Co-operative banks in India serve a unique role in the banking sector. With 1,457 urban co-operative banks and several state and district central co-operative banks across the country, these financial institutions have been supporting local communities and small businesses for decades.

If you're exploring banking options for your business, you've probably come across co-operative banks and wondered whether they're the right fit. These banks typically operate in a different way from commercial banks.

In this guide, we break down everything you need to know about co-operative banks in India. You'll learn about their types, objectives, functions, and how they compare to other banking options. By the end, you'll have a complete view of whether a co-operative bank fits your needs. Let’s get into it.

Co-operative banks in India are financial institutions owned and operated by their members based on co-operative principles. Unlike commercial banks, where shareholders own the entity, co-operative banks belong to the people who use their services. Each member gets one vote regardless of how many shares they hold, creating a democratic structure.

These banks emerged to serve communities that traditional banks overlooked. Farmers, small business owners, and middle-class individuals came together to form these institutions. The primary goal was to provide affordable credit and banking services to members who couldn't easily access commercial banking.

Co-operative banks operate at different levels across India. Some serve entire states, others focus on districts, and many concentrate on specific urban or rural areas. They range from small primary credit societies with a few hundred members to large urban co-operative banks serving thousands of customers. This structure allows them to stay connected to local needs while remaining part of a larger co-operative banking network.

The ownership model makes co-operative banks different. Members invest small amounts to become shareholders, giving them both banking services and a say in how the bank runs. This creates institutions that prioritize member welfare over profit maximization, though they still need to remain financially viable.

India's co-operative banking structure has multiple layers, each designed to serve specific communities and purposes. The system works as a network where different types of banks connect to provide comprehensive coverage from villages to cities.

Here's how these banks differ in their scope and operations:

Let’s look at each type and what they actually do:

State co-operative banks sit at the top of the rural co-operative banking structure. They operate at the state level and work primarily with district central co-operative banks rather than individual customers. These banks provide refinancing facilities, meaning they give funds to smaller co-operative banks that then lend to farmers and rural businesses.

You'll find one state co-operative bank in most Indian states. For instance, The Punjab State Co-operative Bank serves Punjab, while The Andhra Pradesh State Co-operative Bank operates in Andhra Pradesh. They also supervise and guide district-level banks, helping maintain standards across the co-operative banking network in their state.

District central co-operative banks form the middle layer of rural co-operative banking. They work at the district level, connecting state co-operative banks with village-level primary societies. These banks provide credit to primary agricultural credit societies and sometimes directly to large farmers.

A district central co-operative bank typically covers one district, though some larger districts have multiple banks. They collect deposits from the public and channel funds from state co-operative banks down to primary societies. This makes them important connectors in the rural credit flow.

Urban co-operative banks serve cities and towns across India. Unlike rural co-operative banks that focus on agriculture, these institutions provide full banking services to urban customers, including businesses, professionals, and salaried individuals. They offer savings accounts, fixed deposits, loans, and payment services similar to commercial banks.

Some well-known urban co-operative banks include Cosmos Co-operative Bank, Shamrao Vithal Co-operative Bank, Saraswat Co-operative Bank, and NKGSB Co-operative Bank. These banks have grown significantly and now compete with commercial banks in urban markets. They're popular among small businesses and middle-class customers looking for personalized service and better interest rates on deposits.

Primary agricultural credit societies operate at the village or town level. They're the foundation of rural co-operative banking, providing credit directly to farmers and rural households. These societies are small, member-owned institutions where local farmers pool resources to meet their credit needs.

There are nearly 1,01,524 primary agricultural credit societies across India. They provide short-term and medium-term agricultural loans, helping farmers buy seeds, fertilizers, and equipment. Members deposit their savings here and borrow for agricultural activities. The close community ties help these societies know their members well and tailor services to local farming patterns.

Land development banks focus specifically on long-term agricultural credit. Farmers need long-term loans for activities like buying land, installing irrigation systems, or making permanent farm improvements. Regular co-operative banks typically provide short-term credit, while land development banks fill the long-term financing gap.

