Which bank account should you open for your business operations? Recent data indicate India will grow to a $7.3 trillion economy and reach the third spot globally by 2030. With this rapid economic growth, it’s also essential that you have the right financial foundation in place from the start.

Current accounts and savings accounts serve completely different purposes. One is built for frequent business transactions without limits. The other helps you save money and earn interest over time. Using the wrong one costs you in fees, transaction limits, or missed interest earnings.

In this guide, we break down the differences between the two account types so you can evaluate your actual transaction needs and choose the account that best supports your business.

A current account is a deposit account designed for businesses, organizations, and professionals who handle a high volume of transactions regularly.

Current accounts focus on operational convenience rather than earning returns. Banks typically do not pay interest on current account balances because these accounts are meant for active cash flow management, not savings.

For example, if you run an export business and need to pay suppliers weekly, receive customer payments daily, and manage payroll twice a month, a current account gives you the flexibility to handle all these transactions smoothly.

Current accounts suit businesses that need frequent access to funds, issue multiple checks, or process numerous transactions each month.

A savings account is designed for individuals who want to save money and grow their wealth gradually. Banks pay interest on the balance you maintain, helping your money grow over time without you doing anything extra.

These accounts work well for personal financial goals like building an emergency fund, saving for a down payment, or setting aside money for future needs. Unlike current accounts, savings accounts have transaction limits. Most banks allow a certain number of free withdrawals or transfers per month. Beyond that, you may face charges.

For instance, if you're a freelancer who receives project payments occasionally and wants to save a portion of your income, a savings account lets you earn interest while keeping your funds accessible when needed. The minimum balance requirement is usually lower compared to current accounts, and some banks even offer zero-balance savings accounts.

Savings accounts prioritize helping you save and earn, not managing daily business transactions.

Both account types serve different purposes and come with distinct features. Here's what sets them apart.

Let’s look at each difference in detail so that you can decide which account fits your needs.

Current accounts are built for businesses and professionals managing frequent transactions. Savings accounts cater to individuals looking to save money and earn interest on their deposits. If your primary goal is saving for future needs, a savings account makes sense. If you're managing daily business operations, a current account fits better.

Savings accounts pay interest on your balance, helping your money grow over time. Current accounts typically do not offer interest because they're designed for active cash flow, not wealth accumulation. For example, if you maintain ₹1,00,000 in a savings account at 4% annual interest, you earn ₹4,000 per year. The same balance in a current account earns nothing.

Current accounts allow higher transaction volume without penalties or charges. You can deposit, withdraw, and transfer funds as often as your business requires, as long as you stay within the limit allotted to your account by your bank. Savings accounts usually restrict the number of free transactions per month. Exceeding this limit results in charges per transaction.

Current accounts generally require higher minimum balances to avoid service charges. This balance can range from ₹10,000 to ₹25,000 or more, depending on the bank and account type. Savings accounts typically have lower minimum balance requirements, sometimes as low as ₹1,000 or even zero for certain account variants.

Current accounts may have higher service charges due to the additional features they offer, such as checkbooks and unlimited transactions. Savings accounts generally have lower fees and fewer charges, making them more affordable for personal use.

Current accounts are meant for businesses, firms, partnerships, companies, and professionals who need operational accounts. Savings accounts are designed for individuals, including salaried employees, students, and self-employed professionals who want to save and earn interest.

Your choice depends on your transaction patterns, financial goals, and whether you're managing business operations or personal savings. Here are the key factors to consider when deciding which account fits your needs.

If you make frequent deposits, withdrawals, and transfers daily or weekly, a current account works better. It lets you operate without worrying about hitting monthly caps. If you only need to access your funds occasionally and want to save for future goals, a savings account is the right choice.

If growing your money through interest is important, a savings account delivers that benefit. Current accounts don't pay interest, so if you're keeping idle funds in the account, you're missing out on potential earnings. For example, a freelancer with irregular income might prefer a savings account to earn interest on funds between projects.

Businesses with regular cash flow needs, supplier payments, salary disbursements, and customer collections should open a current account. It's built for operational flexibility and comes with features like checkbook facilities. If you're an individual managing personal finances, a savings account is sufficient.

Current accounts typically require higher minimum balances. If maintaining a high balance is not feasible for you right now, a savings account with a lower or zero-balance requirement makes more sense. Check the bank's penalty structure for falling below the minimum balance before deciding.

If you're doing business globally, receiving payments from international clients, or paying international suppliers, standard current accounts often involve high fees and slow processing times. For instance, if you're a service exporter collecting payments from clients in the US or UK, you need a solution that handles multi-currency transactions efficiently without eating into your margins with conversion fees and delays.

Standard current accounts work well for domestic transactions, but they fall short when your business operates across borders. If you're exporting goods or services, receiving payments from international clients, or managing multi-currency transactions, you need a solution built for global commerce.

PayGlocal gives you the tools to collect, track, and settle international payments without the complexity and costs that come with traditional banking.

Here’s how PayGlocal supports your global payment needs:

Whether you're a freelancer receiving payments from global platforms, a goods exporter managing marketplace settlements, or a service provider handling client invoices, PayGlocal makes international payments simple, transparent, and cost-effective.

