Starting a business with partners brings together different skills, capital, and ideas. But before you can accept payments or sign contracts, you need to know what structure works best.

A partnership firm is one of the simplest business structures in India. Many exporters, freelancers, and service providers choose this structure when starting out. In fact, partnership firms typically fall under India's Micro, Small, and Medium Enterprises (MSME) sector, which accounts for up to 45% of the country's exports.

In this guide, we cover what partnership firms are, their key features, types, and what you need to consider before forming one. You'll also learn how to set up payments when your partnership business serves global clients.

A partnership firm is a business structure where two or more people agree to own, manage, and share the profits and losses of a business together. Each person contributes capital, skills, or labor and works toward a common goal.

The people involved in this business structure are called partners individually, and together they form the firm. The key element is mutual agreement. Partners decide how to split profits, who handles what responsibilities, and how decisions get made.

For example, two software developers might form a partnership to offer web development services to clients abroad. One partner handles coding while the other manages client relationships and finances. They share profits 60-40 based on their agreement.

You can structure your partnership based on how long you want it to last and what you want to achieve. Each type serves different business goals and comes with its own rules.

Let’s take a detailed look at each type.

This is the most common type. Partners continue the business indefinitely without a fixed end date. The partnership keeps running until partners mutually decide to dissolve it or one partner gives notice to leave.

For example, a design agency formed by three partners operates as long as all partners agree to continue. If one partner wants to exit, they follow the exit terms in the partnership deed.

This partnership is formed for a specific project or limited period. Once the project completes or the time period ends, the partnership automatically dissolves.

For instance, two construction contractors might form a partnership to complete a single building project. After project delivery and profit distribution, the partnership ends.

A Limited Liability Partnership (LLP) combines features of partnerships and companies. Partners have limited liability, meaning personal assets are protected from business debts. Only the amount invested in the LLP is at risk.

LLPs require formal registration and are treated as separate legal entities. Many professional services firms, like consultancies and law firms, choose this structure.

Partnership firms operate differently from other business structures, such as a company or a sole proprietorship. Knowing these key features upfront helps you determine whether this structure matches your business goals.

Every partnership starts with an agreement between partners. This can be written or verbal, though written agreements called partnership deeds are strongly recommended. The deed outlines profit-sharing ratios, capital contributions, roles, and procedures for adding or removing partners.

The main goal is earning and sharing profits. Partners contribute resources and work together, expecting financial returns. Charitable organizations or clubs don't qualify as partnerships because profit isn't their primary objective.

You need at least two people to form a partnership. The maximum depends on the business type. Most partnerships can have up to 50 partners under current regulations.

General partners are personally liable for business debts. If the firm can't pay suppliers or lenders, creditors can claim partners' personal assets. This makes partners careful about financial decisions.

Each partner acts as an agent for the firm and other partners. Actions taken by one partner in business matters bind all partners. For instance, if one partner signs a contract, all partners are bound by it.

The firm isn't a separate legal entity like a company. It can't own property or enter into contracts in its own name. Everything is done in the partners' names.

Starting a partnership requires minimal paperwork compared to a company. There's no mandatory registration. However, registered partnerships get legal benefits like the ability to sue third parties.

The way partners participate in your business can take several forms. Recognizing these different partner types ensures everyone knows their roles and what they're accountable for:

A partnership deed is a written agreement that documents the terms of the partnership. It's a legal document that covers essential details like profit-sharing ratios, partner roles, capital contributions, and procedures for resolving disputes.

While partnerships can be formed with verbal agreements, written deeds prevent misunderstandings. The deed typically includes partner names and addresses, business name and nature, capital contribution by each partner, profit and loss sharing ratio, partner duties and responsibilities, rules for admitting or removing partners, and dispute resolution procedures.

For example, a partnership deed might state that Partner A contributes 60% capital and receives 60% profits, while Partner B contributes 40% and receives 40%. It might also specify that major decisions require unanimous consent.

Having a clear deed protects all partners and provides a reference point when disagreements arise.

Partnerships and companies have different legal structures, liability, and regulatory requirements. Here's how they compare.

Companies exist as separate legal entities that can own property, enter contracts, and sue or be sued independently. Partnership firms don't have this separation. The partners and the firm are legally the same.

