Recent data shows that India recorded over 65,000 crore digital transactions worth more than ₹12,000 lakh crore in the last 6 years alone. P2P transactions drive much of this growth, giving people and businesses a faster alternative to traditional payment methods.

They are quick, convenient, and require nothing more than a smartphone. But what happens when you start using P2P apps for your business? Can they handle client payments, international transfers, and the documentation you need for compliance?

In this guide, we break down what P2P transactions are, how they work, and when you need something more professional for your growing business. Let’s get into it.

P2P transactions, or peer-to-peer transactions, are electronic money transfers made directly from one person to another through a digital platform. The "peer-to-peer" name means you're sending money directly to another individual, not through traditional banking processes.

These transfers happen through P2P payment apps or platforms that act as intermediaries. You link your bank account, debit card, or credit card to the app, then send money to someone else who also uses the same platform. The money moves from your account to theirs, usually within minutes.

For example, you can use Google Pay to split a restaurant bill with friends. You open the app, enter your friend's phone number or UPI ID, type in your share of the bill, and confirm. The money leaves your account and arrives in theirs almost instantly. That's a P2P transaction.

P2P transactions follow a straightforward process that happens mostly in the background. Here's what happens when you send or receive money through a P2P app:

Step 1: Account setup- Both sender and recipient need accounts with the same P2P service. You download the app, create your account, and link a funding source. This could be your bank account, debit card, or credit card. The app verifies your identity and confirms your payment method works.

Step 2: Find the recipient - When you want to send money, you search for the recipient within the app. Most P2P platforms let you find people using their phone number, email address, or username. Some apps, like those using UPI (Unified Payments Interface) in India, let you search by UPI ID or scan a QR code.

Step 3: Enter the amount and confirm - You type in how much money you want to send. Many apps let you add a note explaining what the payment is for. You review the details and confirm the transaction.

Step 4: Funds transfer - The P2P platform processes your transfer. The money moves from your linked account through the platform's system to the recipient's account. Depending on the service, this happens instantly or within a few hours. UPI payments in India are typically instant, while some international P2P services take 1-3 business days.

Step 5: Recipient accesses funds - The recipient gets a notification that money has arrived. They can keep the funds in their app wallet or transfer them to their linked bank account. Some platforms hold the money in the app until the recipient requests a transfer to their bank.

P2P transactions come in several forms, each serving different needs and operating through different mechanisms. Here's what you need to know about each type:

Here's a closer look at each type:

Mobile wallet P2P transfers happen when you send money from your digital wallet to someone else's wallet. Popular examples include Paytm, PhonePe, and Google Pay in India, or Venmo and Cash App internationally.

You load money into your wallet from your bank account, then transfer it to other users. For instance, you can add ₹5,000 to your Paytm wallet, then send ₹500 to a friend who also uses Paytm. The money moves instantly between wallets, and your friend can either keep it in their wallet for future use or transfer it to their bank account.

Some P2P services connect directly to your bank account without using a digital wallet. Zelle in the US works this way, and many banking apps in India now offer similar features.

The transfer happens directly between bank accounts, with the P2P platform acting as a facilitator. For example, if you send money through your bank's app to someone at a different bank, the P2P system handles the routing while the money moves directly from your account to theirs.

UPI (Unified Payments Interface) has become the dominant P2P method in India. Apps like Google Pay, PhonePe, and BHIM all use UPI infrastructure to enable instant transfers.

You create a UPI ID linked to your bank account. When you send money, you enter the recipient's UPI ID or scan their QR code, confirm the amount and transaction, and the transfer completes in seconds. For instance, a freelancer can share their UPI QR code with a client, who scans it and pays immediately.

International P2P transactions let you send money across borders. Services like PayPal and Western Union offer international P2P options.

These work similarly to domestic P2P but involve currency conversion and typically take longer. For example, if you receive payment from a US client through PayPal, the money arrives in USD, gets converted to INR (with PayPal taking a conversion fee), and then settles in your Indian bank account within 2-5 business days.

P2P transactions offer several advantages that explain their popularity, especially for personal use:

Speed and convenience: Most P2P payments complete within minutes, often instantly. You can send money from anywhere using just your phone. No need to visit a bank, write a cheque, or handle cash. For instance, if you need to pay your share of a group dinner, you can transfer the money while still at the restaurant.

