According to recent data, the country is expected to grow at 6.8% in 2025-26, making it the fastest-growing major economy in the world.

To keep up with the rapid growth and take full advantage of new opportunities, you need enough cash on hand to run operations smoothly. This is where working capital comes in. It tells you whether your business has enough liquid resources to keep operations running without scrambling for loans or delaying payments.

If you're managing a business that deals with international clients, working capital becomes even more critical. Payment delays, currency conversion wait times, and settlement lags can drain your liquidity fast. Let’s take a detailed look at what working capital is, how to calculate it, and effective steps to improve it.

Working capital is the money your business has available for day-to-day operations after covering immediate obligations.

In simple terms, working capital tells you if you have enough liquid resources to pay suppliers, cover payroll, buy inventory, and handle other short-term expenses without borrowing money or selling assets.

Positive working capital means you're in good shape. Negative working capital means your short-term debts exceed your available assets, which can signal trouble.

For instance, if your business has ₹50 lakh in current assets (cash, receivables, inventory) and ₹30 lakh in current liabilities (payables, short-term loans), your working capital is ₹20 lakh. That's the cushion you have to run operations smoothly.

Working capital isn't static. It fluctuates based on sales cycles, payment terms, and how quickly you collect from clients.

Working capital directly affects your ability to operate without disruptions. When you have positive working capital, you can pay suppliers on time, take advantage of bulk purchase discounts, invest in marketing, and handle unexpected expenses without panic. It gives you flexibility and control over your business decisions.

Negative working capital doesn't always mean disaster, but it's a warning sign. It means your short-term liabilities are larger than your liquid assets. For growing businesses, this can limit your ability to scale or seize new opportunities.

Here's why working capital matters:

For businesses collecting payments from global clients, working capital takes on added importance.

International payment delays, currency conversion timelines, and platform settlement lags can tie up funds for days or weeks. If your working capital is already tight, these delays can force you to take expensive short-term loans just to keep operations running.

Calculating working capital is simple. You need two numbers from your balance sheet: current assets and current liabilities.

Working Capital Formula:

Working Capital = Current Assets - Current Liabilities

Here's what goes into each part:

Current assets

Current assets are resources you can convert to cash within one year. These include:

Current liabilities

Current liabilities are obligations you need to pay within one year. These include:

Example:

Your business has:

Working Capital = ₹80 lakh - ₹50 lakh = ₹30 lakh

This means you have ₹30 lakh available to run daily operations after covering immediate debts.

Tracking this number monthly helps you spot trends. If working capital is shrinking, you know you need to collect receivables faster, reduce inventory, or negotiate better payment terms with suppliers.

The working capital cycle (also called the cash conversion cycle) measures how long it takes for your business to convert inventory and receivables into cash.

Here's how it works:

The cycle repeats. The shorter your working capital cycle, the faster you convert investments into cash, which improves liquidity.

Formula:

Working Capital Cycle = Inventory Days + Receivables Days - Payables Days

Example:

Working Capital Cycle = 20 + 40 - 30 = 30 days

This means it takes 30 days from the time you invest cash into inventory until you get paid. A shorter cycle is better because cash isn't tied up as long.

For businesses doing international transactions, receivables days often stretch due to international payment delays. If your overseas clients take 45-60 days to pay instead of 30, your working capital cycle extends, putting pressure on liquidity.

There are different types of working capital based on business needs, seasonal cycles, and operational requirements.

Here's how the main types compare:

Let’s take a look at each type in detail.

This is the baseline amount of working capital your business needs to operate every day, regardless of season or sales cycles. It covers fixed costs like rent, salaries, utilities, and minimum inventory levels.

For example, if you run a SaaS company, your permanent working capital covers server costs, team salaries, and software subscriptions. This amount stays relatively stable throughout the year.

This is extra working capital you need during peak periods, seasonal demand spikes, or one-off projects. It's not part of your regular operations but becomes necessary when demand increases.

