Key Takeaways

Wire transfer refers to the fast and secure transfer of money between banks, often used for high-value or time-sensitive transactions. It’s a preferred method for businesses and individuals needing speed, traceability, and global reach.

- There are two main types of wire transfers: domestic and international. Domestic transfers are quicker and less expensive, whereas international transfers involve additional steps, including currency exchange, SWIFT codes, and regulatory checks.

- Wire transfers offer advantages over ACH and other methods, including near-instant processing, stronger security protocols, and irreversible transactions. However, they may involve higher fees and limited refund options.

- Knowing the costs, risks, and procedures involved helps you make informed decisions. When handled correctly, wire transfers offer unmatched reliability for global commerce, particularly when combined with platforms like PayGlocal for secure cross-border payments.

Have you ever wondered how large amounts of money move between countries in a matter of minutes?

That's the advantage of wire transfers. They ensure the smooth movement of money as global commerce grows. Wire transfers are a fast, secure, and traceable method of electronically transferring money between banks, particularly for high-value or international transactions.

According to the World Bank, India accounted for 14.3%/news-in-shorts#:~:text=14.1%20News%20In%20Shorts,economic%20prosperity%20and%20aging%20population.) of global remittances in 2024, marking its highest share ever. This highlights the scale of international money transfers. This guide will give you clarity and confidence if you are someone who manages international payments regularly.

What are wire transfers, and how do they work?

Wire transfers are an electronic method of transferring money between banks worldwide. They are typically used for high-value or time-sensitive transactions where speed and accuracy are critical.

Historically, wire transfers revolutionized money transfers, paving the way for the fast-paced financial systems we use today. They eliminate the need for physical cash, offering a reliable way to send large sums swiftly.

In the 19th century, this was done using telegraph wires, hence the term "wire." Today, digital networks like SWIFT have replaced telegraph lines, making the system far more efficient and secure.

SWIFT, Fedwire, and CHIPS are among the most widely used systems. Each offers different advantages based on transaction speed, cost, and geographic reach.

The evolution of wire transfers demonstrates how technology has revolutionized global finance, making it faster, more efficient, and more secure.

What are the different types of wire transfers?

Wire transfers are broadly categorized based on their geographic scope and application. While domestic and international transfers serve similar purposes, they each have distinct challenges and benefits.

- Domestic Wire Transfers are used for bank-to-bank transfers within the same country. They are usually faster and less costly than international transfers and rely on local networks like Fedwire.

- International Wire Transfers involve banks across different countries using networks like SWIFT and require codes like IBAN or BIC. These are more complex due to regulatory checks, currency exchange, and time zone differences.

- Bank Wire Transfers are conducted directly between banks through networks like SWIFT or other clearinghouses.

- Consumer-to-Consumer Wire Transfers occur when individuals send money to others, often via banks or specialized services.

- Real-Time Wire Transfers are used when some countries offer instant or near-instant wire transfers that settle immediately, such as the Faster Payments Service in the UK or RTP in the US.

The process is faster and more affordable for domestic transfers. However, international payments are more complex and require more steps and oversight.

