In India, 40% of all transactions occur digitally. In fact, 85% of all the digital transactions are UPI-based. Digital payments have changed how you handle money. What used to take bank visits and paperwork now happens in seconds on your phone. pib.gov

Digital wallets let you store money electronically, pay bills instantly, transfer funds to anyone, and track every transaction from one place. For businesses collecting payments from customers or managing expenses, wallets offer speed and convenience that traditional methods can't match.

In this guide, we cover everything you need to know about digital wallets in India. You'll learn what they are, how different types work, what benefits they offer, and how to choose the right solution for your needs. Let's get started.

A digital wallet is a software application that stores your payment information electronically and lets you make transactions without physical cash or cards. You link your bank account or card to the wallet app, add money, and then use it to pay for purchases, transfer funds, or collect payments from customers.

Digital wallets work through mobile apps that connect to your existing financial accounts. When you make a payment, the wallet securely transmits your payment details to complete the transaction.

For example, when you scan a QR code to accept payment from a customer or send money to a supplier, your wallet app processes the transaction in seconds. The money moves instantly, and you get a confirmation right away. This speed helps businesses manage cash flow better than waiting for bank transfers or checks to clear.

Digital wallets in India fall into three main categories based on how they work and where you can use them. Each type serves different purposes and comes with specific features. Here's how they compare:

Let's look at each type in detail.

Open wallets offer the most flexibility and features. Banks and licensed financial institutions issue these wallets, which let you make payments, transfer money, and even withdraw cash from ATMs.

With an open wallet, you can pay at any merchant, send money to anyone, buy products online, and access banking services. These wallets connect directly to your bank account and work like a digital extension of your bank. For instance, YONO SBI is an open wallet that provides full banking integration.

The main advantage here is complete freedom. You're not limited to specific stores or platforms. Any transaction you could do with a bank account, you can do with an open wallet.

Semi-closed wallets are the most common type in India. Apps like Paytm, PhonePe, Amazon Pay, and MobiKwik fall into this category. These wallets let you pay at a wide network of merchants and service providers, but you can't withdraw the money as cash.

You can use semi-closed wallets to pay bills, collect payments from customers, send money to suppliers, and make merchant payments. The wallet works across thousands of merchants who accept that payment method. For example, you can use your Paytm balance at any store that displays a Paytm QR code.

These wallets often offer cashback, rewards, and business features like payment links. Many small businesses prefer semi-closed wallets because they're easy to set up and integrate with existing systems.

Closed wallets work only within a single company's platform. When you add money to your Flipkart wallet or Swiggy Money, you can only use that balance for purchases on that specific platform.

These wallets serve specific purposes. E-commerce sites use them to speed up checkout, process refunds instantly, and encourage repeat purchases. For instance, if you return a product on Amazon, the refund goes to your Amazon Pay balance, which you can then use for future purchases.

The limitation is that you can't use closed wallet funds anywhere else. But for frequent users of a particular platform, they offer convenience and faster transactions.

Choosing the right digital wallet depends on what you need it for. Some wallets work better for personal transactions, while others suit business operations or specific use cases.

Here are the top digital wallets available in India:

Let's look at each wallet in detail.

Paytm is one of India's most popular digital wallets. You can use it for mobile recharges, bill payments, online shopping, ticket bookings, and peer-to-peer transfers.

The wallet also offers a Paytm Postpaid feature for buy now, pay later purchases. It works across a wide merchant network, making it practical for daily transactions and accepting payments from local customers.

PhonePe focuses on UPI-based payments with a clean, simple interface. It facilitates instant bank transfers, bill splitting, and access to third-party services like travel and insurance.

The app has grown popular for its ease of use and quick transaction processing. It works well for both personal payments and small business collections with QR codes.

Google Pay (GPay) uses UPI for direct bank-to-bank transfers with a user-friendly design. It offers reward systems, scratch cards, and cashback incentives for transactions.

You can pay utility bills, send money to contacts, and accept merchant payments through QR codes. The interface integrates smoothly with other Google services for business users.

Amazon Pay works seamlessly within the Amazon ecosystem. You can also use it for general bill payments, recharges, and payments at select merchants outside Amazon.

The wallet often provides exclusive cashback and discounts for Amazon purchases. It's particularly useful if your business buys supplies or sells products on the Amazon platform.

MobiKwik offers digital wallet functions along with bill payment services and investment options in mutual funds. You can recharge phones, pay bills, and even buy insurance through the app.

The wallet provides a MobiKwik Zip feature for credit-based payments. It's suitable for users who want payment and investment options in one place for managing business finances.

