International trade payments can make or break your global business success. While traditional methods like letters of credit dominated for decades, modern payment solutions now offer faster, safer alternatives that reduce costs and increase transaction success rates.

Recent data shows that India's trade finance sector will grow from $2.06 billion in 2024 to $3.18 billion by 2030. Whether you're an Indian exporter shipping goods to Europe or a SaaS company serving global clients, knowing about these payment methods directly impacts your cash flow and growth potential.

In this guide, we break down each international trade payment method that solves common payment challenges. You'll also learn how to choose the right method for your business needs and avoid costly payment delays.

Key takeaways:

- PayGlocal accelerates collections: Multi-currency accounts, higher success rates, and automated compliance help Indian businesses get paid faster with transparent pricing.

- Mix methods strategically: Smart traders use different payment options based on order size, customer history, and market conditions to balance security with competitiveness.

International trade payment refers to the financial settlement process between buyers and sellers located in different countries. These transactions involve currency exchange, compliance with international banking regulations, and coordination between multiple financial institutions across borders.

Unlike local payments that clear within the same banking system, international trade payments involve different currencies, time zones, regulatory frameworks, and banking networks.

For example, when a food exporter in India sells products to a retailer in Germany, the payment process involves multiple steps. The payment starts as Euros in a German bank. It gets converted through international exchange networks. Finally, it arrives as Indian Rupees in the manufacturer's account. This process includes compliance checks and currency conversion that can take anywhere from hours to several business days.

International trade offers multiple payment methods, each designed to balance risk, speed, and cost considerations for different business relationships and transaction sizes.

Studies show that global B2B cross-border payments will increase by 43% between 2024 and 2032, largely due to growing online business-to-business sales worldwide.

