India has reached an 87% fintech adoption rate, far ahead of the 67% global average. This shows that Indian businesses are actively using modern digital financial solutions to scale and serve customers better.

If you're looking to accept payments globally or offer financial features without becoming a bank, Banking as a Service is the solution you need. BaaS lets you integrate banking capabilities into your platform without obtaining licenses or building infrastructure from scratch.

In this guide, we break down in detail what BaaS service really means, how it works, the benefits, and how to choose the right solution for your needs. Let’s get into it.

BaaS service, or Banking as a Service, is a model where licensed banks provide their financial infrastructure to other companies through APIs. Instead of building banking capabilities from scratch or becoming a licensed bank yourself, you integrate ready-made banking features into your platform.

Think of it as renting banking infrastructure instead of building it. A licensed bank handles all the regulatory compliance, capital requirements, and security protocols.

You get access to their systems through APIs and can offer features like payment processing, account creation, or loan disbursement under your own brand. Your customers interact with your interface while the actual banking operations happen in the background through your partner bank.

For example, a freelance platform might use BaaS to let users receive payments from clients worldwide directly into virtual accounts, all while the platform maintains its own branding. The platform doesn't need a banking license because the partner bank provides the regulated infrastructure.

This is especially helpful for businesses expanding globally, as traditional banking relationships often have lengthy approval processes and limited flexibility. BaaS removes these barriers and gives you banking capabilities at scale without the overhead.

Banking as a Service connects licensed banks with businesses through APIs. When you use BaaS, transactions flow through a simple process that happens in seconds. Here's how BaaS works step-by-step:

This entire process takes seconds. You can launch banking features in weeks without obtaining licenses or building infrastructure yourself.

Banking as a Service offers clear advantages for different stakeholders in the financial ecosystem. Here's what you gain by using BaaS:

Real-world applications show how BaaS works in practice across different industries and use cases. These examples demonstrate the flexibility and power of Banking as a Service. Here's how different businesses use BaaS:

Real-world applications show how BaaS works in practice across different industries and use cases. These examples demonstrate the flexibility and power of Banking as a Service. Here's how different businesses use BaaS:

Here's how these work in practice:

Online sellers use BaaS to accept payments in multiple currencies. They don't need to set up merchant accounts in each country. The BaaS provider handles currency conversion, compliance, and settlement. The seller maintains their branding throughout.

For instance, an Indian exporter can receive USD payments. These payments automatically convert and settle in INR. The exporter gets proper documentation for tax purposes.

Platforms that connect freelancers with clients use BaaS to create virtual accounts for each user. Freelancers receive payments directly into these accounts. They can withdraw funds when needed. They also get automatic invoicing and tax documentation.

The platform never touches the money directly. It provides a seamless banking experience under its own brand.

SaaS companies integrate recurring payment capabilities. These automatically charge customers based on usage or subscription tiers. The BaaS infrastructure handles payment retries, updates card information, and manages payment methods across different countries. This reduces failed payments and improves cash flow predictability.

Retail platforms offer financing options at the point of sale. They don't need to become lenders themselves. When a customer chooses to pay in installments, the BaaS provider performs instant credit checks. It disburses funds to the merchant and manages the loan. The customer sees a branded checkout experience.

Companies doing business across borders use BaaS to maintain accounts in different currencies. They receive payments in USD, EUR, or GBP. They can hold funds in those currencies to avoid conversion costs. They transfer to local currency only when it is favorable. For example, an Indian software company can maintain a USD account for US clients. They settle in INR for local expenses.

Travel booking platforms offer insurance during checkout. They integrate insurance products through BaaS providers. The platform earns commission on insurance sales. Customers get instant coverage without leaving the booking flow.

Companies issue virtual or physical cards to employees for business expenses. This happens through BaaS platforms. They set spending limits and track expenses in real time. They automatically categorize transactions for accounting purposes. All of this happens without becoming a bank or card issuer.

Platforms that facilitate transactions between buyers and sellers use BaaS to hold funds in escrow. Money moves from the buyer to the escrow account. It is released to the seller after delivery confirmation. The system handles disputes automatically based on platform rules.

Selecting a BaaS provider requires a proper evaluation of several factors that directly impact your operations, costs, and customer experience. Here's what matters most when making this decision:

The right BaaS partner becomes a growth enabler, while the wrong one creates ongoing friction and hidden costs.

Banking as a Service solves infrastructure problems, but choosing the right provider determines whether you actually capture international revenue or lose it to failed transactions and poor customer experiences. If you're an Indian business selling globally, you face unique challenges that generic BaaS platforms don't address.

