India's export sector has grown significantly, with total exports jumping from $466.22 billion in 2013-14 to $778.21 billion in 2023-24. More Indian businesses are now handling international payments daily, and many face dynamic currency conversion offers during these transactions.

You might see DCC when paying overseas suppliers or receiving payments from international clients. While DCC ensures transparency and ease in transactions, it often comes with higher fees and high exchange rates that can impact your business expenses.

In this guide, we break down exactly how dynamic currency conversion works, when it might be useful, and what challenges it presents. We also cover what alternatives exist for businesses that need reliable, cost-effective international payment processing.

Dynamic Currency Conversion (DCC) is a service that lets you pay for international transactions in your home currency instead of the local currency. When you're traveling or making cross-border payments, DCC converts the transaction amount at the point of sale, showing you the exact cost in your familiar currency.

Let’s say, you're buying software from a US company, and the bill is $500. With DCC, instead of paying in US dollars and letting your bank convert it later, the merchant's payment system converts it immediately to INR, say ₹42,000, and shows you this amount upfront.

You see exactly what you'll pay without doing mental math or worrying about surprise charges on your statement. For businesses managing budgets and cash flow, this transparency can feel valuable.

DCC operates through agreements between merchants, payment processors, and acquiring banks. The service is offered at millions of locations worldwide, from hotel check-ins to online purchases, making it one of the most common currency services travelers and businesses encounter.

DCC operates through a chain of agreements between merchants, payment processors, and acquiring banks. When you initiate a transaction, the system detects your card's country of origin and offers the conversion option. Here’s how the process works:

= Fee distribution: The markup from the exchange rate gets split between the merchant, payment processor, and acquiring bank as revenue.

Different platforms and locations offer DCC in various forms, each with specific characteristics that affect your costs and experience.

Each type operates differently based on location and payment method. Here's how they work in practice and when you might encounter them.

ATMs worldwide offer DCC when you withdraw cash or check balances. These machines are specifically programmed to detect foreign cards and present conversion options that maximize their profit margins.

For example, withdrawing €200 might show: "Convert to INR at rate 1 EUR = 89.50 INR? Total: ₹17,900." Meanwhile, your bank's rate might be 1 EUR = 87.20 INR, making the actual cost ₹17,440. You pay ₹460 extra for this service.

Retail terminals in airports, hotels, and tourist areas frequently offer DCC. The system is designed to make DCC seem like the recommended choice, even though it costs more.

The cashier might even recommend it as easier or safer for foreign customers. These systems often default to DCC, requiring you to actively decline. The markup is typically 3-6%, which seems small but adds up quickly on larger purchases. A ₹50,000 business expense becomes ₹53,000 with DCC markup.

E-commerce websites and digital service providers increasingly offer DCC at checkout. This appears as a currency toggle or automatic conversion based on your IP address.

Online DCC can be tricky to spot, as some sites show prices in your currency by default, making it hard to notice that conversion is happening. Always check if you can switch to the original currency before completing payment.

While DCC comes with additional costs, there are specific situations where businesses might find value in the service. Here's why some companies consider using DCC despite the higher fees.

DCC's convenience comes with several costly trade-offs that can impact your business finances. The markup fees and rate differences often outweigh any perceived benefits.

It typically depends on your specific situation, but local currency typically offers better value. Here's how to evaluate your options:

Banks typically offer better rates and lower total costs compared to DCC, even when you factor in foreign transaction fees. Here's why local currency payments usually save money.

There are limited scenarios where DCC could justify its higher costs, though these situations usually indicate a need for better payment solutions overall.

Even in these situations, the convenience costs 3-6% extra. For most businesses, setting up proper multi-currency payment collection removes the need for DCC entirely.

DCC costs come from multiple sources, often bundled together in ways that can be difficult to spot. Here's how the fees break down.

Smart businesses develop clear guidelines for handling DCC offers to make informed decisions. Following these practices helps you manage your international transactions effectively:

DCC might promise convenience, but it comes with expensive trade-offs that reduce your profits. If you're regularly collecting payments from international clients or making global payments, you need a solution built for global business.

Traditional payment methods force you to choose between transparency and cost-effectiveness. You either accept expensive DCC markups or deal with unpredictable bank conversion rates and foreign transaction fees.