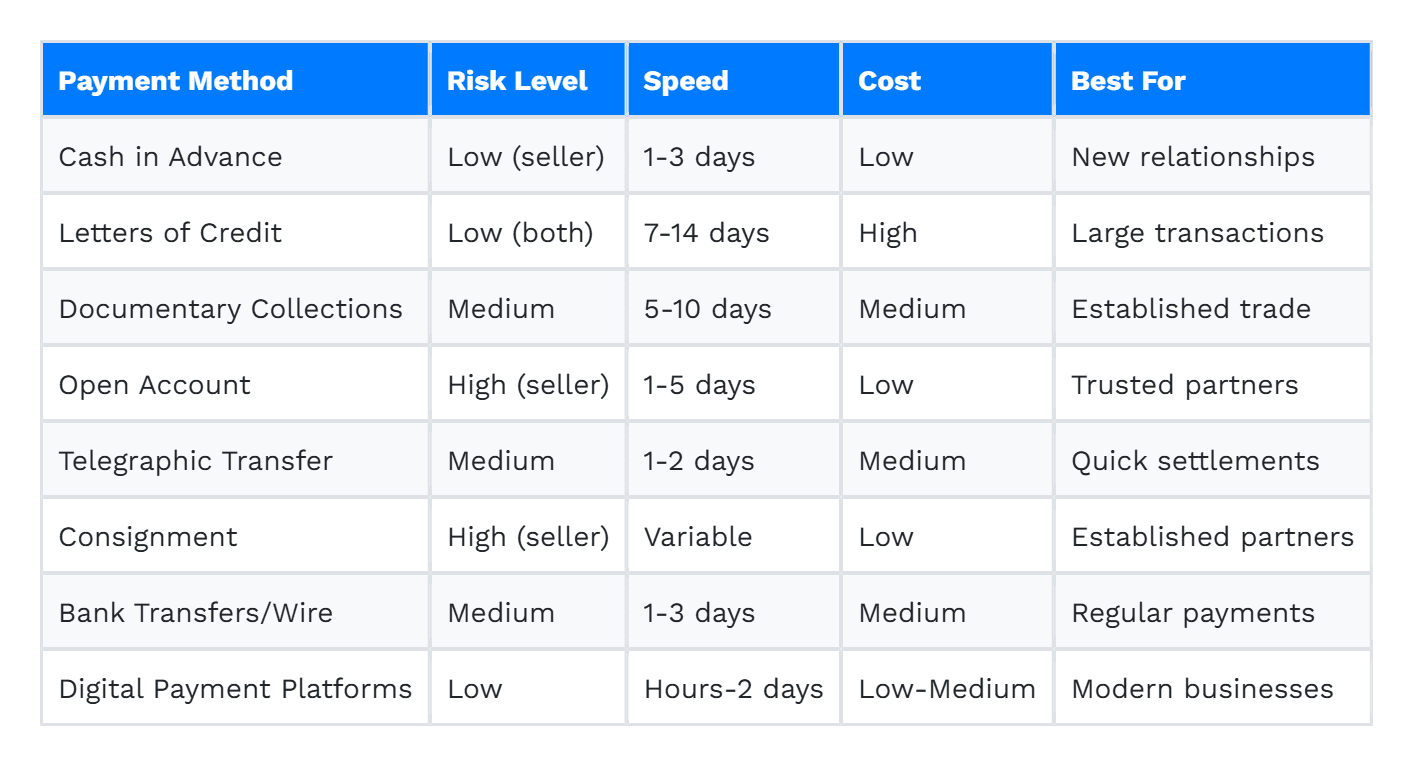

Here's a comparison of the main international trade payment methods and their key characteristics:

Each method serves specific business scenarios, trade relationships, and risk tolerance levels. Let's take a closer look at how each one works in practice.

Cash in advance requires buyers to pay for goods before shipment, making it the safest option for sellers but placing all risk on the purchasing party. This method works through bank transfers, wire payments, or digital platforms where funds move from buyer to seller before any goods change hands.

The seller receives guaranteed payment and can use these funds to finance production or shipping costs. However, buyers must trust that sellers will deliver goods as promised since they've already transferred money. This payment method works best for new business relationships where sellers want to minimize risk, or for high-value items where advance payment provides working capital.

For instance, a handicrafts exporter in India might require cash in advance from first-time international buyers. They can use multi-currency accounts to receive payments in USD or EUR. The funds then get converted to INR at competitive rates.

Benefits:

Limitations:

Best for: New business relationships, small suppliers, high-risk markets, or custom-manufactured products.

Letters of credit involve banks guaranteeing payment to sellers once they meet specific documentation and shipping requirements outlined in the credit terms. The buyer's bank issues the LC, promising to pay the seller's bank when proper documents prove goods were shipped according to agreed specifications.

This method protects both parties through banking intermediaries that verify all conditions before releasing funds. Sellers get payment assurance from reputable banks, while buyers ensure they only pay when goods are properly shipped and documented. The process requires precise export documentation, including bills of lading, commercial invoices, and inspection certificates.

Consider a machinery manufacturer in India selling equipment to a construction company in Brazil. The Brazilian buyer's bank issues an LC guaranteeing payment. The Indian seller must provide shipping documents proving the machinery was sent according to specifications. This process gives both parties security through banking oversight.

Benefits:

Limitations:

Best for: Large transactions, new international relationships, high-value capital goods, or politically unstable regions.

Documentary collections use banks as intermediaries to handle document exchange, but without the payment guarantee that letters of credit provide. Sellers ship goods and send shipping documents through their bank to the buyer's bank, which releases documents only when buyers pay (documents against payment) or accept payment terms (documents against acceptance).

This method costs less than letters of credit since banks don't guarantee payment; they simply facilitate document exchange. Sellers maintain some control since buyers can't claim goods without proper documents, but they still face risk if buyers refuse to pay or accept documents when they arrive.

For example, a spice exporter in India might use documentary collection to sell to European importers. They send shipping documents through banking channels. This maintains better control than open account terms. It also avoids the high costs associated with bill of exchange procedures.

Benefits:

Limitations:

No payment guarantee: Banks don't promise payment if buyers default.

Buyer dependency: Success relies on the buyer's willingness to pay.

Limited recourse: Fewer options if transactions go wrong.

Best for: Established trading relationships, moderate-value transactions, or situations where full LC protection isn't necessary.

Open account terms allow buyers to receive goods before payment, essentially providing trade credit where sellers ship first and collect payment later according to agreed terms like net 30 or net 60 days. This method offers maximum flexibility and convenience for buyers while placing significant risk on sellers.

Sellers must trust buyers to pay on time without bank guarantees or document controls. However, open account terms can provide competitive advantages in markets where buyers expect flexible payment options, and they reduce transaction costs since no banking intermediaries or special documentation are required.

For instance, a software company in India might offer open account terms to established clients in the US. They ship products first and invoice for payment within 30 days. This approach uses recurring payment systems to automate collection processes. It also reduces administrative overhead.

