Digital lending has become the foundation of modern financial services, processing loans faster than traditional banks ever could. From personal loans approved in minutes to business credit lines accessible 24/7, digital lending platforms are reshaping how money flows in the economy.

The Indian government has launched the Mutual Credit Guarantee Scheme, which offers 60% guarantee coverage to lending institutions for providing up to ₹100 crore credit facilities. This scheme helps small and medium businesses to access funding more easily.

Find out how digital lending works, what benefits it offers, and explore the latest trends in digital lending.

Digital lending refers to the process of providing loans through online platforms using automated systems, data analytics, and digital technologies. Unlike traditional lending that relies on physical paperwork and manual processes, digital lending handles everything electronically, from application submission to fund disbursement.

The core components include online application portals, automated financial risk assessment systems, digital document verification, and electronic payment processing.

For example, a small business owner can apply for a working capital loan through a mobile app, get approved within hours based on bank transaction data, and receive funds directly to their account.

Digital lending covers various loan types, including personal loans, business loans, peer-to-peer lending, and marketplace lending. The key differentiator is the end-to-end digital process that removes manual intervention while maintaining security and compliance standards.

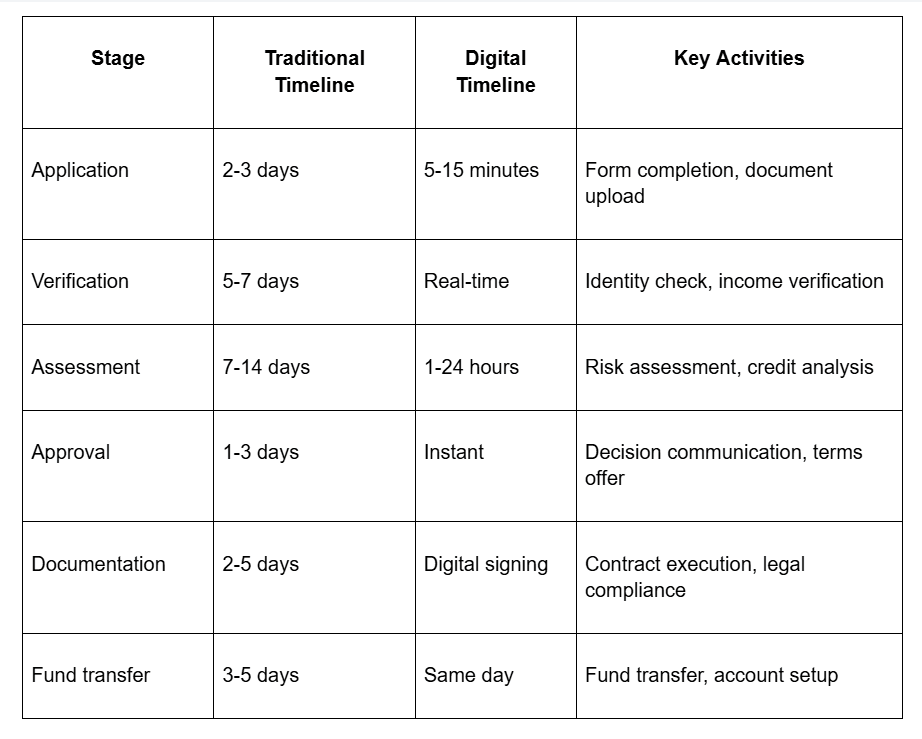

Digital lending follows a structured process that uses technology at every step to create efficient, secure loan origination and management. The digital lending process includes these key stages:

Let’s see how each of these stages works:

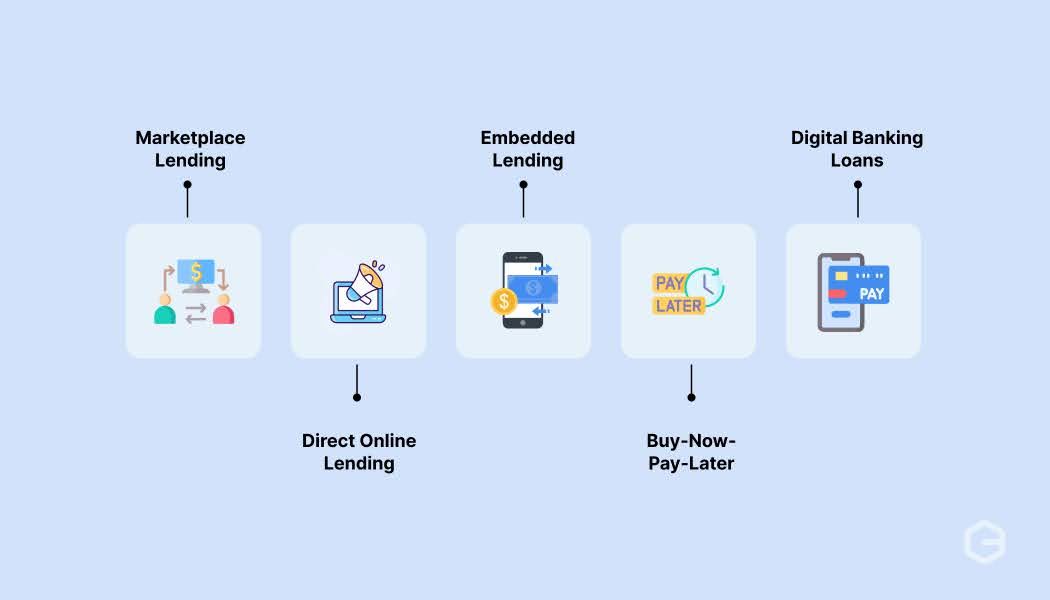

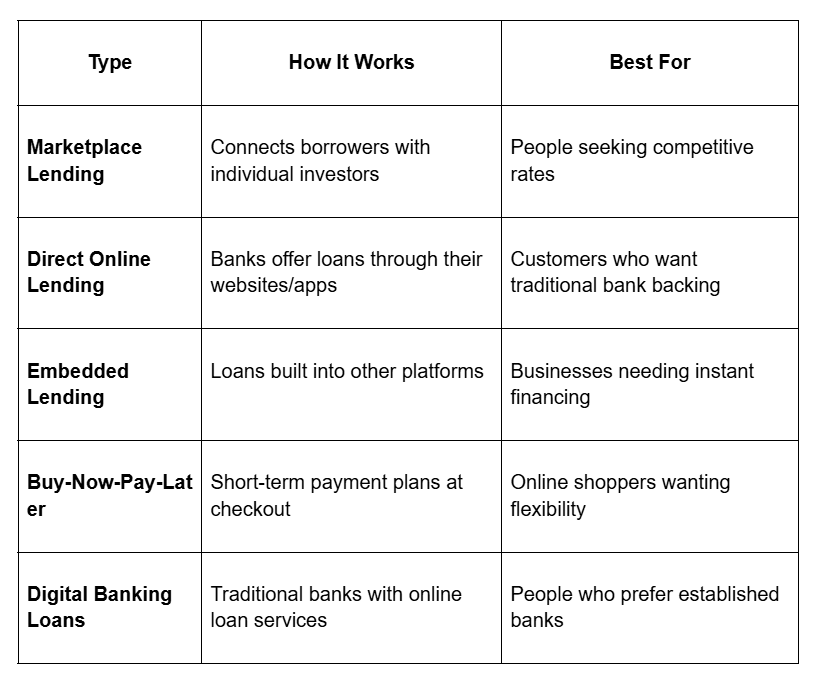

Digital lending comes in several different forms, each designed to serve specific customer needs and business models.

Different types of platforms work better for different situations, whether you're buying something online or running a business that needs quick funding.

Digital lending offers significant advantages over traditional lending methods, making it attractive for both lenders and borrowers. Here are the key benefits that make digital lending popular:

Speed and efficiency: Automated systems process applications in minutes rather than days. Risk assessment algorithms analyze hundreds of data points instantly, while digital verification removes waiting periods for document review.

