Digital payments in India grew at 46% annually between 2021 and 2024, jumping from 8,839 crore to 18,737 crore transactions. This shows that more businesses are moving money digitally than ever before.

RTGS is one of the most popular digital payment methods in India for business transactions. But how much you can actually transfer depends on whether you're using online banking or visiting a branch, which bank you're with, and what type of account you hold.

In this guide, we break down everything you need to know about RTGS limits, including the minimum amount to send, maximum daily caps, bank-specific limits, and how to increase your transfer limit when you need to move larger amounts.

RTGS limit refers to the minimum and maximum amount you can transfer using Real Time Gross Settlement, a payment system for high-value electronic fund transfers in India. The limit determines how much money you can send in a single transaction and within a 24-hour period.

Banking regulations set a minimum RTGS limit of ₹2 lakh per transaction. This means you cannot use RTGS for transfers below ₹2,00,000. For amounts below this threshold, you need to use NEFT, IMPS, or UPI instead.

There is no maximum limit set by regulators for RTGS transfers. However, individual banks apply their own daily caps for online transactions made through internet banking or mobile apps. These caps typically range from ₹10 lakh to ₹50 lakh per day, depending on your bank and account type.

The minimum RTGS limit is ₹2 lakh (₹2,00,000) per transaction. This is a mandatory requirement that applies to all banks across India.

You cannot initiate an RTGS transfer for any amount below ₹2 lakh. If you try to send ₹1.9 lakh or any amount under the threshold, your bank will reject the transaction. For instance, if you need to pay a supplier ₹1.5 lakh urgently, you'll need to use NEFT or IMPS instead, as RTGS is not available for this amount.

This minimum limit exists because RTGS is designed specifically for high-value transactions that need immediate settlement. The system processes each transaction individually in real time rather than in batches, making it suitable for large, time-sensitive payments like property purchases, business invoices, or investment transactions.

There is no maximum RTGS limit set by regulators. You can technically transfer any amount above ₹2 lakh without an upper cap from banking authorities.

However, this doesn't mean you can transfer unlimited amounts through your banking app. Banks impose their own daily and per-transaction limits for online RTGS transfers made through internet banking or mobile apps. These limits vary widely based on your bank, account type, and relationship with the bank.

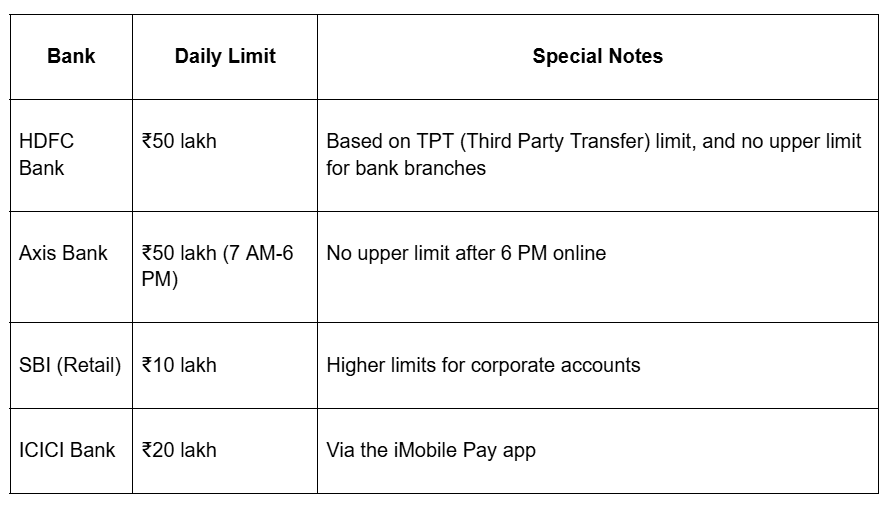

For instance, you might have a daily online RTGS limit of ₹50 lakh with HDFC Bank but only ₹20 lakh with ICICI Bank on certain account types.

Different banks set different daily RTGS limits for online transactions. Here's what you can expect from major banks in India:

You can increase your RTGS transfer limit by requesting your bank to raise your daily cap. Most banks allow you to do this through multiple channels. Here's how to increase your RTGS limit:

The approval depends on several factors. Banks evaluate your account history, average balance, transaction patterns, credit profile, and relationship tenure before approving limit increases. For instance, if you've maintained a high average balance for years and have a clean transaction history, your bank is more likely to approve a significant increase.

RTGS charges depend on whether you make the transfer online or at a bank branch. Online RTGS transfers have been free since July 2019.

When you use internet banking or mobile banking for RTGS, there are no charges. Banking regulations require all banks to waive fees for online RTGS transactions to encourage digital payments.

