You closed a major international deal last week. The invoice went out, but the payment is stuck in a banking black hole. Your finance team is chasing wire confirmations, your customer is frustrated, and your cash flow is stalled.

This isn't just a communication gap; it’s a failure of the infrastructure. For Indian businesses, which now contribute nearly 48.58% of the country’s total exports, relying on basic transfer tools is no longer an option. Scaling globally in 2026 requires robust corporate payment systems, dedicated platforms designed to handle the high-volume, multi-currency, and regulatory complexities of modern trade.

This guide breaks down what corporate payment systems are, how they differ from the apps you use for personal errands, and how to choose a platform that turns your payment operations into a competitive advantage.

A corporate payment system is a platform that helps businesses manage all their payment activity from one place. This includes collecting payments from clients, paying vendors, processing payroll, and handling subscriptions or recurring charges.

Unlike personal payment apps, these systems are built for business-level needs. They handle larger transaction volumes, support more payment methods, and include features like role-based access, fraud checks, and detailed reporting.

For instance, if your business sells software to clients in the US, UK, and Singapore, a corporate payment system lets you collect from all three regions, track each payment, and settle funds into your account. No more juggling bank portals or chasing wire confirmations manually.

Most payment delays and errors trace back to manual steps that should have been automated long ago. The more transactions your business handles, the more those manual steps slow everything down.

Here are the main benefits your business gets from a corporate payment system.

The right combination depends on your business model and where your customers are. Pick platforms where these features work together in one workflow rather than needing manual steps between them.

Note: Not every platform offers all of these features. Check what is included before you commit, especially for cross-border payments where fraud screening and multi-currency support are critical.

Tools built for personal payments often break when businesses try to use them at scale. The approval workflows, security layers, and reporting needs are fundamentally different. Here is a side-by-side look at how they compare:

Consumer payments are simple and quick. Corporate payments need more control, more visibility, and more security because the stakes are higher. A missed vendor payment or a failed customer collection affects your cash flow, not just a single purchase.

Businesses deal with different kinds of payments depending on who they are paying or collecting from. Each type has its own flow, frequency, and priority. Here's a quick look at the main types of corporate payments and how they compare.

Each type needs different handling. Here's what to know about each one:

These are outgoing payments your business makes to suppliers, service providers, or contractors. For example, paying a cloud hosting provider or a logistics partner every month.

Most businesses handle these through bank transfers or scheduled payouts. The key is making sure payments go out on time and are easy to track against invoices.

This is money coming into your business from the people or companies you sell to. For an Indian exporter selling handmade goods to buyers in Europe, this means collecting payments in euros or pounds and settling them in INR.

The challenge here is payment success. If your checkout fails or does not support your customer's preferred payment method, you lose the sale.

Payroll covers regular salary payments to your team. It also includes contractor payouts, bonuses, and reimbursements.

For businesses with remote or international teams, payroll gets more complex. You need to handle different currencies, tax rules, and payment timelines.

If your business runs on subscriptions, recurring payments keep revenue flowing without manual follow-up. For instance, a SaaS company charging clients monthly needs a system that can auto-debit cards on schedule.

When recurring payments fail, revenue drops, and customers churn. A good system validates cards upfront and retries failed charges automatically.

These include GST, professional tax, TDS, and other statutory payments your business makes to government bodies. While most corporate payment systems do not process these directly, they help by keeping records clean for tax filing.

Having clear transaction records and downloadable reports saves hours during audit season.

The method you use to send or receive a payment affects speed, cost, and success rate. Different markets and customers prefer different methods, so your system needs to support more than one approach.

Here are the most common payment methods used in corporate transactions:

The right mix depends on where your customers are. For instance, if you sell to buyers in Europe and the US, you need card support, local European methods, plus USD bank transfers. A system that only supports one method leaves money on the table.

Tip: Check which payment methods your customers actually use before choosing a platform. Supporting the right three or four methods matters more than supporting dozens that your customers never pick.

Behind every payment, there is a process that moves money from one account to another. Corporate payment systems automate most of this, so your team does not have to do it manually.