Choosing between a current account and a savings account comes down to your transaction needs and financial goals. Current accounts work best for businesses with frequent transactions and operational flexibility needs. Savings accounts suit individuals looking to save money and earn interest over time.

If you're managing a business that operates locally, a current account from any major bank will serve your needs. But if you're expanding internationally or already receiving payments from global clients, standard banking options can slow you down with high fees, complicated processes, and poor exchange rates.

That's where PayGlocal makes the difference. You get multi-currency accounts, transparent pricing, instant compliance documentation, and seamless international payment collection, all in one platform.

Stop losing money to high conversion fees and slow settlement times. Get started with PayGlocal today and give your business the global payment infrastructure it needs to grow.

Current accounts and savings accounts serve completely different purposes. One is built for frequent business transactions without limits. The other helps you save money and earn interest over time. Using the wrong one costs you in fees, transaction limits, or missed interest earnings.

In this guide, we break down the differences between the two account types so you can evaluate your actual transaction needs and choose the account that best supports your business.

Key takeaways

- Purpose matters: Current accounts are built for frequent business transactions, while savings accounts help individuals save money and earn interest over time.

- Transaction flexibility: Current accounts allow high-volume transactions without penalties or extra charges. Savings accounts typically limit the number of free transactions per month.

- Interest earnings: With savings accounts, you earn interest on your balance, but current accounts generally do not offer interest.

- Best use: Choose current accounts for business operations with high transaction volumes. Choose savings accounts for personal savings goals and long-term wealth building.

- Global payment needs: If you're doing business internationally, you need more than a standard current account. PayGlocal offers multi-currency accounts with local collection capabilities in USD, GBP, EUR, and CAD.

What is a current account?

A current account is a deposit account designed for businesses, organizations, and professionals who handle a high volume of transactions regularly.

Current accounts focus on operational convenience rather than earning returns. Banks typically do not pay interest on current account balances because these accounts are meant for active cash flow management, not savings.

For example, if you run an export business and need to pay suppliers weekly, receive customer payments daily, and manage payroll twice a month, a current account gives you the flexibility to handle all these transactions smoothly.

Current accounts suit businesses that need frequent access to funds, issue multiple checks, or process numerous transactions each month.

What is a savings account?

A savings account is designed for individuals who want to save money and grow their wealth gradually. Banks pay interest on the balance you maintain, helping your money grow over time without you doing anything extra.

These accounts work well for personal financial goals like building an emergency fund, saving for a down payment, or setting aside money for future needs. Unlike current accounts, savings accounts have transaction limits. Most banks allow a certain number of free withdrawals or transfers per month. Beyond that, you may face charges.

For instance, if you're a freelancer who receives project payments occasionally and wants to save a portion of your income, a savings account lets you earn interest while keeping your funds accessible when needed. The minimum balance requirement is usually lower compared to current accounts, and some banks even offer zero-balance savings accounts.

Savings accounts prioritize helping you save and earn, not managing daily business transactions.

What are the key differences between current and savings accounts?

Both account types serve different purposes and come with distinct features. Here's what sets them apart.

Let’s look at each difference in detail so that you can decide which account fits your needs.

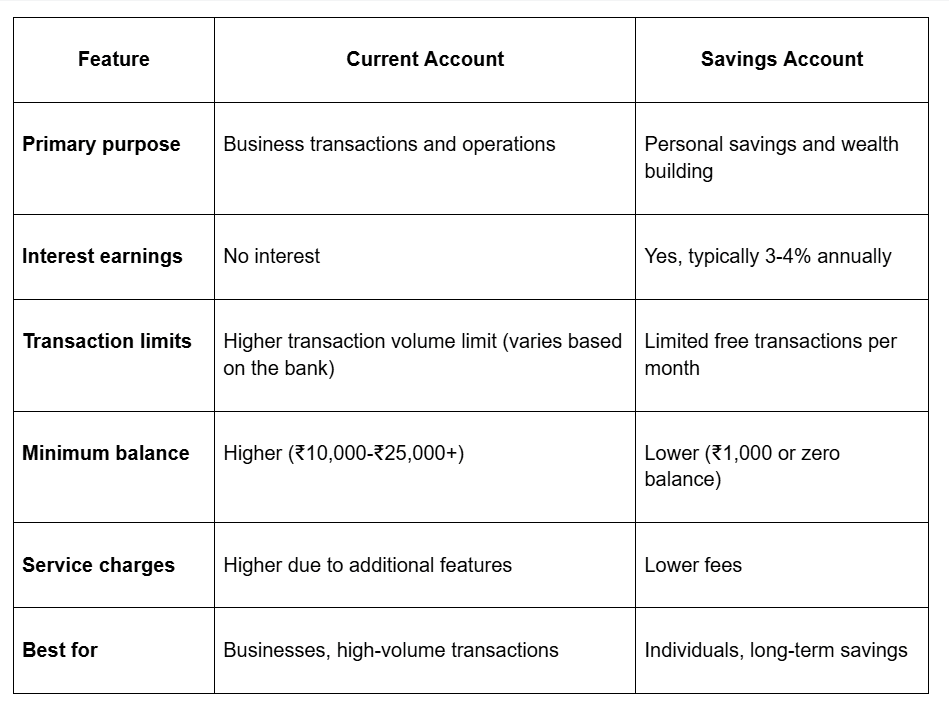

Purpose and usage

Current accounts are built for businesses and professionals managing frequent transactions. Savings accounts cater to individuals looking to save money and earn interest on their deposits. If your primary goal is saving for future needs, a savings account makes sense. If you're managing daily business operations, a current account fits better.

