Are you set up to accept payments the way your customers actually want to pay?

Recent data shows that over 40% of India's payments now happen through digital channels. Customers use UPI, cards, wallets, and net banking regularly. If your store doesn't support their preferred method, they'll leave without buying.

Your customers expect smooth, secure checkouts. One failed payment or missing payment method can mean a lost sale. For businesses selling globally, requirements increase further with multi-currency payments and global payment options.

In this guide, we break down all the requirements you need to follow to accept digital payments in e-commerce. Find out what merchants need, what customers need, and how to choose solutions that actually work for your business.

Digital payment requirements in e-commerce are the technical, regulatory, and infrastructure components you need to accept and process payments online. These requirements cover both what you, as a merchant, must have in place and what your customers need to complete transactions.

For merchants, this includes payment processing infrastructure like gateways and merchant accounts, security compliance measures, technical integration capabilities, and the ability to support various payment methods. For customers, it means having online banking access, internet connectivity, and the credentials needed for their chosen payment method.

For instance, an Indian D2C brand selling skincare products needs a payment gateway integrated into their Shopify store, PCI-DSS compliance to handle card data securely, a merchant account to receive settlements, and support for credit cards, UPI, and digital wallets.

Their customers need online banking, a stable internet connection, and valid payment credentials. When all these pieces work together, transactions happen smoothly.

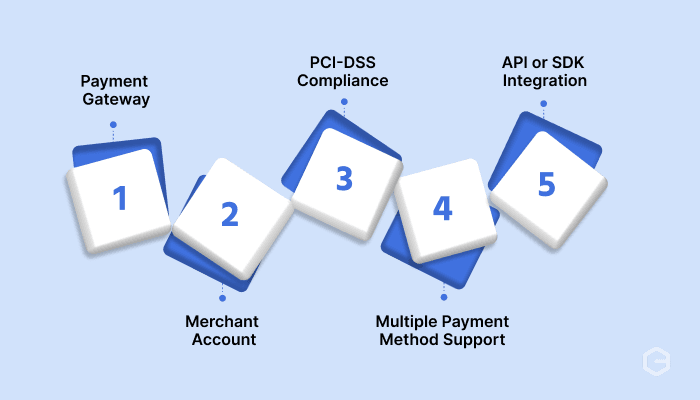

Setting up digital payments as a merchant involves the following five core requirements. Each plays a specific role in enabling secure, reliable payment acceptance.

Payment gateway

A payment gateway is the service that processes transactions between your website and the customer's bank. It encrypts payment data, communicates with card networks, and returns approval or decline messages.

For example, when a customer enters card details on your checkout page, the payment gateway securely transmits that data to the bank for authorization. You need a gateway that integrates with your e-commerce platform and supports your target payment methods.

Merchant account

A merchant account is a special business bank account that holds funds from customer transactions before they're settled into your regular business account.

Payment providers require this to manage transaction flows and handle chargebacks or disputes. Some payment providers include merchant account services in their offering, simplifying setup.

PCI-DSS compliance

Payment Card Industry Data Security Standard (PCI-DSS) compliance is mandatory when handling card payments.

This means implementing security measures to protect cardholder data, including encryption, secure networks, regular security testing, and restricted access to sensitive information. Non-compliance can result in fines and loss of payment processing privileges.

Multiple payment method support

Your system must handle various payment options that your customers prefer. In India, this includes credit and debit cards (Visa, Mastercard, RuPay, Amex), UPI (Unified Payments Interface), digital wallets like Google Pay and Paytm, and net banking.

For international customers, you need to support global cards and region-specific payment methods, such as iDEAL for the Netherlands.

API or SDK integration

You need technical capability to integrate the payment gateway into your e-commerce platform. Most gateways provide APIs (Application Programming Interfaces) or SDKs (Software Development Kits) that your development team uses to connect payment processing to your website or app. The integration handles transaction requests, payment confirmations, and status updates.

Your customers also need specific requirements in place to complete digital payments. Making these requirements clear helps reduce payment failures and cart abandonment.

Bank account with online access

Customers need an active bank account with online banking or mobile banking enabled. This allows them to authorize net banking payments, link accounts to UPI apps, or load digital wallets. Most Indian banks now offer instant online banking activation.