These banks operate at both the state and district levels. They raise funds through special bonds and provide loans with extended repayment periods. This makes them important for farmers investing in land development and major agricultural infrastructure.

Co-operative banks exist to serve their members rather than maximize profits for outside shareholders. This fundamental difference shapes everything these banks do, from the loans they offer to how they make decisions.

The main objectives guide how these banks operate:

These objectives make co-operative banks valuable for the communities they serve. However, the focus on local operations and member service means they typically lack the infrastructure for sophisticated services like international payment processing, multi-currency transactions, or global payment method acceptance.

Co-operative banks perform core banking functions while staying focused on member needs. Their day-to-day operations support the objectives of providing affordable credit and promoting financial inclusion in their operating areas.

Here’s what co-operative banks actually do:

Co-operative banks and commercial banks both provide financial services, but they operate on fundamentally different principles. The ownership structure, governance model, and primary objectives create distinct experiences for customers.

Knowing these differences helps you choose the right banking partner for your needs:

The ownership model creates the biggest difference. In co-operative banks, you're both a customer and an owner. You get a say in how the bank runs, regardless of your account balance. Commercial banks answer to shareholders who want maximum returns, which can mean higher fees and less personalized service.

Geographic limitations also matter significantly. Co-operative banks typically operate within one state or district. If your business expands to other regions, you’ll need banking relationships in each area. Commercial banks and modern payment platforms operate nationally and internationally, giving you seamless access wherever your business goes.

For domestic operations, co-operative banks can work well. They offer competitive rates, personal service, and support local communities. However, businesses doing international trade face major limitations.

Co-operative banks rarely have the infrastructure for efficient international payments, multi-currency management, or global payment method acceptance that growing businesses need.

Choosing a co-operative bank depends on your business location, industry, and transaction needs. Not all co-operative banks serve all areas or customer types, so you need to match your requirements with what specific banks offer. Here's what to evaluate when choosing the right co-operative bank:

For businesses focused purely on local operations with no international transactions, a good co-operative bank offers personalized service and competitive rates. However, if you're exporting goods or services, receiving payments from international clients, or planning global expansion, you need advanced payment solutions.

Co-operative banks serve an important purpose in India's banking sector. They provide accessible, member-focused banking for local communities and domestic operations. However, if you're collecting payments from overseas clients, dealing with multiple currencies, or managing international transactions, you need infrastructure that co-operative banks don’t have.

You need local accounts in major currencies, transparent fee structures, instant compliance documentation, and payment success rates that don’t hurt your revenue. PayGlocal gives you exactly that. Here's how PayGlocal can help:

With PayGlocal, you get better payment success rates, faster settlements, lower fees, and the infrastructure to scale globally without the complexity of traditional international banking.

Co-operative banks fill an important role in India’s financial system. They provide accessible, member-focused banking for millions of people and businesses across the country. Their democratic structure, local knowledge, and community orientation make them valuable for domestic banking needs, especially in areas where commercial banks don’t focus.

However, limitations become clear when your business grows beyond local operations. Geographic restrictions, limited technology, and virtually no international banking capabilities mean co-operative banks work best for businesses with purely domestic operations. The moment you start receiving payments from overseas clients or need to manage multiple currencies, traditional co-operative banking infrastructure becomes a bottleneck.

Modern businesses need banking solutions that match their global growth goals. PayGlocal gives you the international payment capabilities that traditional banks can’t, with the simplicity and transparency your business deserves.

Ready to collect payments globally and settle locally? Get started with PayGlocal today.

If you're exploring banking options for your business, you've probably come across co-operative banks and wondered whether they're the right fit. These banks typically operate in a different way from commercial banks.

In this guide, we break down everything you need to know about co-operative banks in India. You'll learn about their types, objectives, functions, and how they compare to other banking options. By the end, you'll have a complete view of whether a co-operative bank fits your needs. Let’s get into it.

Key takeaways

- Member-owned structure: Members own the bank democratically with equal voting rights, creating community-focused financial institutions.

- Multiple types serve different needs: Five main types, from state-level banks to village societies, serve farmers, urban businesses, and specific communities.

- Cost advantages for local banking: Lower fees and better deposit rates make them attractive for businesses with purely domestic operations.

