitor, manage, and match transactions efficiently.

Multi-channel payment systems serve as a central hub, connecting various payment methods and channels to your business account.

Here's how the complete process flows:

Different businesses, customers, and sales flows need different methods. Here's a breakdown of the main types of payment methods involved in the multi-channel payment system:

A unified payment system that supports different methods reduces chaos and gives you more control. With India's e-commerce market growing at 18.29% annually, businesses that offer diverse payment options are better positioned to capture this opportunity.

Some of the top advantages of using multi-channel payments include:

Setting up multi-channel payments requires a systematic approach to ensure all customer touchpoints are covered effectively. Here’s how you can implement multi-channel payments:

Begin by mapping every location where your customers interact with your business, as this foundation determines which payment methods you'll need to support.

For instance, website visitors expect seamless checkout experiences that load quickly and offer familiar payment options, while mobile app users prioritize convenience and want payment processes that work smoothly on smaller screens.

Document each touchpoint carefully, noting current payment limitations and any customer complaints. This in-depth audit reveals gaps where potential customers might abandon purchases due to missing payment options, helping you prioritize which improvements will have the biggest impact on your conversion rates.

Match payment methods strategically to customer preferences and technical capabilities on each specific channel.

For example, online customers typically expect traditional options like credit cards, debit cards, and net banking, but they also appreciate newer methods, such as digital wallets, when available.

On the other hand, mobile users generally prefer faster options such as UPI, digital wallets, and payment apps that integrate with their existing mobile banking habits.

Consider your customer demographics carefully, as international customers often prefer alternate payment methods that are popular in their specific countries. This includes local bank transfer systems, region-specific digital wallets, or country-specific online banking solutions that feel familiar and trustworthy to international buyers.

Evaluate platforms based on their ability to provide centralized dashboard functionality that tracks all transactions regardless of their source. This unified view becomes essential for efficient operations.

Look for providers that offer transparent pricing with zero setup fees and no fixed monthly costs. This reduces your initial investment risk while allowing you to scale payment processing costs with your actual transaction volume.

Additionally, consider the platform's integration complexity and technical requirements, since some providers offer no-code solutions that significantly reduce implementation time.

Start implementation by focusing on your highest-volume channels first. This approach delivers the most immediate impact while allowing you to test the system thoroughly before expanding to additional channels.

Use available APIs, plugins, or no-code tools to integrate your chosen platform with existing systems. However, ensure that you thoroughly test all payment flows before going live with real customers.

Train your team thoroughly on the new dashboard features, so they can handle customer questions confidently and resolve payment issues quickly.

Managing payment collection across multiple channels, currencies, and countries creates operational complexity that slows down your business growth. Most payment platforms require you to manage multiple systems, currencies, and compliance requirements.

PayGlocal solves this challenge with a unified platform designed for Indian businesses selling internationally. Here's what you get:

Whether you sell services, products, or run a digital platform, PayGlocal helps you scale payment collection globally without operational chaos.

Multi-channel payments remove the friction between your customers and their money. When you accept payments the way customers want to pay, conversion rates improve and cash flow accelerates.

To successfully implement a multi-channel payment system, choose a platform that unifies different payment methods without involving technical complexity. Start by auditing your customer touchpoints, then implement payment methods that match customer preferences on each channel.

For Indian businesses selling internationally, handling multiple currencies and compliance requirements adds another layer of complexity. PayGlocal solves these challenges with a unified platform that simplifies multi-channel payment collection globally.

Get started with PayGlocal and see how multi-channel payments can improve your collection efficiency.

Multi-channel payments solve this issue by letting you accept payments across all customer touchpoints through one unified system. Instead of managing separate platforms for website cards, email payment links, and mobile wallets, you get complete visibility and control from a single dashboard.

In this guide, we break down how multi-channel payments work and how to set them up without the operational chaos. We also cover the main types, key benefits, and all the steps you need to take to get started effectively.

Key Takeaways:

Multi-channel payments definition: Accept payments from customers across different platforms and methods through one unified system instead of managing separate tools.

Main types: Online payments (cards, net banking), offline payments (POS, QR codes), and mobile payments (UPI, payment links, wallets) serve different customer preferences.

Business benefits: Higher conversion rates, better cash flow, simplified operations, and improved customer experience when payment methods match customer preferences.