Low or no fees for personal use: Many P2P platforms charge nothing for basic transfers between individuals. UPI transactions in India are free for users, and apps like Google Pay don't charge fees for sending money to friends. This makes P2P ideal for splitting bills, paying back borrowed money, or sending small amounts to family.

Easy to start using: Setting up a P2P app takes minutes. You download the app, enter your phone number, link a bank account or card, and you're ready to send money. The process is simpler than opening a bank account or setting up traditional payment systems.

Works for people without credit cards: P2P platforms accept bank accounts and debit cards, so you don't need a credit card to participate. This makes digital payments accessible to more people, including students and those new to banking.

Transparent transactions: Most P2P apps show you exactly how much you're sending, what fees apply (if any), and when the recipient will get the money. You get instant notifications confirming your transaction went through.

However, these benefits apply mainly to personal, small-value transactions. When you start using P2P for business purposes, limitations quickly appear.

P2P platforms work well for personal use, but they create significant challenges when you're running a business:

Transaction limits restrict growth: Most P2P apps limit how much you can send or receive per transaction, per day, or per month. Many apps limit individual transactions to ₹1 lakh, and many platforms cap monthly volumes. When you're invoicing clients for ₹5 lakhs or more, these limits force you to split payments or find workarounds.

Missing business features: P2P apps don't offer professional invoicing, payment tracking, or integration with accounting software. You can't generate proper invoices, track which client paid for which project, or export transaction data for your accounts. For instance, if you're managing payments from 10 different clients, a P2P app gives you a list of transactions but no way to organize them by project or invoice.

No compliance documentation: When you receive international payments, you need a FIRC (Foreign Inward Remittance Certificate) for tax compliance and audits. P2P apps don't provide these documents automatically. You'll spend time requesting documentation from your bank or the platform, often receiving incomplete information.

High international fees: P2P platforms that support international transfers often charge high currency conversion fees and offer poor exchange rates. These costs add up quickly when you're receiving regular payments from international clients.

Irreversible transactions create risk: Most P2P transfers can't be reversed. If you send money to the wrong person, you have almost no chance of getting it back. Unlike credit card payments with chargeback protection, most P2P transactions are final. For businesses, this means one mistake can cost you thousands.

P2P works fine when you're starting out or handling occasional small payments. But as your business grows, you need purpose-built payment infrastructure.

If you're currently using P2P platforms for business payments, here's how to make the process work better:

Create a dedicated business account: Don't mix personal and business transactions. Set up a separate P2P account used only for business. This makes accounting easier and looks more professional to clients.

Track every transaction manually: Since P2P apps don't offer business features, maintain a spreadsheet tracking each payment. Record the date, client name, amount, project or invoice number, and any fees charged.

Send clear payment requests: When requesting payment, include your invoice number and project details in the payment note. This helps you and your client match the payment to the correct invoice.

Set up automatic transfers to your business account: Don't let money pile up in P2P app wallets. Configure automatic transfers to move funds to your business bank account regularly.

Communicate limits to clients upfront: If you're using P2P apps with transaction limits, tell clients about these restrictions before they send large payments. This prevents failed transactions and frustrated clients.

Request confirmation for international payments: When receiving international P2P payments, ask for screenshots or confirmation numbers. You'll need this documentation if issues arise.

However, these payment methods only take you so far. For sustainable business growth, you need a payment solution designed for business use.

P2P apps work for personal transactions and early-stage freelancing, but they can't support serious business growth. When you're collecting payments from international clients or scaling your operations, you need infrastructure built for business.

PayGlocal gives you everything, including professional payment collection tools, compliance documentation, multi-currency support, and transparent pricing. Here's how PayGlocal can help you:

Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries. Get local accounts in USD, GBP, EUR, and CAD so international clients can pay you like a local business.

Instant compliance documentation: Receive your FIRC automatically in your inbox after every settlement. No more chasing documentation for tax compliance or audits.

Zero fixed costs: Pay only when you transact. No setup fees, no platform fees, no documentation charges. Transparent pricing with no surprises.

Recurring payments: Set up subscriptions for clients who pay monthly or annually. Automatic billing with network-compliant international card debits.