Branch RTGS transfers have charges that vary by bank and transaction amount. But it’s typically just ₹25-50 + GST at most banks. Banking authorities have set the maximum charge ceilings so banks cannot charge more than the set amounts.

RTGS offers several advantages for businesses and individuals who need to transfer large amounts quickly. Here's why you might want to choose RTGS:

RTGS works well for large domestic transfers, but it also has limitations like a minimum payment limit and daily caps set by banks. If you're doing business internationally, you need an effective payment solution that can help you collect payments from overseas clients, manage multi-currency transactions, and handle proper compliance documentation.

PayGlocal is built for businesses that operate globally. Whether you're a freelancer collecting from international clients, an exporter managing overseas invoices, or a company scaling across borders, you need a payment solution that works in multiple currencies without the restrictions of domestic banking.

Here's what you get with PayGlocal:

PayGlocal helps businesses collect globally and settle locally without the friction of traditional banking limits. You focus on growing your business while it handles the complexity of international payments.

RTGS limits vary based on how you transfer: online banking typically caps you at ₹10-50 lakh per day, depending on your bank, while branch transfers have no upper limit beyond the ₹2 lakh minimum. You can increase these limits by contacting your bank with proper documentation and account history.

For domestic high-value transfers, RTGS works well with its real-time settlement and 24x7 availability. But if you're collecting payments from international clients or need to manage multi-currency transactions, domestic payment systems have clear limitations.

Ready to accept international payments fast? Get started with PayGlocal today and start collecting payments from 180+ countries with transparent pricing and instant compliance.

RTGS is one of the most popular digital payment methods in India for business transactions. But how much you can actually transfer depends on whether you're using online banking or visiting a branch, which bank you're with, and what type of account you hold.

In this guide, we break down everything you need to know about RTGS limits, including the minimum amount to send, maximum daily caps, bank-specific limits, and how to increase your transfer limit when you need to move larger amounts.

Key takeaways

- Minimum RTGS limit: ₹2 lakh per transaction, mandated by banking regulations for all banks.

- Maximum RTGS limit: No upper cap from regulators, but banks set their own daily online limits.

- Bank-specific daily caps: Most banks allow ₹10-50 lakh per day for online RTGS, with some banks having no upper limit at branches.

- All-time availability: RTGS works round the clock, 365 days a year, with real-time settlement.

- For international payments: PayGlocal offers an efficient global payment solution with multi-currency accounts and transparent pricing.

What is the RTGS limit per day?

RTGS limit refers to the minimum and maximum amount you can transfer using Real Time Gross Settlement, a payment system for high-value electronic fund transfers in India. The limit determines how much money you can send in a single transaction and within a 24-hour period.

Banking regulations set a minimum RTGS limit of ₹2 lakh per transaction. This means you cannot use RTGS for transfers below ₹2,00,000. For amounts below this threshold, you need to use NEFT, IMPS, or UPI instead.

There is no maximum limit set by regulators for RTGS transfers. However, individual banks apply their own daily caps for online transactions made through internet banking or mobile apps. These caps typically range from ₹10 lakh to ₹50 lakh per day, depending on your bank and account type.

What is the minimum RTGS limit?

The minimum RTGS limit is ₹2 lakh (₹2,00,000) per transaction. This is a mandatory requirement that applies to all banks across India.

You cannot initiate an RTGS transfer for any amount below ₹2 lakh. If you try to send ₹1.9 lakh or any amount under the threshold, your bank will reject the transaction. For instance, if you need to pay a supplier ₹1.5 lakh urgently, you'll need to use NEFT or IMPS instead, as RTGS is not available for this amount.

This minimum limit exists because RTGS is designed specifically for high-value transactions that need immediate settlement. The system processes each transaction individually in real time rather than in batches, making it suitable for large, time-sensitive payments like property purchases, business invoices, or investment transactions.

What is the maximum RTGS limit?

There is no maximum RTGS limit set by regulators. You can technically transfer any amount above ₹2 lakh without an upper cap from banking authorities.

However, this doesn't mean you can transfer unlimited amounts through your banking app. Banks impose their own daily and per-transaction limits for online RTGS transfers made through internet banking or mobile apps. These limits vary widely based on your bank, account type, and relationship with the bank.

For instance, you might have a daily online RTGS limit of ₹50 lakh with HDFC Bank but only ₹20 lakh with ICICI Bank on certain account types.

What are the RTGS limits for different banks?

Different banks set different daily RTGS limits for online transactions. Here's what you can expect from major banks in India:

How to increase RTGS limit?

You can increase your RTGS transfer limit by requesting your bank to raise your daily cap. Most banks allow you to do this through multiple channels. Here's how to increase your RTGS limit:

- Visit your bank branch: Go to your home branch with your identity documents and request a limit increase. Branch managers can approve higher limits based on your account history and relationship with the bank.