For instance, an exporter might need temporary working capital to fulfill a large international order that requires upfront inventory purchases. Once the payment is collected, this extra capital is no longer needed.

Gross working capital refers to the total value of your current assets without subtracting liabilities. It gives you a sense of the overall resources available but doesn't reflect liquidity or your ability to meet obligations.

For example, if your business has ₹1 crore in current assets (cash, receivables, inventory), your gross working capital is ₹1 crore. This number shows your asset base but doesn't tell you if you can cover immediate debts.

Net working capital is the standard measure: current assets minus current liabilities. This is the number most businesses track because it directly reflects liquidity and the ability to cover short-term debts.

For instance, if you have ₹80 lakh in current assets and ₹50 lakh in current liabilities, your net working capital is ₹30 lakh. This shows you have ₹30 lakh available for operations after meeting short-term obligations.

Positive working capital means your current assets exceed your current liabilities. You have enough liquid resources to cover short-term obligations and invest in growth.

For example, if you have ₹60 lakh in current assets and ₹40 lakh in current liabilities, your working capital is ₹20 lakh. You're in a comfortable position to handle expenses and unexpected costs without borrowing.

This happens when liabilities exceed assets. While it can signal trouble, some business models thrive with negative working capital. Retailers that collect cash upfront and pay suppliers later can operate this way successfully.

For instance, if you have ₹30 lakh in current assets and ₹50 lakh in current liabilities, your working capital is -₹20 lakh. Unless you have a business model that supports this (like collecting payments upfront), you'll need to improve collections or reduce short-term debt.

Note: For most service exporters and SaaS businesses dealing with international clients, positive working capital is essential because payment delays can stretch for weeks.

Improving working capital comes down to three main components: speeding up cash inflows, slowing down cash outflows, and optimizing asset use. Here's how you can improve your working capital effectively:

For businesses collecting payments from international clients, the biggest working capital drain is slow settlement times. Traditional payment methods can take 3–7 days or longer, during which your cash is stuck in transit. Choosing a payment platform that settles funds quickly and transparently can significantly improve your working capital position.

Working capital management gets complicated when you're dealing with international clients. Payment delays, high transaction fees, currency conversion wait times, and compliance paperwork can tie up cash for weeks.

If you're exporting goods or services, freelancing for global clients, or running a business that serves customers in multiple countries, your working capital depends on how quickly you can collect and settle international payments.

PayGlocal helps you improve working capital by making global payment collection faster, cheaper, and more transparent. Here's how:

Whether you're invoicing a client, collecting subscription payments, or settling marketplace payouts, PayGlocal ensures your international payments don't become a working capital bottleneck.

Working capital is one of the most important metrics for running a healthy business. It tells you whether you have enough liquid resources to cover short-term obligations, invest in growth, and handle unexpected expenses without borrowing.

For businesses dealing with international clients, working capital management becomes even more critical. The faster you collect payments, the more liquidity you have available to grow your business.

Stop waiting weeks for international payments. Get started with PayGlocal today and accept payments from global clients faster, cheaper, and with full compliance.

To keep up with the rapid growth and take full advantage of new opportunities, you need enough cash on hand to run operations smoothly. This is where working capital comes in. It tells you whether your business has enough liquid resources to keep operations running without scrambling for loans or delaying payments.

If you're managing a business that deals with international clients, working capital becomes even more critical. Payment delays, currency conversion wait times, and settlement lags can drain your liquidity fast. Let’s take a detailed look at what working capital is, how to calculate it, and effective steps to improve it.

Key takeaways

- Working capital basics: Working capital is the difference between your current assets and current liabilities. It shows whether you can meet short-term obligations.

- Why it matters: Positive working capital means you have enough funds for daily operations. Negative working capital signals potential liquidity problems.

- Calculation is simple: Use the formula: Working Capital = Current Assets - Current Liabilities. Track it regularly to spot cash flow issues early.