Sanction screening: Verify transactions with privacy-first technology to stay compliant with global regulations and protect your business.

PayGlocal helps businesses like yours collect payments professionally while reducing costs and improving payment success rates.

P2P transactions made digital payments accessible to everyone. They're fast, convenient, and perfect for personal use. When you're splitting bills with friends, sending money to family, or making small purchases, P2P apps are great.

But when you're running a business, especially one that collects international payments, P2P platforms fall short. Transaction limits, missing compliance features, high international fees, and a lack of professional tools all create friction that slows your growth.

If you're collecting payments from international clients, managing multiple currencies, or need proper documentation for compliance, it's time to upgrade to a purpose-built payment infrastructure.

Stop working around traditional payment limitations. Switch to a payment platform built for your business needs. Get started with PayGlocal today.

They are quick, convenient, and require nothing more than a smartphone. But what happens when you start using P2P apps for your business? Can they handle client payments, international transfers, and the documentation you need for compliance?

In this guide, we break down what P2P transactions are, how they work, and when you need something more professional for your growing business. Let’s get into it.

Key takeaways

- P2P transactions enable direct money transfers: P2P (Peer-to-Peer) payments let you send money directly to another person through apps like Google Pay, PhonePe, or PayPal without visiting a bank.

- They work through linked accounts: You connect your bank account or card to a P2P app, select a recipient, and transfer funds instantly or within hours.

- Transaction limits can block business growth: Most P2P platforms have daily and monthly limits that restrict how much you can send or receive, creating problems as your business scales.

- International transfers face high fees: Some P2P apps do support international payments, but they often charge high currency conversion fees and offer poor exchange rates.

- Professional payment solutions drive business growth: Platforms like PayGlocal offer multi-currency accounts, compliance documentation, and transparent pricing designed specifically for businesses accepting international payments.

What are P2P transactions?

P2P transactions, or peer-to-peer transactions, are electronic money transfers made directly from one person to another through a digital platform. The "peer-to-peer" name means you're sending money directly to another individual, not through traditional banking processes.

These transfers happen through P2P payment apps or platforms that act as intermediaries. You link your bank account, debit card, or credit card to the app, then send money to someone else who also uses the same platform. The money moves from your account to theirs, usually within minutes.

For example, you can use Google Pay to split a restaurant bill with friends. You open the app, enter your friend's phone number or UPI ID, type in your share of the bill, and confirm. The money leaves your account and arrives in theirs almost instantly. That's a P2P transaction.

How do P2P transactions work?

P2P transactions follow a straightforward process that happens mostly in the background. Here's what happens when you send or receive money through a P2P app:

Step 1: Account setup- Both sender and recipient need accounts with the same P2P service. You download the app, create your account, and link a funding source. This could be your bank account, debit card, or credit card. The app verifies your identity and confirms your payment method works.

Step 2: Find the recipient - When you want to send money, you search for the recipient within the app. Most P2P platforms let you find people using their phone number, email address, or username. Some apps, like those using UPI (Unified Payments Interface) in India, let you search by UPI ID or scan a QR code.

Step 3: Enter the amount and confirm - You type in how much money you want to send. Many apps let you add a note explaining what the payment is for. You review the details and confirm the transaction.

Step 4: Funds transfer - The P2P platform processes your transfer. The money moves from your linked account through the platform's system to the recipient's account. Depending on the service, this happens instantly or within a few hours. UPI payments in India are typically instant, while some international P2P services take 1-3 business days.

Step 5: Recipient accesses funds - The recipient gets a notification that money has arrived. They can keep the funds in their app wallet or transfer them to their linked bank account. Some platforms hold the money in the app until the recipient requests a transfer to their bank.

What are the types of P2P transactions?