Digital lending in India has grown rapidly, driven by government initiatives, smartphone adoption, and increasing demand for convenient credit access. The sector has attracted huge investments and is reshaping how Indians access credit.

In the last 5 financial years (from 2020-21 to 2024-25), total digital transactions in India grew by more than four times, reaching over 18,000 crores total digital payment transactions.

India's digital infrastructure, including Aadhaar, UPI, and Jan Dhan accounts, has created a digital identity and payment foundation that enables lending at scale. This infrastructure allows lenders to verify identity, check bank statements, and disburse funds instantly without traditional banking relationships.

Regulatory support has also been crucial for growth. Indian financial regulators have introduced several guidelines for digital lending platforms and banks to promote financial support and growth. For instance, banks have been guided to issue loan amounts to the MSE (Micro and Small Enterprise) sector for up to ₹25 lakhs within 14 working days.

The market now includes traditional banks with online platforms, new companies focusing on specific segments, and large technology companies offering lending products. This competition has improved product quality and reduced costs for borrowers across urban and rural areas.

Digital lending platforms rely on several key technologies to deliver fast, accurate, and secure lending services. These technologies work together to create the automated processes that make digital lending possible.

Modern digital lending platforms are built on these core technologies:

Digital lending keeps changing as new technologies appear and customer needs shift. Today's trends focus on making borrowing easier and reaching more people, while tomorrow's changes will bring even smarter lending options.

Some of the current market changes show several important patterns happening now:

The next wave of changes will reshape how people borrow money completely. These new developments will likely become normal within the next few years.

The differences between digital and traditional lending help businesses choose the right approach for their needs.

Digital lending offers several advantages compared to traditional lending methods:

Despite its advantages, digital lending faces several challenges that platforms must solve for sustainable success. Some of the key challenges include:

Digital lending platforms need payment infrastructure that matches their speed, scale, and global ambitions. Traditional payment systems often create challenges with slow settlements, limited currency support, and complex compliance requirements that hold back platform growth.

PayGlocal provides the payment foundation that digital lending platforms need to compete globally while maintaining local market compliance and customer experience standards.

Whether you're processing microloans for emerging markets or enterprise credit facilities, PayGlocal adapts to your lending model while providing the reliability and transparency that financial services demand.

Digital lending represents the future of financial services, offering speed, efficiency, and accessibility that traditional lending cannot match. The key to sustainable growth in digital lending comes from choosing the right technology partners who know the complexities of global financial services.

Payment processing, in particular, can make or break the customer experience and operational efficiency of digital lending platforms. PayGlocal provides the payment infrastructure to handle multi-currency transactions, regulatory compliance, and customer experience requirements that modern lending demands.

Ready to build a digital lending platform that scales globally? Get started with PayGlocal today.

The Indian government has launched the Mutual Credit Guarantee Scheme, which offers 60% guarantee coverage to lending institutions for providing up to ₹100 crore credit facilities. This scheme helps small and medium businesses to access funding more easily.

Find out how digital lending works, what benefits it offers, and explore the latest trends in digital lending.

Key Takeaways:

- Faster processing: Digital lending reduces loan approval times from weeks to minutes through AI-powered risk assessment.

- Better customer experience: Online applications, instant decisions, and digital documentation create seamless borrowing experiences that customers expect today.

- Data-driven decisions: Advanced analytics and machine learning enable more accurate risk assessment and personalized lending products.

- Enhanced payment solutions: Modern digital lending platforms require advanced payment infrastructure like PayGlocal to handle multi-currency transactions and global compliance seamlessly.

What is digital lending?

Digital lending refers to the process of providing loans through online platforms using automated systems, data analytics, and digital technologies. Unlike traditional lending that relies on physical paperwork and manual processes, digital lending handles everything electronically, from application submission to fund disbursement.

The core components include online application portals, automated financial risk assessment systems, digital document verification, and electronic payment processing.

For example, a small business owner can apply for a working capital loan through a mobile app, get approved within hours based on bank transaction data, and receive funds directly to their account.