Digital wallet setup

For wallet payments, customers need to download wallet apps like Google Pay, PhonePe, or Paytm, complete KYC (Know Your Customer) verification, and link their bank account or cards. Wallets store payment credentials securely, enabling quick one-tap payments.

Net banking credentials

Customers choosing net banking need their bank-issued user ID and password or PIN. They use these credentials to log into their bank's portal during checkout and authorize the payment directly from their account.

Valid payment cards

For card payments, customers need active credit or debit cards with a sufficient balance or credit limit. Cards must be enabled for online transactions, which some banks disable by default for security. Customers can activate online transactions through their bank's app or net banking.

Internet connectivity

A stable internet connection is essential for initiating and completing transactions. Poor connectivity can cause payment timeouts or failures, leading to frustrated customers and abandoned carts.

Two-factor authentication credentials

Most transactions require two-factor authentication (2FA) for security. This might be an OTP (One-Time Password) sent via SMS, authentication through the customer's UPI app, or card-linked OTP verification. Customers need access to their registered mobile number or authentication app.

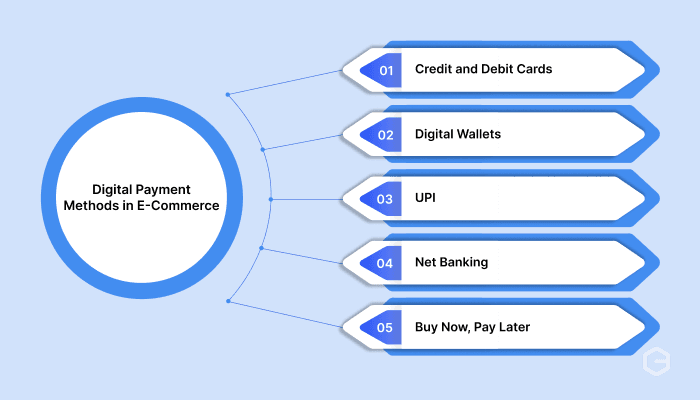

Supporting diverse payment methods improves conversion rates by matching customer preferences. Different demographics and regions favor different payment options. Here are the main payment methods you should consider:

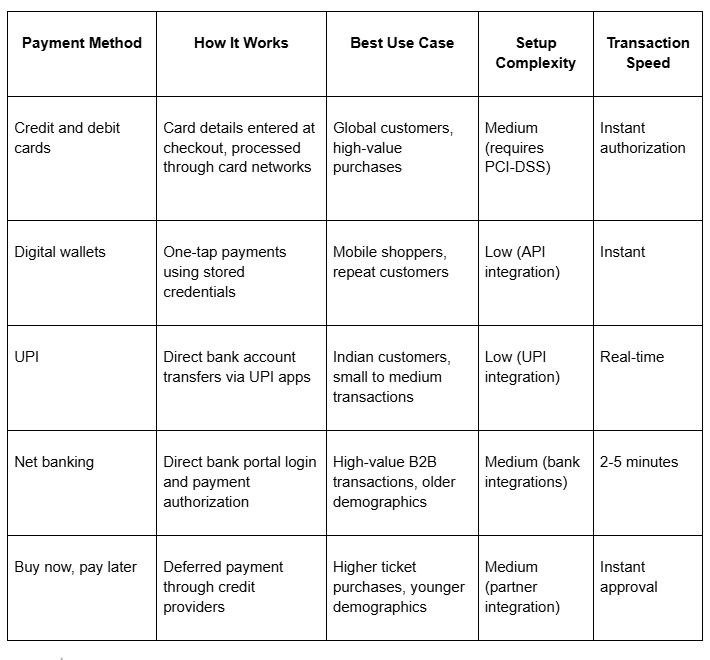

Credit and debit cards

Card payments remain the most common method globally. Customers enter their card details, and the payment gateway processes the payment via Visa, Mastercard, RuPay, or Amex networks. Cards work internationally, making them essential for cross-border sales.

For example, an Indian exporter selling handicrafts to US customers needs strong international card processing to accept Visa and Mastercard payments in USD.

Digital wallets

Digital wallets like Google Pay, PhonePe, Apple Pay, and PayPal securely store payment credentials. Customers authenticate with a PIN or biometric, and the wallet handles the payment processing. Wallets reduce checkout friction significantly.

For instance, a customer buying groceries online can complete payment in seconds with Google Pay instead of entering card details.