Here's what happens at each stage when a payment moves through a corporate system:

1. Initiation: The payment starts when a customer checks out, an invoice is raised, or a scheduled payout triggers. The system captures the payment details and method.

2. Processing: The system routes the payment through the right channel, whether that is a card network, bank transfer, or local payment method. This is where payment orchestration plays a role, picking the best route for higher success.

3. Verification: Before the payment clears, the system runs fraud checks, validates the card or account, and confirms authorization. This step protects both the sender and receiver.

4. Settlement: Once verified, funds are settled into the receiver's account. Settlement timelines depend on the payment method and region, ranging from real-time to a few business days.

5. Reporting: The system logs the transaction, generates receipts, and updates dashboards. You get a clear record of every payment for reconciliation and compliance.

A well-built system handles all the stages without your team touching each transaction manually. The less manual work involved, the fewer errors and delays.

Even with the right system in place, corporate payments come with their own set of challenges. Knowing these challenges helps you pick a platform that actually solves them.

Here are the most common problems businesses face:

These challenges do not just slow your operations. They cost you real revenue in the form of lost sales, extra fees, and time spent on manual fixes.

Picking the wrong platform costs you time, money, and customers. The right choice depends on your business model, where your customers are, and what you need most.

Here’s what to check while selecting the corporate payment platform:

Tip: Ask for a full fee breakdown before signing up. Hidden charges on FX conversion or settlement can add up fast on high-volume accounts.

Collecting payments from international customers comes with real challenges: failed transactions, unclear fees, slow settlements, and fraud risks. Indian businesses selling globally need a payment system built for cross-border commerce, not a patchwork of bank portals and manual processes.

PayGlocal replaces the patchwork of bank portals and manual follow-ups with a single, high-performance command center. We've built the infrastructure so you can collect from 180+ countries without the usual cross-border headaches.

Here's what PayGlocal brings to your business:

PayGlocal charges no setup fees, no platform fees, and no documentation charges. You only pay when you transact. That means your costs stay tied to your revenue, not to a monthly subscription you pay regardless.

Corporate payment systems take the manual work out of managing business payments. The right system gives you faster collections, fewer failed transactions, clear records, and the security your business and customers need. Pick one that matches your payment methods, currencies, and customer locations.

If your business collects payments from global customers, the cost of staying on an outdated setup adds up every month in lost sales and delayed settlements. PayGlocal gives Indian businesses a single platform to collect from 180+ countries with high success rates, transparent pricing, and zero fixed costs. Get started with PayGlocal today.

This isn't just a communication gap; it’s a failure of the infrastructure. For Indian businesses, which now contribute nearly 48.58% of the country’s total exports, relying on basic transfer tools is no longer an option. Scaling globally in 2026 requires robust corporate payment systems, dedicated platforms designed to handle the high-volume, multi-currency, and regulatory complexities of modern trade.

This guide breaks down what corporate payment systems are, how they differ from the apps you use for personal errands, and how to choose a platform that turns your payment operations into a competitive advantage.

Key takeaways

- Corporate payment systems defined: These are platforms that help businesses send, receive, and track payments across clients, vendors, and teams in one place.

- Common payment types covered: Vendor payouts, customer collections, payroll, subscriptions, and tax-related transfers all fall under corporate payments.

- How they work: Payments move through initiation, processing, verification, settlement, and reporting stages.

- Key benefits: Faster collections, fewer errors, better cash flow visibility, and stronger security for every transaction.

- PayGlocal fits global businesses: It offers multi-currency accounts, smart checkout, fraud screening, and recurring payment support on a single platform with no fixed costs.

What is a corporate payment system?

A corporate payment system is a platform that helps businesses manage all their payment activity from one place. This includes collecting payments from clients, paying vendors, processing payroll, and handling subscriptions or recurring charges.

Unlike personal payment apps, these systems are built for business-level needs. They handle larger transaction volumes, support more payment methods, and include features like role-based access, fraud checks, and detailed reporting.

For instance, if your business sells software to clients in the US, UK, and Singapore, a corporate payment system lets you collect from all three regions, track each payment, and settle funds into your account. No more juggling bank portals or chasing wire confirmations manually.

What are the benefits of using a corporate payment system?