- Geographic restrictions apply: Banks typically operate within specific states or districts, limiting reach for businesses expanding across regions.

- Global payments: Platforms like PayGlocal offer multi-currency accounts, global payment acceptance, and instant compliance for international trade.

What are co-operative banks in India?

Co-operative banks in India are financial institutions owned and operated by their members based on co-operative principles. Unlike commercial banks, where shareholders own the entity, co-operative banks belong to the people who use their services. Each member gets one vote regardless of how many shares they hold, creating a democratic structure.

These banks emerged to serve communities that traditional banks overlooked. Farmers, small business owners, and middle-class individuals came together to form these institutions. The primary goal was to provide affordable credit and banking services to members who couldn't easily access commercial banking.

Co-operative banks operate at different levels across India. Some serve entire states, others focus on districts, and many concentrate on specific urban or rural areas. They range from small primary credit societies with a few hundred members to large urban co-operative banks serving thousands of customers. This structure allows them to stay connected to local needs while remaining part of a larger co-operative banking network.

The ownership model makes co-operative banks different. Members invest small amounts to become shareholders, giving them both banking services and a say in how the bank runs. This creates institutions that prioritize member welfare over profit maximization, though they still need to remain financially viable.

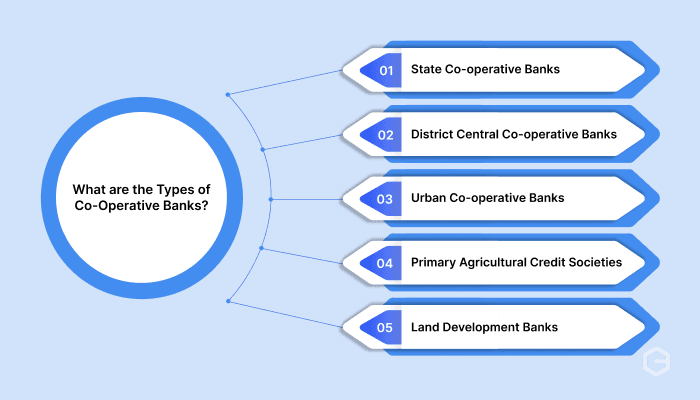

What are the types of co-operative banks?

India's co-operative banking structure has multiple layers, each designed to serve specific communities and purposes. The system works as a network where different types of banks connect to provide comprehensive coverage from villages to cities.

Here's how these banks differ in their scope and operations:

Let’s look at each type and what they actually do:

State co-operative banks

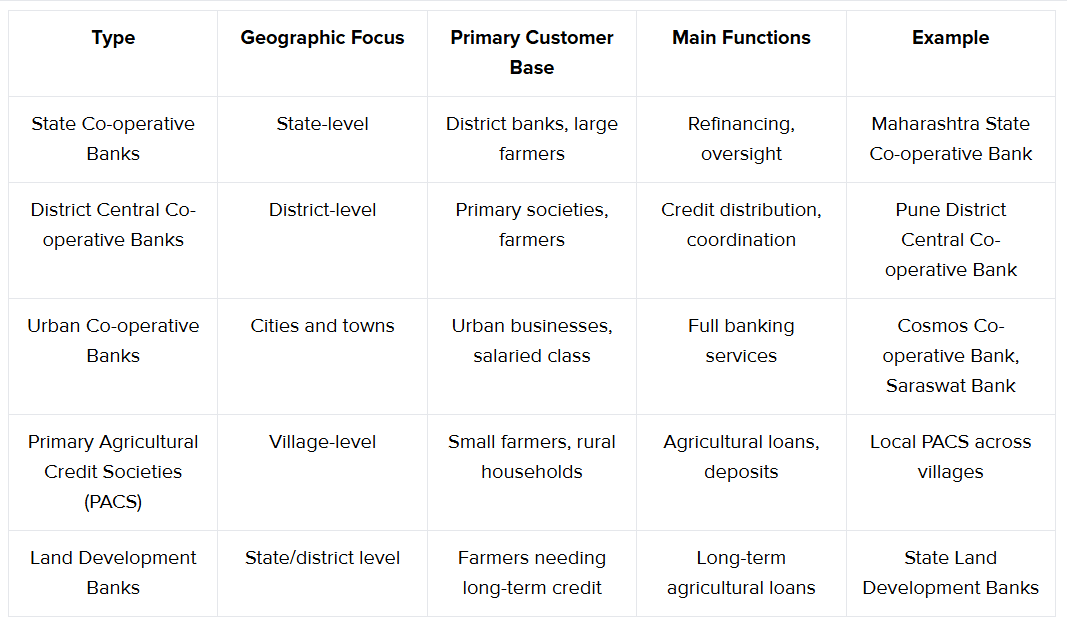

State co-operative banks sit at the top of the rural co-operative banking structure. They operate at the state level and work primarily with district central co-operative banks rather than individual customers. These banks provide refinancing facilities, meaning they give funds to smaller co-operative banks that then lend to farmers and rural businesses.

You'll find one state co-operative bank in most Indian states. For instance, The Punjab State Co-operative Bank serves Punjab, while The Andhra Pradesh State Co-operative Bank operates in Andhra Pradesh. They also supervise and guide district-level banks, helping maintain standards across the co-operative banking network in their state.

District central co-operative banks

District central co-operative banks form the middle layer of rural co-operative banking. They work at the district level, connecting state co-operative banks with village-level primary societies. These banks provide credit to primary agricultural credit societies and sometimes directly to large farmers.

A district central co-operative bank typically covers one district, though some larger districts have multiple banks. They collect deposits from the public and channel funds from state co-operative banks down to primary societies. This makes them important connectors in the rural credit flow.

Urban co-operative banks

Urban co-operative banks serve cities and towns across India. Unlike rural co-operative banks that focus on agriculture, these institutions provide full banking services to urban customers, including businesses, professionals, and salaried individuals. They offer savings accounts, fixed deposits, loans, and payment services similar to commercial banks.

Some well-known urban co-operative banks include Cosmos Co-operative Bank, Shamrao Vithal Co-operative Bank, Saraswat Co-operative Bank, and NKGSB Co-operative Bank. These banks have grown significantly and now compete with commercial banks in urban markets. They're popular among small businesses and middle-class customers looking for personalized service and better interest rates on deposits.

Primary agricultural credit societies

Primary agricultural credit societies operate at the village or town level. They're the foundation of rural co-operative banking, providing credit directly to farmers and rural households. These societies are small, member-owned institutions where local farmers pool resources to meet their credit needs.

There are nearly 1,01,524 primary agricultural credit societies across India. They provide short-term and medium-term agricultural loans, helping farmers buy seeds, fertilizers, and equipment. Members deposit their savings here and borrow for agricultural activities. The close community ties help these societies know their members well and tailor services to local farming patterns.

Land development banks

Land development banks focus specifically on long-term agricultural credit. Farmers need long-term loans for activities like buying land, installing irrigation systems, or making permanent farm improvements. Regular co-operative banks typically provide short-term credit, while land development banks fill the long-term financing gap.

These banks operate at both the state and district levels. They raise funds through special bonds and provide loans with extended repayment periods. This makes them important for farmers investing in land development and major agricultural infrastructure.

What are the objectives of co-operative banks?

Co-operative banks exist to serve their members rather than maximize profits for outside shareholders. This fundamental difference shapes everything these banks do, from the loans they offer to how they make decisions.

The main objectives guide how these banks operate:

- Provide affordable credit: Co-operative banks aim to offer loans at reasonable interest rates to members who might struggle to access credit from commercial banks. Small farmers, urban traders, and middle-class professionals often find co-operative banks more approachable and willing to work with them.

- Encourage savings habits: These banks promote savings among members by offering attractive interest rates on deposits and making the process simple. By pooling member savings, the bank creates capital that it can then lend to other members who need credit.

- Support local economic development: Co-operative banks channel funds into local businesses, farms, and households within their operating area. This keeps money circulating in the community and supports regional economic growth.

- Practice democratic governance: Each member gets one vote in bank decisions regardless of their shareholding. This ensures the bank serves member interests rather than prioritizing wealthy stakeholders.