You need multi-currency capabilities, payment methods that your international customers trust, and settlements in INR with automatic documentation. Most importantly, you need success rates that don't leave money on the table.

PayGlocal builds Banking as a Service specifically for businesses like yours. Here's what you get:

PayGlocal removes the guesswork from international payments. You get transparent pricing, reliable performance, and support from teams who know cross-border commerce. Whether you're a freelancer receiving your first international payment or an exporter processing thousands of transactions monthly, the platform scales with your needs.

Banking as a Service changes how businesses access financial infrastructure. Instead of spending months obtaining licenses and building systems, you can integrate banking capabilities in weeks through APIs. This matters because speed and flexibility determine who wins in competitive markets.

The right BaaS provider gives you more than just technology. You get compliance handled automatically, access to payment methods your customers prefer, and the ability to create seamless financial experiences under your own brand.

Don't let banking infrastructure slow your growth. The tools exist today to accept payments from anywhere, in any currency, with the same ease as a domestic transaction. You just need the right partner who handles the complexity while you focus on customers.

Ready to turn global payment acceptance from a challenge into an advantage? Get started with PayGlocal today and start collecting international payments with confidence.

If you're looking to accept payments globally or offer financial features without becoming a bank, Banking as a Service is the solution you need. BaaS lets you integrate banking capabilities into your platform without obtaining licenses or building infrastructure from scratch.

In this guide, we break down in detail what BaaS service really means, how it works, the benefits, and how to choose the right solution for your needs. Let’s get into it.

Key takeaways

- BaaS meaning: Banking as a Service lets non-bank businesses offer banking features like payments, accounts, and loans through APIs provided by licensed banks.

- How it works: Banks provide the infrastructure and regulatory compliance, while businesses integrate these capabilities into their own platforms.

- Top benefits: Faster market entry, lower setup costs, better customer experience, and no need to obtain banking licenses or build complex infrastructure.

- Who uses it: Fintech startups, e-commerce platforms, SaaS companies, and exporters who need to accept global payments or offer financial services to customers.

- Easy global payments: PayGlocal offers multi-currency accounts, global payment acceptance, and compliance automation specifically built for Indian businesses doing global commerce.

What is a BaaS service?

BaaS service, or Banking as a Service, is a model where licensed banks provide their financial infrastructure to other companies through APIs. Instead of building banking capabilities from scratch or becoming a licensed bank yourself, you integrate ready-made banking features into your platform.

Think of it as renting banking infrastructure instead of building it. A licensed bank handles all the regulatory compliance, capital requirements, and security protocols.

You get access to their systems through APIs and can offer features like payment processing, account creation, or loan disbursement under your own brand. Your customers interact with your interface while the actual banking operations happen in the background through your partner bank.

For example, a freelance platform might use BaaS to let users receive payments from clients worldwide directly into virtual accounts, all while the platform maintains its own branding. The platform doesn't need a banking license because the partner bank provides the regulated infrastructure.

This is especially helpful for businesses expanding globally, as traditional banking relationships often have lengthy approval processes and limited flexibility. BaaS removes these barriers and gives you banking capabilities at scale without the overhead.

How does Banking as a Service work?

Banking as a Service connects licensed banks with businesses through APIs. When you use BaaS, transactions flow through a simple process that happens in seconds. Here's how BaaS works step-by-step:

- Licensed bank provides infrastructure: The bank maintains regulatory compliance, holds required licenses, and operates payment systems with APIs.

- You integrate into your product: Your business adds the bank's APIs to your website or app for customers to use.

- Customer makes a transaction: Your customer initiates a payment or account action through your branded interface.

- Request goes to the bank: Your system sends transaction details to the bank through the API.

- Bank executes the transaction: The bank processes the payment, performs compliance checks, and moves the funds.

- Confirmation returns instantly: The bank confirms back to your system, updating everything in real time.

This entire process takes seconds. You can launch banking features in weeks without obtaining licenses or building infrastructure yourself.

What are the benefits of the BaaS service?

Banking as a Service offers clear advantages for different stakeholders in the financial ecosystem. Here's what you gain by using BaaS:

- Faster time to market: You can launch financial features in weeks instead of spending years obtaining banking licenses and building infrastructure. Integration through APIs means you connect existing systems rather than building from scratch.

- Lower entry costs: No need to invest in banking infrastructure, hire compliance teams, or maintain capital requirements that banks face. You pay for what you use, turning fixed costs into variable ones that scale with your business.

