You check one dashboard for card payments, another for recurring billing, and a third for multi-currency collections. By the time you have reconciled everything, half your morning is gone. Your payment setup works, but it does not work together.

Cross-channel payment solutions fix this by connecting every payment touchpoint into one system. India recorded over 18,000 crore digital payment transactions in 2024-25, and that volume is growing every year. The businesses keeping up are the ones collecting across all channels from a single connected platform.

This guide covers what cross-channel payment solutions are, how they work, and how to choose the right one for your needs.

Key Takeaways

What are cross-channel payment solutions?

Cross-channel payment solutions are platforms that let you accept and manage payments across all your sales channels from one place. Instead of using one tool for your website checkout, another for payment links, and a third for subscriptions, everything connects through a single system.

For example, an Indian D2C brand selling globally might collect card payments on its Shopify store, send payment links to wholesale buyers over email, and run monthly subscriptions for a loyalty program. A cross-channel solution handles all three through one platform, with shared data and consistent payment options.

The key idea is connection. Each channel connects to the others. When a customer saves their card during checkout, that information carries over if they later pay through a link or set up a recurring payment. You get one view of every transaction, and your customer gets a smooth experience at every step.

What are the benefits of cross-channel payment solutions?

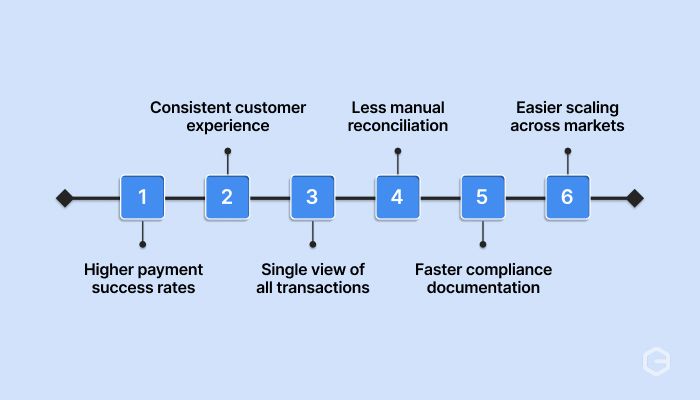

When your payment channels work together, the improvements show up across your business. From fewer failed payments to less manual work, the benefits add up fast. Here is what connected payment channels do for you:

The right cross-channel setup ensures you get more approved payments and a checkout experience your global customers trust.

Note: Cross-channel benefits are strongest when all your payment methods, from cards to local wallets to recurring billing, run on the same platform. Connecting separate tools adds complexity and delay.

What channels does a cross-channel payment solution cover?

A cross-channel setup connects the specific touchpoints where your customers pay you. For businesses selling globally, these are not physical store terminals. They are the digital channels where international buyers complete purchases and send funds.