Most payment delays and errors trace back to manual steps that should have been automated long ago. The more transactions your business handles, the more those manual steps slow everything down.

Here are the main benefits your business gets from a corporate payment system.

- Faster payment collection: Automated checkout and smart routing mean customers pay faster, and funds reach your account sooner.

- Fewer manual errors: When payments are processed automatically, there is less room for data entry mistakes, duplicate entries, or missed invoices.

- Better cash flow visibility: Real-time dashboards show you exactly what came in, what is pending, and what failed, so you can plan ahead.

- Stronger security: Built-in fraud screening, encryption, and multi-factor authentication protect your business and your customers.

- Easier compliance: Automatic transaction records, downloadable reports, and compliance documents like Foreign Inward Remittance Certificate (FIRC) make audits and filings simpler.

- Support for global customers: Multi-currency support and local payment methods let your international buyers pay the way they prefer.

The right combination depends on your business model and where your customers are. Pick platforms where these features work together in one workflow rather than needing manual steps between them.

Note: Not every platform offers all of these features. Check what is included before you commit, especially for cross-border payments where fraud screening and multi-currency support are critical.

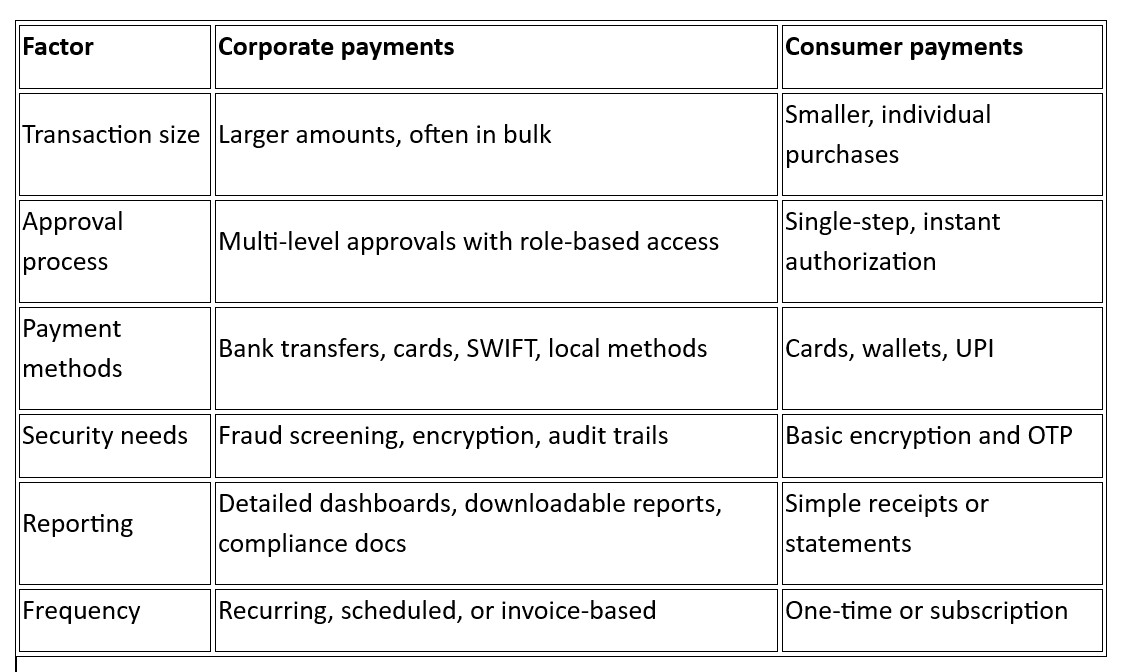

How do corporate payments differ from consumer payments?

Tools built for personal payments often break when businesses try to use them at scale. The approval workflows, security layers, and reporting needs are fundamentally different. Here is a side-by-side look at how they compare:

Consumer payments are simple and quick. Corporate payments need more control, more visibility, and more security because the stakes are higher. A missed vendor payment or a failed customer collection affects your cash flow, not just a single purchase.

