You collect payments from customers in different countries. You log into three dashboards, chase settlements across two banks, and spend half a day every month matching numbers in a spreadsheet. It shouldn't be this hard.

Centralized payment processing solves this by putting all your global payments into one system. As India’s economy scales toward a projected 7.4% growth in FY 2025-26, more Indian businesses are going global and finding that their payment setups can't keep up with the volume.

This guide covers in detail what centralized payment processing is and how it works. Find out more about their key benefits, challenges, and how to pick the right platform for your needs.

Centralized payment processing is when a business routes all its payment activity through one system instead of using separate tools for each country, currency, or payment type. Every transaction, whether it is a card payment from the US or a bank transfer from the UK, goes through the same platform.

For instance, you run a SaaS company in India with customers in the US, UK, and Germany. Without centralization, you might use one tool for USD card payments, another for GBP bank transfers, and a third for EUR invoices. Each has its own dashboard, fee structure, and settlement timeline.

With centralized payment processing, all three flow through one platform. You see every payment in one place. You reconcile once instead of three times. Your finance team saves hours every week.

Most businesses start with a decentralized setup without realizing it. They add a new payment tool every time they enter a new market. Over time, this creates systems that don't connect well with each other.

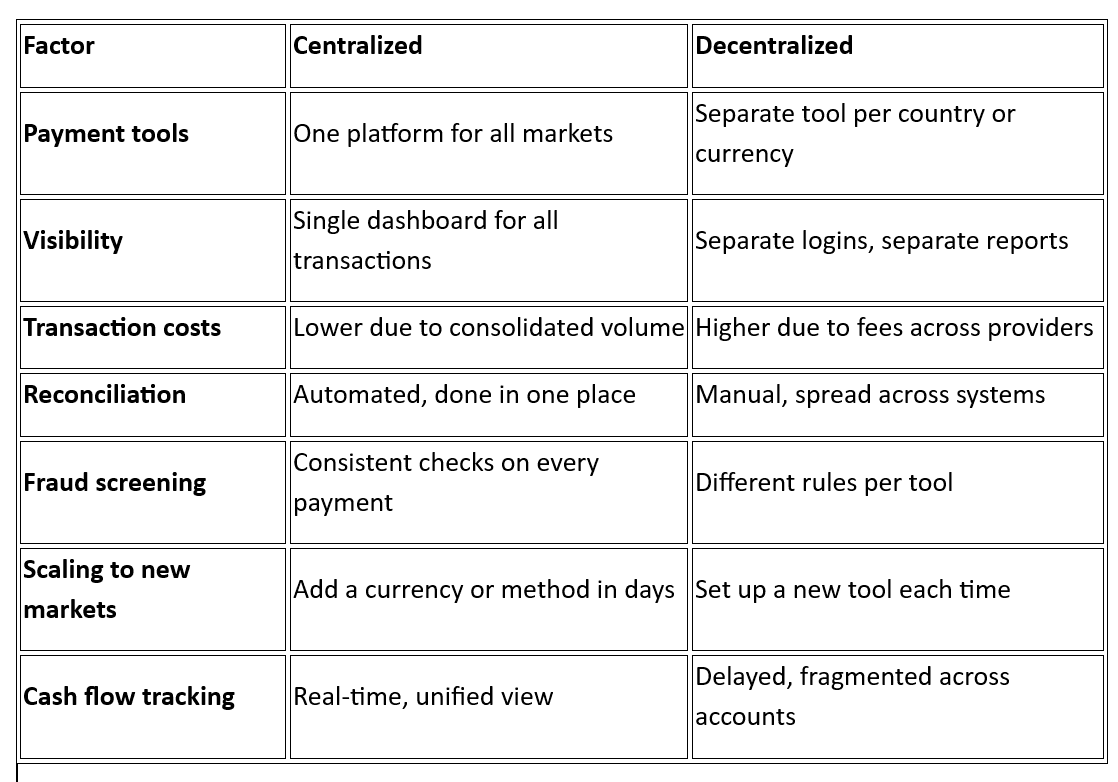

Here's how the two approaches compare side by side:

A decentralized setup might feel manageable when you're just starting. But as you add markets, the hidden costs of fragmented data and manual reconciliation grow faster than your revenue. Centralized processing keeps your operations simple, no matter how many countries you sell in.

