Digital transactions have grown rapidly in recent years. In fact, according to recent data, over 65,000 crore digital transactions occurred in India in the last 6 financial years (from 2019-2020 to 2024-2025).

Digital payments have completely changed how businesses and consumers handle money. Instead of carrying cash or physical cards, many users now rely on digital wallets for quick, secure transactions.

But what exactly is a digital wallet, and how does it work? Let’s find out, along with a complete breakdown of its common types, like closed, semi-closed, and open digital wallets.

A digital wallet is an electronic application that stores payment information and allows users to make transactions without carrying physical cash or cards. Also known as e-wallets or mobile wallets, these software programs run on smartphones, tablets, or computers to facilitate secure digital payments.

Digital wallets store various payment methods, including credit cards, debit cards, and bank account details. When you make a purchase, the wallet securely transmits your payment information to complete the transaction. Popular examples include Apple Pay, Google Wallet, PayPal, and regional solutions like Paytm in India.

Digital wallets offer convenience and security advantages. Instead of entering card details for every online purchase or carrying multiple physical cards, you can complete transactions with a simple tap, scan, or click.

Digital wallets operate through a simple but secure process that connects users, merchants, and financial institutions. When you add a payment method to your digital wallet, the system stores your information using advanced encryption and payment tokenization.

Here's how a typical digital wallet transaction works:

This process typically takes seconds and offers multiple layers of security that surpass traditional card payments.

Digital wallets come in several forms, each designed for specific use cases and user preferences. The main categories include:

Let’s explore each type in detail:

Closed wallets work exclusively with specific retailers or service providers. Users load money into these wallets and can only spend it with that particular company. These wallets cannot be used for cash withdrawals or transfers to other platforms.

For instance, BookMyShow Wallet and Myntra Wallet are some examples of closed digital wallets that you can use only on purchases made on their specific platforms. While limited in scope, closed wallets often offer loyalty rewards and exclusive discounts to encourage customer retention.

Semi-closed wallets offer more flexibility than closed systems but still have restrictions. Users can make payments to multiple merchants who have agreements with the wallet provider, but cannot withdraw cash or transfer money to bank accounts directly.

In India, Paytm Wallet and Airtel Money fall into this category, allowing payments to various merchants, bill payments, and limited money transfers.

Open wallets provide full banking functionality and are typically issued by banks or financial institutions. Users can perform all financial transactions, including purchases, money transfers, cash withdrawals, and bill payments, without restrictions.

PayPal functions as an open wallet, allowing users to send money globally, withdraw to bank accounts, and make purchases at millions of merchants worldwide. Google Pay and Apple Pay, when linked to bank accounts, also function as open wallets.

Bank mobile apps fall into this category as well, offering complete control over finances. These wallets require stronger authentication and regulatory compliance due to their comprehensive functionality and features.

Digital wallets offer numerous advantages that make them attractive for both consumers and businesses:

Security remains a top priority for digital wallet providers, with multiple layers of protection built into every transaction:

These security measures make digital wallets significantly safer than carrying physical cards or cash, which offer no protection against theft or loss.

Several key technologies enable digital wallet functionality:

While digital wallets solve many payment challenges, businesses operating internationally need more than basic wallet functionality. Managing multiple currencies, compliance requirements, and global payment methods can quickly become overwhelming.

PayGlocal solves these complexities with a complete payment platform designed for businesses that want to expand into international markets.

PayGlocal combines the convenience of digital wallets with the power needed for growing international business, helping you get paid faster and more reliably from anywhere in the world.

Digital wallets have changed how we handle payments, offering security, convenience, and features that traditional payment methods cannot match. From contactless purchases to international transfers, the right digital wallet can significantly improve both customer experience and business operations.

For businesses operating globally or planning international expansion, standard digital wallets may not provide the comprehensive functionality needed for success. PayGlocal goes beyond basic wallet features to offer true global payment capabilities with transparent pricing and instant compliance support.

Ready to improve your global payment processes and grow faster? Get started with PayGlocal today.

Digital payments have completely changed how businesses and consumers handle money. Instead of carrying cash or physical cards, many users now rely on digital wallets for quick, secure transactions.

But what exactly is a digital wallet, and how does it work? Let’s find out, along with a complete breakdown of its common types, like closed, semi-closed, and open digital wallets.

Key Takeaways:

- Electronic payment storage: Digital wallets store payment information and enable contactless transactions without physical cards or cash.