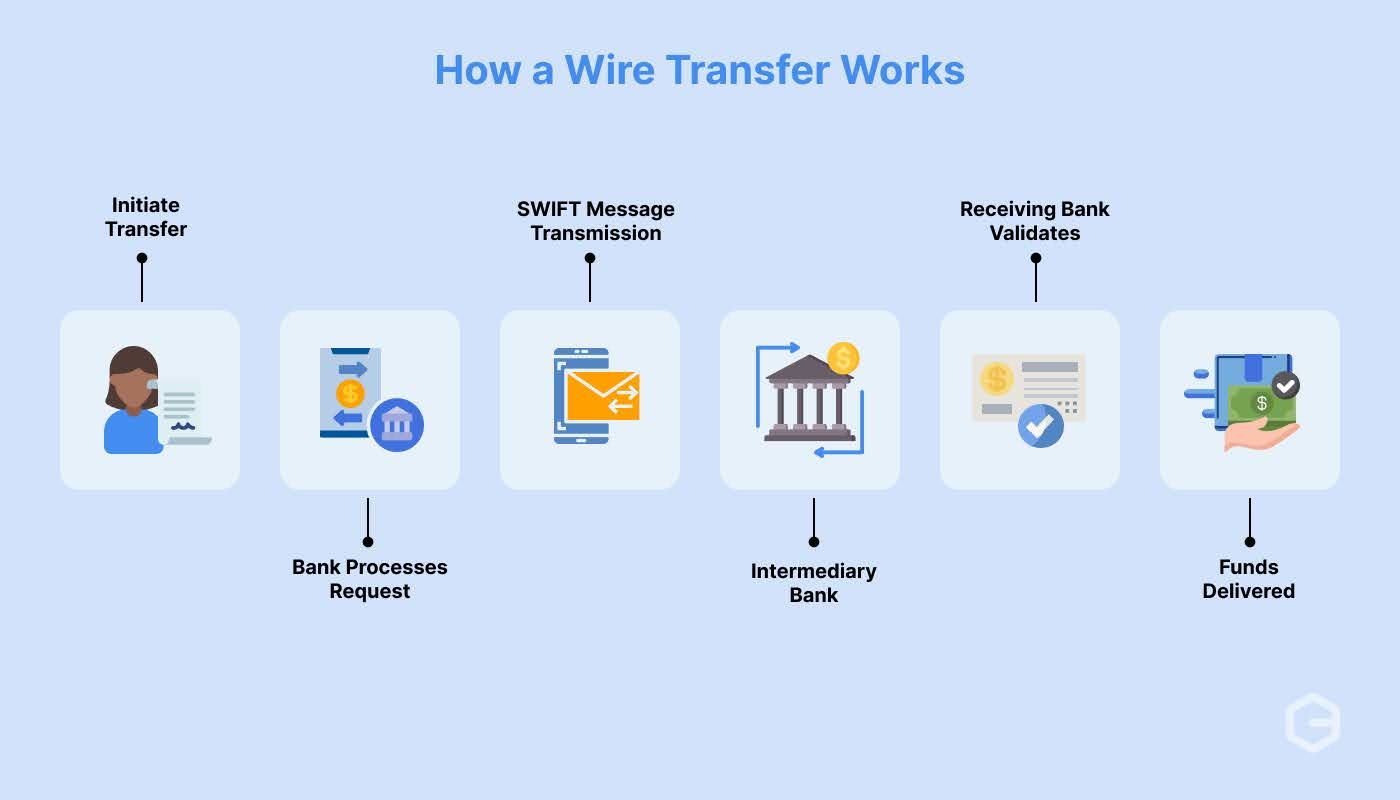

How does a wire transfer process work?

Though wire transfers appear seamless, several steps and verifications are involved. The process involves multiple intermediaries and detailed checks to ensure the transfer is secure, correct, and efficient.

1. Initiating the Transfer: The sender provides details like the recipient’s name, bank name, account number, and SWIFT code. This information must be accurate to avoid delays or failed transfers.

2. The Role of Banks and the SWIFT System: Banks act as intermediaries to process and verify details through the SWIFT system, which sends secure messages between financial institutions to ensure the legitimacy of transactions.

The involvement of multiple intermediaries and systems ensures that wire transfers are secure, though it requires careful attention to detail.

How do wire transfers compare to ACH transfers?

Wire transfers are often the preferred method for time-sensitive and high-value transactions. However, depending on the situation, other transfer options, like ACH transfers, may offer advantages in cost or speed.

1. Wire vs. ACH Transfers: Wire transfers are faster and often completed within the same day. However, they are more costly. ACH transfers are more economical but slower, typically taking 1–3 days.

2. Reversibility and Reliability: Wire transfers are typically non-reversible, offering more certainty but requiring more care. ACH services offer some recourse but may delay settlement.

Wire transfers are often preferred for large or urgent transactions, while ACH is better suited for everyday or smaller payments. Wire transfers stand out when speed and reliability are essential, although they come with higher fees than more economical options, such as ACH.

What risks should you consider with wire transfers?

Wire transfers, like any financial tool, carry risks, especially when not accompanied by adequate checks. These risks can be minimized by knowing the process, ensuring accuracy, and knowing how to protect yourself. Awareness of potential challenges will help you manage your transfers with more confidence.

Key risks and what you should know include:

Irreversibility: Once processed, transfers can't be undone. Double-check all recipient details before initiating.