- Regulatory compliance handled: The licensed bank manages all regulatory requirements, from know-your-customer checks to other regulatory protocols. You get compliance as a built-in feature rather than a separate burden.

- Better customer experience: You can embed financial services directly into your existing customer journey instead of sending users to third-party banking sites. For instance, an e-commerce platform can offer instant checkout financing without redirecting customers elsewhere.

- Access to global markets: BaaS providers often support multiple currencies and international payment methods, letting you accept payments from customers worldwide without setting up banking relationships in each country.

- Scalability without friction: As your transaction volumes grow, the infrastructure scales automatically. You don’t need to renegotiate contracts or upgrade systems to handle increased load.

- Focus on core business: Instead of becoming experts in banking regulations and financial infrastructure, you can focus on your product, customers, and competitive advantages while leaving the banking complexity to specialists.

- Revenue opportunities: You can generate additional revenue by offering financial services to your customers or taking a share of transaction fees, all without the overhead of traditional financial service providers.

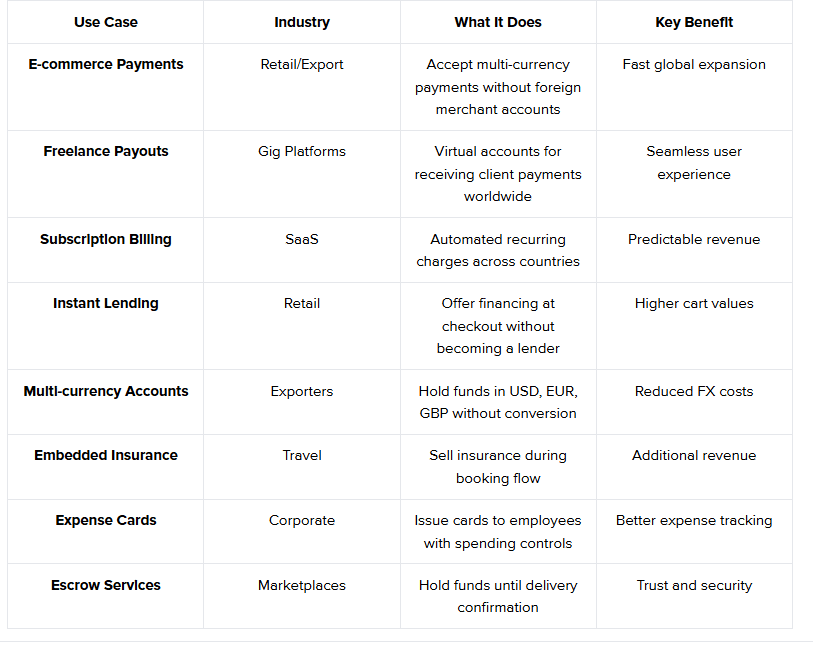

What are the use cases of Banking as a Service?

Real-world applications show how BaaS works in practice across different industries and use cases. These examples demonstrate the flexibility and power of Banking as a Service. Here's how different businesses use BaaS:

Real-world applications show how BaaS works in practice across different industries and use cases. These examples demonstrate the flexibility and power of Banking as a Service. Here's how different businesses use BaaS:

Here's how these work in practice:

E-commerce payment acceptance

Online sellers use BaaS to accept payments in multiple currencies. They don't need to set up merchant accounts in each country. The BaaS provider handles currency conversion, compliance, and settlement. The seller maintains their branding throughout.

For instance, an Indian exporter can receive USD payments. These payments automatically convert and settle in INR. The exporter gets proper documentation for tax purposes.

Freelance platform payouts

Platforms that connect freelancers with clients use BaaS to create virtual accounts for each user. Freelancers receive payments directly into these accounts. They can withdraw funds when needed. They also get automatic invoicing and tax documentation.

The platform never touches the money directly. It provides a seamless banking experience under its own brand.

Subscription billing

SaaS companies integrate recurring payment capabilities. These automatically charge customers based on usage or subscription tiers. The BaaS infrastructure handles payment retries, updates card information, and manages payment methods across different countries. This reduces failed payments and improves cash flow predictability.

Instant lending at checkout

Retail platforms offer financing options at the point of sale. They don't need to become lenders themselves. When a customer chooses to pay in installments, the BaaS provider performs instant credit checks. It disburses funds to the merchant and manages the loan. The customer sees a branded checkout experience.

