You worked hard to earn that international payment. The last thing you want is to lose a chunk of it to currency conversion every single time. That is exactly the problem the Exchange Earner's Foreign Currency (EEFC) account was built to solve, and yet most exporters either do not have one or are not using it optimally.

An Exchange Earner's Foreign Currency (EEFC) account is a non-interest-bearing current account held in a foreign currency, maintained with an authorized dealer essentially a bank authorized by the Reserve Bank of India (RBI) in India. The account enables exporters, service providers, and other foreign exchange earners to retain their foreign currency earnings without immediately converting them to Indian Rupees (INR).

Think of it as your 'forex parking account'. Instead of converting every dollar, euro, or pound you receive into INR the moment it hits your bank, you can hold that foreign currency in the EEFC account for a definite period of time and convert it when the rate is favorable, or use it directly for permissible foreign currency expenses without conversion altogether.

The operation of this account is governed by the Foreign Exchange Management Act (FEMA) 1999 and regulatory frameworks prescribed by RBI's Foreign Exchange Management (Deposit) Regulations.

Quick Snapshot

Before you rush to open one, here is the honest picture. EEFC accounts are powerful — but they are not for everyone or every situation.

EEFC accounts are tightly regulated. Not knowing the rules is not just a compliance risk — it can result in penalties under FEMA. Here is what you need to keep in mind:

RBI permits debit from an EEFC account for the following purposes:

Important: The 30-Day Rule

The sum of the accruals in the account during a calendar month should be converted into Rupees on or before the last day of the succeeding calendar month after adjusting for utilisation of the balances for approved purposes or forward commitments.

Any authorized dealer bank in India — basically any scheduled commercial bank — can open an EEFC account for you. There is no shortage of options; what matters is choosing a bank with strong trade finance infrastructure and competitive forex spreads.

*The feature highlight is illustrative in nature, and you are advised to consult with the respective banks for overall features.

* Document requirement may vary from bank to bank.

Most private sector banks now allow you to initiate the EEFC account application online. Processing time typically ranges from 2 to 5 working days once all documents are in order.

By default, PayGlocal settles your international collections into your INR current account. That works perfectly for most merchants — but if you already have an EEFC account, you have a better option.

Note: EEFC settlement through PayGlocal is available only for merchants who hold a Multi-Currency Account. PayGlocal enables this settlement under its RBI-regulated Payment Aggregator – Cross Border license framework.

This means you keep full control of your forex — when to convert, how much to convert, and at what rate.

It is that straightforward. No re-routing, no double handling, no unnecessary conversions of eating into your hard-earned export revenue.

Can a freelancer or solo service exporter open an EEFC account?

Yes. Any person resident in India who earns foreign exchange — including freelancers, consultants, individual IT exporters, and sole proprietors — is eligible to open an EEFC account. You do not need to be a registered company. However, having an Import-Export Code (IEC) is generally required by most banks.

Is there a minimum balance requirement for an EEFC account?

Most banks do not impose a minimum average balance requirement for EEFC accounts, since they are current accounts and are meant for active transactional use. However, individual bank policies vary — always check with your specific bank before opening.

Can I earn interest in my EEFC account balance?

No. Since May 2012, RBI has directed that EEFC accounts are non-interest-bearing. This was done to prevent entities from using the account as an interest-yielding investment vehicle instead of a genuine forex management tool. The trade-off is the flexibility and potential conversion savings you gain.

What happens if I forget to convert the EEFC balance at the end of 30 days?

If funds credited to your EEFC account are not utilized within 30 days, they must be converted to INR. Banks are expected to convert unused balances on your behalf if you do not act. Habitual non-compliance can attract regulatory scrutiny under FEMA, so it is best to have a clear policy for managing your forex balance.

Can a startup or e-commerce exporter use an EEFC account?