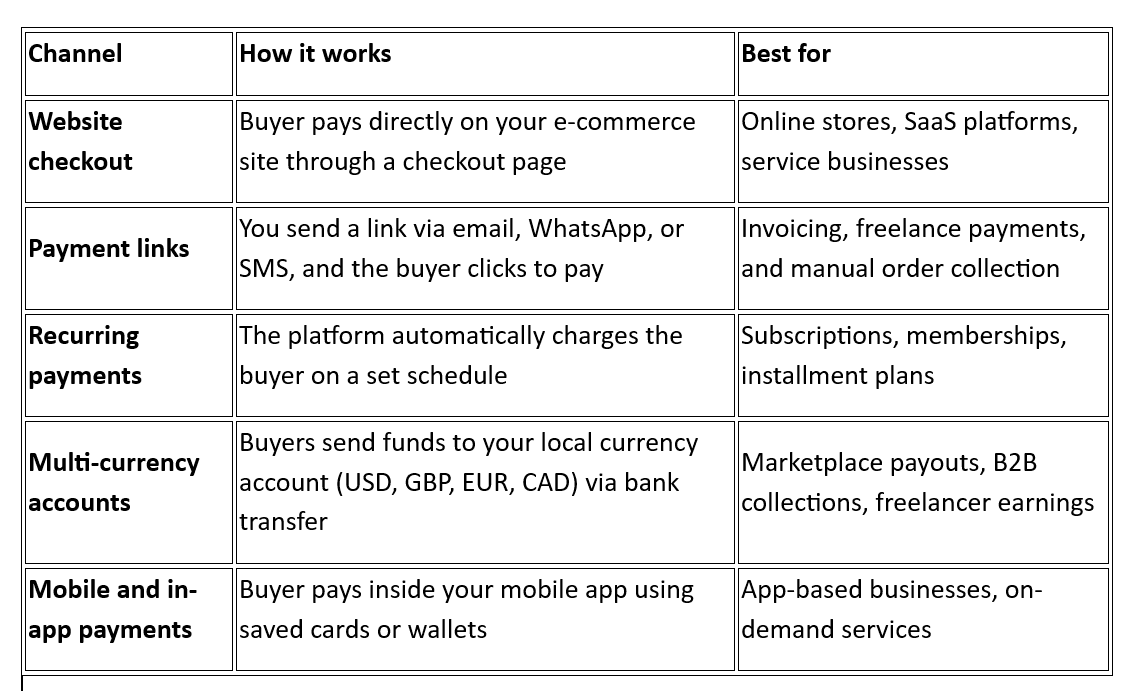

Here’s how the main channel types compare and how each one fits into a cross-channel system.

Each of these channels serves a different buying situation. Here is what makes each one work within a connected system.

1. Website checkout

The website checkout is where most global transactions start. Your checkout page shows payment options based on the buyer's location, like international cards, Apple Pay, or local wallets.

For example, a buyer in the UK sees GBP pricing and their preferred card network, while a buyer in Singapore sees options relevant to them. A cross-channel platform makes sure this checkout shares data with your other channels.

2. Payment links

Payment links are useful when there is no storefront involved. You create a link, send it to the buyer, and they pay through a hosted page.

For instance, a services exporter can send a payment link after delivering a project, and the buyer completes payment in their local currency. In a cross-channel setup, this transaction shows up in the same dashboard as your website sales.

3. Recurring payments

If you charge customers on a schedule, whether weekly, monthly, or yearly, recurring payments handle this automatically. The platform stores card details securely using tokenization and debits on the agreed dates.

For example, an edtech company billing parents monthly for online classes uses recurring payments so collections happen without manual follow-up each cycle.

4. Multi-currency accounts

These let your international buyers send funds to a local account in their own currency. For instance, a US client pays into your multi-currency account via bank transfer, and the funds settle to your Indian bank account. This channel is especially useful for freelancers and exporters who collect from marketplaces or B2B clients.

5. Mobile and in-app payments

If your business has a mobile app, this channel lets buyers pay inside the app using saved cards, wallets, or one-tap options like Apple Pay. The cross-channel benefit is that payment data from the app syncs with your web checkout, so a customer who saves a card in your app does not need to re-enter it on your website.

The value of cross-channel shows up when these channels share data. A customer's payment history, saved methods, and preferences carry across every touchpoint, giving you a complete picture and giving them a consistent experience.

Tip: Start with the two or three channels your business uses most. You can add more channels later without rebuilding your payment setup, as long as your platform supports them from the start.

How do cross-channel payment solutions work?

When all your channels run through one platform, every payment follows the same path from checkout to settlement. That consistency is what keeps approval rates high and reconciliation simple. Here’s how the process works:

1. Customer picks a channel: Your buyer pays on your website, clicks a payment link, or gets charged through a recurring billing setup.

2. Payment method is selected: The platform shows locally relevant options like international cards, Apple Pay, bank transfers, or alternate payment methods based on the buyer's location.

3. Transaction is routed: The platform sends the payment through the best processing path to improve approval chances. For instance, enhanced messaging to the card issuer can reduce false declines on international cards.

4. Data syncs across channels: Payment details, customer preferences, and transaction history update across all connected channels in real time.

5. You see everything in one dashboard: Settlement status, compliance documents, and fund tracking are available from a single screen.

Tip: Look for platforms that offer smart routing and enhanced issuer messaging. These features directly affect how many of your international transactions get approved.

What happens when your payment channels are not connected?

Most businesses don't start with a cross-channel setup. They add payment tools one at a time as they grow, and each tool works on its own. That creates real problems once your transaction volume or customer base crosses a certain point.

Here’s what typically goes wrong when channels run separately:

1. Manual reconciliation eats up time

When your checkout, payment links, and multi-currency accounts live on separate platforms, someone on your team has to match transactions manually. For example, reconciling a month of Shopify orders against bank transfer collections and recurring charges in three separate dashboards takes hours that could go toward sales or support.

2. Inconsistent buyer experience

A customer who pays on your website gets one checkout flow, while someone paying through a link sees a completely different page. This creates confusion, especially for international buyers who expect a familiar and trusted payment experience every time.

3. Leaking revenue on international cards

Fragmented tools lack the intelligence to talk to global banks effectively. Without smart routing or enhanced issuer messaging, you face higher false declines on perfectly good transactions.

4. No single view of your payments

You check one dashboard for card payments, another for recurring charges, and a third for multi-currency collections. Finding a specific transaction or getting a full picture of your monthly revenue means pulling data from each tool and combining it yourself.

5. Scaling gets harder

Every time you add a new market, currency, or payment method, you either patch it into an existing tool or add yet another one. The more tools you stack, the more integration work and hidden costs your team handles.