Airtel Money is a bank and telecom-linked wallet that provides integrated financial services to Airtel customers. You can recharge, pay bills, transfer money, and access banking features.

The wallet works particularly well for Airtel users who want to manage telecom and payment needs together. It also offers a prepaid card option for business expenses.

Freecharge started as a recharge platform and expanded into a full digital wallet. It handles mobile recharges, bill payments, and merchant transactions with regular cashback offers.

The app has a simple interface focused on quick recharges and payments. It appeals to businesses looking for straightforward payment and recharge options for operational expenses.

JioMoney integrates with the Jio ecosystem, offering payments, recharges, and access to Jio services. You can pay bills, transfer money, and make merchant payments through the app.

The wallet works best for Jio users who want to manage payments within the Jio platform. It also supports payments on other platforms through UPI for broader business use.

YONO SBI (You Only Need One) is State Bank of India's comprehensive banking and payment app. It's an open wallet that provides full banking services including payments, transfers, account management, and loans.

You can withdraw cash, pay merchants, and access all SBI banking features through one app. It's ideal for SBI customers who want complete banking integration for their business operations.

PayZapp is HDFC Bank's digital wallet offering tap and pay functionality through NFC. It supports card payments, UPI transfers, bill payments, and merchant transactions.

The wallet works well for HDFC customers who want contactless payment options. It also offers rewards and cashback on various transactions for business spending.

Digital wallets offer several advantages over traditional payment methods. Here's what they offer:

The combination of speed, security, and tracking makes digital wallets practical for both personal use and business operations. But while consumer wallets work well for everyday transactions, businesses handling international payments need more specialized features.

Digital wallets connect your existing financial accounts to a mobile app that handles transactions. Here's how the process works:

Picking a digital wallet depends on how you'll use it. Different wallets serve different needs, and what works for personal use might not work for business operations. Here's what to consider:

The biggest question is whether a consumer wallet actually fits your business model. If you're exporting goods or services, accepting international payments, or managing complex payment workflows, you need a solution built for those specific challenges.

Consumer digital wallets work well for everyday transactions in India. But when you're running a business that serves international clients or handles cross-border payments, those wallets fall short.

You need tools that handle multiple currencies, provide instant compliance documents, offer transparent tracking across borders, and deliver high payment success rates. Standard wallets can't do this because they're built for local, consumer-focused transactions.

PayGlocal provides the payment infrastructure you need for global commerce:

PayGlocal handles the complexity of cross-border payments so you can focus on growing your business. While consumer wallets keep your personal spending organized, PayGlocal powers your international revenue with the reliability and features you need.

Digital wallets have made payments faster and more convenient across India. They work well for personal transactions, bill payments, and local commerce. The variety of options means you can find a wallet that fits your basic payment needs.

But business requirements differ from personal use, especially when you're dealing with international clients. Consumer wallets can't handle multi-currency complexity or the payment success rates you need for cross-border commerce.

If you're exporting products or services, the right payment infrastructure makes a significant difference. PayGlocal gives you the tools to collect globally and settle locally with transparent pricing and reliable processing.

Get started with PayGlocal today and start collecting payments globally.

Digital wallets let you store money electronically, pay bills instantly, transfer funds to anyone, and track every transaction from one place. For businesses collecting payments from customers or managing expenses, wallets offer speed and convenience that traditional methods can't match.

In this guide, we cover everything you need to know about digital wallets in India. You'll learn what they are, how different types work, what benefits they offer, and how to choose the right solution for your needs. Let's get started.

Key takeaways

- What digital wallets are: Software-based applications linked to bank accounts or cards that enable instant digital transactions without physical cash or cards.

- Three main wallet types: Open wallets offer full banking features, semi-closed wallets work across merchant networks, and closed wallets stay within single platforms.

- Speed and convenience: Complete transactions in seconds, skip bank visits, and access payment history instantly from your phone.

- Security features matter: Encryption, biometric authentication, and tokenization protect your financial data during every transaction.

- International payments need different tools: PayGlocal handles cross-border payments with local accounts in multiple currencies, instant compliance documents, and transparent tracking that consumer wallets don't offer.

What is a digital wallet in India?

A digital wallet is a software application that stores your payment information electronically and lets you make transactions without physical cash or cards. You link your bank account or card to the wallet app, add money, and then use it to pay for purchases, transfer funds, or collect payments from customers.

Digital wallets work through mobile apps that connect to your existing financial accounts. When you make a payment, the wallet securely transmits your payment details to complete the transaction.