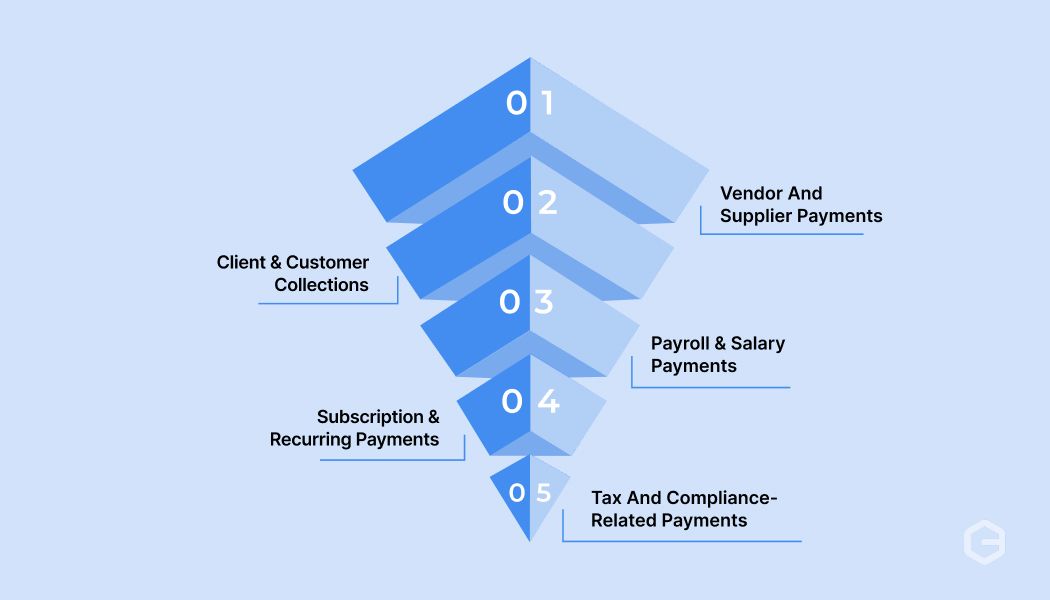

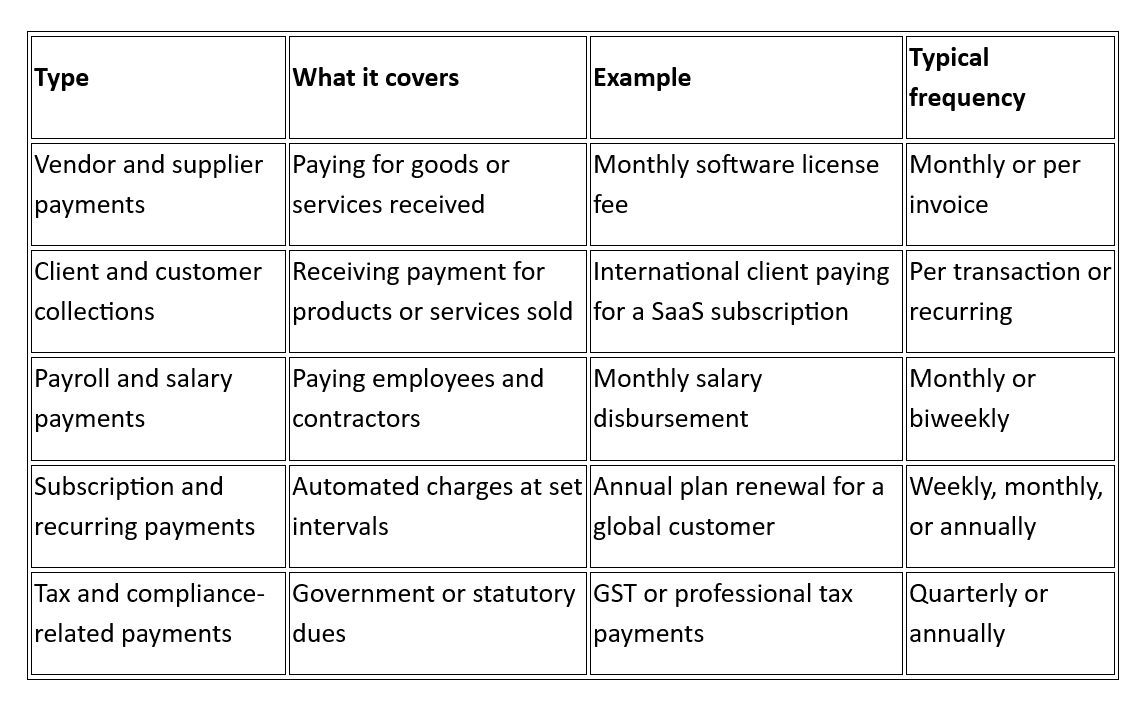

What are the common types of corporate payments?