- Improve through better receivables: Faster payment collection directly improves working capital. International payments can create delays that tie up your funds.

- Global payments: PayGlocal helps you accept international payments faster with transparent pricing and instant compliance documentation, so your working capital stays strong.

What is working capital?

Working capital is the money your business has available for day-to-day operations after covering immediate obligations.

In simple terms, working capital tells you if you have enough liquid resources to pay suppliers, cover payroll, buy inventory, and handle other short-term expenses without borrowing money or selling assets.

Positive working capital means you're in good shape. Negative working capital means your short-term debts exceed your available assets, which can signal trouble.

For instance, if your business has ₹50 lakh in current assets (cash, receivables, inventory) and ₹30 lakh in current liabilities (payables, short-term loans), your working capital is ₹20 lakh. That's the cushion you have to run operations smoothly.

Working capital isn't static. It fluctuates based on sales cycles, payment terms, and how quickly you collect from clients.

Why is working capital important?

Working capital directly affects your ability to operate without disruptions. When you have positive working capital, you can pay suppliers on time, take advantage of bulk purchase discounts, invest in marketing, and handle unexpected expenses without panic. It gives you flexibility and control over your business decisions.

Negative working capital doesn't always mean disaster, but it's a warning sign. It means your short-term liabilities are larger than your liquid assets. For growing businesses, this can limit your ability to scale or seize new opportunities.

Here's why working capital matters:

- Operational stability: You can cover expenses like rent, salaries, and vendor payments without delays or borrowing.

- Growth funding: Positive working capital gives you the freedom to invest in new projects, hire talent, or expand into new markets.

- Creditworthiness: Lenders and investors look at working capital to assess financial health. Strong working capital improves your chances of securing loans or funding.

- Supplier relationships: Paying on time builds trust with vendors, which can lead to better terms, discounts, or priority service.

- Cash flow buffer: It acts as a safety net during slow months, seasonal dips, or when clients delay payments.

For businesses collecting payments from global clients, working capital takes on added importance.

International payment delays, currency conversion timelines, and platform settlement lags can tie up funds for days or weeks. If your working capital is already tight, these delays can force you to take expensive short-term loans just to keep operations running.

How to calculate working capital?

Calculating working capital is simple. You need two numbers from your balance sheet: current assets and current liabilities.

Working Capital Formula:

Working Capital = Current Assets - Current Liabilities

Here's what goes into each part:

Current assets

Current assets are resources you can convert to cash within one year. These include:

- Cash and cash equivalents: Money in your bank accounts or highly liquid instruments.

- Accounts receivable: Money your clients owe you for goods or services delivered.

- Inventory: Stock you plan to sell within the year.

- Prepaid expenses: Costs you've paid in advance, like insurance or rent.

Current liabilities

Current liabilities are obligations you need to pay within one year. These include:

- Accounts payable: Money you owe suppliers or vendors.

- Short-term loans: Any debt due within 12 months.

- Accrued expenses: Costs you've incurred but haven't paid yet, like wages or taxes.

- Unearned revenue: Payments received in advance for services or products not yet delivered.

Example:

Your business has:

- Current Assets: ₹80 lakh (₹30 lakh cash, ₹35 lakh receivables, ₹15 lakh inventory)

- Current Liabilities: ₹50 lakh (₹25 lakh payables, ₹15 lakh short-term loan, ₹10 lakh accrued expenses)

Working Capital = ₹80 lakh - ₹50 lakh = ₹30 lakh

This means you have ₹30 lakh available to run daily operations after covering immediate debts.

Tracking this number monthly helps you spot trends. If working capital is shrinking, you know you need to collect receivables faster, reduce inventory, or negotiate better payment terms with suppliers.

What is the working capital cycle?

The working capital cycle (also called the cash conversion cycle) measures how long it takes for your business to convert inventory and receivables into cash.