Partners face unlimited liability, meaning creditors can claim personal assets if business assets aren't enough to cover debts. Company shareholders only risk the amount they invested in shares.

Companies must register with the Ministry of Corporate Affairs and follow strict compliance requirements. Partnerships have simpler formation and fewer ongoing compliance burdens, though LLPs need registration.

For small businesses and professional services starting out, partnerships offer simplicity. As businesses scale and need external funding or want to limit liability, converting to a company structure often makes sense.

Partnerships offer several benefits for entrepreneurs who want to start quickly without heavy regulations. Some of the top advantages of this structure include:

Every business structure has trade-offs you should consider before committing. These challenges affect how partnerships grow, handle risk, and maintain stability.

Registration gives your partnership formal recognition and makes business operations smoother. The process involves drafting a deed, submitting documents to your state's Registrar of Firms, and obtaining necessary tax registrations.

When your partnership firm starts serving clients in the USA, UK, or Europe, payment collection becomes critical. You need accounts that work in their currencies.

Operating a partnership firm serving international clients means managing cross-border payments. Traditional bank transfers take days, charge high fees, and create paperwork headaches. Your business needs a payment solution built for global trade.

PayGlocal is an all-in-one payment platform designed for partnership businesses expanding globally. Whether you're exporting goods, providing services, or working with overseas clients, PayGlocal simplifies how you collect and manage international payments.

Here's what partnership firms get with PayGlocal:

PayGlocal handles the complexity of international payments so your partnership can focus on serving clients and growing revenue.

A partnership firm offers a simple, flexible way to start a business with others who share your vision. The structure works well for professional services, exporters, and small businesses that want to get started quickly without heavy compliance burdens.

The key to success is choosing the right partners, drafting a clear partnership deed, and maintaining open communication about business decisions and finances. Consider your liability comfort level and growth plans when deciding between a general partnership and an LLP.

As your partnership grows and serves clients across borders, having the right payment infrastructure becomes critical. You need solutions that handle multiple currencies, provide compliance documents automatically, and give you complete visibility into payment status.

Get started with PayGlocal today and start accepting international payments easily in multiple currencies.

A partnership firm is one of the simplest business structures in India. Many exporters, freelancers, and service providers choose this structure when starting out. In fact, partnership firms typically fall under India's Micro, Small, and Medium Enterprises (MSME) sector, which accounts for up to 45% of the country's exports.

In this guide, we cover what partnership firms are, their key features, types, and what you need to consider before forming one. You'll also learn how to set up payments when your partnership business serves global clients.

Key takeaways

- Two or more owners: A partnership firm requires at least two people who agree to run a business together and share profits based on an agreed ratio.

- Simple formation: Starting a partnership is faster and less expensive than forming a private limited company, with minimal regulatory requirements.

- Shared liability: General partners have unlimited liability, meaning personal assets can be used to pay business debts if needed.

- Defined by agreement: The partnership deed defines each partner's role, capital contribution, profit-sharing ratio, and exit terms.

- Global payment needs: Partnership businesses serving international clients need reliable cross-border payment solutions like PayGlocal to collect in multiple currencies and settle in INR.

What is a partnership firm?

A partnership firm is a business structure where two or more people agree to own, manage, and share the profits and losses of a business together. Each person contributes capital, skills, or labor and works toward a common goal.

The people involved in this business structure are called partners individually, and together they form the firm. The key element is mutual agreement. Partners decide how to split profits, who handles what responsibilities, and how decisions get made.

For example, two software developers might form a partnership to offer web development services to clients abroad. One partner handles coding while the other manages client relationships and finances. They share profits 60-40 based on their agreement.

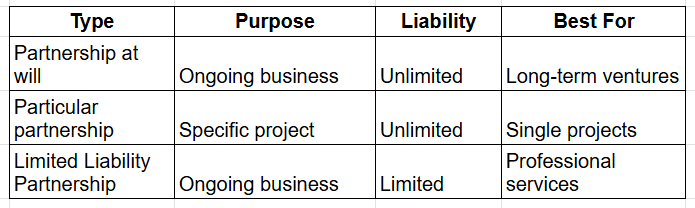

What are the types of partnership firms?

You can structure your partnership based on how long you want it to last and what you want to achieve. Each type serves different business goals and comes with its own rules.

Let’s take a detailed look at each type.