Businesses deal with different kinds of payments depending on who they are paying or collecting from. Each type has its own flow, frequency, and priority. Here's a quick look at the main types of corporate payments and how they compare.

Each type needs different handling. Here's what to know about each one:

1. Vendor and supplier payments

These are outgoing payments your business makes to suppliers, service providers, or contractors. For example, paying a cloud hosting provider or a logistics partner every month.

Most businesses handle these through bank transfers or scheduled payouts. The key is making sure payments go out on time and are easy to track against invoices.

2. Client and customer collections

This is money coming into your business from the people or companies you sell to. For an Indian exporter selling handmade goods to buyers in Europe, this means collecting payments in euros or pounds and settling them in INR.

The challenge here is payment success. If your checkout fails or does not support your customer's preferred payment method, you lose the sale.

3. Payroll and salary payments

Payroll covers regular salary payments to your team. It also includes contractor payouts, bonuses, and reimbursements.

For businesses with remote or international teams, payroll gets more complex. You need to handle different currencies, tax rules, and payment timelines.

4. Subscription and recurring payments

If your business runs on subscriptions, recurring payments keep revenue flowing without manual follow-up. For instance, a SaaS company charging clients monthly needs a system that can auto-debit cards on schedule.

When recurring payments fail, revenue drops, and customers churn. A good system validates cards upfront and retries failed charges automatically.

5. Tax and compliance-related payments

These include GST, professional tax, TDS, and other statutory payments your business makes to government bodies. While most corporate payment systems do not process these directly, they help by keeping records clean for tax filing.

Having clear transaction records and downloadable reports saves hours during audit season.

What methods do businesses use for corporate payments?

The method you use to send or receive a payment affects speed, cost, and success rate. Different markets and customers prefer different methods, so your system needs to support more than one approach.

Here are the most common payment methods used in corporate transactions:

- Bank transfers (SWIFT, NEFT, wire): The traditional method for large B2B payments. SWIFT transfers handle international payments, while NEFT and RTGS cover domestic ones. Reliable, but slower and often more expensive for cross-border transactions.

- Credit and debit cards: Common for online purchases, subscriptions, and smaller B2B transactions. International card payments need smart routing to keep approval rates high across regions.

- Local payment methods: These include country-specific options like iDEAL in the Netherlands, Bancontact in Belgium, or Boleto in Brazil. Offering these at checkout builds trust and increases conversions with local buyers.

- Real-time payments: Instant settlement systems like UPI in India or Faster Payments in the UK. Growing fast, but availability and limits vary by country.

- Digital wallets: Options like Apple Pay, Google Pay, or regional wallets. Useful for consumer-facing businesses that collect from individual buyers globally.

The right mix depends on where your customers are. For instance, if you sell to buyers in Europe and the US, you need card support, local European methods, plus USD bank transfers. A system that only supports one method leaves money on the table.

Tip: Check which payment methods your customers actually use before choosing a platform. Supporting the right three or four methods matters more than supporting dozens that your customers never pick.

How do corporate payment systems work?

Behind every payment, there is a process that moves money from one account to another. Corporate payment systems automate most of this, so your team does not have to do it manually.

Here's what happens at each stage when a payment moves through a corporate system:

1. Initiation: The payment starts when a customer checks out, an invoice is raised, or a scheduled payout triggers. The system captures the payment details and method.

2. Processing: The system routes the payment through the right channel, whether that is a card network, bank transfer, or local payment method. This is where payment orchestration plays a role, picking the best route for higher success.