Here's how it works:

- You buy inventory or invest in production: Cash goes out to purchase materials or pay for services.

- You deliver goods or services to clients: Inventory turns into accounts receivable.

- You collect payment from clients: Receivables turn into cash.

- You pay suppliers and vendors: Cash goes out to settle payables.

The cycle repeats. The shorter your working capital cycle, the faster you convert investments into cash, which improves liquidity.

Formula:

Working Capital Cycle = Inventory Days + Receivables Days - Payables Days

Example:

- You hold inventory for 20 days before selling.

- Clients take 40 days to pay after delivery.

- You pay suppliers in 30 days.

Working Capital Cycle = 20 + 40 - 30 = 30 days

This means it takes 30 days from the time you invest cash into inventory until you get paid. A shorter cycle is better because cash isn't tied up as long.

For businesses doing international transactions, receivables days often stretch due to international payment delays. If your overseas clients take 45-60 days to pay instead of 30, your working capital cycle extends, putting pressure on liquidity.

What are the types of working capital?

There are different types of working capital based on business needs, seasonal cycles, and operational requirements.

Here's how the main types compare:

Let’s take a look at each type in detail.

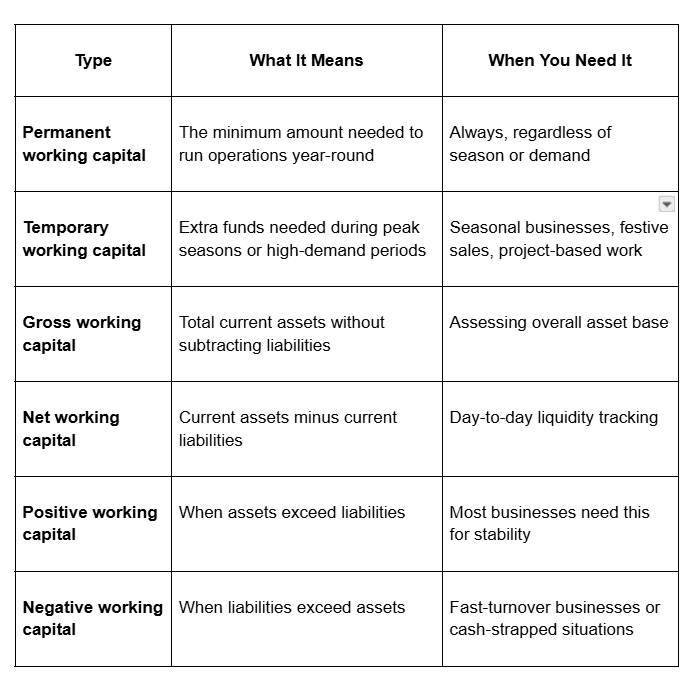

Permanent working capital

This is the baseline amount of working capital your business needs to operate every day, regardless of season or sales cycles. It covers fixed costs like rent, salaries, utilities, and minimum inventory levels.

For example, if you run a SaaS company, your permanent working capital covers server costs, team salaries, and software subscriptions. This amount stays relatively stable throughout the year.

Temporary working capital

This is extra working capital you need during peak periods, seasonal demand spikes, or one-off projects. It's not part of your regular operations but becomes necessary when demand increases.

For instance, an exporter might need temporary working capital to fulfill a large international order that requires upfront inventory purchases. Once the payment is collected, this extra capital is no longer needed.

Gross working capital

Gross working capital refers to the total value of your current assets without subtracting liabilities. It gives you a sense of the overall resources available but doesn't reflect liquidity or your ability to meet obligations.

For example, if your business has ₹1 crore in current assets (cash, receivables, inventory), your gross working capital is ₹1 crore. This number shows your asset base but doesn't tell you if you can cover immediate debts.

Net working capital

Net working capital is the standard measure: current assets minus current liabilities. This is the number most businesses track because it directly reflects liquidity and the ability to cover short-term debts.