PayGlocal simplifies implementation: One platform to accept 40+ payment methods across channels with multi-currency support and instant compliance documentation.

What are multi-channel payments?

Multi-channel payments allow you to accept money from customers across different platforms and methods while managing everything from one centralized system. Rather than running separate payment systems for your website, mobile app, and offline store, you create a unified approach that handles all transactions seamlessly.

This approach is also known as omnichannel payments when it creates connected experiences across all customer touchpoints. The main difference lies in how integrated the experience becomes for both you and your customers.

For instance, an Indian software exporter might receive payments through credit cards on their website, international money transfers to their USD account, and payment links sent via email. Instead of logging into three different systems to track these payments, multi-channel solutions connect all methods to one dashboard where you can monitor, manage, and match transactions efficiently.

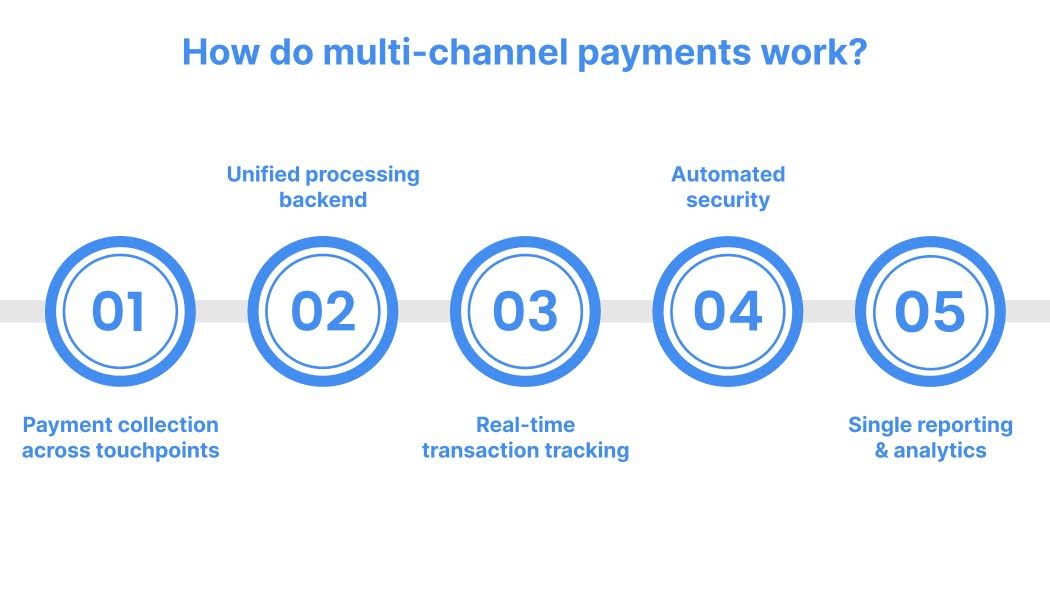

How do multi-channel payments work?

Multi-channel payment systems serve as a central hub, connecting various payment methods and channels to your business account.

Here's how the complete process flows:

- Payment collection across touchpoints: Your customers interact through various channels, including websites, mobile apps, email links, WhatsApp messages, and physical locations, with each channel supporting their preferred payment methods.

- Unified processing backend: All payment requests route through one centralized system that identifies the payment method, applies security protocols, and processes transactions consistently.

- Real-time transaction tracking: Every payment appears instantly in your unified dashboard with complete transaction details, customer information, and settlement timelines.

- Automated security: The system applies the same security standards across all channels, detecting suspicious activity regardless of the payment source.

- Single reporting and analytics: Get comprehensive insights into payment patterns, success rates, and customer preferences across all channels from one centralized location.