Partnership at will

This is the most common type. Partners continue the business indefinitely without a fixed end date. The partnership keeps running until partners mutually decide to dissolve it or one partner gives notice to leave.

For example, a design agency formed by three partners operates as long as all partners agree to continue. If one partner wants to exit, they follow the exit terms in the partnership deed.

Particular partnership

This partnership is formed for a specific project or limited period. Once the project completes or the time period ends, the partnership automatically dissolves.

For instance, two construction contractors might form a partnership to complete a single building project. After project delivery and profit distribution, the partnership ends.

Limited liability partnership

A Limited Liability Partnership (LLP) combines features of partnerships and companies. Partners have limited liability, meaning personal assets are protected from business debts. Only the amount invested in the LLP is at risk.

LLPs require formal registration and are treated as separate legal entities. Many professional services firms, like consultancies and law firms, choose this structure.

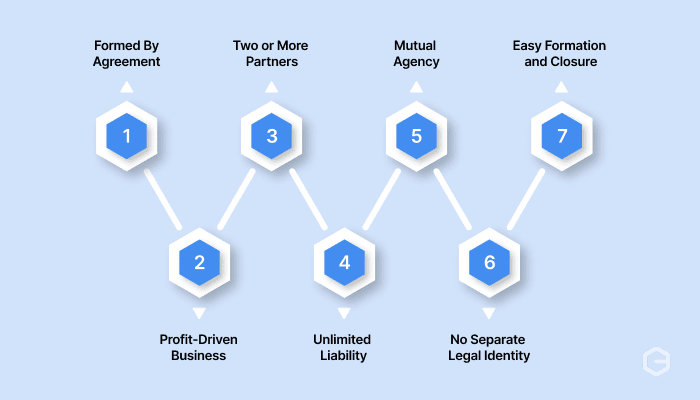

What are the key features of a partnership firm?

Partnership firms operate differently from other business structures, such as a company or a sole proprietorship. Knowing these key features upfront helps you determine whether this structure matches your business goals.

Formed by agreement

Every partnership starts with an agreement between partners. This can be written or verbal, though written agreements called partnership deeds are strongly recommended. The deed outlines profit-sharing ratios, capital contributions, roles, and procedures for adding or removing partners.

Profit-driven business

The main goal is earning and sharing profits. Partners contribute resources and work together, expecting financial returns. Charitable organizations or clubs don't qualify as partnerships because profit isn't their primary objective.

Two or more partners

You need at least two people to form a partnership. The maximum depends on the business type. Most partnerships can have up to 50 partners under current regulations.

Unlimited liability

General partners are personally liable for business debts. If the firm can't pay suppliers or lenders, creditors can claim partners' personal assets. This makes partners careful about financial decisions.

Mutual agency

Each partner acts as an agent for the firm and other partners. Actions taken by one partner in business matters bind all partners. For instance, if one partner signs a contract, all partners are bound by it.

No separate legal identity

The firm isn't a separate legal entity like a company. It can't own property or enter into contracts in its own name. Everything is done in the partners' names.

Easy formation and closure

Starting a partnership requires minimal paperwork compared to a company. There's no mandatory registration. However, registered partnerships get legal benefits like the ability to sue third parties.

What are the types of partners in a partnership firm?

The way partners participate in your business can take several forms. Recognizing these different partner types ensures everyone knows their roles and what they're accountable for:

- Active partner: These partners actively manage day-to-day operations. They make business decisions, interact with clients, and handle transactions. Active partners have unlimited liability and are known to the public as owners.

- Sleeping or dormant partner: These partners invest capital but don't participate in daily management. They share profits and losses but stay in the background. Their liability remains unlimited despite not being actively involved.

- Nominal partner: A nominal partner lends their name and reputation to the firm but doesn't contribute capital or participate in management. They don't share profits or losses. However, they can be held liable to third parties because outsiders believe they're actual partners.

- Partner in profits only: This partner receives a share of profits but isn't liable for losses. This arrangement must be clearly stated in the partnership deed and isn't common because it creates an imbalance in risk-sharing.

- Sub-partner: A sub-partner is someone an existing partner shares their profit with. They have no direct relationship with the firm or other partners. The sub-partner's rights are limited to receiving the agreed profit share from one partner.