Scattered payment tools drain your finance team's time every single month. Hours go into reconciliation, settlement tracking, and pulling reports from separate dashboards. One system changes how your team operates day-to-day.

Here are the main reasons why businesses centralize their payment processing:

Every hour your team spends switching between dashboards or chasing settlement updates is an hour not spent on growth. The businesses that centralize early free up that time and put it back into selling.

Tip: Track how many hours your finance team spends on reconciliation each month. That number alone tells you how much a centralized system would save.

Centralized payment processing helps any business that collects payments from more than one country. That said, some business types see results faster than others. Here's a quick overview of who benefits the most, and why.

If you export goods or services to buyers in the US, UK, Europe, or the Middle East, you likely deal with different currencies, payment methods, and settlement timelines for each market. Centralizing puts all of that into one system.

For instance, an Indian textile exporter shipping to five countries can collect USD, GBP, and EUR through one platform instead of managing separate bank accounts for each currency.

Recurring billing across countries gets complicated fast. You need to handle auto-debits, failed payment retries, and mandate management for each market. A centralized platform handles all of this in one place.

For example, an ed-tech company billing parents in the US, Canada, and the UK monthly can set up recurring payments for all three markets through one system instead of three.

If your online store ships to international customers, your checkout needs to support local currencies and payment methods. A centralized platform shows each customer their preferred way to pay, no matter where they are.

For instance, a fashion brand selling globally can offer card payments for US customers and local wallet options for customers in Southeast Asia, all from one checkout page.

Consultants, agencies, and freelancers billing clients in different countries often rely on separate invoicing tools or marketplace payouts. Centralizing these into one account gives you a single view of all incoming payments and faster access to your funds.

Note: You don't need to be a large company to centralize. Even a business with customers in two or three countries saves time and money by bringing payments into one system early.

Every international payment goes through several steps before it reaches your account. When those steps are split across tools, tracking becomes challenging. A centralized system keeps the full journey visible and connected on a single platform.

Here’s how the centralized payment processing works from start to finish:

1. Customer initiates payment: Your customer pays through your checkout page, payment link, or invoice. The platform detects their location and shows the right currency and payment method.

2. Platform processes the transaction: The system handles currency acceptance, fraud screening, and authentication in one step. No manual input from your side.

3. Payment gets confirmed: Both you and your customer get instant confirmation. The platform logs the transaction with full details.

4. Funds settle to your account: The platform settles the funds directly into your Indian bank account in INR, handling the conversion and applying a transparent fee so you don't have to chase bank transfers.

5. You track everything from one dashboard: Every transaction across all currencies and countries shows up in a single view. Reports, notifications, and compliance documents are available in one place.

The right platform handles each step without you switching between tools or chasing status updates across systems.

Tip: When evaluating platforms, ask how they handle failed transactions. A good centralized system logs every failure with a reason code and notifies you in real time so you can act quickly.

Switching to a centralized system is not always simple. Knowing where most businesses get stuck helps you plan better. Here are the common challenges you should expect and how to handle them:

If your team already uses two or three payment tools, migrating data and workflows takes time. You need to map your current payment flows, test the new system, and run both in parallel before switching fully.

For example, if your recurring billing runs on one tool and one-time payments on another, check that the new platform handles both before you commit.

Your finance team, operations team, and sometimes your developers all need to use the new system. Training takes effort. The easier the platform is to set up and use, the faster your team adopts it.

Not every platform supports every local payment method. If you sell in markets where customers prefer local wallets or bank transfers over cards, make sure your centralized platform covers those methods.

For instance, customers in the Netherlands prefer iDEAL, while customers in Germany often use Sofort. A good centralized platform offers these alongside standard card payments.

Different currencies and payment methods settle at different speeds. When you centralize, you need clear visibility into when each payment will land in your account. Choose a platform that shows real-time fund status at every step.

Note: The biggest risk in centralizing payments is choosing a platform that does not support your growth. Always check how easy it is to add new currencies, payment methods, or markets before you commit.

Your platform decides how much time your team saves from the moment you start using centralized payment processing. Not every platform fits every business, so the selection matters more than most people expect.

Here’s what to evaluate before picking the right platform:

Check how many currencies the platform supports and in how many countries it can accept payments. If you plan to expand into new markets in the next year, make sure the platform already covers those regions.

