You're processing more international orders than last quarter, and then a payment gets frozen. No warning, no clear reason, just your funds sitting in a bank's review queue while you try to figure out what went wrong. That's what happens when compliance issues show up.

Non-compliance with the regulations leads to payment failures, account freezes, regulatory penalties, and operational disruptions that hurt your business. In fact, data shows that compliance violations have cost up to $45.679 billion in penalties.

This guide breaks down in detail what cross-border payment compliance actually means, which requirements apply to your business, and how to handle them without all the complexity.

Cross-border payment compliance refers to the regulatory requirements you must follow when sending or receiving money internationally. These regulations exist to prevent illegal financial activities, such as money laundering, while protecting customer data across jurisdictions. Every international transaction triggers compliance checks before funds can move from one country to another.

For instance, when a customer in the United States pays your India-based business, that transaction must meet compliance requirements from both countries. This includes verifying who your customer is, checking they're not on any restricted lists, and handling their payment data securely.

Compliance isn't a one-time checklist. It applies to every international transaction you process, whether you're a freelancer receiving payments from clients abroad or an e-commerce business selling to customers worldwide.

Payment processors and banks operate under strict regulatory oversight. They're required to verify every international transaction meets compliance standards before processing it. This means your payments either meet requirements or they fail.

Here's what compliance protects you from:

Tip: Compliance also builds customer trust. When customers see proper security measures and data protection, they feel confident completing international transactions with your business.

Before any international payment processes, it goes through multiple verification steps that check identity, screen for risks, and ensure proper documentation. Payment processors run these checks automatically on every transaction to meet regulatory standards and prevent financial crimes. Missing even one requirement causes the payment to fail or get flagged for manual review.

Here's what applies to your cross-border transactions:

You must verify the identity of customers, vendors, and business partners before processing payments. This means collecting and validating documentation like government IDs, business registration certificates, and proof of address. KYC ensures you know who you're doing business with across borders.

Systems must monitor transaction patterns to detect suspicious activities that could indicate money laundering or terrorist financing. This includes watching for unusual transaction amounts, frequencies, or destinations that don't match normal business patterns.

Every transaction gets checked in real-time against international sanctions lists from organizations like OFAC and the UN. This prevents you from accidentally processing payments involving restricted entities, individuals, or countries.

Customer financial data must be handled according to regional privacy regulations. For instance, European customers are protected by GDPR, which sets strict rules on how their payment information can be collected, stored, and used.

Proper records must be maintained for every cross-border payment, including transaction details, compliance checks performed, and verification documents. These records support audits and regulatory reporting requirements.

Note: Compliance requirements vary by country and payment type. The regulations that apply to a freelancer receiving $500 differ from those facing a business processing thousands of international transactions monthly. Always verify which specific requirements apply to your situation.

Cross-border compliance verifies the legitimacy of every payment before it moves ahead. Instead of a single check, the system runs multiple automated validations the moment a customer initiates a payment. Here's what happens at each stage of the process:

- Payment initiated: Customer enters payment details on your checkout or invoice.

- Identity verification: System checks customer information against KYC records and flags any mismatches.

- Sanctions screening: Transaction details get checked against current international sanctions lists in real-time.

- Risk assessment: Automated rules evaluate transaction amount, frequency, destination country, and customer history.

- Approval or flag: Compliant transactions are processed immediately, while flagged transactions go to manual review.

- Documentation: System records all checks performed and stores an audit trail for regulatory reporting.

For instance, when a US customer pays your India-based business $2,000 for services, the payment system verifies whether the customer's identity matches their previous transactions, confirms neither party appears on sanctions lists, checks the payment falls within normal patterns, and documents everything before releasing funds to your account. This entire process happens in seconds for compliant transactions.

Businesses handle cross-border payment compliance through different approaches. Your choice depends on your transaction volume, technical resources, and how much control you want over the compliance process. Here's how each model works:

Most businesses moving money across borders choose third-party providers because building in-house compliance requires regulatory licenses, legal expertise, technology infrastructure, and ongoing monitoring of changing regulations across multiple countries. Banks offer compliance coverage but often lack flexibility for modern payment needs like multi-currency accounts or recurring billing.