Benefits:

Limitations:

Best for: Established customers, trusted long-term relationships, competitive markets, or low-value repeat transactions.

Telegraphic transfers are electronic bank-to-bank money transfers that move funds directly from the buyer's bank to the seller's bank account. This method is faster than traditional mail-based transfers and more secure than cash payments, making it popular for international trade settlements.

TT payments can be arranged as an advance payment (before shipment) or as a payment against documents (after receiving shipping papers). Banks charge fixed fees plus exchange rate margins, but the process is straightforward with clear timelines. Most telegraphic transfers complete within 1-2 business days, depending on the countries involved.

For example, an electronics manufacturer in India can request TT payment from distributors in Southeast Asia. The funds are transferred directly between banks. This provides faster settlement than letters of credit while maintaining good security levels.

Benefits:

Fast processing speed: Money transfers within 1-2 business days across most routes.

Direct bank involvement: Secure transfer through established banking networks.

Clear fee structure: Fixed charges plus transparent exchange rate costs.

Wide global acceptance: Available between most international banking systems.

Limitations:

Limited buyer protection: No document verification or shipment guarantees.

Exchange rate risk: Currency fluctuations can affect final amounts received.

Irrevocable nature: Difficult to reverse once the transfer is initiated.

Best for: Trusted trading relationships, time-sensitive payments, moderate transaction values, or regular business partnerships.

Consignment arrangements allow sellers to ship goods to buyers without immediate payment, with settlement occurring only after the goods are sold to end customers. The seller retains ownership of goods until they're sold, while the buyer acts as an agent, marketing and selling the products.

This method provides maximum flexibility for buyers since they don't need upfront capital and only pay for goods that actually sell. However, sellers face significant risk as they must wait for sales to occur and trust buyers to report sales accurately and remit payments promptly.

For example, a textile manufacturer in India might send fabrics on consignment to a retailer in Dubai. The retailer displays and sells the fabrics to customers. Payment occurs only after sales, with the retailer keeping an agreed commission and remitting the balance to the manufacturer.

Benefits:

Limitations:

Best for: New market entry, established distributor relationships, high-value specialty products, or seasonal merchandise.

Bank transfers move money directly between financial institutions using secure networks like SWIFT, providing reliable fund movement for international trade transactions. These payments work for both advance payments and post-shipment settlements, offering faster processing than traditional trade finance instruments.

Modern bank transfers can complete within 1-3 business days for most international routes, making them suitable for regular trading relationships where speed matters more than complex risk mitigation. However, they offer limited protection since funds move directly without document verification or banking guarantees.

For instance, an automobile parts manufacturer might use international money transfers to receive payments from overseas distributors. This provides faster settlement times. They can also use credit insurance or other risk management tools to protect against buyer default.

Benefits:

Limitations:

Best for: Regular trading partners, moderate-value transactions, time-sensitive payments, or established business relationships.

Digital payment platforms combine multiple payment methods into unified systems that handle international transactions through modern technology infrastructure. These platforms integrate card processing, bank transfers, digital wallets, and multi-currency accounts while providing real-time tracking, automated compliance, and competitive exchange rates.

Unlike traditional banking methods that require separate relationships with multiple institutions, digital platforms offer one-stop solutions for global payment collection and processing. They use smart routing technology to ensure higher success rates and faster settlement times compared to conventional payment methods.

For example, a software company in India can use digital platforms to accept payments from global clients through multiple methods. Customers can pay via cards, bank transfers, or local payment options. The platform handles currency conversion and compliance automatically while providing real-time transaction updates.

Benefits:

Limitations:

Best for: Growing businesses, e-commerce companies, SaaS providers, or exporters seeking modern payment solutions.

Many businesses still struggle with failed international payments, hidden fees, and weeks-long settlement delays. Modern platforms solve these problems while traditional methods often create more friction for global growth.

Want a better way to digitize your international payments? PayGlocal provides all the features you need in one modern platform that actually works for growing businesses.

Selecting the right payment method requires balancing risk, cost, speed, and relationship factors based on your specific business situation and trading partners.

Consider these key decision factors when evaluating international payment options:

-

Smart businesses often use multiple payment methods depending on the customer, order size, and market conditions.

Traditional international payment methods often create delays, high costs, and uncertainty that slow down business growth. That's where modern payment solutions make a real difference.

PayGlocal helps Indian businesses collect international payments with higher success rates, transparent pricing, and faster settlement times compared to traditional banking methods.