- Partner by estoppel: If someone represents themselves as a partner or allows others to believe they're a partner, they can be held liable as one even if they're not actually a partner. This protects third parties who deal with the firm based on that belief.

- Incoming partner: When a new person joins an existing partnership, they're called an incoming partner. They're liable for debts and obligations that arise after they join, not for previous debts unless they explicitly agree.

- Outgoing partner: When a partner leaves, they're called an outgoing partner. They remain liable for debts that existed before their exit unless creditors agree to release them from liability.

What is a partnership deed?

A partnership deed is a written agreement that documents the terms of the partnership. It's a legal document that covers essential details like profit-sharing ratios, partner roles, capital contributions, and procedures for resolving disputes.

While partnerships can be formed with verbal agreements, written deeds prevent misunderstandings. The deed typically includes partner names and addresses, business name and nature, capital contribution by each partner, profit and loss sharing ratio, partner duties and responsibilities, rules for admitting or removing partners, and dispute resolution procedures.

For example, a partnership deed might state that Partner A contributes 60% capital and receives 60% profits, while Partner B contributes 40% and receives 40%. It might also specify that major decisions require unanimous consent.

Having a clear deed protects all partners and provides a reference point when disagreements arise.

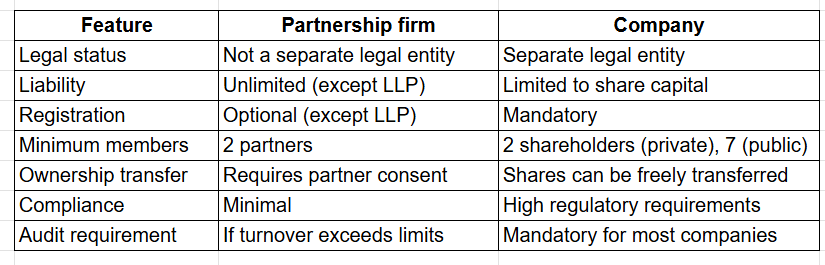

How does a partnership firm differ from a company?

Partnerships and companies have different legal structures, liability, and regulatory requirements. Here's how they compare.

Companies exist as separate legal entities that can own property, enter contracts, and sue or be sued independently. Partnership firms don't have this separation. The partners and the firm are legally the same.

Partners face unlimited liability, meaning creditors can claim personal assets if business assets aren't enough to cover debts. Company shareholders only risk the amount they invested in shares.

Companies must register with the Ministry of Corporate Affairs and follow strict compliance requirements. Partnerships have simpler formation and fewer ongoing compliance burdens, though LLPs need registration.

For small businesses and professional services starting out, partnerships offer simplicity. As businesses scale and need external funding or want to limit liability, converting to a company structure often makes sense.

What are the top benefits of a partnership firm?

Partnerships offer several benefits for entrepreneurs who want to start quickly without heavy regulations. Some of the top advantages of this structure include:

- Easy and quick formation: Setting up a partnership requires minimal paperwork and lower costs compared to companies. You can start operating almost immediately after drafting the partnership deed.

- Shared financial burden: Multiple partners mean shared capital requirements. You don't need to arrange all funding alone. Partners pool resources to cover startup costs and working capital needs.

- Combined expertise: Different partners bring different skills. One might handle operations while another manages finances or marketing. This diversity creates a stronger business foundation.

- Simple decision-making: With fewer people involved than in a large company, decisions happen faster. Partners can quickly respond to market changes or customer needs without lengthy approval processes.

- Flexible profit distribution: Partners can agree on any profit-sharing ratio that makes sense for their contributions. This flexibility lets you structure rewards based on actual value added, not just capital invested.

- Tax benefits: Partnerships often pay lower taxes than companies in certain situations. Partners can also claim deductions for business expenses on their personal tax returns.

- Privacy: Partnership firms have fewer disclosure requirements than companies. You don't need to file public financial statements, keeping your business details private.

- Better credit access: Having multiple partners can improve creditworthiness. Lenders see reduced risk when several people are personally liable for debts.

What are the main challenges of a partnership firm?

Every business structure has trade-offs you should consider before committing. These challenges affect how partnerships grow, handle risk, and maintain stability.

- Unlimited liability: Partners are personally liable for business debts. If the business fails, creditors can claim your house, car, or other personal assets. This puts significant personal risk on partners.