For instance, if you have ₹80 lakh in current assets and ₹50 lakh in current liabilities, your net working capital is ₹30 lakh. This shows you have ₹30 lakh available for operations after meeting short-term obligations.

Positive working capital

Positive working capital means your current assets exceed your current liabilities. You have enough liquid resources to cover short-term obligations and invest in growth.

For example, if you have ₹60 lakh in current assets and ₹40 lakh in current liabilities, your working capital is ₹20 lakh. You're in a comfortable position to handle expenses and unexpected costs without borrowing.

Negative working capital

This happens when liabilities exceed assets. While it can signal trouble, some business models thrive with negative working capital. Retailers that collect cash upfront and pay suppliers later can operate this way successfully.

For instance, if you have ₹30 lakh in current assets and ₹50 lakh in current liabilities, your working capital is -₹20 lakh. Unless you have a business model that supports this (like collecting payments upfront), you'll need to improve collections or reduce short-term debt.

Note: For most service exporters and SaaS businesses dealing with international clients, positive working capital is essential because payment delays can stretch for weeks.

How to improve your working capital?

Improving working capital comes down to three main components: speeding up cash inflows, slowing down cash outflows, and optimizing asset use. Here's how you can improve your working capital effectively:

- Collect receivables faster: The quicker you get paid, the more working capital you have. Offer early payment discounts, send invoices immediately after delivery, and follow up on overdue accounts. For businesses collecting international payments, choose platforms that settle funds quickly without hidden delays.

- Negotiate better payment terms with suppliers: Extend your payment terms from 30 days to 45 or 60 days if possible. This keeps cash in your business longer without affecting supplier relationships.

- Reduce inventory holding costs: Excess inventory ties up cash. Use just-in-time inventory management, forecast demand accurately, and clear out slow-moving stock with discounts or promotions.

- Shorten your cash conversion cycle: The cash conversion cycle measures how long it takes to convert inventory and receivables into cash. Reduce this by speeding up production, delivering faster, and collecting payments sooner.

- Use working capital loans carefully: Short-term loans can bridge cash flow gaps but add to liabilities. Use them only when necessary.

- Automate invoicing and payment tracking: Use automated systems to send invoices instantly, track payment status, and send reminders.

- Improve pricing and margins: Higher margins give you more cash per sale, directly boosting working capital.

For businesses collecting payments from international clients, the biggest working capital drain is slow settlement times. Traditional payment methods can take 3–7 days or longer, during which your cash is stuck in transit. Choosing a payment platform that settles funds quickly and transparently can significantly improve your working capital position.

Accept global payments faster and scale your business

Working capital management gets complicated when you're dealing with international clients. Payment delays, high transaction fees, currency conversion wait times, and compliance paperwork can tie up cash for weeks.

If you're exporting goods or services, freelancing for global clients, or running a business that serves customers in multiple countries, your working capital depends on how quickly you can collect and settle international payments.

PayGlocal helps you improve working capital by making global payment collection faster, cheaper, and more transparent. Here's how:

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD.

- Global payment methods: Accept 40+ local payment methods from 180+ countries.

- Card payments: Process international credit and debit card payments with high approval rates.

- Instant compliance documentation: Get FIRC (Foreign Inward Remittance Certificate) automatically after settlement.

- Transparent pricing with zero fixed costs: Pay only when you transact.

Whether you're invoicing a client, collecting subscription payments, or settling marketplace payouts, PayGlocal ensures your international payments don't become a working capital bottleneck.

Final thoughts

Working capital is one of the most important metrics for running a healthy business. It tells you whether you have enough liquid resources to cover short-term obligations, invest in growth, and handle unexpected expenses without borrowing.

For businesses dealing with international clients, working capital management becomes even more critical. The faster you collect payments, the more liquidity you have available to grow your business.

Stop waiting weeks for international payments. Get started with PayGlocal today and accept payments from global clients faster, cheaper, and with full compliance.