- Promote financial inclusion: Many co-operative banks operate in areas and serve populations that commercial banks ignore. They bring banking services to rural villages, small towns, and economically weaker sections of society.

- Provide personalized service: With their local focus and member ownership, co-operative banks can offer customized services based on community needs. Loan officers often know members personally and can make flexible decisions.

These objectives make co-operative banks valuable for the communities they serve. However, the focus on local operations and member service means they typically lack the infrastructure for sophisticated services like international payment processing, multi-currency transactions, or global payment method acceptance.

What are the functions of co-operative banks?

Co-operative banks perform core banking functions while staying focused on member needs. Their day-to-day operations support the objectives of providing affordable credit and promoting financial inclusion in their operating areas.

Here’s what co-operative banks actually do:

- Accept deposits from members: The banks offer various deposit products, including savings accounts, fixed deposits, and recurring deposits. They typically provide better interest rates than commercial banks to attract member savings, which then become the capital base for lending operations.

- Provide loans and credit facilities: Members can access different types of loans based on their needs. Agricultural co-operative banks offer crop loans, equipment financing, and land development loans. Urban co-operative banks provide business loans, personal loans, home loans, and working capital financing for small businesses.

- Enable payment and settlement services: These banks offer basic payment services like cheque clearing, demand drafts, and fund transfers. Urban co-operative banks increasingly provide debit cards, online banking, and mobile banking, though their digital infrastructure often lags behind commercial banks.

- Manage financial operations for members: Co-operative banks help members manage their finances by offering financial advice, maintaining safe deposit lockers, and providing documentation for loans. The personal relationship between bank staff and members enables customized financial guidance.

- Support community development: Beyond individual member services, these banks finance community projects, support local businesses, and contribute to regional development. They often provide credit for activities that directly benefit the local economy.

- Facilitate government schemes: Many co-operative banks act as channels for government subsidies, welfare schemes, and financial inclusion programs targeted at farmers and economically weaker sections. This helps members access government benefits more easily.

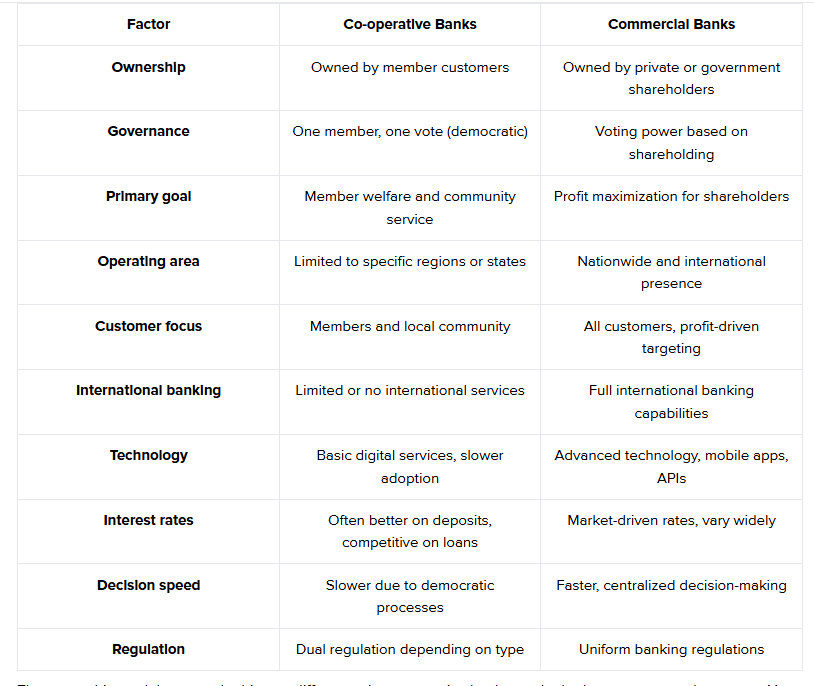

How do co-operative banks differ from commercial banks?

Co-operative banks and commercial banks both provide financial services, but they operate on fundamentally different principles. The ownership structure, governance model, and primary objectives create distinct experiences for customers.