3. Verification: Before the payment clears, the system runs fraud checks, validates the card or account, and confirms authorization. This step protects both the sender and receiver.

4. Settlement: Once verified, funds are settled into the receiver's account. Settlement timelines depend on the payment method and region, ranging from real-time to a few business days.

5. Reporting: The system logs the transaction, generates receipts, and updates dashboards. You get a clear record of every payment for reconciliation and compliance.

A well-built system handles all the stages without your team touching each transaction manually. The less manual work involved, the fewer errors and delays.

What are the common challenges with corporate payments?

Even with the right system in place, corporate payments come with their own set of challenges. Knowing these challenges helps you pick a platform that actually solves them.

Here are the most common problems businesses face:

- Payment failures and declines: International card payments get declined more often than domestic ones because issuing banks flag incorrect card data, currency mismatches, or weak transaction messaging.

- Fraud and security risks: Without real-time screening, your business is exposed to chargebacks and fake transactions that cost more to fix after settlement than to prevent upfront.

- Managing payments across currencies: Unclear conversion rates and hidden costs in FX markups eat into your margins, especially when you cannot see exactly what the customer paid versus what you received.

- Lack of visibility into payment status: Without real-time tracking, your finance team spends time chasing updates on whether a payment is processing, failed, or settled instead of planning ahead.

These challenges do not just slow your operations. They cost you real revenue in the form of lost sales, extra fees, and time spent on manual fixes.

How to choose the right corporate payment system?

Picking the wrong platform costs you time, money, and customers. The right choice depends on your business model, where your customers are, and what you need most.

Here’s what to check while selecting the corporate payment platform:

- Multi-currency account support: Your system should accept payments in your customers' local currencies so they do not drop off at checkout or pay extra conversion fees on their end.

- Payment success rates: Ask about authorization rates on international card payments specifically, since even a small improvement in approval rates translates directly into more revenue.

- Fraud and risk features: The system should screen transactions in real-time using device data, location signals, and card behavior patterns without blocking genuine customers.

- Integration and setup: Check how the payment gateway connects with your website, app, or ERP system, and whether it offers API, plugin, or no-code options to go live faster.

- Pricing and hidden fees: Do not just look at the base transaction fees. Check for setup charges, monthly platform costs, FX markups, and settlement fees that add up on high-volume accounts.

Tip: Ask for a full fee breakdown before signing up. Hidden charges on FX conversion or settlement can add up fast on high-volume accounts.

Set up your corporate payment system with higher success rates using PayGlocal

Collecting payments from international customers comes with real challenges: failed transactions, unclear fees, slow settlements, and fraud risks. Indian businesses selling globally need a payment system built for cross-border commerce, not a patchwork of bank portals and manual processes.

PayGlocal replaces the patchwork of bank portals and manual follow-ups with a single, high-performance command center. We've built the infrastructure so you can collect from 180+ countries without the usual cross-border headaches.

Here's what PayGlocal brings to your business:

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD, and globally in 33+ currencies. Your international clients pay in their own currency, and you settle in INR.

- Dynamic checkout: A checkout experience that adapts to each customer's region and preferred payment method, leading to higher conversion rates at the final step.

- Card payments: Accept international credit and debit cards with smart routing and enhanced messaging that pushes approval rates higher on cross-border transactions.

- Recurring payments: Set up subscriptions, standing instructions, and auto-debits on international cards so your revenue keeps flowing without manual follow-up.

- One platform: Manage all your payments, reports, user roles, and compliance documents from a single dashboard. No switching between tools.

PayGlocal charges no setup fees, no platform fees, and no documentation charges. You only pay when you transact. That means your costs stay tied to your revenue, not to a monthly subscription you pay regardless.

Final thoughts

Corporate payment systems take the manual work out of managing business payments. The right system gives you faster collections, fewer failed transactions, clear records, and the security your business and customers need. Pick one that matches your payment methods, currencies, and customer locations.

If your business collects payments from global customers, the cost of staying on an outdated setup adds up every month in lost sales and delayed settlements. PayGlocal gives Indian businesses a single platform to collect from 180+ countries with high success rates, transparent pricing, and zero fixed costs. Get started with PayGlocal today.