Here's how PayGlocal solves common international payment challenges:

Get started with PayGlocal today and see how modern payment solutions can speed up your international collections while reducing costs and complexity.

International trade payment methods have evolved significantly, offering businesses more options than ever to balance risk, cost, and convenience. While traditional methods like letters of credit remain important for large transactions and new relationships, modern digital solutions provide faster, more cost-effective alternatives for many business situations.

PayGlocal specializes in helping Indian exporters, freelancers, and global businesses collect international payments more efficiently through modern payment solutions that combine security, speed, and competitive pricing in one platform.

Ready to simplify your international trade payments? Get started with PayGlocal and experience how the right payment partner can accelerate your global business growth while reducing complexity and costs.

Recent data shows that India's trade finance sector will grow from $2.06 billion in 2024 to $3.18 billion by 2030. Whether you're an Indian exporter shipping goods to Europe or a SaaS company serving global clients, knowing about these payment methods directly impacts your cash flow and growth potential.

In this guide, we break down each international trade payment method that solves common payment challenges. You'll also learn how to choose the right method for your business needs and avoid costly payment delays.

Key takeaways:

- Traditional methods still matter: Letters of credit remain the gold standard for large transactions and new relationships, while digital solutions work better for speed and cost efficiency.

- Match method to relationship: New partners need secure options like letters of credit, established customers can use open account terms, or direct transfers based on trust levels.

- PayGlocal accelerates collections: Multi-currency accounts, higher success rates, and automated compliance help Indian businesses get paid faster with transparent pricing.

- Mix methods strategically: Smart traders use different payment options based on order size, customer history, and market conditions to balance security with competitiveness.

What is an international trade payment?

International trade payment refers to the financial settlement process between buyers and sellers located in different countries. These transactions involve currency exchange, compliance with international banking regulations, and coordination between multiple financial institutions across borders.

Unlike local payments that clear within the same banking system, international trade payments involve different currencies, time zones, regulatory frameworks, and banking networks.

For example, when a food exporter in India sells products to a retailer in Germany, the payment process involves multiple steps. The payment starts as Euros in a German bank. It gets converted through international exchange networks. Finally, it arrives as Indian Rupees in the manufacturer's account. This process includes compliance checks and currency conversion that can take anywhere from hours to several business days.

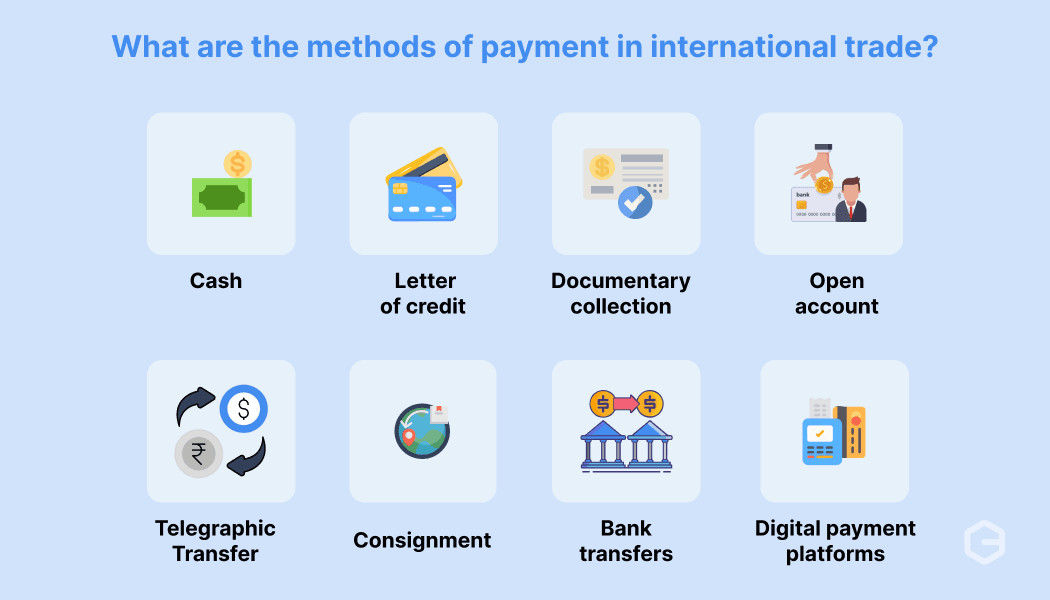

What are the methods of payment in international trade?