For example, when you scan a QR code to accept payment from a customer or send money to a supplier, your wallet app processes the transaction in seconds. The money moves instantly, and you get a confirmation right away. This speed helps businesses manage cash flow better than waiting for bank transfers or checks to clear.

What are the types of digital wallets in India?

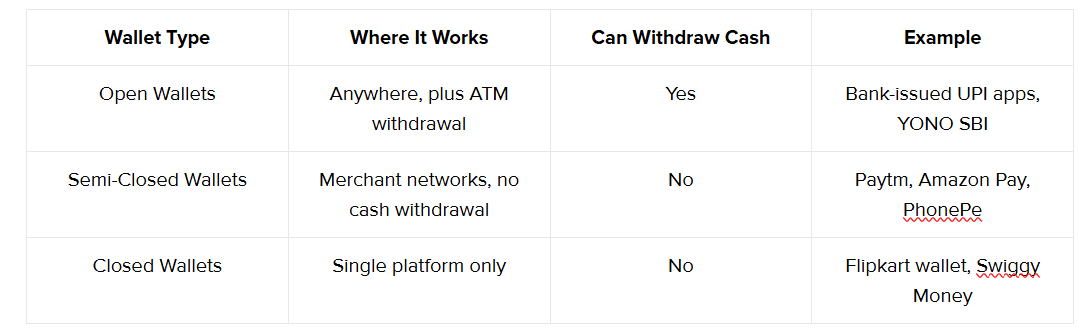

Digital wallets in India fall into three main categories based on how they work and where you can use them. Each type serves different purposes and comes with specific features. Here's how they compare:

Let's look at each type in detail.

Open wallets

Open wallets offer the most flexibility and features. Banks and licensed financial institutions issue these wallets, which let you make payments, transfer money, and even withdraw cash from ATMs.

With an open wallet, you can pay at any merchant, send money to anyone, buy products online, and access banking services. These wallets connect directly to your bank account and work like a digital extension of your bank. For instance, YONO SBI is an open wallet that provides full banking integration.

The main advantage here is complete freedom. You're not limited to specific stores or platforms. Any transaction you could do with a bank account, you can do with an open wallet.

Semi-closed wallets

Semi-closed wallets are the most common type in India. Apps like Paytm, PhonePe, Amazon Pay, and MobiKwik fall into this category. These wallets let you pay at a wide network of merchants and service providers, but you can't withdraw the money as cash.

You can use semi-closed wallets to pay bills, collect payments from customers, send money to suppliers, and make merchant payments. The wallet works across thousands of merchants who accept that payment method. For example, you can use your Paytm balance at any store that displays a Paytm QR code.

These wallets often offer cashback, rewards, and business features like payment links. Many small businesses prefer semi-closed wallets because they're easy to set up and integrate with existing systems.

Closed wallets

Closed wallets work only within a single company's platform. When you add money to your Flipkart wallet or Swiggy Money, you can only use that balance for purchases on that specific platform.

These wallets serve specific purposes. E-commerce sites use them to speed up checkout, process refunds instantly, and encourage repeat purchases. For instance, if you return a product on Amazon, the refund goes to your Amazon Pay balance, which you can then use for future purchases.

The limitation is that you can't use closed wallet funds anywhere else. But for frequent users of a particular platform, they offer convenience and faster transactions.

What are the best digital wallets in India?

Choosing the right digital wallet depends on what you need it for. Some wallets work better for personal transactions, while others suit business operations or specific use cases.

Here are the top digital wallets available in India:

Let's look at each wallet in detail.