These problems grow with your business. What feels manageable at 50 transactions a month becomes a serious bottleneck at 500 or 5,000. Connecting your channels early saves you from rebuilding your payment setup later.

Tip: If you are already spending more than a few hours a week on payment tracking, reconciliation, or fixing failed transactions across tools, that is a clear sign your channels need to be connected.

How to choose the right cross-channel payment solution?

The wrong cross-channel payment platform costs you more than a monthly fee. It costs you failed transactions, manual workarounds, and months of migration if you need to switch later.

Here are some of the key factors that will help you select the right solution for your needs:

1. Payment method coverage

Check that the platform supports the payment methods your global customers prefer. This means international credit and debit cards, region-specific wallets like Apple Pay, and local bank transfer options. For instance, if you sell to buyers in Europe, supporting SEPA transfers alongside cards gives you better reach.

2. Currency and country support

Your platform should accept payments in the currencies your customers use. For Indian businesses collecting from 10 or more countries, look for support across major currencies like USD, GBP, EUR, and CAD, plus the ability to accept payments from a wide range of countries.

3. Approval rate performance

Ask providers about their payment success rates, especially on international card transactions. Features like smart routing, enhanced issuer messaging, and built-in fraud screening directly impact how many payments go through on the first attempt.

4. Single dashboard and reporting

A true cross-channel platform gives you one place to view transactions, track settlements, download compliance documents, and manage refunds. If you still need to log into separate tools for each channel, the setup is not fully connected.

5. Integration options

Check how the platform connects to your existing website, app, or e-commerce store. Look for API documentation, plugin support for platforms like Shopify or WooCommerce, and no-code options if your team is not heavily technical.

6. Fraud and risk management

Cross-border transactions carry a higher fraud risk. Your platform should include built-in fraud screening that filters suspicious transactions without blocking genuine customers. The best systems use real-time data from device, location, and card signals to make smart decisions.

Tip: Ask for a test or demo before committing. The best way to evaluate a cross-channel platform is to see how the checkout, dashboard, and reporting actually work with your products and customers.

What is the future of cross-channel payments?

Cross-channel payment solutions that lead today are already building features that will change how businesses collect payments over the next few years. Here's what is shaping the future of cross-channel payments:

- AI-driven fraud prevention: Instead of fixed rules, AI models learn from every transaction to spot suspicious patterns in real time. This means fewer false declines on genuine payments and faster detection of new fraud tactics.

- Biometric authentication: Fingerprint and face recognition are becoming the default at checkout. Buyers complete payments faster, and businesses see fewer drop-offs at the authentication step.

- Embedded payments: Payment collection is moving inside the platforms buyers already use, like messaging apps, social media, and SaaS tools. The checkout becomes invisible because it happens inside the experience, not on a separate page.

- Smart payment routing: AI-powered routing picks the best processing path for each transaction based on card type, geography, and issuer behavior. This pushes approval rates higher without any manual setup from your team.

The providers investing in these features today will give you an advantage as payment behavior changes. When evaluating platforms, ask what is on their product roadmap, not just what they offer right now.

Handle global payments from one platform with PayGlocal

Managing payments across separate tools creates extra work and costs you for approved transactions. When your checkout, card processing, recurring billing, and multi-currency collection run on different systems, things slow down.

PayGlocal brings all of this together into one platform built for Indian businesses collecting payments globally. Here is what you get.

- Dynamic checkout: A unified checkout flow for your global customers to pay through international cards and local payment methods, with options that adjust based on buyer location.

- Global payment methods: 40+ local payment options, including Apple Pay, wallets, and bank transfers, so your buyers can pay the way they prefer.

- Recurring payments: Set up subscriptions, recurring billing, and standing instructions on international cards from one system.

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD, and globally in 33+ currencies from 180+ countries.

- One platform: Manage, track, and settle all your payments from a single dashboard with real-time status updates and auto-generated FIRC.

PayGlocal connects every payment channel your global business needs, with no fixed costs and no platform fees. You pay only when you transact. Plus, you also get all forms of options like API, no-code, and plugin-based integrations.

Final thoughts

Cross-channel payment solutions solve several problems for growing businesses, like too many disconnected payment tools, too much manual work, and too many lost transactions. The right platform connects your checkout, cards, recurring billing, and multi-currency collection into one system where everything works together.

Start by mapping out the payment channels your business uses today and where you see friction. Then evaluate platforms based on method coverage, approval rates, dashboard visibility, and how easily they fit your current setup.

Indian businesses selling globally are already moving to connected payment platforms. The longer you wait, the more approved transactions and repeat customers slip away. Get started with PayGlocal today and bring your cross-channel payments into one place.