International trade offers multiple payment methods, each designed to balance risk, speed, and cost considerations for different business relationships and transaction sizes.

Studies show that global B2B cross-border payments will increase by 43% between 2024 and 2032, largely due to growing online business-to-business sales worldwide.

Here's a comparison of the main international trade payment methods and their key characteristics:

Each method serves specific business scenarios, trade relationships, and risk tolerance levels. Let's take a closer look at how each one works in practice.

1. Cash in advance

Cash in advance requires buyers to pay for goods before shipment, making it the safest option for sellers but placing all risk on the purchasing party. This method works through bank transfers, wire payments, or digital platforms where funds move from buyer to seller before any goods change hands.

The seller receives guaranteed payment and can use these funds to finance production or shipping costs. However, buyers must trust that sellers will deliver goods as promised since they've already transferred money. This payment method works best for new business relationships where sellers want to minimize risk, or for high-value items where advance payment provides working capital.

For instance, a handicrafts exporter in India might require cash in advance from first-time international buyers. They can use multi-currency accounts to receive payments in USD or EUR. The funds then get converted to INR at competitive rates.

Benefits:

- Guaranteed payment security: Sellers receive money before shipping goods.

- Improved cash flow: Immediate access to funds for production and operations.

- No collection risks: Removes concerns about buyer payment delays or defaults.

- Simple transaction process: Straightforward payment without complex documentation.

Limitations:

- Buyer financing burden: Requires buyers to fund purchases upfront.

- Competitive disadvantage: Other suppliers may offer better payment terms.

- Trust barrier: New buyers may hesitate without established relationships.

Best for: New business relationships, small suppliers, high-risk markets, or custom-manufactured products.

2. Letters of credit (LC)

Letters of credit involve banks guaranteeing payment to sellers once they meet specific documentation and shipping requirements outlined in the credit terms. The buyer's bank issues the LC, promising to pay the seller's bank when proper documents prove goods were shipped according to agreed specifications.

This method protects both parties through banking intermediaries that verify all conditions before releasing funds. Sellers get payment assurance from reputable banks, while buyers ensure they only pay when goods are properly shipped and documented. The process requires precise export documentation, including bills of lading, commercial invoices, and inspection certificates.

Consider a machinery manufacturer in India selling equipment to a construction company in Brazil. The Brazilian buyer's bank issues an LC guaranteeing payment. The Indian seller must provide shipping documents proving the machinery was sent according to specifications. This process gives both parties security through banking oversight.

Benefits:

- Bank guarantee protection: Both parties are protected by institutional backing.

- International acceptance: Recognized and trusted globally by banks.

- Document verification: Banks ensure all requirements are met before payment.

- Risk mitigation: Reduces both buyer and seller exposure to default.

Limitations:

- High transaction costs: Bank fees and processing charges add up.

- Complex documentation: Requires precise paperwork and compliance.

- Processing delays: Multiple verification steps slow down transactions.

Best for: Large transactions, new international relationships, high-value capital goods, or politically unstable regions.

3. Documentary collections

Documentary collections use banks as intermediaries to handle document exchange, but without the payment guarantee that letters of credit provide. Sellers ship goods and send shipping documents through their bank to the buyer's bank, which releases documents only when buyers pay (documents against payment) or accept payment terms (documents against acceptance).

This method costs less than letters of credit since banks don't guarantee payment; they simply facilitate document exchange. Sellers maintain some control since buyers can't claim goods without proper documents, but they still face risk if buyers refuse to pay or accept documents when they arrive.

For example, a spice exporter in India might use documentary collection to sell to European importers. They send shipping documents through banking channels. This maintains better control than open account terms. It also avoids the high costs associated with bill of exchange procedures.

Benefits:

- Moderate cost structure: Less expensive than letters of credit.

- Document control: Buyers need documents to claim goods.

- Bank facilitation: Professional handling of international document exchange.

- Flexible terms: Can arrange payment or acceptance options.

Limitations:

No payment guarantee: Banks don't promise payment if buyers default.

Buyer dependency: Success relies on the buyer's willingness to pay.

Limited recourse: Fewer options if transactions go wrong.

Best for: Established trading relationships, moderate-value transactions, or situations where full LC protection isn't necessary.