PayGlocal removes this tradeoff entirely and offers a better alternative solution. Here are some of the different ways PayGlocal supports your international payment processes:

Whether you're a freelancer invoicing international clients or an exporter receiving payments from global buyers, PayGlocal helps you collect payments faster, cheaper, and with complete transparency.

Dynamic currency conversion offers upfront pricing transparency for international transactions, but this convenience typically comes with higher costs than traditional bank conversion.

For occasional travelers, the impact might be manageable. But for businesses handling regular international payments, DCC fees add up to significant costs that directly impact profitability and cash flow. Modern payment solutions like PayGlocal offer multi-currency accounts that let you collect directly in your clients' currencies without DCC markups or conversion headaches.

Ready to save on currency conversion costs and collect faster global payments? Get started with PayGlocal today.

You might see DCC when paying overseas suppliers or receiving payments from international clients. While DCC ensures transparency and ease in transactions, it often comes with higher fees and high exchange rates that can impact your business expenses.

In this guide, we break down exactly how dynamic currency conversion works, when it might be useful, and what challenges it presents. We also cover what alternatives exist for businesses that need reliable, cost-effective international payment processing.

Key Takeaways:

- DCC shows upfront costs: Dynamic currency conversion displays exact amounts in your home currency at the point of sale for complete transparency.

- It's widely available: DCC appears at ATMs, point-of-sale terminals, and online checkouts worldwide, targeting international travelers and businesses.

- Rates vary significantly: DCC uses different exchange rates than banks, typically with markup fees of 3-6% above standard conversion rates.

- Better options exist: PayGlocal offers multi-currency accounts with transparent pricing and local payment collection in USD, EUR, GBP, and CAD.

What is dynamic currency conversion?

Dynamic Currency Conversion (DCC) is a service that lets you pay for international transactions in your home currency instead of the local currency. When you're traveling or making cross-border payments, DCC converts the transaction amount at the point of sale, showing you the exact cost in your familiar currency.

Let’s say, you're buying software from a US company, and the bill is $500. With DCC, instead of paying in US dollars and letting your bank convert it later, the merchant's payment system converts it immediately to INR, say ₹42,000, and shows you this amount upfront.

You see exactly what you'll pay without doing mental math or worrying about surprise charges on your statement. For businesses managing budgets and cash flow, this transparency can feel valuable.

DCC operates through agreements between merchants, payment processors, and acquiring banks. The service is offered at millions of locations worldwide, from hotel check-ins to online purchases, making it one of the most common currency services travelers and businesses encounter.

How does dynamic currency conversion work?

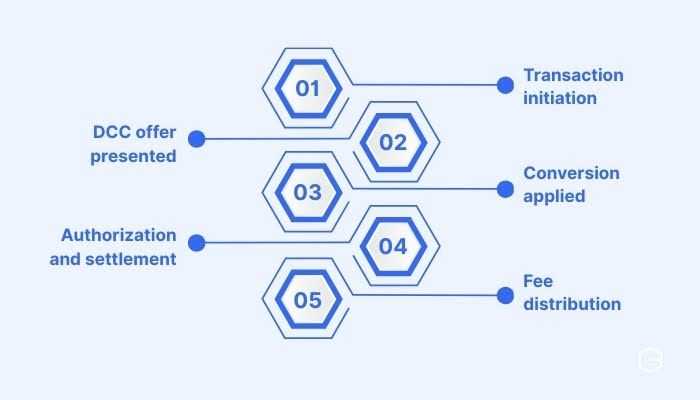

DCC operates through a chain of agreements between merchants, payment processors, and acquiring banks. When you initiate a transaction, the system detects your card's country of origin and offers the conversion option. Here’s how the process works:

- Transaction initiation: You swipe or insert your card at a terminal or enter details online. The system reads your card's Bank Identification Number (BIN) to determine your home currency.

- DCC offer presented: The terminal or checkout page displays two options: pay in local currency or your home currency. The DCC option shows the converted amount, exchange rate, and sometimes additional fees.

- Conversion applied: If you choose DCC, the merchant's acquiring bank or payment processor converts the amount using their predetermined exchange rate, which includes their profit margin.