Absolutely, In fact, for SaaS companies, e-commerce exporters, app developers, and digital service providers receiving recurring USD or EUR payments, an EEFC account can be especially valuable. Combined with PayGlocal's direct EEFC settlement feature, it creates a seamless end-to-end forex receipt and management workflow.

Is it safe to hold large forex amounts in an EEFC account?

Your EEFC account balance is subject to the same deposit insurance and regulatory safeguards as any other bank account in India. For large forex holdings, diversifying across banks and using hedging instruments alongside your EEFC account is a prudent strategy.

How does PayGlocal handle settlement if I have multiple accounts — one INR and one EEFC?

You can configure PayGlocal to settle your EEFC account. If you ever need to switch back to INR settlement, you can update your settlement preferences in the dashboard or via your PayGlocal relationship manager. The system handles it cleanly without any interruption to your payment acceptance.

If you are an exporter, a freelancer for billing an international client, or a startup receiving payments in foreign currency, an EEFC account is not just a compliance checkbox — it is a genuine business tool. Paired with PayGlocal's ability to settle directly to your EEFC account, you gain a clean, efficient, and cost-effective path from international invoice to forex management.

Stop leaving money on the table with every forced conversion. Set up your EEFC account, link it with PayGlocal, and let your export earnings work for you.

What Is an EEFC Account?

An Exchange Earner's Foreign Currency (EEFC) account is a non-interest-bearing current account held in a foreign currency, maintained with an authorized dealer essentially a bank authorized by the Reserve Bank of India (RBI) in India. The account enables exporters, service providers, and other foreign exchange earners to retain their foreign currency earnings without immediately converting them to Indian Rupees (INR).

Think of it as your 'forex parking account'. Instead of converting every dollar, euro, or pound you receive into INR the moment it hits your bank, you can hold that foreign currency in the EEFC account for a definite period of time and convert it when the rate is favorable, or use it directly for permissible foreign currency expenses without conversion altogether.

The operation of this account is governed by the Foreign Exchange Management Act (FEMA) 1999 and regulatory frameworks prescribed by RBI's Foreign Exchange Management (Deposit) Regulations.

Quick Snapshot

- EEFC Full form is Exchange Earner's Foreign Currency Account

- Account type: Current (non-interest-bearing)