Third-party providers and payment aggregators combine regulatory authorization with payment technology, giving you compliant processing without the overhead of building systems yourself. This model works particularly well for businesses that need to scale quickly while staying compliant across different markets.

Each country enforces its own payment regulations based on local laws, economic policies, and security priorities. A payment between two countries must satisfy both jurisdictions simultaneously, so your compliance approach changes depending on who's sending and who's receiving the money.

Here's how regional differences affect your payments:

For example, a payment from Singapore to India must satisfy Singapore's Payment Services Act requirements and India's foreign exchange management rules. Your payment system needs intelligence to apply the correct framework based on the transaction origin and destination.

Manual compliance processes create bottlenecks that prevent you from scaling internationally. For businesses without a large compliance department, the difficulty lies in the sheer volume of data and the speed at which global rules change, creating a constant struggle between staying secure and staying profitable.

Here are the primary challenges that businesses must overcome:

Regulations don't stay static. Countries update their compliance requirements regularly, sanctions lists change frequently, and new data privacy laws emerge. Tracking these changes across multiple jurisdictions while running your business is nearly impossible without dedicated resources.

Different countries require different documents for verification and compliance. Collecting, validating, and storing these documents correctly takes time and creates operational overhead. Missing or incorrect documentation leads to payment failures and compliance gaps.

Each payment must be screened against current sanctions lists before processing. Manual screening is too slow and error-prone for businesses processing multiple daily transactions. Delayed screening creates compliance risks and payment delays.

Strong compliance measures protect your business but can create friction for customers. Excessive verification steps or slow processing drives customers away. Finding the right balance between security and a smooth payment experience is challenging.

Compliance success comes from combining automated systems with clear operational processes. Instead of manually checking every transaction, you need technology that applies compliance rules consistently while documenting everything for audit trails. The businesses that handle this well focus on prevention rather than reaction.

Here's what works in practice:

For instance, when you receive an international payment, your system should automatically verify the payer's identity against your KYC records, screen the transaction against sanctions lists, apply appropriate AML rules, and document everything without manual intervention.

Modern compliance relies on automated systems that handle verification, screening, and monitoring faster and more accurately than manual processes. These tools process several checks per second while maintaining detailed audit trails that satisfy regulatory requirements.

Key technologies that make compliance manageable:

These technologies work together as part of your payment infrastructure. When a customer initiates a payment, automated systems handle identity verification, sanctions screening, risk assessment, and documentation in seconds. You get compliant processing without hiring compliance specialists or building verification systems from scratch.

Compliance failures don't just slow you down. They block payments from reaching your account, trigger manual reviews that delay settlements for days, and force you to chase documentation instead of focusing on growing your business.

PayGlocal builds compliance directly into your payment infrastructure. You get fully authorized payment processing that meets international regulatory standards automatically, without hiring compliance specialists or building verification systems yourself.

Here's how PayGlocal keeps you compliant while you focus on growth:

PayGlocal handles the complexity of multi-jurisdictional compliance automatically. You process international payments confidently while compliance, screening, and documentation happen seamlessly in the background.

Cross-border payment compliance protects your business and enables smooth international transactions. While requirements like KYC, AML, sanctions screening, and data privacy apply to every international payment, you don't need to become a compliance expert or build systems from scratch.

The businesses that succeed globally are those that embed compliance into their payment infrastructure rather than treating it as a separate burden. Your competitors who've already solved this are processing international payments smoothly while you're still dealing with compliance questions and payment failures.

Ready to accept international payments with confidence? PayGlocal gives you compliant, secure cross-border payment processing that works seamlessly across 180+ countries. Stop worrying about compliance requirements and start growing globally.

Get started with PayGlocal today to see how simple international payments can be when compliance is built in from day one.