- Authorization and settlement: The transaction processes in your home currency. Your bank sees it as a domestic transaction and typically doesn't apply foreign transaction fees.

= Fee distribution: The markup from the exchange rate gets split between the merchant, payment processor, and acquiring bank as revenue.

What are the types of dynamic currency conversion?

Different platforms and locations offer DCC in various forms, each with specific characteristics that affect your costs and experience.

Each type operates differently based on location and payment method. Here's how they work in practice and when you might encounter them.

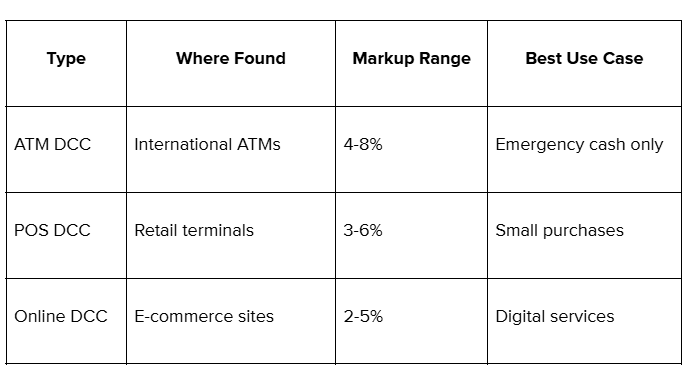

ATM dynamic currency conversion

ATMs worldwide offer DCC when you withdraw cash or check balances. These machines are specifically programmed to detect foreign cards and present conversion options that maximize their profit margins.

For example, withdrawing €200 might show: "Convert to INR at rate 1 EUR = 89.50 INR? Total: ₹17,900." Meanwhile, your bank's rate might be 1 EUR = 87.20 INR, making the actual cost ₹17,440. You pay ₹460 extra for this service.

Point-of-sale DCC

Retail terminals in airports, hotels, and tourist areas frequently offer DCC. The system is designed to make DCC seem like the recommended choice, even though it costs more.

The cashier might even recommend it as easier or safer for foreign customers. These systems often default to DCC, requiring you to actively decline. The markup is typically 3-6%, which seems small but adds up quickly on larger purchases. A ₹50,000 business expense becomes ₹53,000 with DCC markup.

Online DCC

E-commerce websites and digital service providers increasingly offer DCC at checkout. This appears as a currency toggle or automatic conversion based on your IP address.

Online DCC can be tricky to spot, as some sites show prices in your currency by default, making it hard to notice that conversion is happening. Always check if you can switch to the original currency before completing payment.

What are the benefits of DCC?

While DCC comes with additional costs, there are specific situations where businesses might find value in the service. Here's why some companies consider using DCC despite the higher fees.

- Upfront clarity: You know exactly what you'll pay in your familiar currency before completing the transaction.

- Budget control: Easier to track expenses against predetermined budgets without waiting for bank statements.

- No foreign transaction fees: Your bank treats it as a domestic transaction, avoiding additional fees.

- Immediate confirmation: Hotel and rental deposits show precise amounts for authorization purposes.

- Simplified accounting: Payments appear in your home currency on statements, reducing conversion calculations.

What challenges come with using DCC?

DCC's convenience comes with several costly trade-offs that can impact your business finances. The markup fees and rate differences often outweigh any perceived benefits.

- Higher exchange rates: Conversion rates are typically 3-8% worse than interbank rates or your bank's rates.

- Hidden markup fees: The service comes with substantial built-in costs that aren't always clearly disclosed.

- Compounds with fees: Some cards still charge foreign transaction fees even with DCC, creating double charges.

- Rate timing issues: DCC systems often use outdated exchange rates rather than real-time market rates.

Should you use DCC or pay in local currency?

It typically depends on your specific situation, but local currency typically offers better value. Here's how to evaluate your options:

When local currency is better:

Banks typically offer better rates and lower total costs compared to DCC, even when you factor in foreign transaction fees. Here's why local currency payments usually save money.

- Better exchange rates: Banks typically offer rates within 1-2% of interbank rates, compared to DCC markups of 3-8%.

- Competitive fees: Even with foreign transaction fees, total costs stay lower. For instance, a 2.5% bank fee is better than a 6% DCC markup.