Cards alone are not enough. Your platform should support local payment methods, bank transfers, recurring payments, and payment links. The more methods it covers, the fewer customers you lose at checkout.

Look for platforms with clear, simple pricing. No setup fees, no hidden charges, no monthly minimums. You should know exactly what you pay per transaction before you sign up.

A centralized platform is only useful if you can actually see what is happening. Look for real-time dashboards, downloadable reports, payment status notifications, and compliance document generation.

Check if the platform works with your existing website, e-commerce store, or billing system. Look for API access, plugins for platforms like Shopify or WooCommerce, and no-code options for quick setup.

Tip: Ask for a test account or demo before signing up. Run a few test transactions to see how the dashboard, notifications, and settlement process actually work in practice.

If you collect payments from customers in different countries, you already know the pain of managing separate tools, chasing settlement updates, and handling compliance for each currency.

PayGlocal cuts through the complexity, giving Indian businesses one powerful command center to collect, track, and settle every global transaction. Here's what you get:

PayGlocal charges no setup fees, no platform fees, and no documentation charges. You pay only when you transact. Indian businesses across travel, e-commerce, SaaS, and education already use it to collect global payments with high success rates.

Centralized payment processing takes the complexity out of global payments. Instead of managing separate tools, bank accounts, and reconciliation workflows for each market, you run everything through one system. The result is lower costs, better visibility, and faster settlements.

If your business collects payments from international customers, centralizing now saves you time and money as you grow. PayGlocal gives you everything you need in one platform, from multi-currency accounts to fraud screening to a real-time dashboard.

The longer you wait to centralize, the more you spend on manual processes and scattered tools. Get started with PayGlocal today and bring your global payments into one place.

Centralized payment processing solves this by putting all your global payments into one system. As India’s economy scales toward a projected 7.4% growth in FY 2025-26, more Indian businesses are going global and finding that their payment setups can't keep up with the volume.

This guide covers in detail what centralized payment processing is and how it works. Find out more about their key benefits, challenges, and how to pick the right platform for your needs.

Key takeaways

- One system for all payments: Centralized payment processing puts all your global transactions in a single place so you can stop juggling separate tools.

- Better cash flow visibility: You get a clear, real-time view of every payment across currencies and countries from one dashboard.

- Lower costs per transaction: Consolidating payments into one system often reduces processing fees and removes hidden charges.

- Fewer manual errors: Automated tracking and notifications replace spreadsheets and manual reconciliation.

- Centralized payment platform: PayGlocal lets businesses collect payments in 33+ currencies from 180+ countries through one platform.

What is centralized payment processing?

Centralized payment processing is when a business routes all its payment activity through one system instead of using separate tools for each country, currency, or payment type. Every transaction, whether it is a card payment from the US or a bank transfer from the UK, goes through the same platform.

For instance, you run a SaaS company in India with customers in the US, UK, and Germany. Without centralization, you might use one tool for USD card payments, another for GBP bank transfers, and a third for EUR invoices. Each has its own dashboard, fee structure, and settlement timeline.

With centralized payment processing, all three flow through one platform. You see every payment in one place. You reconcile once instead of three times. Your finance team saves hours every week.

What is the difference between centralized and decentralized payment processing?

Most businesses start with a decentralized setup without realizing it. They add a new payment tool every time they enter a new market. Over time, this creates systems that don't connect well with each other.

Here's how the two approaches compare side by side:

A decentralized setup might feel manageable when you're just starting. But as you add markets, the hidden costs of fragmented data and manual reconciliation grow faster than your revenue. Centralized processing keeps your operations simple, no matter how many countries you sell in.

Why do businesses need centralized payment processing?

Scattered payment tools drain your finance team's time every single month. Hours go into reconciliation, settlement tracking, and pulling reports from separate dashboards. One system changes how your team operates day-to-day.

Here are the main reasons why businesses centralize their payment processing:

- Complete visibility across markets: You see every transaction from every country in one dashboard. No more logging into separate systems to check payment status.

- Lower transaction costs: One platform often means better pricing. You avoid paying setup fees, platform fees, and currency markups across separate providers.

- Stronger cash flow control: When every payment, pending or settled, shows up in one place with clear timelines, you know exactly when funds will land. This makes weekly and monthly cash planning much easier.