Non-compliance with the regulations leads to payment failures, account freezes, regulatory penalties, and operational disruptions that hurt your business. In fact, data shows that compliance violations have cost up to $45.679 billion in penalties.

This guide breaks down in detail what cross-border payment compliance actually means, which requirements apply to your business, and how to handle them without all the complexity.

Key takeaways

- Compliance is mandatory, not optional: Cross-border payments require adherence to international regulations, including KYC, AML, and sanctions screening to prevent fraud and illegal finance activities.

- Multiple compliance frameworks apply: Different countries have varying requirements, so you need to align with both sender and receiver regulations for every transaction.

- Core requirements include identity verification: KYC processes verify customer identities, while AML monitoring detects suspicious transaction patterns across borders.

- Technology handles complexity: Modern compliance-by-design tools automate screening, monitoring, and documentation to reduce errors and manual work.

- The right payment partner simplifies everything: Working with PayGlocal means compliance is built into your payment stack, letting you focus on growth instead of regulations.

What is cross-border payment compliance?

Cross-border payment compliance refers to the regulatory requirements you must follow when sending or receiving money internationally. These regulations exist to prevent illegal financial activities, such as money laundering, while protecting customer data across jurisdictions. Every international transaction triggers compliance checks before funds can move from one country to another.

For instance, when a customer in the United States pays your India-based business, that transaction must meet compliance requirements from both countries. This includes verifying who your customer is, checking they're not on any restricted lists, and handling their payment data securely.

Compliance isn't a one-time checklist. It applies to every international transaction you process, whether you're a freelancer receiving payments from clients abroad or an e-commerce business selling to customers worldwide.

Why does cross-border payment compliance matter?

Payment processors and banks operate under strict regulatory oversight. They're required to verify every international transaction meets compliance standards before processing it. This means your payments either meet requirements or they fail.

Here's what compliance protects you from:

- Payment failures and rejections: Non-compliant transactions get blocked automatically by payment processors, causing failed checkouts and lost revenue.

- Account suspensions and freezes: One compliance violation can trigger investigations that freeze your entire payment account, stopping all international transactions while authorities review.

- Regulatory penalties and fines: Authorities impose financial penalties for compliance breaches, with amounts scaling based on violation severity and transaction volumes.

- Damaged business reputation: Compliance issues signal poor operational controls, making payment partners, banks, and customers hesitant to work with you.

- Lost business opportunities: Many global marketplaces and enterprise clients require compliance certifications before they'll accept you as a vendor or partner.

Tip: Compliance also builds customer trust. When customers see proper security measures and data protection, they feel confident completing international transactions with your business.

What are the key cross-border payment compliance requirements?

Before any international payment processes, it goes through multiple verification steps that check identity, screen for risks, and ensure proper documentation. Payment processors run these checks automatically on every transaction to meet regulatory standards and prevent financial crimes. Missing even one requirement causes the payment to fail or get flagged for manual review.

Here's what applies to your cross-border transactions:

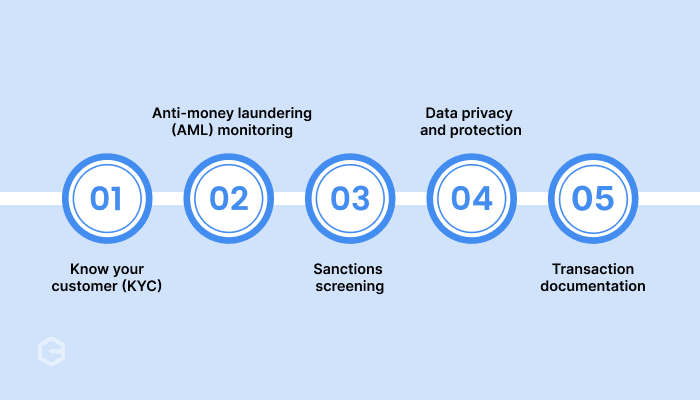

- Know your customer (KYC)

You must verify the identity of customers, vendors, and business partners before processing payments. This means collecting and validating documentation like government IDs, business registration certificates, and proof of address. KYC ensures you know who you're doing business with across borders.