- Real-time rates: Banks use current exchange rates, while DCC systems often use day-old rates with additional padding.

- Transparency: Your bank statement shows the original amount and conversion details, making expense tracking cleaner.

When DCC is a better option:

There are limited scenarios where DCC could justify its higher costs, though these situations usually indicate a need for better payment solutions overall.

- Strict budget constraints: If you absolutely must know the exact cost upfront for authorization purposes and can't afford any variance.

- Small transactions: On purchases under ₹500, the absolute difference might be minimal enough to justify convenience.

- Corporate policies: Some companies require upfront cost certainty for compliance reasons.

Even in these situations, the convenience costs 3-6% extra. For most businesses, setting up proper multi-currency payment collection removes the need for DCC entirely.

What fees are associated with dynamic currency conversion?

DCC costs come from multiple sources, often bundled together in ways that can be difficult to spot. Here's how the fees break down.

- Markup on exchange rates: This is the biggest cost. DCC providers buy currency at interbank rates (say, 1 USD = 83.00 INR) but sell to you at marked-up rates (1 USD = 85.50 INR). That 2.50 INR difference per dollar is pure profit, costing you 3% on the conversion alone.

- Service fees: Some DCC providers charge flat fees on top of poor rates. A service fee of ₹50-200 might appear for smaller transactions, making the total cost even worse.

- Merchant commissions: Merchants earn 0.5-2% commission for offering DCC. This cost ultimately comes from your markup fees.

- Hidden transaction fees: Some banks might also charge foreign transaction fees on DCC purchases, creating double charges that can push total costs to 8-10%.

What are the best practices for dynamic currency conversion?

Smart businesses develop clear guidelines for handling DCC offers to make informed decisions. Following these practices helps you manage your international transactions effectively:

- Compare total costs: Calculate DCC fees against your bank's foreign transaction fees plus exchange rate differences before choosing.

- Read all terms: Look for additional fees, exchange rate margins, and settlement timeframes in DCC offers.

- Train your team: Educate employees on DCC costs and benefits so they can make informed payment decisions.

- Monitor exchange rates: Track currency fluctuations to understand when DCC rates might be competitive with bank rates.

- Document transactions: Keep detailed records of DCC choices and costs for accounting and expense analysis.

- Review regularly: Assess your international payment methods quarterly to ensure you're getting the best rates available.

- Consider alternatives: Evaluate multi-currency accounts and other payment solutions that might offer better value.

- Plan ahead: For predictable expenses, consider forward contracts or other hedging options to lock in favorable rates.

Collect payments globally and settle locally with PayGlocal

DCC might promise convenience, but it comes with expensive trade-offs that reduce your profits. If you're regularly collecting payments from international clients or making global payments, you need a solution built for global business.

Traditional payment methods force you to choose between transparency and cost-effectiveness. You either accept expensive DCC markups or deal with unpredictable bank conversion rates and foreign transaction fees.

PayGlocal removes this tradeoff entirely and offers a better alternative solution. Here are some of the different ways PayGlocal supports your international payment processes:

- Local accounts in USD, GBP, EUR, CAD: Your international clients pay to local accounts, avoiding cross-border fees and delays.

- Instant compliance documentation: Auto-generated FIRC and other compliance docs reduce paperwork delays.

- One platform management: Track all currencies, transactions, and settlements from a single dashboard.

- Zero setup fees: Pay only when you transact, with no monthly fees or minimum commitments.

- Real-time notifications: Get instant updates on payment status, currency fluctuations, and settlement timelines.

Whether you're a freelancer invoicing international clients or an exporter receiving payments from global buyers, PayGlocal helps you collect payments faster, cheaper, and with complete transparency.

Final thoughts

Dynamic currency conversion offers upfront pricing transparency for international transactions, but this convenience typically comes with higher costs than traditional bank conversion.

For occasional travelers, the impact might be manageable. But for businesses handling regular international payments, DCC fees add up to significant costs that directly impact profitability and cash flow. Modern payment solutions like PayGlocal offer multi-currency accounts that let you collect directly in your clients' currencies without DCC markups or conversion headaches.

Ready to save on currency conversion costs and collect faster global payments? Get started with PayGlocal today.