UPI payments

UPI has become India's dominant payment method for transactions under ₹10,000. Customers use UPI apps to transfer money directly from their bank account to yours using a UPI ID or QR code. UPI payments are instant, free for customers, and have very low merchant fees.

For instance, a small clothing store selling products between ₹500 to ₹5,000 finds UPI perfect for their customer base. Customers simply scan a QR code at checkout, approve the payment in their UPI app, and the transaction completes in seconds.

Net banking

Net banking redirects customers to their bank's secure portal, where they log in and authorize payment directly. This method works well for higher-value transactions and B2B purchases where customers prefer direct bank transfers.

For example, a corporate buyer purchasing office furniture for ₹2 lakhs might choose net banking over cards for security and record-keeping.

Buy now, pay later

BNPL services like Simpl, LazyPay, or ZestMoney let customers split payments into installments. This increases average order values and conversion rates for expensive products.

For instance, a customer buying a laptop for ₹60,000 might use BNPL to pay in three interest-free installments, making the purchase more accessible.

Choosing a payment solution impacts your conversion rates, costs, and customer experience. The wrong choice can mean lost sales, high fees, or technical limitations. Consider these factors when evaluating payment providers:

Setting up digital payments for e-commerce involves multiple moving parts. You need the right infrastructure, security compliance, diverse payment methods, and reliable processing. For businesses selling internationally, these requirements multiply with multi-currency needs, cross-border regulations, and global payment methods.

PayGlocal simplifies international payment acceptance for Indian businesses. Whether you're a freelancer receiving payments from overseas clients, a D2C brand expanding globally, or a service exporter managing invoices, PayGlocal provides everything you need in one platform.

Here's how PayGlocal helps you meet all digital payment requirements:

PayGlocal helps you collect globally and settle locally with unmatched reliability. Whether you're processing just a few transactions monthly or scaling to high volume, our platform grows with your business.

Digital payment requirements in e-commerce cover technical infrastructure, security compliance, diverse payment methods, and reliable processing systems. Getting these requirements right directly impacts your conversion rates and revenue.

For businesses expanding internationally, requirements include multi-currency support, global payment methods, and global compliance. Modern payment platforms like PayGlocal handle the complexity so that you can focus on growing your business.

Ready to simplify international payment acceptance? Get started with PayGlocal today and start converting more international customers.

Recent data shows that over 40% of India's payments now happen through digital channels. Customers use UPI, cards, wallets, and net banking regularly. If your store doesn't support their preferred method, they'll leave without buying.

Your customers expect smooth, secure checkouts. One failed payment or missing payment method can mean a lost sale. For businesses selling globally, requirements increase further with multi-currency payments and global payment options.

In this guide, we break down all the requirements you need to follow to accept digital payments in e-commerce. Find out what merchants need, what customers need, and how to choose solutions that actually work for your business.

Key takeaways

- Merchant requirements: You need a payment gateway, merchant account, PCI-DSS compliance, and API integration capabilities to accept digital payments online.

- Customer requirements: Your customers need bank accounts with online access, internet connectivity, and optionally digital wallets or net banking credentials to complete transactions.

- Payment method diversity: Supporting multiple payment options, including cards, digital wallets, UPI, and net banking, increases conversion rates and customer trust.

- Technical infrastructure: Your e-commerce platform needs proper API/SDK integration to connect payment gateways and process transactions securely.

- Global payments: PayGlocal offers a complete payment stack with high success rates, multi-currency accounts, global payment methods, and built-in compliance for businesses selling internationally.

What are the digital payment requirements in e-commerce?

Digital payment requirements in e-commerce are the technical, regulatory, and infrastructure components you need to accept and process payments online. These requirements cover both what you, as a merchant, must have in place and what your customers need to complete transactions.

For merchants, this includes payment processing infrastructure like gateways and merchant accounts, security compliance measures, technical integration capabilities, and the ability to support various payment methods. For customers, it means having online banking access, internet connectivity, and the credentials needed for their chosen payment method.

For instance, an Indian D2C brand selling skincare products needs a payment gateway integrated into their Shopify store, PCI-DSS compliance to handle card data securely, a merchant account to receive settlements, and support for credit cards, UPI, and digital wallets.

Their customers need online banking, a stable internet connection, and valid payment credentials. When all these pieces work together, transactions happen smoothly.