- Anti-money laundering (AML) monitoring

Systems must monitor transaction patterns to detect suspicious activities that could indicate money laundering or terrorist financing. This includes watching for unusual transaction amounts, frequencies, or destinations that don't match normal business patterns.

- Sanctions screening

Every transaction gets checked in real-time against international sanctions lists from organizations like OFAC and the UN. This prevents you from accidentally processing payments involving restricted entities, individuals, or countries.

- Data privacy and protection

Customer financial data must be handled according to regional privacy regulations. For instance, European customers are protected by GDPR, which sets strict rules on how their payment information can be collected, stored, and used.

- Transaction documentation

Proper records must be maintained for every cross-border payment, including transaction details, compliance checks performed, and verification documents. These records support audits and regulatory reporting requirements.

Note: Compliance requirements vary by country and payment type. The regulations that apply to a freelancer receiving $500 differ from those facing a business processing thousands of international transactions monthly. Always verify which specific requirements apply to your situation.

How does cross-border payment compliance work?

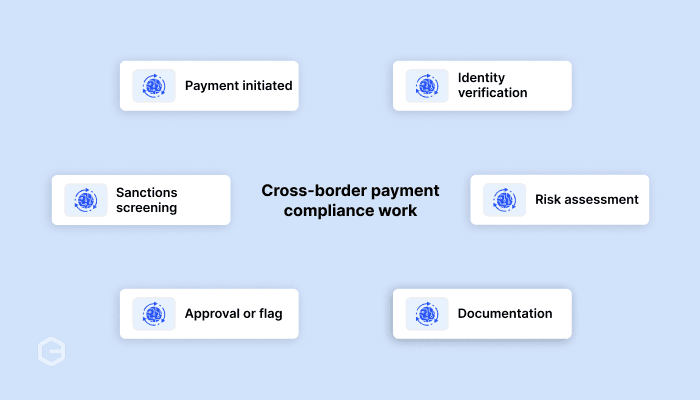

Cross-border compliance verifies the legitimacy of every payment before it moves ahead. Instead of a single check, the system runs multiple automated validations the moment a customer initiates a payment. Here's what happens at each stage of the process:

- Payment initiated: Customer enters payment details on your checkout or invoice.

- Identity verification: System checks customer information against KYC records and flags any mismatches.

- Sanctions screening: Transaction details get checked against current international sanctions lists in real-time.

- Risk assessment: Automated rules evaluate transaction amount, frequency, destination country, and customer history.

- Approval or flag: Compliant transactions are processed immediately, while flagged transactions go to manual review.

- Documentation: System records all checks performed and stores an audit trail for regulatory reporting.

For instance, when a US customer pays your India-based business $2,000 for services, the payment system verifies whether the customer's identity matches their previous transactions, confirms neither party appears on sanctions lists, checks the payment falls within normal patterns, and documents everything before releasing funds to your account. This entire process happens in seconds for compliant transactions.

What are the different types of compliance models?