- Main types: Closed wallets work with specific stores, semi-closed wallets work with multiple merchants, and open wallets provide full banking features.

- Top benefits: Faster transactions, enhanced security through encryption, expense tracking, and support for contactless payments and instant money transfers.

- International payments: PayGlocal offers global digital payment solutions with multi-currency support, global payment methods, and seamless international transaction processing.

What is a digital wallet?

A digital wallet is an electronic application that stores payment information and allows users to make transactions without carrying physical cash or cards. Also known as e-wallets or mobile wallets, these software programs run on smartphones, tablets, or computers to facilitate secure digital payments.

Digital wallets store various payment methods, including credit cards, debit cards, and bank account details. When you make a purchase, the wallet securely transmits your payment information to complete the transaction. Popular examples include Apple Pay, Google Wallet, PayPal, and regional solutions like Paytm in India.

Digital wallets offer convenience and security advantages. Instead of entering card details for every online purchase or carrying multiple physical cards, you can complete transactions with a simple tap, scan, or click.

How do digital wallets work?

Digital wallets operate through a simple but secure process that connects users, merchants, and financial institutions. When you add a payment method to your digital wallet, the system stores your information using advanced encryption and payment tokenization.

Here's how a typical digital wallet transaction works:

- Registration and setup: You download the wallet app and add payment methods by scanning cards or entering details manually. The wallet creates encrypted tokens that represent your actual card numbers.

- Transaction initiation: When making a purchase, you select your preferred payment method from the wallet and authenticate the transaction.

- Secure transmission: The wallet sends tokenized payment data to the /'s payment processor, never exposing actual card numbers or sensitive information.

- Authorization and processing: The payment processor communicates with the bank or card issuer to verify funds and approve the transaction.

- Confirmation: Both the user and merchant receive instant confirmation of the successful payment, with transaction details logged in the wallet for future reference.

This process typically takes seconds and offers multiple layers of security that surpass traditional card payments.

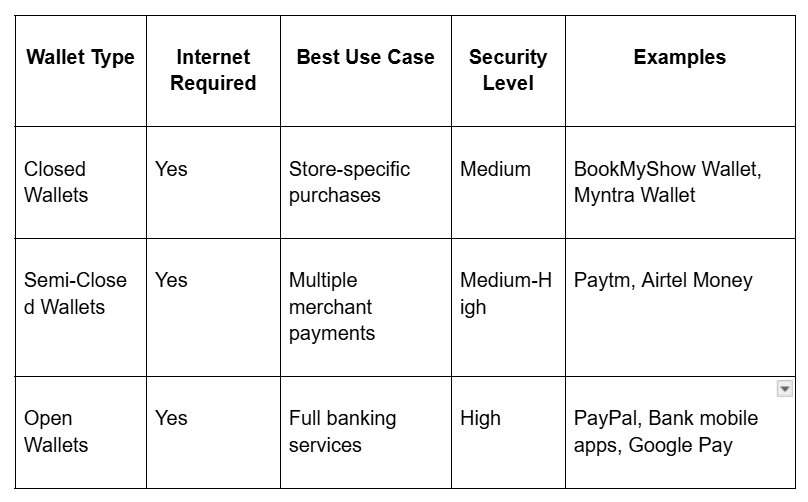

What are the different types of digital wallets?

Digital wallets come in several forms, each designed for specific use cases and user preferences. The main categories include:

Let’s explore each type in detail:

Closed wallets

Closed wallets work exclusively with specific retailers or service providers. Users load money into these wallets and can only spend it with that particular company. These wallets cannot be used for cash withdrawals or transfers to other platforms.

For instance, BookMyShow Wallet and Myntra Wallet are some examples of closed digital wallets that you can use only on purchases made on their specific platforms. While limited in scope, closed wallets often offer loyalty rewards and exclusive discounts to encourage customer retention.

Semi-closed wallets

Semi-closed wallets offer more flexibility than closed systems but still have restrictions. Users can make payments to multiple merchants who have agreements with the wallet provider, but cannot withdraw cash or transfer money to bank accounts directly.

In India, Paytm Wallet and Airtel Money fall into this category, allowing payments to various merchants, bill payments, and limited money transfers.

Open wallets

Open wallets provide full banking functionality and are typically issued by banks or financial institutions. Users can perform all financial transactions, including purchases, money transfers, cash withdrawals, and bill payments, without restrictions.

PayPal functions as an open wallet, allowing users to send money globally, withdraw to bank accounts, and make purchases at millions of merchants worldwide. Google Pay and Apple Pay, when linked to bank accounts, also function as open wallets.