Digital lending covers various loan types, including personal loans, business loans, peer-to-peer lending, and marketplace lending. The key differentiator is the end-to-end digital process that removes manual intervention while maintaining security and compliance standards.

How does digital lending work?

Digital lending follows a structured process that uses technology at every step to create efficient, secure loan origination and management. The digital lending process includes these key stages:

Let’s see how each of these stages works:

- Application submission: Borrowers complete online forms providing personal, financial, and business information. Advanced platforms use pre-filled data and API integrations to minimize manual entry and reduce errors.

- Automated risk assessment: Algorithms analyze applicant data against predefined criteria using credit scores, income verification, bank statements, and alternative data sources. Machine learning models continuously refine approval criteria based on historical performance.

- Digital verification: Identity verification uses document scanning, biometric authentication, and database cross-checks. Income and employment verification happens through direct API connections to payroll systems and bank accounts.

- Risk assessment: Advanced scoring models evaluate creditworthiness using traditional and non-traditional data points. This includes transaction patterns, cash flow analysis, and behavioral indicators that provide comprehensive risk profiles.

- Approval and terms: Approved applications receive loan offers with specific terms, interest rates, and repayment schedules. Borrowers can review and accept terms digitally without physical signatures or paperwork.

- Fund transfer: Approved loans are sent electronically to borrower accounts, often within hours of approval. This requires a payment infrastructure to handle various currencies and banking systems securely.

What are the types of digital lending?

Digital lending comes in several different forms, each designed to serve specific customer needs and business models.

Different types of platforms work better for different situations, whether you're buying something online or running a business that needs quick funding.

What are the benefits of digital lending?

Digital lending offers significant advantages over traditional lending methods, making it attractive for both lenders and borrowers. Here are the key benefits that make digital lending popular:

- Speed and efficiency: Digital lending offers significant advantages over traditional lending methods, making it attractive for both lenders and borrowers. Here are the key benefits that make digital lending popular:

Speed and efficiency: Automated systems process applications in minutes rather than days. Risk assessment algorithms analyze hundreds of data points instantly, while digital verification removes waiting periods for document review.

- 24/7 accessibility: Borrowers can apply anytime from anywhere using mobile devices or computers. This convenience particularly benefits small businesses and individuals who cannot visit bank branches during business hours.

- Lower operational costs: Automation reduces the need for manual processing, physical infrastructure, and extensive paperwork. These savings often translate to competitive interest rates and fees for borrowers.

- Better risk management: Advanced analytics and machine learning models analyze alternative data sources like social media, transaction history, and behavioral patterns. This comprehensive view enables more accurate risk assessment than traditional credit scoring alone.

- Improved customer experience: Simple applications, real-time status updates, and digital communication create positive borrowing experiences. Customers appreciate transparency and control over their loan journey.

- Scalability: Digital platforms can handle thousands of applications simultaneously without proportional increases in staff or infrastructure. This scalability enables rapid business growth and market expansion.

How is digital lending changing in India?

Digital lending in India has grown rapidly, driven by government initiatives, smartphone adoption, and increasing demand for convenient credit access. The sector has attracted huge investments and is reshaping how Indians access credit.

In the last 5 financial years (from 2020-21 to 2024-25), total digital transactions in India grew by more than four times, reaching over 18,000 crores total digital payment transactions.

India's digital infrastructure, including Aadhaar, UPI, and Jan Dhan accounts, has created a digital identity and payment foundation that enables lending at scale. This infrastructure allows lenders to verify identity, check bank statements, and disburse funds instantly without traditional banking relationships.

Regulatory support has also been crucial for growth. Indian financial regulators have introduced several guidelines for digital lending platforms and banks to promote financial support and growth. For instance, banks have been guided to issue loan amounts to the MSE (Micro and Small Enterprise) sector for up to ₹25 lakhs within 14 working days.

The market now includes traditional banks with online platforms, new companies focusing on specific segments, and large technology companies offering lending products. This competition has improved product quality and reduced costs for borrowers across urban and rural areas.

What technologies are used in digital lending?