4. Open account

Open account terms allow buyers to receive goods before payment, essentially providing trade credit where sellers ship first and collect payment later according to agreed terms like net 30 or net 60 days. This method offers maximum flexibility and convenience for buyers while placing significant risk on sellers.

Sellers must trust buyers to pay on time without bank guarantees or document controls. However, open account terms can provide competitive advantages in markets where buyers expect flexible payment options, and they reduce transaction costs since no banking intermediaries or special documentation are required.

For instance, a software company in India might offer open account terms to established clients in the US. They ship products first and invoice for payment within 30 days. This approach uses recurring payment systems to automate collection processes. It also reduces administrative overhead.

Benefits:

- Competitive advantage: Attractive terms help win business against competitors.

- Low transaction costs: No banking fees or special documentation required.

- Relationship building: Shows trust and confidence in long-term partnerships.

- Administrative simplicity: Straightforward invoicing and collection processes.

Limitations:

- High collection risk: No guarantee buyers will pay on time.

- Cash flow impact: Delays between shipping and payment affect working capital.

- Credit management: Requires systems to monitor and collect outstanding amounts.

Best for: Established customers, trusted long-term relationships, competitive markets, or low-value repeat transactions.

5. Telegraphic transfer (TT)

Telegraphic transfers are electronic bank-to-bank money transfers that move funds directly from the buyer's bank to the seller's bank account. This method is faster than traditional mail-based transfers and more secure than cash payments, making it popular for international trade settlements.

TT payments can be arranged as an advance payment (before shipment) or as a payment against documents (after receiving shipping papers). Banks charge fixed fees plus exchange rate margins, but the process is straightforward with clear timelines. Most telegraphic transfers complete within 1-2 business days, depending on the countries involved.

For example, an electronics manufacturer in India can request TT payment from distributors in Southeast Asia. The funds are transferred directly between banks. This provides faster settlement than letters of credit while maintaining good security levels.

Benefits:

Fast processing speed: Money transfers within 1-2 business days across most routes.

Direct bank involvement: Secure transfer through established banking networks.

Clear fee structure: Fixed charges plus transparent exchange rate costs.

Wide global acceptance: Available between most international banking systems.

Limitations:

Limited buyer protection: No document verification or shipment guarantees.

Exchange rate risk: Currency fluctuations can affect final amounts received.

Irrevocable nature: Difficult to reverse once the transfer is initiated.

Best for: Trusted trading relationships, time-sensitive payments, moderate transaction values, or regular business partnerships.

6. Consignment

Consignment arrangements allow sellers to ship goods to buyers without immediate payment, with settlement occurring only after the goods are sold to end customers. The seller retains ownership of goods until they're sold, while the buyer acts as an agent, marketing and selling the products.

This method provides maximum flexibility for buyers since they don't need upfront capital and only pay for goods that actually sell. However, sellers face significant risk as they must wait for sales to occur and trust buyers to report sales accurately and remit payments promptly.

For example, a textile manufacturer in India might send fabrics on consignment to a retailer in Dubai. The retailer displays and sells the fabrics to customers. Payment occurs only after sales, with the retailer keeping an agreed commission and remitting the balance to the manufacturer.

Benefits:

- No upfront buyer investment: Reduces financial burden on purchasing parties.

- Market testing opportunity: Allows buyers to test products without commitment.

- Flexible inventory management: Sellers can place products in multiple markets.

- Relationship building: Shows confidence in products and buyer capabilities.

Limitations:

- High seller risk: No guarantee of payment or product return.

- Extended settlement periods: Payment depends on the end customer sales timing.

- Inventory control challenges: Difficult to monitor stock levels and sales.

Best for: New market entry, established distributor relationships, high-value specialty products, or seasonal merchandise.

7. Bank transfers and wire payments

Bank transfers move money directly between financial institutions using secure networks like SWIFT, providing reliable fund movement for international trade transactions. These payments work for both advance payments and post-shipment settlements, offering faster processing than traditional trade finance instruments.

Modern bank transfers can complete within 1-3 business days for most international routes, making them suitable for regular trading relationships where speed matters more than complex risk mitigation. However, they offer limited protection since funds move directly without document verification or banking guarantees.

For instance, an automobile parts manufacturer might use international money transfers to receive payments from overseas distributors. This provides faster settlement times. They can also use credit insurance or other risk management tools to protect against buyer default.

Benefits:

- Fast processing: Quicker than traditional trade finance methods.

- Global accessibility: Available between most international banking networks.