- Regulatory body: Reserve Bank of India (RBI) under FEMA 1999

- Who can open it: Any person resident in India earning foreign exchange

- Retention allowed: Up to 100% of foreign exchange receipts

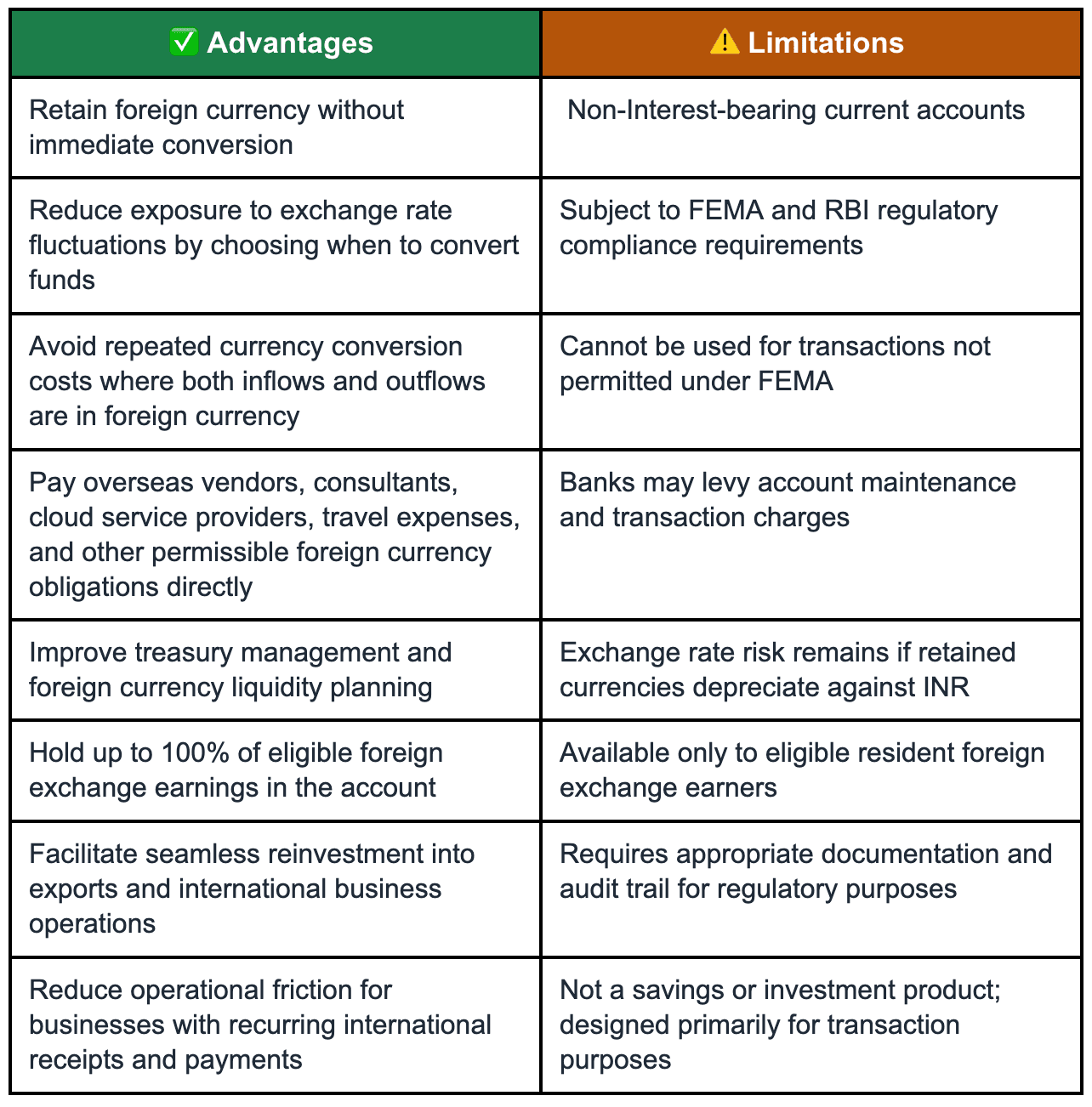

Advantages and Limitations at a Glance

Before you rush to open one, here is the honest picture. EEFC accounts are powerful — but they are not for everyone or every situation.

The bottom line: if you have recurring foreign currency expenses, such as paying overseas vendors, SaaS subscriptions, travel, or reinvesting in imports — an EEFC account can save you real money. If your entire income gets converted to INR and reinvested domestically, the advantage diminishes.