P2P transactions come in several forms, each serving different needs and operating through different mechanisms. Here's what you need to know about each type:

Here's a closer look at each type:

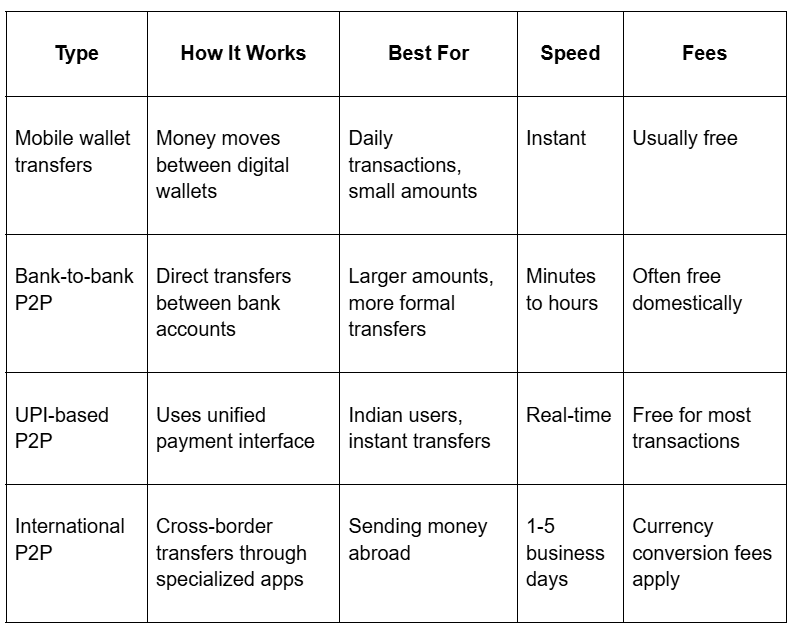

Mobile wallet transfers

Mobile wallet P2P transfers happen when you send money from your digital wallet to someone else's wallet. Popular examples include Paytm, PhonePe, and Google Pay in India, or Venmo and Cash App internationally.

You load money into your wallet from your bank account, then transfer it to other users. For instance, you can add ₹5,000 to your Paytm wallet, then send ₹500 to a friend who also uses Paytm. The money moves instantly between wallets, and your friend can either keep it in their wallet for future use or transfer it to their bank account.

Bank-to-bank P2P

Some P2P services connect directly to your bank account without using a digital wallet. Zelle in the US works this way, and many banking apps in India now offer similar features.

The transfer happens directly between bank accounts, with the P2P platform acting as a facilitator. For example, if you send money through your bank's app to someone at a different bank, the P2P system handles the routing while the money moves directly from your account to theirs.

UPI-based P2P

UPI (Unified Payments Interface) has become the dominant P2P method in India. Apps like Google Pay, PhonePe, and BHIM all use UPI infrastructure to enable instant transfers.

You create a UPI ID linked to your bank account. When you send money, you enter the recipient's UPI ID or scan their QR code, confirm the amount and transaction, and the transfer completes in seconds. For instance, a freelancer can share their UPI QR code with a client, who scans it and pays immediately.

International P2P

International P2P transactions let you send money across borders. Services like PayPal and Western Union offer international P2P options.

These work similarly to domestic P2P but involve currency conversion and typically take longer. For example, if you receive payment from a US client through PayPal, the money arrives in USD, gets converted to INR (with PayPal taking a conversion fee), and then settles in your Indian bank account within 2-5 business days.

What are the benefits of P2P transactions?

P2P transactions offer several advantages that explain their popularity, especially for personal use:

Speed and convenience: Most P2P payments complete within minutes, often instantly. You can send money from anywhere using just your phone. No need to visit a bank, write a cheque, or handle cash. For instance, if you need to pay your share of a group dinner, you can transfer the money while still at the restaurant.

Low or no fees for personal use: Many P2P platforms charge nothing for basic transfers between individuals. UPI transactions in India are free for users, and apps like Google Pay don't charge fees for sending money to friends. This makes P2P ideal for splitting bills, paying back borrowed money, or sending small amounts to family.

Easy to start using: Setting up a P2P app takes minutes. You download the app, enter your phone number, link a bank account or card, and you're ready to send money. The process is simpler than opening a bank account or setting up traditional payment systems.

Works for people without credit cards: P2P platforms accept bank accounts and debit cards, so you don't need a credit card to participate. This makes digital payments accessible to more people, including students and those new to banking.

Transparent transactions: Most P2P apps show you exactly how much you're sending, what fees apply (if any), and when the recipient will get the money. You get instant notifications confirming your transaction went through.

However, these benefits apply mainly to personal, small-value transactions. When you start using P2P for business purposes, limitations quickly appear.