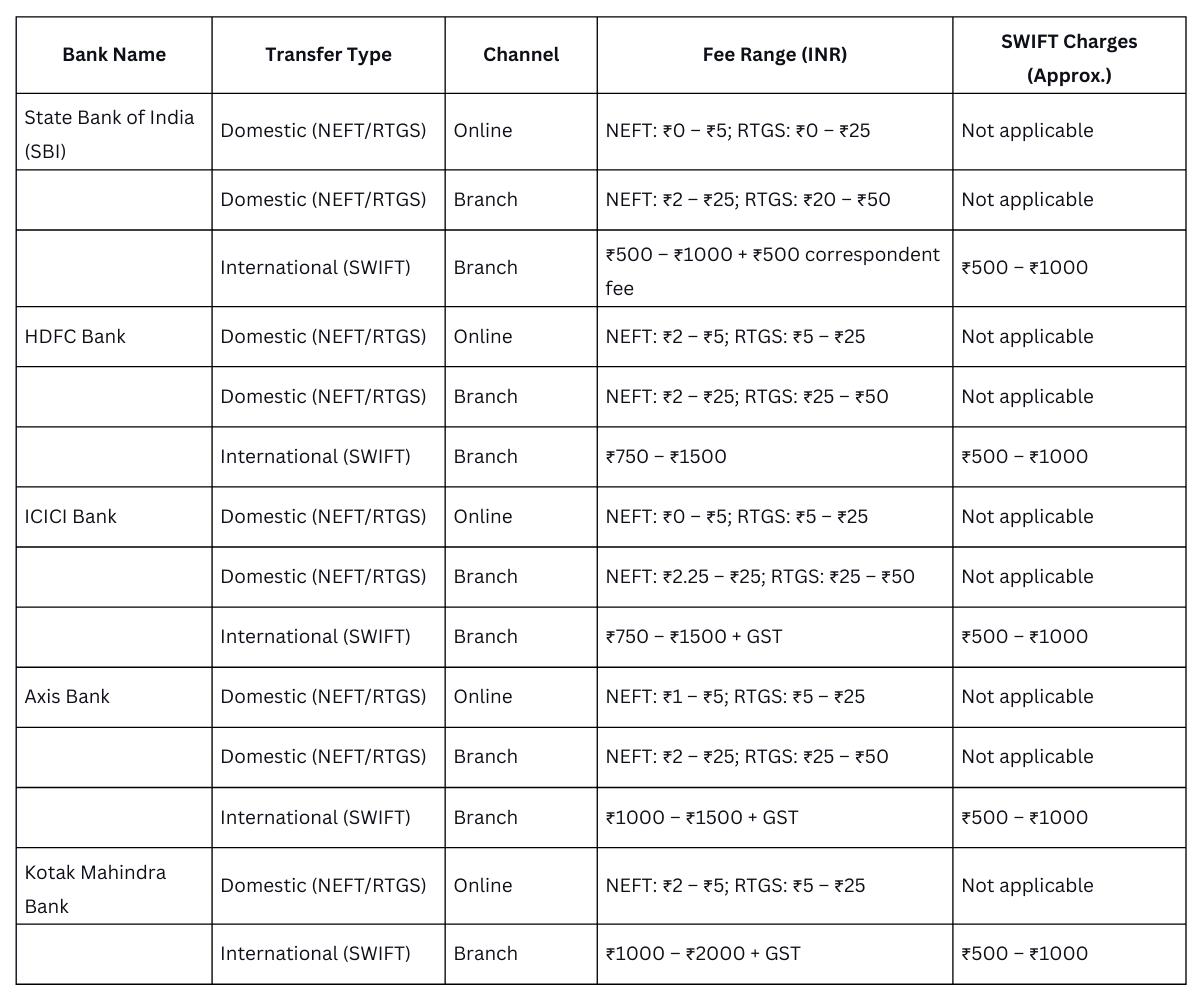

Fee Structure: Fees can range from ₹500 to ₹ 2,500 or more per transfer, depending on the destination and currency. Intermediate banks may charge additional hidden fees.

Security Protocols: Banks require Know Your Customer (KYC) and screening measures to prevent fraud and money laundering. These checks can delay transfers if documents are incomplete.

While the risks are manageable, it’s important for you to ensure that the details are accurate and the process is secure.

What are the cost factors involved in wire transfers?

Wire transfers often come with costs, but planning can reduce them. While some fees are unavoidable, careful planning and strategic decision-making can reduce costs.

The following can help minimize expenses:

Domestic vs. International Fees: Domestic transfers are typically less expensive, whereas international transfers incur additional fees for currency conversion and intermediary services. Choosing the right partner can reduce overall charges.

Saving Tips: Schedule transfers in advance and avoid peak hours. Utilizing providers like PayGlocal, which offer competitive foreign exchange rates, can also be beneficial.

Why many businesses are switching to PayGlocal for cross-border transfers

PayGlocal is designed to simplify and streamline international payments for Indian freelancers, exporters, and global businesses. Whether you're managing high-value wire transfers, recurring subscriptions, or global customer transactions, PayGlocal offers a unified platform that prioritizes speed, compliance, and clarity.

If wire transfers feel overwhelming or expensive due to delays, hidden fees, or compliance issues, PayGlocal helps you stay in control with transparent solutions designed for global operations. Here’s how PayGlocal empowers your international transactions:

Dynamic checkout: Customize the payment experience based on user location, currency, and device to increase conversions and reduce drop-offs.

Card payments: Accept global credit and debit cards with high success rates and built-in fraud protection designed for cross-border commerce.

Global payment methods: Support popular local alternatives, including wallets, bank transfers, and UPI, to offer customers a wider range of secure payment options.

Recurring payments: Automate billing cycles for international subscriptions, retainers, or long-term clients with complete reliability.

Multi-currency account: Receive and settle payments in multiple currencies while minimizing conversion losses and improving FX transparency.

One platform: Manage all your cross-border collections from a single dashboard with unified reporting, analytics, and settlement tracking.

Sanction screening: Ensure every transaction is compliant with international regulations through real-time verification and risk filters.

With PayGlocal, wire transfers, and international payments become less about paperwork and more about progress. Sign up for free with PayGlocal today and find more innovative ways to grow global revenue while staying compliant and confident.

Conclusion

So, what does a wire transfer mean for your finances? It means speed, security, and peace of mind, especially for large or cross-border payments. Knowing the process, types, and risks ensures smoother transactions with fewer surprises.

Clarity in wire transfers ensures operational efficiency for businesses handling international and domestic payments. For platforms like PayGlocal, integrating with secure wire systems helps merchants complete high-value transactions with lower friction.

Do you need a secure and efficient way to send or receive international payments? Curious about how to reduce currency loss and boost approval rates? Contact PayGlocal today and simplify cross-border transactions with enhanced security, speed, and a seamless user experience.