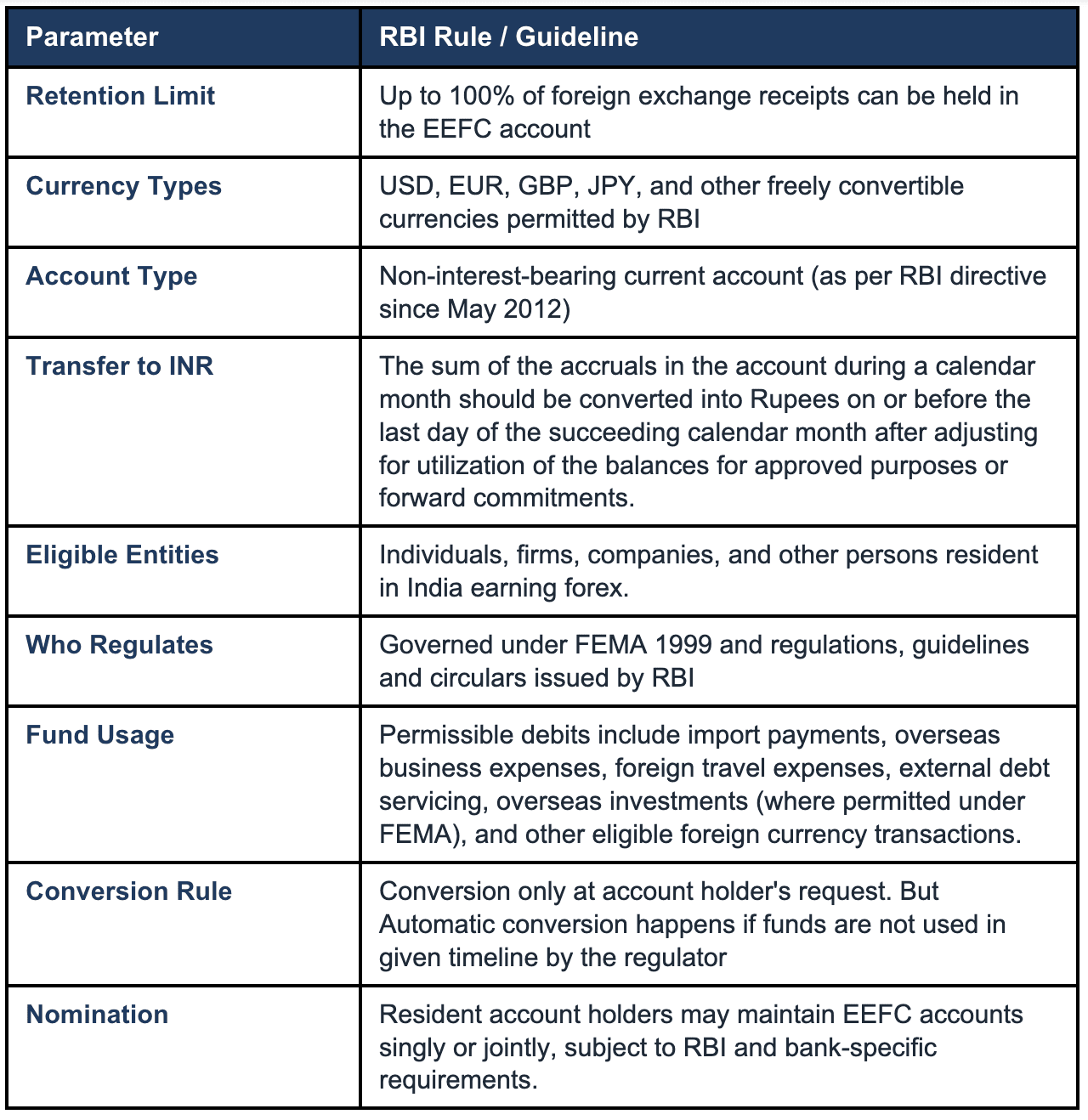

Key Rules and RBI Guidelines You Must Know

EEFC accounts are tightly regulated. Not knowing the rules is not just a compliance risk — it can result in penalties under FEMA. Here is what you need to keep in mind:

What Can You Use EEFC Funds For?

RBI permits debit from an EEFC account for the following purposes:

- Payments for imports of goods and services

- Repayment of foreign currency obligations

- Trade related loans and advances

- Travel-related expenses (business or personal)

- Investments abroad — equity, debt, or otherwise (subject to LRS/ODI regulations)

- Customs duty payments

Important: The 30-Day Rule

The sum of the accruals in the account during a calendar month should be converted into Rupees on or before the last day of the succeeding calendar month after adjusting for utilisation of the balances for approved purposes or forward commitments.

How to open an EEFC Account?