- Shared authority and conflicts: Every partner has a say in decisions. Disagreements can slow down operations or create tension. When partners have different visions, the business suffers.

- Limited capital: Partnerships can only raise funds through partner contributions or loans. You can't issue shares to public investors like companies can. This limits growth potential for capital-intensive businesses.

- Lack of continuity: If a partner wants to exit, the partnership may dissolve unless the deed specifies continuation terms. This instability can worry clients and suppliers.

- Difficulty transferring ownership: You can't simply sell your share like you would company shares. Adding new partners or removing existing ones requires consent from all partners.

- Joint liability: Each partner is liable for actions taken by other partners in business matters. If one partner makes a bad decision, all partners face consequences.

- Less credibility: Some clients and suppliers prefer dealing with companies because they seem more established and permanent. Partnerships might face credibility challenges in competitive markets.

How do you register a partnership firm?

Registration gives your partnership formal recognition and makes business operations smoother. The process involves drafting a deed, submitting documents to your state's Registrar of Firms, and obtaining necessary tax registrations.

- Choose your partners: Decide who will be your partners. Each partner should bring value through capital, skills, or networks. Discuss roles, responsibilities, and expectations upfront.

- Select a firm name: Pick a unique name that's not already registered in your state. Avoid names that resemble existing firms or companies. Check name availability with the Registrar of Firms.

- Draft the partnership deed: Create a comprehensive deed covering all partnership terms. Include capital contributions, profit-sharing ratios, partner responsibilities, decision-making procedures, and exit terms. Get it printed on stamp paper of appropriate value as per your state's requirements.

- Apply for registration: Submit the registration application to the Registrar of Firms in your state. Include the partnership deed, application form, and required fees. Partners may need to provide identity proof and address proof.

- Obtain registration certificate: Once approved, you'll receive a registration certificate. This certificate gives legal standing to sue third parties and proves the partnership's existence.

- Get PAN and TAN: Apply for a Permanent Account Number (PAN) for the firm from the Income Tax Department. Also, obtain a Tax Deduction and Collection Account Number (TAN) if you'll deduct tax at source.

- Open a bank account: Use the partnership deed and registration certificate to open a business bank account. All partners typically need to be present or provide authorization.

- Register for GST: If your annual turnover exceeds the threshold, register for Goods and Services Tax.

When your partnership firm starts serving clients in the USA, UK, or Europe, payment collection becomes critical. You need accounts that work in their currencies.

Accept global payments seamlessly with PayGlocal

Operating a partnership firm serving international clients means managing cross-border payments. Traditional bank transfers take days, charge high fees, and create paperwork headaches. Your business needs a payment solution built for global trade.

PayGlocal is an all-in-one payment platform designed for partnership businesses expanding globally. Whether you're exporting goods, providing services, or working with overseas clients, PayGlocal simplifies how you collect and manage international payments.

Here's what partnership firms get with PayGlocal:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries. Get local accounts in USD, GBP, EUR, and CAD so you look like a local business to your international clients.

- Global payment methods: Go beyond cards. Accept 40+ local payment methods that your international customers prefer, increasing trust and conversion rates.

- Instant compliance: Receive FIRC (Foreign Inward Remittance Certificate) right in your inbox after settlement. Stay compliant without chasing banks for documents.

- Zero fixed costs: Pay only when you transact. No setup fees, no monthly charges, no platform fees. Transparent pricing with no surprises.

- Recurring payments: Set up subscriptions or recurring billing for international clients. Automate collections and focus on growing your business.

PayGlocal handles the complexity of international payments so your partnership can focus on serving clients and growing revenue.

Final thoughts

A partnership firm offers a simple, flexible way to start a business with others who share your vision. The structure works well for professional services, exporters, and small businesses that want to get started quickly without heavy compliance burdens.

The key to success is choosing the right partners, drafting a clear partnership deed, and maintaining open communication about business decisions and finances. Consider your liability comfort level and growth plans when deciding between a general partnership and an LLP.

As your partnership grows and serves clients across borders, having the right payment infrastructure becomes critical. You need solutions that handle multiple currencies, provide compliance documents automatically, and give you complete visibility into payment status.

Get started with PayGlocal today and start accepting international payments easily in multiple currencies.