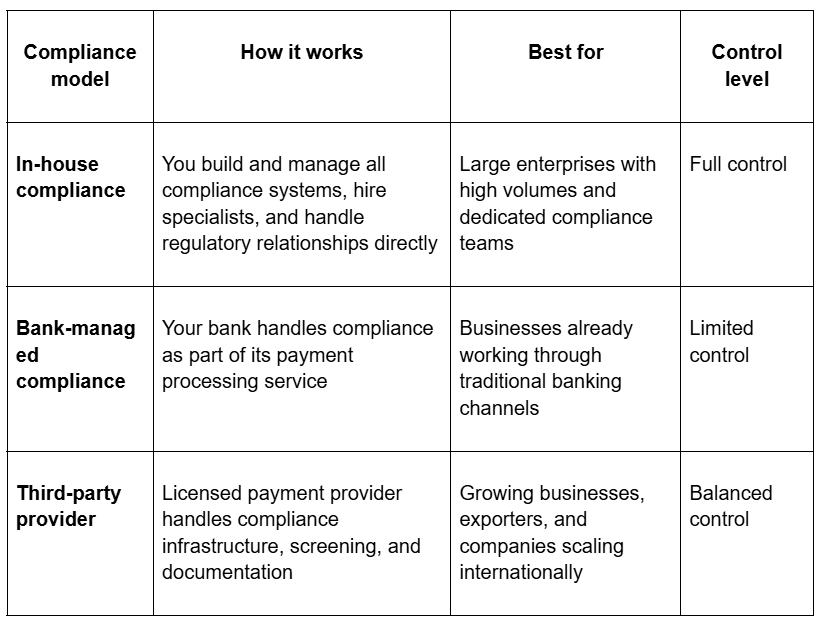

Businesses handle cross-border payment compliance through different approaches. Your choice depends on your transaction volume, technical resources, and how much control you want over the compliance process. Here's how each model works:

Most businesses moving money across borders choose third-party providers because building in-house compliance requires regulatory licenses, legal expertise, technology infrastructure, and ongoing monitoring of changing regulations across multiple countries. Banks offer compliance coverage but often lack flexibility for modern payment needs like multi-currency accounts or recurring billing.

Third-party providers and payment aggregators combine regulatory authorization with payment technology, giving you compliant processing without the overhead of building systems yourself. This model works particularly well for businesses that need to scale quickly while staying compliant across different markets.

How do compliance frameworks differ across regions?

Each country enforces its own payment regulations based on local laws, economic policies, and security priorities. A payment between two countries must satisfy both jurisdictions simultaneously, so your compliance approach changes depending on who's sending and who's receiving the money.

Here's how regional differences affect your payments:

- Multi-jurisdictional requirements: Your business must meet compliance standards from both the sender's country and the receiver's country for every transaction.

- Varying verification standards: Some countries require minimal documentation while others demand extensive proof of identity, business legitimacy, and transaction purpose.

- Different data handling rules: European customers are protected by GDPR's strict data privacy requirements, while other regions follow different frameworks for storing and processing payment information.

- Country-specific reporting obligations: Certain jurisdictions require detailed transaction reporting, tax withholding, or currency conversion documentation that others don't mandate.

- Changing regulatory landscapes: Countries update their payment regulations at different times, meaning requirements that apply today may shift tomorrow in specific markets.

For example, a payment from Singapore to India must satisfy Singapore's Payment Services Act requirements and India's foreign exchange management rules. Your payment system needs intelligence to apply the correct framework based on the transaction origin and destination.

What are the main compliance challenges businesses face?

Manual compliance processes create bottlenecks that prevent you from scaling internationally. For businesses without a large compliance department, the difficulty lies in the sheer volume of data and the speed at which global rules change, creating a constant struggle between staying secure and staying profitable.

Here are the primary challenges that businesses must overcome:

- Keeping up with changing regulations

Regulations don't stay static. Countries update their compliance requirements regularly, sanctions lists change frequently, and new data privacy laws emerge. Tracking these changes across multiple jurisdictions while running your business is nearly impossible without dedicated resources.

- Managing documentation across borders

Different countries require different documents for verification and compliance. Collecting, validating, and storing these documents correctly takes time and creates operational overhead. Missing or incorrect documentation leads to payment failures and compliance gaps.

- Screening every transaction in real-time

Each payment must be screened against current sanctions lists before processing. Manual screening is too slow and error-prone for businesses processing multiple daily transactions. Delayed screening creates compliance risks and payment delays.

- Balancing security with customer experience

Strong compliance measures protect your business but can create friction for customers. Excessive verification steps or slow processing drives customers away. Finding the right balance between security and a smooth payment experience is challenging.

How can you ensure cross-border payment compliance?

Compliance success comes from combining automated systems with clear operational processes. Instead of manually checking every transaction, you need technology that applies compliance rules consistently while documenting everything for audit trails. The businesses that handle this well focus on prevention rather than reaction.