Digital lending platforms rely on several key technologies to deliver fast, accurate, and secure lending services. These technologies work together to create the automated processes that make digital lending possible.

Modern digital lending platforms are built on these core technologies:

- Artificial Intelligence and Machine Learning: AI algorithms analyze borrower data, predict default risk, and automate approval decisions. ML models continuously learn from new data to improve accuracy over time.

- Application Programming Interfaces (APIs): APIs connect lending platforms with banks, credit bureaus, payment systems, and other financial services. These connections enable real-time data sharing and automated processes.

- Cloud Computing: Cloud infrastructure provides the scalability and reliability needed to handle varying loan volumes. Cloud services also offer advanced analytics and security features at lower costs than traditional IT infrastructure.

- Mobile Technology: Mobile apps make lending accessible to smartphone users, while mobile wallets enable instant fund transfers. Mobile technology is particularly important in emerging markets with limited banking infrastructure.

- Robotic Process Automation (RPA): RPA tools automate repetitive tasks like document processing, compliance checks, and report generation. This reduces processing time and human error while cutting operational costs.

What are the current and future trends in digital lending?

Digital lending keeps changing as new technologies appear and customer needs shift. Today's trends focus on making borrowing easier and reaching more people, while tomorrow's changes will bring even smarter lending options.

Current trends in digital lending

Some of the current market changes show several important patterns happening now:

- Embedded finance: Loan options are being built directly into shopping websites and business software. This means people can get loans exactly when they need them, like when buying equipment for their business.

- Open banking APIs: Banks and lenders can now share customer data safely and quickly. This makes it faster to check someone's income and financial history when they apply for a loan.

- Buy now, pay later growth: More shoppers are using short-term payment plans when buying things online. Merchants like this because it helps them sell more, and customers like the flexibility.

- Instant lending: Many platforms now approve loans in just seconds or minutes. They use computer programs that can look at your past financial data and make quick decisions about whether to lend you money.

- Industry-specific solutions: Lenders are creating special loan products for different types of businesses like hospitals, schools, and farms. Each industry gets loan terms that match how their business works.

Future trends in digital lending

The next wave of changes will reshape how people borrow money completely. These new developments will likely become normal within the next few years.

- Smart personalization: Computer programs will get much better at creating loan offers that fit exactly what each person needs. They'll look at how you behave and what you can afford to give you the best terms.

- Connected device integration: Smart devices in homes and businesses will share information about how things are being used. This will help lenders make better decisions about loans for equipment and property.

- Better automation: Computer systems will handle more complex loan decisions without needing people to review them. This will make loans even faster and cheaper.

- Advanced computing: New computer technologies will make it possible to spot fraud better and assess risks more accurately than ever before.

- New lending models: Different ways of lending money will develop that don't need traditional banks. This could make loans cheaper and more available to everyone.

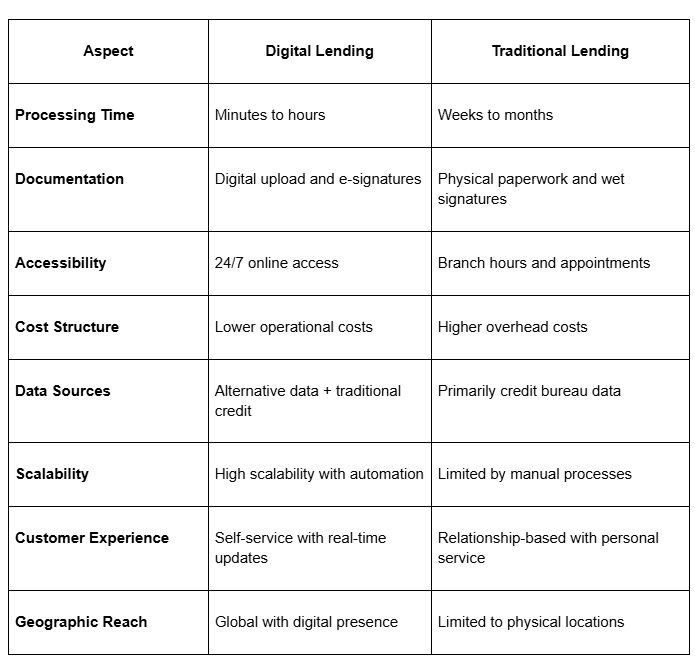

How does digital lending compare to traditional lending?