Bank mobile apps fall into this category as well, offering complete control over finances. These wallets require stronger authentication and regulatory compliance due to their comprehensive functionality and features.

What are the benefits of digital wallets?

Digital wallets offer numerous advantages that make them attractive for both consumers and businesses:

- Contactless payments: You can pay by tapping your phone on NFC-enabled terminals or scanning QR codes, reducing physical contact and speeding up transactions.

- Enhanced security: Advanced encryption, tokenization, and biometric authentication provide better security than traditional cards. Even if a phone is stolen, wallets require authentication to access.

- Expense tracking: Automatic transaction logging helps users monitor spending patterns and manage budgets- more effectively than cash transactions.

- Instant money transfers: Send money instantly to friends, family, or business contacts without needing cash or checks.

- Bill payments and recharges: Pay utility bills, mobile recharges, and subscription services directly from the wallet interface.

- Loyalty integration: Many wallets store loyalty cards and automatically apply rewards during purchases.

- Reduced checkout friction: Online purchases require fewer clicks and form fields, leading to higher conversion rates for businesses.

How secure are digital wallets?

Security remains a top priority for digital wallet providers, with multiple layers of protection built into every transaction:

- Tokenization: Digital wallets replace actual card numbers with unique tokens that are useless to fraudsters even if intercepted.

- Biometric authentication: Fingerprint, face recognition, or voice authentication ensures only authorized users can access the wallet.

- End-to-end encryption: All payment data is encrypted during transmission, making it unreadable to potential attackers.

- Two-factor authentication: Additional verification steps like SMS codes or app notifications provide extra security layers.

- Device-specific binding: Wallets are tied to specific devices and require re-authentication if accessed from new devices.

- Remote wipe capabilities: If a device is lost or stolen, users can remotely disable the wallet to prevent unauthorized access.

These security measures make digital wallets significantly safer than carrying physical cards or cash, which offer no protection against theft or loss.

What technologies power digital wallets?

Several key technologies enable digital wallet functionality:

- Near Field Communication (NFC): Allows contactless payments by tapping phones on compatible terminals within a few centimeters of range.

- QR codes: Quick Response codes enable payments by scanning merchant-displayed codes with the wallet app camera.

- Bluetooth Low Energy: Enables payments in situations where NFC isn't available, though less commonly used.

- Magnetic Secure Transmission (MST): Samsung Pay's technology that works with traditional magnetic strip readers by generating magnetic signals.

- Tokenization platforms: Convert sensitive payment data into secure tokens that can be safely transmitted and stored.

- Biometric sensors: Fingerprint scanners, facial recognition cameras, and other authentication hardware built into modern devices.

- Cloud infrastructure: Secure servers that store encrypted wallet data and facilitate real-time transaction processing.

Scale globally with fast and secure payment solutions

While digital wallets solve many payment challenges, businesses operating internationally need more than basic wallet functionality. Managing multiple currencies, compliance requirements, and global payment methods can quickly become overwhelming.

PayGlocal solves these complexities with a complete payment platform designed for businesses that want to expand into international markets.

- Multi-currency acceptance: Collect payments in 33+ currencies from 180+ countries and settle in your preferred currency. This reduces banking complexity while giving customers local payment convenience.

- Dynamic checkout options: Provide customers with multiple payment method choices, which increases conversion rates and reduces cart abandonment across different markets.

- Global payment method support: Accept 40+ payment methods, including regional bank transfers and local payment options, so you never lose sales due to limited payment options.

- Recurring payment solutions: Set up automated billing for subscriptions, installments, and repeat purchases across all currencies and payment methods. This ensures a consistent revenue flow while reducing manual collection efforts.

- Instant compliance documentation: Receive automatic FIRC immediately upon settlement without manual paperwork. This saves administrative time while ensuring compliance.

PayGlocal combines the convenience of digital wallets with the power needed for growing international business, helping you get paid faster and more reliably from anywhere in the world.

Final thoughts

Digital wallets have changed how we handle payments, offering security, convenience, and features that traditional payment methods cannot match. From contactless purchases to international transfers, the right digital wallet can significantly improve both customer experience and business operations.

For businesses operating globally or planning international expansion, standard digital wallets may not provide the comprehensive functionality needed for success. PayGlocal goes beyond basic wallet features to offer true global payment capabilities with transparent pricing and instant compliance support.

Ready to improve your global payment processes and grow faster? Get started with PayGlocal today.