Here's what works in practice:

- Work with compliant payment partners: Choose payment providers that are licensed and authorized for cross-border transactions. They handle regulatory requirements as part of their service, which reduces your compliance burden significantly.

- Implement automated screening: Use systems that automatically screen transactions against sanctions lists and apply risk rules in real-time. Automation catches issues instantly and processes legitimate payments faster than manual review.

- Maintain clear documentation: Keep organized records of verification documents, transaction details, and compliance checks performed. Good documentation supports audits and helps resolve any questions that arise.

- Set up monitoring alerts: Configure systems to flag unusual transaction patterns automatically. Early detection of suspicious activity helps you investigate and respond before small issues become serious problems.

- Secure customer data properly: Implement encryption for data storage and transmission. Ensure your systems meet data protection standards for all regions where you do business.

For instance, when you receive an international payment, your system should automatically verify the payer's identity against your KYC records, screen the transaction against sanctions lists, apply appropriate AML rules, and document everything without manual intervention.

What technology solutions support cross-border payment compliance?

Modern compliance relies on automated systems that handle verification, screening, and monitoring faster and more accurately than manual processes. These tools process several checks per second while maintaining detailed audit trails that satisfy regulatory requirements.

Key technologies that make compliance manageable:

- Real-time screening systems: Automatically check every transaction against current sanctions lists from multiple international sources before processing payments.

- Transaction monitoring platforms: Track payment patterns across your business to detect unusual activities that might indicate fraud or money laundering attempts.

- Automated KYC verification: Digital identity verification systems validate customer documents, check databases, and confirm legitimacy without manual document review.

- Risk scoring engines: Assign risk levels to transactions based on amount, frequency, destination, customer history, and other factors to prioritize review resources.

- Compliance documentation systems: Generate and store required records automatically, including verification certificates, screening results, and transaction details for audits.

- API integration capabilities: Connect compliance checks directly into your payment flow so verification happens seamlessly without redirecting customers or adding manual steps.

These technologies work together as part of your payment infrastructure. When a customer initiates a payment, automated systems handle identity verification, sanctions screening, risk assessment, and documentation in seconds. You get compliant processing without hiring compliance specialists or building verification systems from scratch.

Handle compliance effortlessly with PayGlocal and scale globally

Compliance failures don't just slow you down. They block payments from reaching your account, trigger manual reviews that delay settlements for days, and force you to chase documentation instead of focusing on growing your business.

PayGlocal builds compliance directly into your payment infrastructure. You get fully authorized payment processing that meets international regulatory standards automatically, without hiring compliance specialists or building verification systems yourself.

Here's how PayGlocal keeps you compliant while you focus on growth:

- Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries with built-in compliance for ensuring secure transactions.

- Sanction screening: Every transaction is automatically screened against international sanctions lists in real-time using privacy-first technology.

- Advanced fraud and risk management: Real-time fraud detection screens suspicious transactions while letting legitimate payments through, protecting your business without blocking customers.

- One Platform: Manage all compliance documentation, transaction records, and monitoring from a single dashboard with customizable access controls.

- Automatic compliance documentation: Receive Foreign Inward Remittance Certificate (FIRC) and other required compliance documents directly after settlement with no manual processing needed.

PayGlocal handles the complexity of multi-jurisdictional compliance automatically. You process international payments confidently while compliance, screening, and documentation happen seamlessly in the background.

Final thoughts

Cross-border payment compliance protects your business and enables smooth international transactions. While requirements like KYC, AML, sanctions screening, and data privacy apply to every international payment, you don't need to become a compliance expert or build systems from scratch.

The businesses that succeed globally are those that embed compliance into their payment infrastructure rather than treating it as a separate burden. Your competitors who've already solved this are processing international payments smoothly while you're still dealing with compliance questions and payment failures.

Ready to accept international payments with confidence? PayGlocal gives you compliant, secure cross-border payment processing that works seamlessly across 180+ countries. Stop worrying about compliance requirements and start growing globally.

Get started with PayGlocal today to see how simple international payments can be when compliance is built in from day one.