The differences between digital and traditional lending help businesses choose the right approach for their needs.

Digital lending offers several advantages compared to traditional lending methods:

- Speed advantage: Digital lending's automated processes remove waiting periods associated with manual review and physical document handling. Borrowers receive decisions faster, improving satisfaction and reducing dropout rates.

- Cost efficiency: Reduced infrastructure and automation lead to lower costs per loan. These savings benefit both lenders through improved margins and borrowers through competitive rates.

- Data utilization: Digital platforms leverage alternative data sources like transaction history, social media, and behavioral patterns. This comprehensive approach enables lending to previously underserved segments.

- Customer control: Borrowers manage applications independently, tracking progress and receiving updates through digital dashboards. This transparency builds trust and reduces support requirements.

What are the challenges of digital lending?

Despite its advantages, digital lending faces several challenges that platforms must solve for sustainable success. Some of the key challenges include:

- Regulatory compliance: Financial services face strict regulations that vary by jurisdiction. Digital platforms must ensure compliance with lending laws, data protection requirements, and consumer protection regulations across all markets they serve.

- Cybersecurity risks: Digital platforms handle sensitive financial data, making them attractive targets for cybercriminals. Strong security measures, encryption, and fraud detection systems are essential for maintaining customer trust and regulatory compliance.

- Risk assessment accuracy: While digital platforms can process more data, ensuring accurate risk models requires continuous refinement. False positives lead to lost business, while false negatives result in loan defaults and financial losses.

- Technology infrastructure: Reliable, scalable systems are crucial for handling high transaction volumes and maintaining uptime. Platform failures during peak periods can damage reputation and lose customers to competitors.

- Customer education: Many borrowers are unfamiliar with digital lending processes and may prefer traditional banking relationships. Platforms must invest in education and support to build confidence in digital-first approaches.

- Integration complexity: Digital lending platforms often require integration with multiple systems, including payment processors, credit bureaus, banking networks, and regulatory reporting systems. Managing these connections adds technical complexity and operational risk.

Power your digital lending platform with PayGlocal

Digital lending platforms need payment infrastructure that matches their speed, scale, and global ambitions. Traditional payment systems often create challenges with slow settlements, limited currency support, and complex compliance requirements that hold back platform growth.

PayGlocal provides the payment foundation that digital lending platforms need to compete globally while maintaining local market compliance and customer experience standards.

- Multi-currency account management: Accept loan payments and disburse funds in 33+ currencies across 180+ countries, enabling global lending operations without currency conversion delays or excessive fees.

- Instant settlement capabilities: Process loan disbursements and repayments with same-day settlement, improving cash flow management and customer satisfaction through faster fund availability.

- Automated compliance documentation: Generate FIRC and regulatory reports automatically, reducing compliance overhead and ensuring lending platforms meet international banking requirements effortlessly.

- Real-time payment tracking: Provide borrowers and lenders with transparent payment status updates throughout the loan lifecycle, building trust and reducing support requirements.

- Zero setup costs with pay-per-transaction: Scale payment processing costs with business growth, removing fixed infrastructure costs that burden early-stage platforms.

Whether you're processing microloans for emerging markets or enterprise credit facilities, PayGlocal adapts to your lending model while providing the reliability and transparency that financial services demand.

Final thoughts

Digital lending represents the future of financial services, offering speed, efficiency, and accessibility that traditional lending cannot match. The key to sustainable growth in digital lending comes from choosing the right technology partners who know the complexities of global financial services.

Payment processing, in particular, can make or break the customer experience and operational efficiency of digital lending platforms. PayGlocal provides the payment infrastructure to handle multi-currency transactions, regulatory compliance, and customer experience requirements that modern lending demands.

Ready to build a digital lending platform that scales globally? Get started with PayGlocal today.