Interest earnings

Savings accounts pay interest on your balance, helping your money grow over time. Current accounts typically do not offer interest because they're designed for active cash flow, not wealth accumulation. For example, if you maintain ₹1,00,000 in a savings account at 4% annual interest, you earn ₹4,000 per year. The same balance in a current account earns nothing.

Transaction limits

Current accounts allow higher transaction volume without penalties or charges. You can deposit, withdraw, and transfer funds as often as your business requires, as long as you stay within the limit allotted to your account by your bank. Savings accounts usually restrict the number of free transactions per month. Exceeding this limit results in charges per transaction.

Minimum balance requirements

Current accounts generally require higher minimum balances to avoid service charges. This balance can range from ₹10,000 to ₹25,000 or more, depending on the bank and account type. Savings accounts typically have lower minimum balance requirements, sometimes as low as ₹1,000 or even zero for certain account variants.

Service charges and fees

Current accounts may have higher service charges due to the additional features they offer, such as checkbooks and unlimited transactions. Savings accounts generally have lower fees and fewer charges, making them more affordable for personal use.

Account holders

Current accounts are meant for businesses, firms, partnerships, companies, and professionals who need operational accounts. Savings accounts are designed for individuals, including salaried employees, students, and self-employed professionals who want to save and earn interest.

How to choose between a current account and a savings account?

Your choice depends on your transaction patterns, financial goals, and whether you're managing business operations or personal savings. Here are the key factors to consider when deciding which account fits your needs.

Transaction volume

If you make frequent deposits, withdrawals, and transfers daily or weekly, a current account works better. It lets you operate without worrying about hitting monthly caps. If you only need to access your funds occasionally and want to save for future goals, a savings account is the right choice.

Interest earnings

If growing your money through interest is important, a savings account delivers that benefit. Current accounts don't pay interest, so if you're keeping idle funds in the account, you're missing out on potential earnings. For example, a freelancer with irregular income might prefer a savings account to earn interest on funds between projects.

Business operations

Businesses with regular cash flow needs, supplier payments, salary disbursements, and customer collections should open a current account. It's built for operational flexibility and comes with features like checkbook facilities. If you're an individual managing personal finances, a savings account is sufficient.

Minimum balance

Current accounts typically require higher minimum balances. If maintaining a high balance is not feasible for you right now, a savings account with a lower or zero-balance requirement makes more sense. Check the bank's penalty structure for falling below the minimum balance before deciding.

International payments

If you're doing business globally, receiving payments from international clients, or paying international suppliers, standard current accounts often involve high fees and slow processing times. For instance, if you're a service exporter collecting payments from clients in the US or UK, you need a solution that handles multi-currency transactions efficiently without eating into your margins with conversion fees and delays.

Manage all your global payments in one platform with PayGlocal

Standard current accounts work well for domestic transactions, but they fall short when your business operates across borders. If you're exporting goods or services, receiving payments from international clients, or managing multi-currency transactions, you need a solution built for global commerce.

PayGlocal gives you the tools to collect, track, and settle international payments without the complexity and costs that come with traditional banking.

Here’s how PayGlocal supports your global payment needs:

- Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries and settle in INR.

- Global payment methods: Accept payments through 40+ local payment methods to reach more customers worldwide.

- Instant compliance documents: Receive FIRC (Foreign Inward Remittance Certificate) directly in your inbox after settlement, with no paperwork delays.

- Usage-based pricing: Pay only when you do transactions. No upfront costs, no monthly subscriptions, no documentation fees.

- One platform management: Manage all your international payments, reports, and compliance from a single dashboard easily.

Whether you're a freelancer receiving payments from global platforms, a goods exporter managing marketplace settlements, or a service provider handling client invoices, PayGlocal makes international payments simple, transparent, and cost-effective.

Final thoughts

Choosing between a current account and a savings account comes down to your transaction needs and financial goals. Current accounts work best for businesses with frequent transactions and operational flexibility needs. Savings accounts suit individuals looking to save money and earn interest over time.

If you're managing a business that operates locally, a current account from any major bank will serve your needs. But if you're expanding internationally or already receiving payments from global clients, standard banking options can slow you down with high fees, complicated processes, and poor exchange rates.

That's where PayGlocal makes the difference. You get multi-currency accounts, transparent pricing, instant compliance documentation, and seamless international payment collection, all in one platform.

Stop losing money to high conversion fees and slow settlement times. Get started with PayGlocal today and give your business the global payment infrastructure it needs to grow.