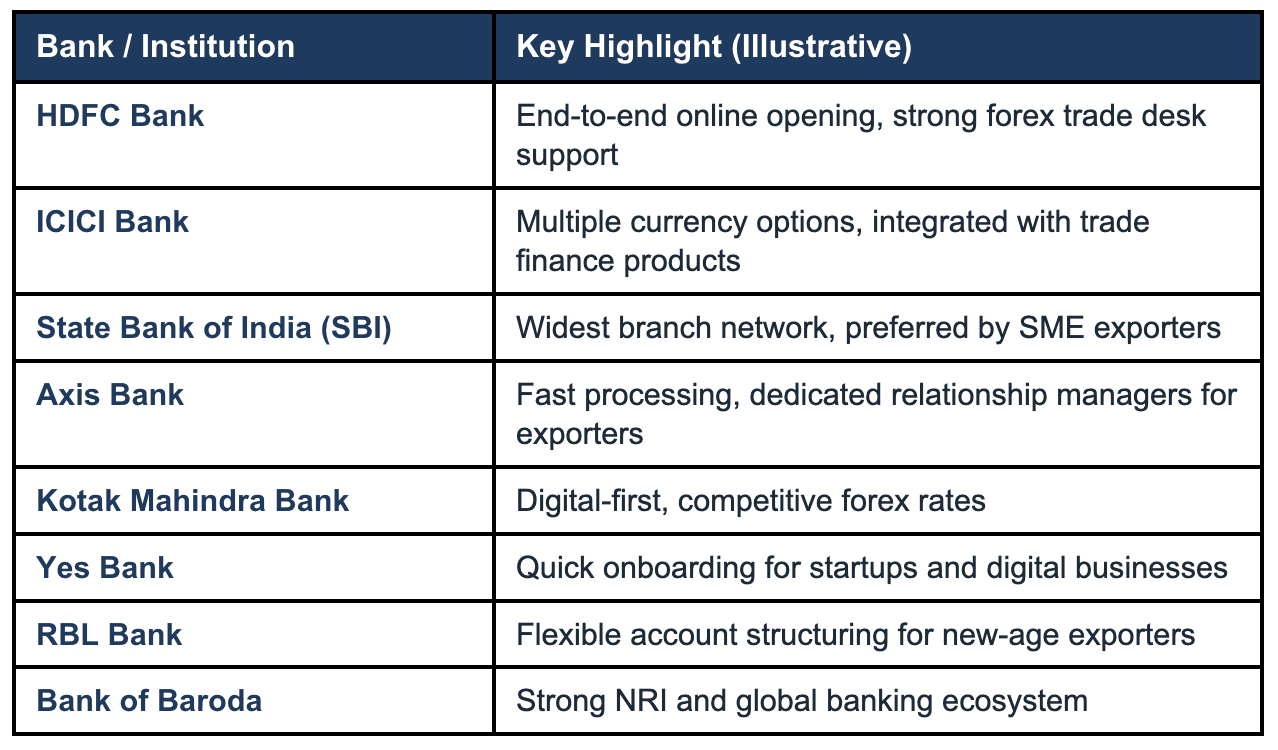

Any authorized dealer bank in India — basically any scheduled commercial bank — can open an EEFC account for you. There is no shortage of options; what matters is choosing a bank with strong trade finance infrastructure and competitive forex spreads.

*The feature highlight is illustrative in nature, and you are advised to consult with the respective banks for overall features.

Documents You Will Typically Need

- Business registration certificate (GST, COI, or equivalent)

- KYC documents — PAN card, Aadhaar or passport

- Proof of foreign exchange earnings

- Import-Export Code (IEC) issued by DGFT

- Existing current account details with the bank

- Board resolution (for companies) authorizing account opening

- FEMA declaration and account opening forms

- Beneficial ownership and constitutional documents

* Document requirement may vary from bank to bank.

Most private sector banks now allow you to initiate the EEFC account application online. Processing time typically ranges from 2 to 5 working days once all documents are in order.

How PayGlocal Works with Your EEFC Account

By default, PayGlocal settles your international collections into your INR current account. That works perfectly for most merchants — but if you already have an EEFC account, you have a better option.