What are the digital payment requirements for merchants?

Setting up digital payments as a merchant involves the following five core requirements. Each plays a specific role in enabling secure, reliable payment acceptance.

Payment gateway

A payment gateway is the service that processes transactions between your website and the customer's bank. It encrypts payment data, communicates with card networks, and returns approval or decline messages.

For example, when a customer enters card details on your checkout page, the payment gateway securely transmits that data to the bank for authorization. You need a gateway that integrates with your e-commerce platform and supports your target payment methods.

Merchant account

A merchant account is a special business bank account that holds funds from customer transactions before they're settled into your regular business account.

Payment providers require this to manage transaction flows and handle chargebacks or disputes. Some payment providers include merchant account services in their offering, simplifying setup.

PCI-DSS compliance

Payment Card Industry Data Security Standard (PCI-DSS) compliance is mandatory when handling card payments.

This means implementing security measures to protect cardholder data, including encryption, secure networks, regular security testing, and restricted access to sensitive information. Non-compliance can result in fines and loss of payment processing privileges.

Multiple payment method support

Your system must handle various payment options that your customers prefer. In India, this includes credit and debit cards (Visa, Mastercard, RuPay, Amex), UPI (Unified Payments Interface), digital wallets like Google Pay and Paytm, and net banking.

For international customers, you need to support global cards and region-specific payment methods, such as iDEAL for the Netherlands.

API or SDK integration

You need technical capability to integrate the payment gateway into your e-commerce platform. Most gateways provide APIs (Application Programming Interfaces) or SDKs (Software Development Kits) that your development team uses to connect payment processing to your website or app. The integration handles transaction requests, payment confirmations, and status updates.

What are the digital payment requirements for customers?

Your customers also need specific requirements in place to complete digital payments. Making these requirements clear helps reduce payment failures and cart abandonment.

Bank account with online access

Customers need an active bank account with online banking or mobile banking enabled. This allows them to authorize net banking payments, link accounts to UPI apps, or load digital wallets. Most Indian banks now offer instant online banking activation.

Digital wallet setup

For wallet payments, customers need to download wallet apps like Google Pay, PhonePe, or Paytm, complete KYC (Know Your Customer) verification, and link their bank account or cards. Wallets store payment credentials securely, enabling quick one-tap payments.

Net banking credentials

Customers choosing net banking need their bank-issued user ID and password or PIN. They use these credentials to log into their bank's portal during checkout and authorize the payment directly from their account.

Valid payment cards

For card payments, customers need active credit or debit cards with a sufficient balance or credit limit. Cards must be enabled for online transactions, which some banks disable by default for security. Customers can activate online transactions through their bank's app or net banking.

Internet connectivity

A stable internet connection is essential for initiating and completing transactions. Poor connectivity can cause payment timeouts or failures, leading to frustrated customers and abandoned carts.

Two-factor authentication credentials

Most transactions require two-factor authentication (2FA) for security. This might be an OTP (One-Time Password) sent via SMS, authentication through the customer's UPI app, or card-linked OTP verification. Customers need access to their registered mobile number or authentication app.

What are the different types of digital payment methods in e-commerce?

Supporting diverse payment methods improves conversion rates by matching customer preferences. Different demographics and regions favor different payment options. Here are the main payment methods you should consider:

Credit and debit cards

Card payments remain the most common method globally. Customers enter their card details, and the payment gateway processes the payment via Visa, Mastercard, RuPay, or Amex networks. Cards work internationally, making them essential for cross-border sales.

For example, an Indian exporter selling handicrafts to US customers needs strong international card processing to accept Visa and Mastercard payments in USD.

Digital wallets

Digital wallets like Google Pay, PhonePe, Apple Pay, and PayPal securely store payment credentials. Customers authenticate with a PIN or biometric, and the wallet handles the payment processing. Wallets reduce checkout friction significantly.

For instance, a customer buying groceries online can complete payment in seconds with Google Pay instead of entering card details.

UPI payments

UPI has become India's dominant payment method for transactions under ₹10,000. Customers use UPI apps to transfer money directly from their bank account to yours using a UPI ID or QR code. UPI payments are instant, free for customers, and have very low merchant fees.

For instance, a small clothing store selling products between ₹500 to ₹5,000 finds UPI perfect for their customer base. Customers simply scan a QR code at checkout, approve the payment in their UPI app, and the transaction completes in seconds.