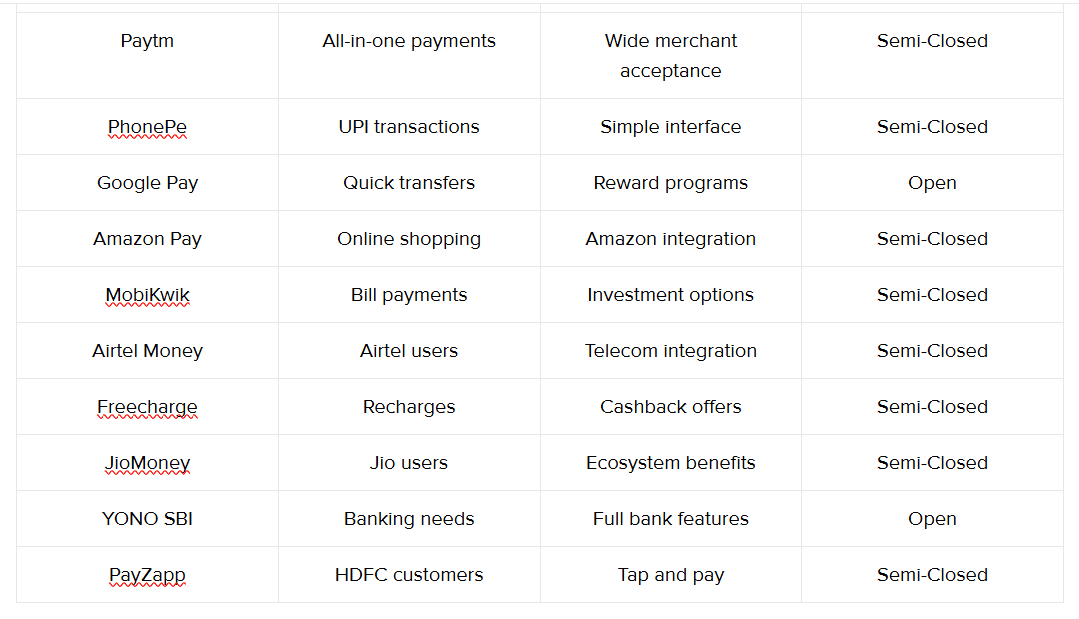

Paytm

Paytm is one of India's most popular digital wallets. You can use it for mobile recharges, bill payments, online shopping, ticket bookings, and peer-to-peer transfers.

The wallet also offers a Paytm Postpaid feature for buy now, pay later purchases. It works across a wide merchant network, making it practical for daily transactions and accepting payments from local customers.

PhonePe

PhonePe focuses on UPI-based payments with a clean, simple interface. It facilitates instant bank transfers, bill splitting, and access to third-party services like travel and insurance.

The app has grown popular for its ease of use and quick transaction processing. It works well for both personal payments and small business collections with QR codes.

Google Pay

Google Pay (GPay) uses UPI for direct bank-to-bank transfers with a user-friendly design. It offers reward systems, scratch cards, and cashback incentives for transactions.

You can pay utility bills, send money to contacts, and accept merchant payments through QR codes. The interface integrates smoothly with other Google services for business users.

Amazon Pay

Amazon Pay works seamlessly within the Amazon ecosystem. You can also use it for general bill payments, recharges, and payments at select merchants outside Amazon.

The wallet often provides exclusive cashback and discounts for Amazon purchases. It's particularly useful if your business buys supplies or sells products on the Amazon platform.

MobiKwik

MobiKwik offers digital wallet functions along with bill payment services and investment options in mutual funds. You can recharge phones, pay bills, and even buy insurance through the app.

The wallet provides a MobiKwik Zip feature for credit-based payments. It's suitable for users who want payment and investment options in one place for managing business finances.

Airtel Money

Airtel Money is a bank and telecom-linked wallet that provides integrated financial services to Airtel customers. You can recharge, pay bills, transfer money, and access banking features.

The wallet works particularly well for Airtel users who want to manage telecom and payment needs together. It also offers a prepaid card option for business expenses.

Freecharge

Freecharge started as a recharge platform and expanded into a full digital wallet. It handles mobile recharges, bill payments, and merchant transactions with regular cashback offers.

The app has a simple interface focused on quick recharges and payments. It appeals to businesses looking for straightforward payment and recharge options for operational expenses.

JioMoney

JioMoney integrates with the Jio ecosystem, offering payments, recharges, and access to Jio services. You can pay bills, transfer money, and make merchant payments through the app.

The wallet works best for Jio users who want to manage payments within the Jio platform. It also supports payments on other platforms through UPI for broader business use.

YONO SBI

YONO SBI (You Only Need One) is State Bank of India's comprehensive banking and payment app. It's an open wallet that provides full banking services including payments, transfers, account management, and loans.

You can withdraw cash, pay merchants, and access all SBI banking features through one app. It's ideal for SBI customers who want complete banking integration for their business operations.

PayZapp

PayZapp is HDFC Bank's digital wallet offering tap and pay functionality through NFC. It supports card payments, UPI transfers, bill payments, and merchant transactions.

The wallet works well for HDFC customers who want contactless payment options. It also offers rewards and cashback on various transactions for business spending.

What are the benefits of using digital wallets?

Digital wallets offer several advantages over traditional payment methods. Here's what they offer:

- Instant transactions: Payments complete in seconds, letting you finish transactions quickly without waiting for card approvals or bank processing.

- No physical items needed: Everything sits on your phone, so you don't need to carry cash, cards, or checkbooks for business meetings or transactions.