What are the challenges of P2P transactions for businesses?

P2P platforms work well for personal use, but they create significant challenges when you're running a business:

Transaction limits restrict growth: Most P2P apps limit how much you can send or receive per transaction, per day, or per month. Many apps limit individual transactions to ₹1 lakh, and many platforms cap monthly volumes. When you're invoicing clients for ₹5 lakhs or more, these limits force you to split payments or find workarounds.

Missing business features: P2P apps don't offer professional invoicing, payment tracking, or integration with accounting software. You can't generate proper invoices, track which client paid for which project, or export transaction data for your accounts. For instance, if you're managing payments from 10 different clients, a P2P app gives you a list of transactions but no way to organize them by project or invoice.

No compliance documentation: When you receive international payments, you need a FIRC (Foreign Inward Remittance Certificate) for tax compliance and audits. P2P apps don't provide these documents automatically. You'll spend time requesting documentation from your bank or the platform, often receiving incomplete information.

High international fees: P2P platforms that support international transfers often charge high currency conversion fees and offer poor exchange rates. These costs add up quickly when you're receiving regular payments from international clients.

Irreversible transactions create risk: Most P2P transfers can't be reversed. If you send money to the wrong person, you have almost no chance of getting it back. Unlike credit card payments with chargeback protection, most P2P transactions are final. For businesses, this means one mistake can cost you thousands.

P2P works fine when you're starting out or handling occasional small payments. But as your business grows, you need purpose-built payment infrastructure.

How to accept P2P payments for your business?

If you're currently using P2P platforms for business payments, here's how to make the process work better:

Create a dedicated business account: Don't mix personal and business transactions. Set up a separate P2P account used only for business. This makes accounting easier and looks more professional to clients.

Track every transaction manually: Since P2P apps don't offer business features, maintain a spreadsheet tracking each payment. Record the date, client name, amount, project or invoice number, and any fees charged.

Send clear payment requests: When requesting payment, include your invoice number and project details in the payment note. This helps you and your client match the payment to the correct invoice.

Set up automatic transfers to your business account: Don't let money pile up in P2P app wallets. Configure automatic transfers to move funds to your business bank account regularly.

Communicate limits to clients upfront: If you're using P2P apps with transaction limits, tell clients about these restrictions before they send large payments. This prevents failed transactions and frustrated clients.

Request confirmation for international payments: When receiving international P2P payments, ask for screenshots or confirmation numbers. You'll need this documentation if issues arise.

However, these payment methods only take you so far. For sustainable business growth, you need a payment solution designed for business use.

Get paid globally with better speed and security using PayGlocal

P2P apps work for personal transactions and early-stage freelancing, but they can't support serious business growth. When you're collecting payments from international clients or scaling your operations, you need infrastructure built for business.

PayGlocal gives you everything, including professional payment collection tools, compliance documentation, multi-currency support, and transparent pricing. Here's how PayGlocal can help you:

Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries. Get local accounts in USD, GBP, EUR, and CAD so international clients can pay you like a local business.

Instant compliance documentation: Receive your FIRC automatically in your inbox after every settlement. No more chasing documentation for tax compliance or audits.

Zero fixed costs: Pay only when you transact. No setup fees, no platform fees, no documentation charges. Transparent pricing with no surprises.

Recurring payments: Set up subscriptions for clients who pay monthly or annually. Automatic billing with network-compliant international card debits.

Sanction screening: Verify transactions with privacy-first technology to stay compliant with global regulations and protect your business.

PayGlocal helps businesses like yours collect payments professionally while reducing costs and improving payment success rates.

Final thoughts

P2P transactions made digital payments accessible to everyone. They're fast, convenient, and perfect for personal use. When you're splitting bills with friends, sending money to family, or making small purchases, P2P apps are great.

But when you're running a business, especially one that collects international payments, P2P platforms fall short. Transaction limits, missing compliance features, high international fees, and a lack of professional tools all create friction that slows your growth.

If you're collecting payments from international clients, managing multiple currencies, or need proper documentation for compliance, it's time to upgrade to a purpose-built payment infrastructure.

Stop working around traditional payment limitations. Switch to a payment platform built for your business needs. Get started with PayGlocal today.