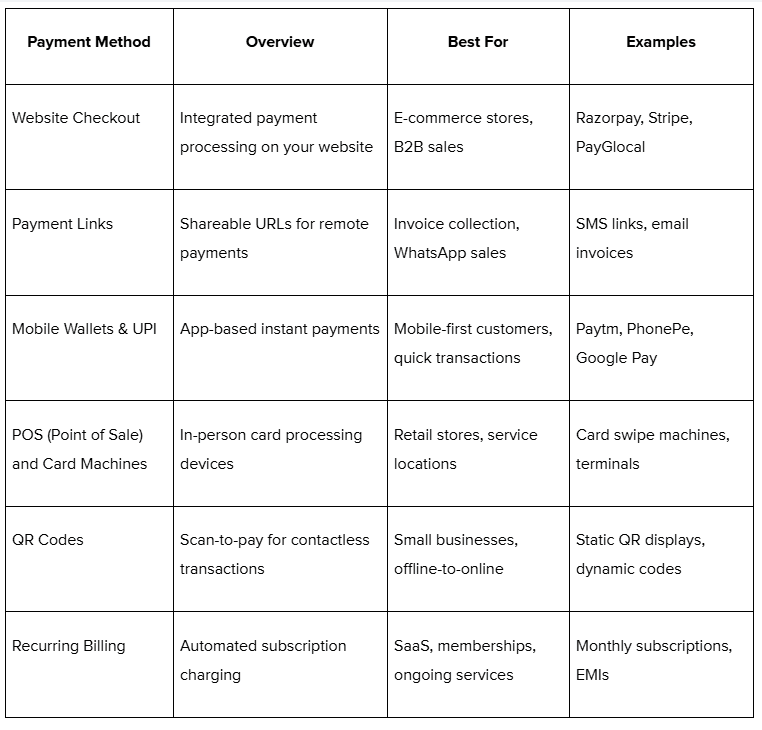

What are the types of payment methods in the multi-channel system?

Different businesses, customers, and sales flows need different methods. Here's a breakdown of the main types of payment methods involved in the multi-channel payment system:

What are the benefits of multi-channel payment solutions?

A unified payment system that supports different methods reduces chaos and gives you more control. With India's e-commerce market growing at 18.29% annually, businesses that offer diverse payment options are better positioned to capture this opportunity.

Some of the top advantages of using multi-channel payments include:

- Increased reach: Capture payments from different customer segments across multiple platforms. Some customers only use cards. Others prefer bank transfers. Mobile users want wallet options.

- Improved cash flow: Faster collections and fewer failed payments mean money reaches your account quicker. Payment transaction processing becomes more efficient when all methods connect to one system.

- Operational simplicity: No need to manually reconcile payments from different systems. Everything is presented on a single dashboard with unified reporting and analytics.

- Customer convenience: People use what they're comfortable with. Let them choose their preferred method instead of forcing them to adapt to your limitations.

- Better analytics: See where payments succeed or fail, and use data to make informed decisions about which channels to prioritize.

- Reduced technical complexity: One integration instead of multiple APIs and systems. Your development team manages fewer moving parts.

How to set up multi-channel payments?

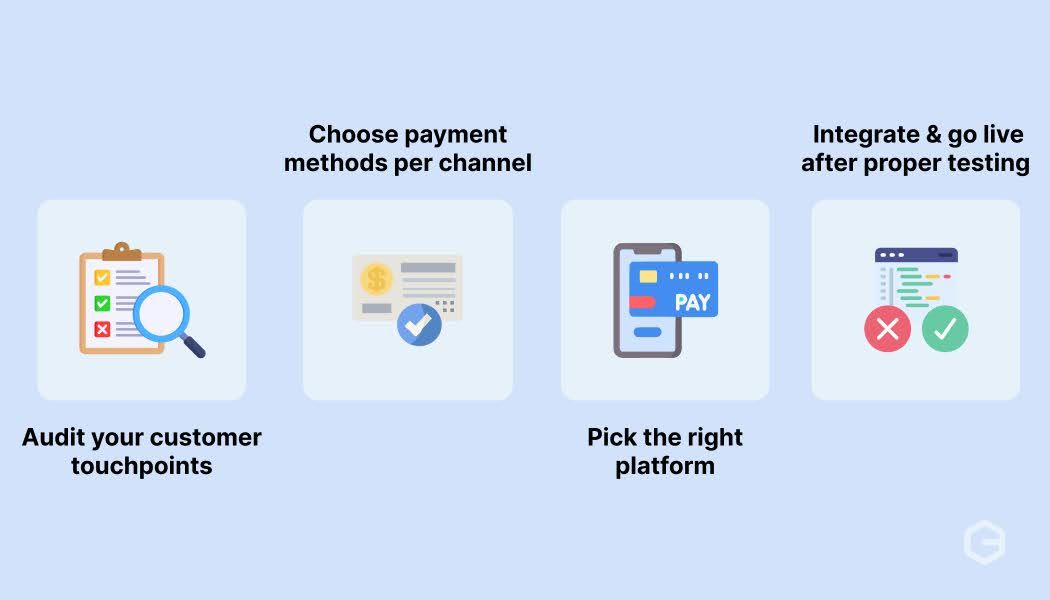

Setting up multi-channel payments requires a systematic approach to ensure all customer touchpoints are covered effectively. Here’s how you can implement multi-channel payments:

Step 1: Audit your customer touchpoints

Begin by mapping every location where your customers interact with your business, as this foundation determines which payment methods you'll need to support.

For instance, website visitors expect seamless checkout experiences that load quickly and offer familiar payment options, while mobile app users prioritize convenience and want payment processes that work smoothly on smaller screens.

Document each touchpoint carefully, noting current payment limitations and any customer complaints. This in-depth audit reveals gaps where potential customers might abandon purchases due to missing payment options, helping you prioritize which improvements will have the biggest impact on your conversion rates.

Step 2: Choose payment methods per channel

Match payment methods strategically to customer preferences and technical capabilities on each specific channel.

For example, online customers typically expect traditional options like credit cards, debit cards, and net banking, but they also appreciate newer methods, such as digital wallets, when available.

On the other hand, mobile users generally prefer faster options such as UPI, digital wallets, and payment apps that integrate with their existing mobile banking habits.

Consider your customer demographics carefully, as international customers often prefer alternate payment methods that are popular in their specific countries. This includes local bank transfer systems, region-specific digital wallets, or country-specific online banking solutions that feel familiar and trustworthy to international buyers.

Step 3: Pick the right platform

Evaluate platforms based on their ability to provide centralized dashboard functionality that tracks all transactions regardless of their source. This unified view becomes essential for efficient operations.

Look for providers that offer transparent pricing with zero setup fees and no fixed monthly costs. This reduces your initial investment risk while allowing you to scale payment processing costs with your actual transaction volume.

Additionally, consider the platform's integration complexity and technical requirements, since some providers offer no-code solutions that significantly reduce implementation time.

Step 4: Integrate and go live after proper testing

Start implementation by focusing on your highest-volume channels first. This approach delivers the most immediate impact while allowing you to test the system thoroughly before expanding to additional channels.

Use available APIs, plugins, or no-code tools to integrate your chosen platform with existing systems. However, ensure that you thoroughly test all payment flows before going live with real customers.

Train your team thoroughly on the new dashboard features, so they can handle customer questions confidently and resolve payment issues quickly.

Scale your payment collection globally with PayGlocal

Managing payment collection across multiple channels, currencies, and countries creates operational complexity that slows down your business growth. Most payment platforms require you to manage multiple systems, currencies, and compliance requirements.

PayGlocal solves this challenge with a unified platform designed for Indian businesses selling internationally. Here's what you get:

- Collect in 33+ currencies: Accept payments from 180+ countries without currency conversion headaches or hidden costs in international payments.

- USD, GBP, EUR, CAD local accounts: Appear local to your global customers with dedicated multi-currency accounts that reduce transaction fees.

- Send payment links, accept cards or bank transfers: One tool handles recurring payments, one-time transactions, and subscription billing.

- No fixed costs: Pay only when you transact, making it perfect for businesses at any scale.

- International payments platform: Manage everything from one dashboard instead of switching between multiple systems.

Whether you sell services, products, or run a digital platform, PayGlocal helps you scale payment collection globally without operational chaos.

Final thoughts

Multi-channel payments remove the friction between your customers and their money. When you accept payments the way customers want to pay, conversion rates improve and cash flow accelerates.

To successfully implement a multi-channel payment system, choose a platform that unifies different payment methods without involving technical complexity. Start by auditing your customer touchpoints, then implement payment methods that match customer preferences on each channel.

For Indian businesses selling internationally, handling multiple currencies and compliance requirements adds another layer of complexity. PayGlocal solves these challenges with a unified platform that simplifies multi-channel payment collection globally.

Get started with PayGlocal and see how multi-channel payments can improve your collection efficiency.