Multi-currency business accounts

Companies doing business across borders use BaaS to maintain accounts in different currencies. They receive payments in USD, EUR, or GBP. They can hold funds in those currencies to avoid conversion costs. They transfer to local currency only when it is favorable. For example, an Indian software company can maintain a USD account for US clients. They settle in INR for local expenses.

Embedded insurance

Travel booking platforms offer insurance during checkout. They integrate insurance products through BaaS providers. The platform earns commission on insurance sales. Customers get instant coverage without leaving the booking flow.

Corporate expense cards

Companies issue virtual or physical cards to employees for business expenses. This happens through BaaS platforms. They set spending limits and track expenses in real time. They automatically categorize transactions for accounting purposes. All of this happens without becoming a bank or card issuer.

Marketplace escrow services

Platforms that facilitate transactions between buyers and sellers use BaaS to hold funds in escrow. Money moves from the buyer to the escrow account. It is released to the seller after delivery confirmation. The system handles disputes automatically based on platform rules.

How to choose the right BaaS service for your business?

Selecting a BaaS provider requires a proper evaluation of several factors that directly impact your operations, costs, and customer experience. Here's what matters most when making this decision:

- Compliance and licensing: Verify that the provider partners with properly licensed banks and handles regulatory updates automatically.

- Payment methods and coverage: Look for providers supporting the payment methods and geographic regions your customers use.

- Pricing transparency: Learn about the complete fee structure and watch for hidden charges like withdrawal or inactivity penalties.

- Integration ease: Check how quickly you can launch with their documentation, pre-built integrations, and developer support.

- Success rates and reliability: Evaluate their payment approval rates, uptime statistics, and how they handle failed transactions.

- Support and service: Consider whether you get dedicated account management or only ticket-based support during operations.

- Reporting and analytics: Assess the visibility you'll have through real-time dashboards, reports, and data export options.

- Scalability and flexibility: Ensure the provider can handle higher volume and support new markets as you expand.

- Security and data protection: Verify their Payment Card Industry Data Security Standard (PCI DSS) compliance, encryption practices, and track record with fraud protection.

- Settlement speed and terms: Knowing how quickly funds reach your account and whether they hold reserves.

The right BaaS partner becomes a growth enabler, while the wrong one creates ongoing friction and hidden costs.

Accept global payments with confidence through PayGlocal

Banking as a Service solves infrastructure problems, but choosing the right provider determines whether you actually capture international revenue or lose it to failed transactions and poor customer experiences. If you're an Indian business selling globally, you face unique challenges that generic BaaS platforms don't address.

You need multi-currency capabilities, payment methods that your international customers trust, and settlements in INR with automatic documentation. Most importantly, you need success rates that don't leave money on the table.

PayGlocal builds Banking as a Service specifically for businesses like yours. Here's what you get:

- Multi-currency accounts: Accept payments in USD, GBP, EUR, and CAD through local accounts. Your international customers see familiar payment options while you receive funds efficiently.

- Dynamic checkout: Create payment experiences that match what your global customers expect. Fast, secure, and customizable checkout flows that work across devices and support multiple payment methods.

- Recurring payments: Handle subscriptions and recurring billing for international customers with network-compliant solutions. Auto-debit functionality keeps revenue flowing while reducing manual work and failed renewals.

- Instant compliance documentation: Receive the Foreign Inward Remittance Certificate (FIRC) automatically after settlement. Track payments through every stage with transparent dashboards and real-time notifications.

- Zero fixed costs: No setup fees, no platform fees, no documentation charges. Pay only when you transact, making it easy to start small and scale as you grow.

PayGlocal removes the guesswork from international payments. You get transparent pricing, reliable performance, and support from teams who know cross-border commerce. Whether you're a freelancer receiving your first international payment or an exporter processing thousands of transactions monthly, the platform scales with your needs.

Final thoughts

Banking as a Service changes how businesses access financial infrastructure. Instead of spending months obtaining licenses and building systems, you can integrate banking capabilities in weeks through APIs. This matters because speed and flexibility determine who wins in competitive markets.

The right BaaS provider gives you more than just technology. You get compliance handled automatically, access to payment methods your customers prefer, and the ability to create seamless financial experiences under your own brand.

Don't let banking infrastructure slow your growth. The tools exist today to accept payments from anywhere, in any currency, with the same ease as a domestic transaction. You just need the right partner who handles the complexity while you focus on customers.

Ready to turn global payment acceptance from a challenge into an advantage? Get started with PayGlocal today and start collecting international payments with confidence.