Knowing these differences helps you choose the right banking partner for your needs:

The ownership model creates the biggest difference. In co-operative banks, you're both a customer and an owner. You get a say in how the bank runs, regardless of your account balance. Commercial banks answer to shareholders who want maximum returns, which can mean higher fees and less personalized service.

Geographic limitations also matter significantly. Co-operative banks typically operate within one state or district. If your business expands to other regions, you’ll need banking relationships in each area. Commercial banks and modern payment platforms operate nationally and internationally, giving you seamless access wherever your business goes.

For domestic operations, co-operative banks can work well. They offer competitive rates, personal service, and support local communities. However, businesses doing international trade face major limitations.

Co-operative banks rarely have the infrastructure for efficient international payments, multi-currency management, or global payment method acceptance that growing businesses need.

Which co-operative bank is right for your business?

Choosing a co-operative bank depends on your business location, industry, and transaction needs. Not all co-operative banks serve all areas or customer types, so you need to match your requirements with what specific banks offer. Here's what to evaluate when choosing the right co-operative bank:

- Geographic coverage: Identify banks operating in your area, whether urban cooperative banks in cities or district banks for rural businesses.

- Service range: Check if the bank offers comprehensive business banking, like current accounts, overdraft facilities, and trade finance, beyond basic deposits.

- Financial stability: Ask other business owners about their experiences and verify the bank hasn't faced regulatory issues or deposit concerns.

- Technology capabilities: Assess whether the bank provides internet banking, mobile apps, and digital payment integration, and if these matter to your operations.

- Growth alignment: Consider if geographic restrictions and lack of international infrastructure will limit you as your business expands.

- Transaction needs: Evaluate if the bank can handle your transaction volumes and whether their services match your business banking requirements.

For businesses focused purely on local operations with no international transactions, a good co-operative bank offers personalized service and competitive rates. However, if you're exporting goods or services, receiving payments from international clients, or planning global expansion, you need advanced payment solutions.

Accept global payments with PayGlocal and scale your business

Co-operative banks serve an important purpose in India's banking sector. They provide accessible, member-focused banking for local communities and domestic operations. However, if you're collecting payments from overseas clients, dealing with multiple currencies, or managing international transactions, you need infrastructure that co-operative banks don’t have.

You need local accounts in major currencies, transparent fee structures, instant compliance documentation, and payment success rates that don’t hurt your revenue. PayGlocal gives you exactly that. Here's how PayGlocal can help:

- Multi-currency accounts: Get local account details in USD, GBP, EUR, and CAD. Your international clients see local account numbers, making payments easy and familiar for them while you collect everything seamlessly.

- Instant compliance documentation: Receive Foreign Inward Remittance Certificate (FIRC) automatically in your inbox after each settlement. No chasing banks, no paperwork delays, just automatic documentation that keeps you compliant.

- Zero fixed costs: Pay only when you transact. No setup fees, no platform fees, no monthly charges. Simple, transparent pricing that scales with your business.

- Recurring payments: Set up subscription billing or recurring charges on international cards. Perfect for software businesses, subscription services, or any model requiring automated payment collection.

- One platform management: Manage all your international payments, compliance documents, and settlement tracking from a single dashboard. No more need to handle multiple platforms.

With PayGlocal, you get better payment success rates, faster settlements, lower fees, and the infrastructure to scale globally without the complexity of traditional international banking.

Final thoughts

Co-operative banks fill an important role in India’s financial system. They provide accessible, member-focused banking for millions of people and businesses across the country. Their democratic structure, local knowledge, and community orientation make them valuable for domestic banking needs, especially in areas where commercial banks don’t focus.

However, limitations become clear when your business grows beyond local operations. Geographic restrictions, limited technology, and virtually no international banking capabilities mean co-operative banks work best for businesses with purely domestic operations. The moment you start receiving payments from overseas clients or need to manage multiple currencies, traditional co-operative banking infrastructure becomes a bottleneck.

Modern businesses need banking solutions that match their global growth goals. PayGlocal gives you the international payment capabilities that traditional banks can’t, with the simplicity and transparency your business deserves.

Ready to collect payments globally and settle locally? Get started with PayGlocal today.