- Faster reconciliation: Matching payments to invoices takes minutes instead of hours. The system does it for you automatically.

- Consistent fraud screening: Every transaction goes through the same security checks. This catches suspicious activity early, lowers chargebacks, and reduces false declines on genuine payments. One set of rules across all markets is always more reliable than different settings on different tools.

- Quicker decision-making: Real-time data on cash flow, payment success rates, and settlement status helps you make faster business decisions.

- Simpler compliance: One platform generates all the documents you need. For instance, if you need a Foreign Inward Remittance Certificate (FIRC) after settlement, a centralized system sends it to you directly.

Every hour your team spends switching between dashboards or chasing settlement updates is an hour not spent on growth. The businesses that centralize early free up that time and put it back into selling.

Tip: Track how many hours your finance team spends on reconciliation each month. That number alone tells you how much a centralized system would save.

Which businesses benefit most from centralized payment processing?

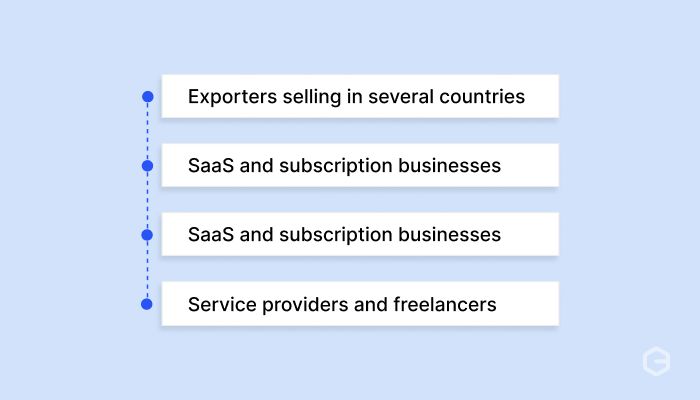

Centralized payment processing helps any business that collects payments from more than one country. That said, some business types see results faster than others. Here's a quick overview of who benefits the most, and why.

1. Exporters selling in several countries

If you export goods or services to buyers in the US, UK, Europe, or the Middle East, you likely deal with different currencies, payment methods, and settlement timelines for each market. Centralizing puts all of that into one system.

For instance, an Indian textile exporter shipping to five countries can collect USD, GBP, and EUR through one platform instead of managing separate bank accounts for each currency.

2. SaaS and subscription businesses

Recurring billing across countries gets complicated fast. You need to handle auto-debits, failed payment retries, and mandate management for each market. A centralized platform handles all of this in one place.

For example, an ed-tech company billing parents in the US, Canada, and the UK monthly can set up recurring payments for all three markets through one system instead of three.

3. D2C and e-commerce brands

If your online store ships to international customers, your checkout needs to support local currencies and payment methods. A centralized platform shows each customer their preferred way to pay, no matter where they are.

For instance, a fashion brand selling globally can offer card payments for US customers and local wallet options for customers in Southeast Asia, all from one checkout page.

4. Service providers and freelancers

Consultants, agencies, and freelancers billing clients in different countries often rely on separate invoicing tools or marketplace payouts. Centralizing these into one account gives you a single view of all incoming payments and faster access to your funds.

Note: You don't need to be a large company to centralize. Even a business with customers in two or three countries saves time and money by bringing payments into one system early.

How does centralized payment processing work?

Every international payment goes through several steps before it reaches your account. When those steps are split across tools, tracking becomes challenging. A centralized system keeps the full journey visible and connected on a single platform.

Here’s how the centralized payment processing works from start to finish:

1. Customer initiates payment: Your customer pays through your checkout page, payment link, or invoice. The platform detects their location and shows the right currency and payment method.

2. Platform processes the transaction: The system handles currency acceptance, fraud screening, and authentication in one step. No manual input from your side.

3. Payment gets confirmed: Both you and your customer get instant confirmation. The platform logs the transaction with full details.

4. Funds settle to your account: The platform settles the funds directly into your Indian bank account in INR, handling the conversion and applying a transparent fee so you don't have to chase bank transfers.

5. You track everything from one dashboard: Every transaction across all currencies and countries shows up in a single view. Reports, notifications, and compliance documents are available in one place.

The right platform handles each step without you switching between tools or chasing status updates across systems.