- Use internet banking: Log into your online banking portal and look for options to modify your transaction limits or TPT limits. Some banks let you increase limits instantly up to certain thresholds.

- Call customer support: Contact your bank's customer care number and request a limit increase. They will verify your identity and guide you through the process.

- Use mobile banking app: Some banks allow you to request limit increases directly through their mobile apps in the settings or security section.

- Submit a written request: For very high limit increases, banks may ask you to submit a formal written request with supporting documents.

The approval depends on several factors. Banks evaluate your account history, average balance, transaction patterns, credit profile, and relationship tenure before approving limit increases. For instance, if you've maintained a high average balance for years and have a clean transaction history, your bank is more likely to approve a significant increase.

What are the RTGS charges?

RTGS charges depend on whether you make the transfer online or at a bank branch. Online RTGS transfers have been free since July 2019.

When you use internet banking or mobile banking for RTGS, there are no charges. Banking regulations require all banks to waive fees for online RTGS transactions to encourage digital payments.

Branch RTGS transfers have charges that vary by bank and transaction amount. But it’s typically just ₹25-50 + GST at most banks. Banking authorities have set the maximum charge ceilings so banks cannot charge more than the set amounts.

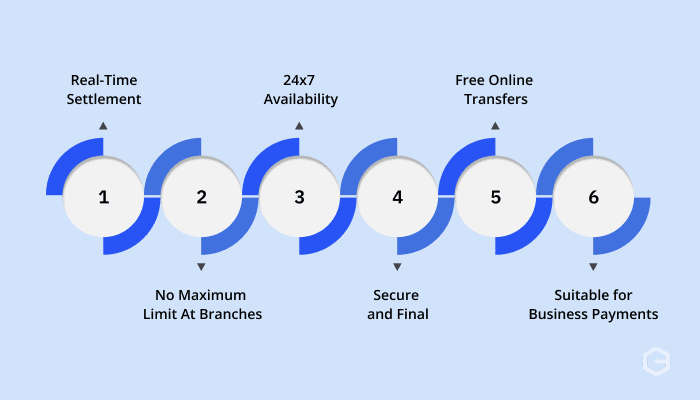

What are the benefits of using RTGS?

RTGS offers several advantages for businesses and individuals who need to transfer large amounts quickly. Here's why you might want to choose RTGS:

- Real-time settlement: Funds reach the beneficiary account within 30 minutes, typically, making it suitable for urgent high-value payments.

- No maximum limit at branches: You can transfer any amount above ₹2 lakh when you visit a bank branch, without upper caps.

- 24x7 availability: RTGS works round the clock, 365 days a year, including weekends and bank holidays, with only brief maintenance downtime.

- Secure and final: Transactions are irrevocable and settle in the central banking system, reducing fraud risk for large payments.

- Free online transfers: No charges when you use internet or mobile banking, helping you save on transaction costs.

- Suitable for business payments: Perfect for vendor payments, property transactions, investment transfers, and other high-value business needs.

Scale your payment processes globally with PayGlocal

RTGS works well for large domestic transfers, but it also has limitations like a minimum payment limit and daily caps set by banks. If you're doing business internationally, you need an effective payment solution that can help you collect payments from overseas clients, manage multi-currency transactions, and handle proper compliance documentation.

PayGlocal is built for businesses that operate globally. Whether you're a freelancer collecting from international clients, an exporter managing overseas invoices, or a company scaling across borders, you need a payment solution that works in multiple currencies without the restrictions of domestic banking.

Here's what you get with PayGlocal:

- Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD.

- Instant compliance documents: Get FIRC (Foreign Inward Remittance Certificate) automatically delivered to your inbox after settlement for tax and export compliance.

- Transparent pricing: Pay only when you transact with no setup fees, no platform fees, and no hidden charges.

- Track every payment: Monitor your funds with real-time status updates and downloadable reports from a single dashboard.

- Global payment methods: Accept payments through international cards and 40+ local payment methods your global customers prefer.

- One platform: Manage all your international payments, settlements, and compliance from a single interface.

PayGlocal helps businesses collect globally and settle locally without the friction of traditional banking limits. You focus on growing your business while it handles the complexity of international payments.

Final thoughts

RTGS limits vary based on how you transfer: online banking typically caps you at ₹10-50 lakh per day, depending on your bank, while branch transfers have no upper limit beyond the ₹2 lakh minimum. You can increase these limits by contacting your bank with proper documentation and account history.

For domestic high-value transfers, RTGS works well with its real-time settlement and 24x7 availability. But if you're collecting payments from international clients or need to manage multi-currency transactions, domestic payment systems have clear limitations.

Ready to accept international payments fast? Get started with PayGlocal today and start collecting payments from 180+ countries with transparent pricing and instant compliance.