Settle Directly to Your EEFC Account: If you already hold an EEFC account, simply share your EEFC account details with PayGlocal, and we will settle your international payments directly to that account — in the original foreign currency minus the MDR & taxes, no conversion required.

Note: EEFC settlement through PayGlocal is available only for merchants who hold a Multi-Currency Account. PayGlocal enables this settlement under its RBI-regulated Payment Aggregator – Cross Border license framework.

This means you keep full control of your forex — when to convert, how much to convert, and at what rate.

Why This Matters for Your Business

- Eliminate forced conversions: Receive USD/EUR/GBP in their original form

- Consolidate all forex in one place: Aggregate PayGlocal settlements with other export receipts in your EEFC account

- Time your conversions strategically: Convert when rates are favorable, not when your payment arrives

- Simplify accounting: Fewer conversion entries, cleaner reconciliation between your PayGlocal dashboard and bank statement

- Pay international vendors instantly: Use your EEFC balance to pay overseas suppliers without routing through INR

How to Set It Up

- Log in to your PayGlocal merchant dashboard

- Go to Settlement Settings or contact your PayGlocal relationship manager

- Provide your EEFC account details

- PayGlocal verifies the account and activates EEFC settlement for your profile

- From the next settlement cycle, international payments will credit directly to your EEFC account

It is that straightforward. No re-routing, no double handling, no unnecessary conversions of eating into your hard-earned export revenue.

Frequently Asked Questions

Can a freelancer or solo service exporter open an EEFC account?

Yes. Any person resident in India who earns foreign exchange — including freelancers, consultants, individual IT exporters, and sole proprietors — is eligible to open an EEFC account. You do not need to be a registered company. However, having an Import-Export Code (IEC) is generally required by most banks.

Is there a minimum balance requirement for an EEFC account?

Most banks do not impose a minimum average balance requirement for EEFC accounts, since they are current accounts and are meant for active transactional use. However, individual bank policies vary — always check with your specific bank before opening.

Can I earn interest in my EEFC account balance?

No. Since May 2012, RBI has directed that EEFC accounts are non-interest-bearing. This was done to prevent entities from using the account as an interest-yielding investment vehicle instead of a genuine forex management tool. The trade-off is the flexibility and potential conversion savings you gain.

What happens if I forget to convert the EEFC balance at the end of 30 days?

If funds credited to your EEFC account are not utilized within 30 days, they must be converted to INR. Banks are expected to convert unused balances on your behalf if you do not act. Habitual non-compliance can attract regulatory scrutiny under FEMA, so it is best to have a clear policy for managing your forex balance.

Can a startup or e-commerce exporter use an EEFC account?

Absolutely, In fact, for SaaS companies, e-commerce exporters, app developers, and digital service providers receiving recurring USD or EUR payments, an EEFC account can be especially valuable. Combined with PayGlocal's direct EEFC settlement feature, it creates a seamless end-to-end forex receipt and management workflow.

Is it safe to hold large forex amounts in an EEFC account?

Your EEFC account balance is subject to the same deposit insurance and regulatory safeguards as any other bank account in India. For large forex holdings, diversifying across banks and using hedging instruments alongside your EEFC account is a prudent strategy.

How does PayGlocal handle settlement if I have multiple accounts — one INR and one EEFC?

You can configure PayGlocal to settle your EEFC account. If you ever need to switch back to INR settlement, you can update your settlement preferences in the dashboard or via your PayGlocal relationship manager. The system handles it cleanly without any interruption to your payment acceptance.

The Takeaway

If you are an exporter, a freelancer for billing an international client, or a startup receiving payments in foreign currency, an EEFC account is not just a compliance checkbox — it is a genuine business tool. Paired with PayGlocal's ability to settle directly to your EEFC account, you gain a clean, efficient, and cost-effective path from international invoice to forex management.

Stop leaving money on the table with every forced conversion. Set up your EEFC account, link it with PayGlocal, and let your export earnings work for you.