- Cost efficiency: Lower fees than complex trade finance instruments.

- Transparency: Clear tracking and confirmation of fund movements.

Limitations:

- Limited protection: No built-in buyer or seller safeguards.

- Exchange rate risk: Currency fluctuations can affect final amounts.

- Compliance requirements: Must meet international anti-money laundering standards.

Best for: Regular trading partners, moderate-value transactions, time-sensitive payments, or established business relationships.

8. Digital payment platforms

Digital payment platforms combine multiple payment methods into unified systems that handle international transactions through modern technology infrastructure. These platforms integrate card processing, bank transfers, digital wallets, and multi-currency accounts while providing real-time tracking, automated compliance, and competitive exchange rates.

Unlike traditional banking methods that require separate relationships with multiple institutions, digital platforms offer one-stop solutions for global payment collection and processing. They use smart routing technology to ensure higher success rates and faster settlement times compared to conventional payment methods.

For example, a software company in India can use digital platforms to accept payments from global clients through multiple methods. Customers can pay via cards, bank transfers, or local payment options. The platform handles currency conversion and compliance automatically while providing real-time transaction updates.

Benefits:

- Multiple payment options: Accept cards, transfers, and local methods through one platform.

- Higher success rates: Smart routing and fraud prevention reduce transaction failures.

- Faster settlements: Money arrives quicker than traditional banking methods.

- Automated compliance: Built-in regulatory handling and documentation.

Limitations:

- Platform dependency: Reliance on third-party service providers for operations.

- Technology requirements: Need for integration and technical setup.

- Variable fee structures: Costs can differ based on the payment methods used.

Best for: Growing businesses, e-commerce companies, SaaS providers, or exporters seeking modern payment solutions.

Many businesses still struggle with failed international payments, hidden fees, and weeks-long settlement delays. Modern platforms solve these problems while traditional methods often create more friction for global growth.

Want a better way to digitize your international payments? PayGlocal provides all the features you need in one modern platform that actually works for growing businesses.

How to choose the best payment method for international trade?

Selecting the right payment method requires balancing risk, cost, speed, and relationship factors based on your specific business situation and trading partners.

Consider these key decision factors when evaluating international payment options:

-

- Relationship history: New partners need more secure methods like letters of credit, while established relationships can use open account terms or direct transfers.

- Transaction size: Large deals justify higher costs for secure methods, while smaller amounts benefit from cost-efficient digital solutions.

- Market conditions: Market stability, currency volatility, and local banking infrastructure affect method viability.

- Industry standards: Some sectors have preferred payment methods that buyers expect and competitors commonly offer.

- Cash flow needs: Consider how payment timing affects your working capital and operational requirements.

- Risk tolerance: Balance collection security against competitive pricing and customer convenience.

Smart businesses often use multiple payment methods depending on the customer, order size, and market conditions.

Collect global payments faster and smarter with PayGlocal

Traditional international payment methods often create delays, high costs, and uncertainty that slow down business growth. That's where modern payment solutions make a real difference.

PayGlocal helps Indian businesses collect international payments with higher success rates, transparent pricing, and faster settlement times compared to traditional banking methods.

Here's how PayGlocal solves common international payment challenges:

- Recurring payment automation: Set up subscription billing and automatic collections for SaaS businesses and service providers with consistent revenue streams.

- Card payment processing: Accept international credit and debit cards with optimized approval rates and competitive transaction fees.

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD without international transfer delays, reducing settlement time from weeks to days.

- Complete payment tracking: Know exactly where your money is at every step with notifications and dashboard updates throughout the entire payment process.

- Dynamic checkout solutions: Offer customers multiple payment options, including cards, local methods, and digital wallets, to increase conversion rates.

Get started with PayGlocal today and see how modern payment solutions can speed up your international collections while reducing costs and complexity.

Final thoughts

International trade payment methods have evolved significantly, offering businesses more options than ever to balance risk, cost, and convenience. While traditional methods like letters of credit remain important for large transactions and new relationships, modern digital solutions provide faster, more cost-effective alternatives for many business situations.

PayGlocal specializes in helping Indian exporters, freelancers, and global businesses collect international payments more efficiently through modern payment solutions that combine security, speed, and competitive pricing in one platform.

Ready to simplify your international trade payments? Get started with PayGlocal and experience how the right payment partner can accelerate your global business growth while reducing complexity and costs.