Tip: When evaluating platforms, ask how they handle failed transactions. A good centralized system logs every failure with a reason code and notifies you in real time so you can act quickly.

What are the common challenges with centralized payment processing?

Switching to a centralized system is not always simple. Knowing where most businesses get stuck helps you plan better. Here are the common challenges you should expect and how to handle them:

1. Moving from existing systems

If your team already uses two or three payment tools, migrating data and workflows takes time. You need to map your current payment flows, test the new system, and run both in parallel before switching fully.

For example, if your recurring billing runs on one tool and one-time payments on another, check that the new platform handles both before you commit.

2. Getting your team on board

Your finance team, operations team, and sometimes your developers all need to use the new system. Training takes effort. The easier the platform is to set up and use, the faster your team adopts it.

3. Handling country-specific payment methods

Not every platform supports every local payment method. If you sell in markets where customers prefer local wallets or bank transfers over cards, make sure your centralized platform covers those methods.

For instance, customers in the Netherlands prefer iDEAL, while customers in Germany often use Sofort. A good centralized platform offers these alongside standard card payments.

4. Keeping settlement timelines predictable

Different currencies and payment methods settle at different speeds. When you centralize, you need clear visibility into when each payment will land in your account. Choose a platform that shows real-time fund status at every step.

Note: The biggest risk in centralizing payments is choosing a platform that does not support your growth. Always check how easy it is to add new currencies, payment methods, or markets before you commit.

How to choose the right centralized payment platform?

Your platform decides how much time your team saves from the moment you start using centralized payment processing. Not every platform fits every business, so the selection matters more than most people expect.

Here’s what to evaluate before picking the right platform:

1. Currency and country coverage

Check how many currencies the platform supports and in how many countries it can accept payments. If you plan to expand into new markets in the next year, make sure the platform already covers those regions.

2. Payment method support

Cards alone are not enough. Your platform should support local payment methods, bank transfers, recurring payments, and payment links. The more methods it covers, the fewer customers you lose at checkout.

3. Pricing transparency

Look for platforms with clear, simple pricing. No setup fees, no hidden charges, no monthly minimums. You should know exactly what you pay per transaction before you sign up.

4. Dashboard and reporting

A centralized platform is only useful if you can actually see what is happening. Look for real-time dashboards, downloadable reports, payment status notifications, and compliance document generation.

5. Integration options

Check if the platform works with your existing website, e-commerce store, or billing system. Look for API access, plugins for platforms like Shopify or WooCommerce, and no-code options for quick setup.

Tip: Ask for a test account or demo before signing up. Run a few test transactions to see how the dashboard, notifications, and settlement process actually work in practice.

Centralize your global payments easily with PayGlocal

If you collect payments from customers in different countries, you already know the pain of managing separate tools, chasing settlement updates, and handling compliance for each currency.

PayGlocal cuts through the complexity, giving Indian businesses one powerful command center to collect, track, and settle every global transaction. Here's what you get:

- Multi-currency accounts: Stop opening bank accounts in every country. Collect locally in USD, GBP, EUR, and CAD, and globally in 33+ currencies, all flowing into one account.

- Global payment methods: Instead of integrating different providers for different regions, use one dynamic checkout that automatically offers 40+ local payment methods globally.

- Recurring payments: Manage subscriptions and auto-debits for US, UK, and Eurozone customers from a single dashboard, removing the need for separate mandate management tools.

- One platform: View every payment, real-time notification, and settlement status in one place. No more manual data merging or spreadsheet reconciliation.

- Sanction screening: Every transaction gets screened automatically, so you stay compliant without adding extra steps to your workflow.

PayGlocal charges no setup fees, no platform fees, and no documentation charges. You pay only when you transact. Indian businesses across travel, e-commerce, SaaS, and education already use it to collect global payments with high success rates.

Final thoughts

Centralized payment processing takes the complexity out of global payments. Instead of managing separate tools, bank accounts, and reconciliation workflows for each market, you run everything through one system. The result is lower costs, better visibility, and faster settlements.

If your business collects payments from international customers, centralizing now saves you time and money as you grow. PayGlocal gives you everything you need in one platform, from multi-currency accounts to fraud screening to a real-time dashboard.

The longer you wait to centralize, the more you spend on manual processes and scattered tools. Get started with PayGlocal today and bring your global payments into one place.