Net banking

Net banking redirects customers to their bank's secure portal, where they log in and authorize payment directly. This method works well for higher-value transactions and B2B purchases where customers prefer direct bank transfers.

For example, a corporate buyer purchasing office furniture for ₹2 lakhs might choose net banking over cards for security and record-keeping.

Buy now, pay later

BNPL services like Simpl, LazyPay, or ZestMoney let customers split payments into installments. This increases average order values and conversion rates for expensive products.

For instance, a customer buying a laptop for ₹60,000 might use BNPL to pay in three interest-free installments, making the purchase more accessible.

How do you choose the right payment solution for your e-commerce business?

Choosing a payment solution impacts your conversion rates, costs, and customer experience. The wrong choice can mean lost sales, high fees, or technical limitations. Consider these factors when evaluating payment providers:

- Payment success rates: Look for providers with high authorization rates, especially for international transactions. Low success rates mean more declined payments and lost revenue.

- Payment method coverage: Your provider should support all payment methods your customers prefer. For domestic sales, this means cards, UPI, wallets, and net banking. For international sales, you need global cards and local payment methods for your target markets.

- Pricing structure: Compare transaction fees, setup costs, monthly charges, and currency conversion fees. Some providers charge a flat percentage per transaction, while others have tiered pricing based on volume. Transparent pricing prevents surprise costs.

- Settlement speed: Faster settlements improve cash flow. Some providers settle funds within 24-48 hours, others take 7-10 days. For businesses with tight cash flow, quick settlements matter significantly.

- Integration ease: Evaluate how easily the solution integrates with your e-commerce platform. Providers offering pre-built plugins and integrations for Shopify, WooCommerce, Magento, or custom platforms reduce development time.

- Multi-currency support: If you're selling internationally, you need multi-currency processing. This lets customers pay in their local currency while you receive settlements in INR. It improves conversion rates because customers trust pricing in familiar currencies.

- Fraud protection: Strong fraud detection reduces chargebacks and protects your business. Look for providers with machine learning-based fraud systems, customizable risk rules, and real-time transaction monitoring.

- Customer support: Reliable technical support helps resolve payment issues quickly. Check if the provider offers 24/7 support, dedicated account managers, and fast response times. Payment failures during peak sales periods need immediate resolution.

- Scalability: Your payment solution should scale with business growth. It must handle increased transaction volumes, support expansion into new markets, and accommodate changing payment method preferences without platform migration.

Start accepting global payments with better speed and security

Setting up digital payments for e-commerce involves multiple moving parts. You need the right infrastructure, security compliance, diverse payment methods, and reliable processing. For businesses selling internationally, these requirements multiply with multi-currency needs, cross-border regulations, and global payment methods.

PayGlocal simplifies international payment acceptance for Indian businesses. Whether you're a freelancer receiving payments from overseas clients, a D2C brand expanding globally, or a service exporter managing invoices, PayGlocal provides everything you need in one platform.

Here's how PayGlocal helps you meet all digital payment requirements:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries. Get local accounts in USD, GBP, EUR, and CAD, letting international customers pay in their local currencies.

- Dynamic checkout: Provide a fast, secure, customizable checkout experience optimized for conversion. Our checkout supports multiple payment flows and seamlessly integrates with your e-commerce platform.

- Card payments with high success rates: Process international card payments with industry-leading success rates. Our payment orchestration engine optimizes routing and messaging to maximize approvals.

- Built-in compliance and fraud protection: We handle PCI-DSS compliance, fraud screening, and sanction checks automatically. Advanced risk management filters suspicious transactions while approving legitimate customers.

- Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) automatically in your inbox after settlement. Stay compliant without manual paperwork.

PayGlocal helps you collect globally and settle locally with unmatched reliability. Whether you're processing just a few transactions monthly or scaling to high volume, our platform grows with your business.

Final thoughts

Digital payment requirements in e-commerce cover technical infrastructure, security compliance, diverse payment methods, and reliable processing systems. Getting these requirements right directly impacts your conversion rates and revenue.

For businesses expanding internationally, requirements include multi-currency support, global payment methods, and global compliance. Modern payment platforms like PayGlocal handle the complexity so that you can focus on growing your business.

Ready to simplify international payment acceptance? Get started with PayGlocal today and start converting more international customers.