- Automatic tracking: Every transaction gets recorded instantly with date, time, amount, and recipient details that you can review for accounting.

- Better security: Encryption protects your payment data, biometric authentication adds protection, and remote blocking helps if you lose your phone.

- Multiple payment options: Choose between UPI, stored balance, linked cards, or bank transfers based on what works best for each transaction.

- Real-time notifications: Get alerts for every transaction so you know immediately when customers pay or when you send money to vendors.

- Lower operational costs: Digital payments reduce the need for handling physical cash, bank visits, and manual reconciliation work.

The combination of speed, security, and tracking makes digital wallets practical for both personal use and business operations. But while consumer wallets work well for everyday transactions, businesses handling international payments need more specialized features.

How do digital wallets work?

Digital wallets connect your existing financial accounts to a mobile app that handles transactions. Here's how the process works:

- Setup and verification: Download a wallet app, create an account, verify your phone number, and link a bank account or card for secure access to your funds.

- Adding money: Load funds into your wallet balance directly from your bank account, or use UPI-based wallets that pull money in real-time during each transaction.

- Making payments: Select the recipient by scanning a QR code, entering a phone number, or choosing from contacts, then enter the amount and confirm the transaction.

- Security processing: The app encrypts your payment information and uses tokens (temporary codes) instead of sharing your actual card or account numbers with merchants.

- Authorization: The payment processor checks your available funds, verifies the transaction isn't fraudulent, and transfers the money within seconds.

- Confirmation: Both you and the recipient receive instant notifications confirming the payment, with complete transaction records stored in the app.

How to choose the right digital wallet?

Picking a digital wallet depends on how you'll use it. Different wallets serve different needs, and what works for personal use might not work for business operations. Here's what to consider:

- Identify your use case: For accepting local customer payments or paying vendors, popular UPI-based wallets work fine, but international business operations need more specialized features.

- Check acceptance: If your business operates on specific platforms like Amazon or needs to accept payments from many customers, choose wallets with wide acceptance and easy QR code generation.

- Review fees and charges: Most consumer wallets charge zero fees for UPI transfers, but business transactions, payment gateway features, and international payments have varying fees you should review carefully.

- Evaluate security: Pick wallets with two-factor authentication, biometric login, transaction alerts, spending limits, and remote account locking for better protection of business funds.

- Consider business features: If you need invoice generation, payment links, recurring payments, multiple user access, or detailed reporting for accounting, consumer wallets won't meet these requirements.

- Assess international needs: For collecting payments from clients abroad, you need multi-currency support, foreign exchange management, compliance documentation, and reliable success rates that standard wallets don't provide.

- Test the experience: Download a few options and make small transactions to see which interface feels most natural and efficient for your daily workflow.

The biggest question is whether a consumer wallet actually fits your business model. If you're exporting goods or services, accepting international payments, or managing complex payment workflows, you need a solution built for those specific challenges.

Get paid globally in multiple currencies with PayGlocal

Consumer digital wallets work well for everyday transactions in India. But when you're running a business that serves international clients or handles cross-border payments, those wallets fall short.

You need tools that handle multiple currencies, provide instant compliance documents, offer transparent tracking across borders, and deliver high payment success rates. Standard wallets can't do this because they're built for local, consumer-focused transactions.

PayGlocal provides the payment infrastructure you need for global commerce:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD that make you look local to international clients.

- Instant compliance: Get FIRC (Foreign Inward Remittance Certificate) documents right in your inbox after settlement without paperwork delays.

- Global payment methods: Offer 40+ local payment methods to international customers, increasing trust and conversions by letting clients pay through their preferred methods.

- Dynamic checkout: Provide a customizable checkout experience for global customers with multiple payment flows and easy integration with your existing systems.

- Recurring payments: Handle subscriptions and recurring billing on international cards with network-compliant solutions and auto-debit functionality from one platform.

PayGlocal handles the complexity of cross-border payments so you can focus on growing your business. While consumer wallets keep your personal spending organized, PayGlocal powers your international revenue with the reliability and features you need.

Final thoughts

Digital wallets have made payments faster and more convenient across India. They work well for personal transactions, bill payments, and local commerce. The variety of options means you can find a wallet that fits your basic payment needs.

But business requirements differ from personal use, especially when you're dealing with international clients. Consumer wallets can't handle multi-currency complexity or the payment success rates you need for cross-border commerce.

If you're exporting products or services, the right payment infrastructure makes a significant difference. PayGlocal gives you the tools to collect globally and settle locally with transparent pricing and reliable processing.

Get started with PayGlocal today and start collecting payments globally.