Electronic payments are transforming the way money is transferred globally. They're faster, cheaper, and more reliable than traditional methods, such as cheques or bank transfers.

Research shows that global digital wallet spending will cross $10 trillion in 2025, marking a major jump from earlier years. In fact, research shows that digital wallets will handle $25 trillion in transactions by 2027, becoming the top choice for online payments globally.

In this guide, you’ll get a detailed breakdown of electronic payments, how they work, their different types, and how you can use them to grow your business.

Key Takeaways

- Electronic payments reduce costs and delays: Compared to traditional banking methods, they help businesses improve cash flow.

- Multiple payment types exist: To serve different business needs, from instant transfers to secure international collections.

- Smart businesses choose reliable payment partners: To avoid common problems like failed transactions and compliance issues.

- Solutions like PayGlocal help Indian businesses: Collect payments globally with higher success rates and transparent pricing.

What are electronic payments?

Electronic payments are digital transactions that transfer money from one account to another without the use of cash or physical checks.

Instead of handing over bills or writing cheques in the banks, payments are made through computer networks and digital systems that connect multiple banks, payment processors, and financial institutions worldwide.

When you make an electronic payment, your banking information gets encrypted and transmitted through secure networks to the recipient's financial institution. The entire process involves multiple security layers, verification steps, and automated systems that ensure money reaches the right destination safely.

For example, a freelancer in India can receive payment from a client in New York through payment gateways like PayGlocal, RazorPay, etc., and the money arrives in the account the same day. The complete transaction records and makes it highly feasible for customers to use it on a regular basis.

Studies show that cashless payments worldwide are expected to nearly double between 2024 and 2028, driven by the shift to real-time payment systems.

Here's how money moves electronically from sender to receiver:

- Customer initiates payment: The person or business starts the payment through their bank, app, or payment platform.

- The payment gateway processes the request: A secure system captures the payment details and verifies that everything is correct.

- The payment processor verifies and transfers funds: It confirms that the sender has sufficient funds, runs fraud checks, and processes the transaction through banking networks.

- The merchant receives payment settlement: The money arrives in the receiver's account, typically within 1-3 business days.

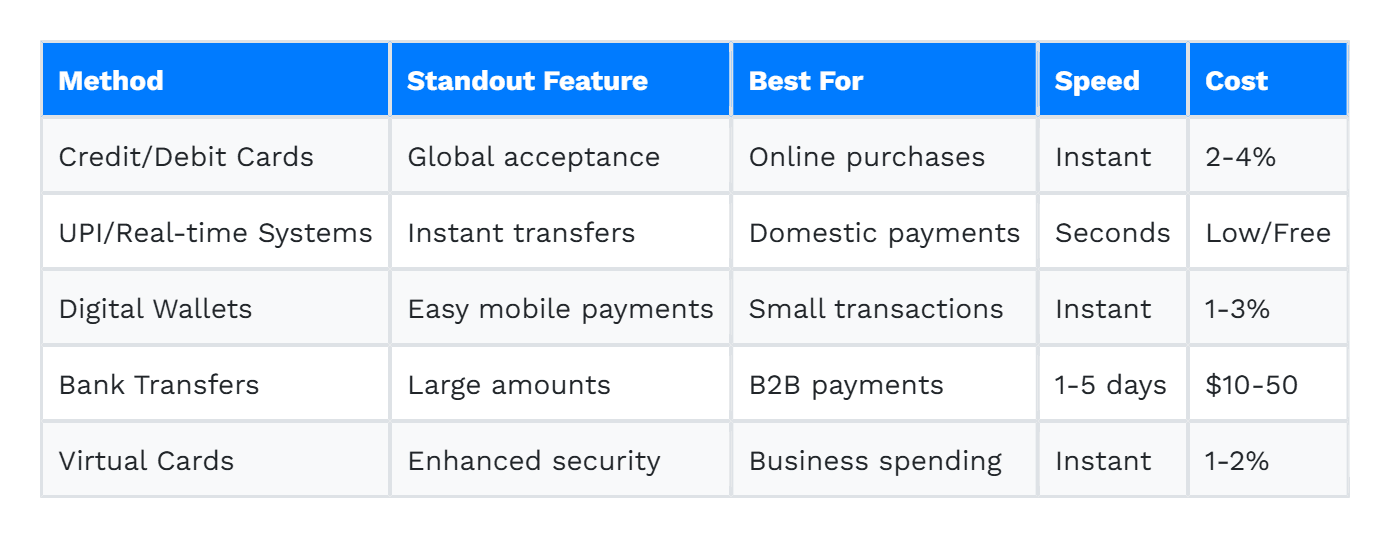

Each payment method works differently and serves specific needs. Here’s a quick overview of the most common electronic payment methods and their key features:

Let's look at each payment method in detail:

Credit and debit cards remain the most popular payment methods for both online and offline transactions worldwide. They work through secure payment gateways that process transactions in real-time, making them ideal for e-commerce and international business.

For instance, an online retailer can accept Visa, Mastercard, and American Express payments from customers in over 200 countries without needing separate banking relationships in each location.

Cards are particularly useful for global transactions because they're accepted almost everywhere. Most card processing systems can handle multiple currencies, making it easy for businesses to serve customers from different countries without worrying about payment compatibility.

UPI (Unified Payments Interface) has transformed how people pay in India by enabling instant money transfers using just a phone number or QR code.

For example, an export business can collect payments from buyers instantly through UPI by sharing a simple payment link or QR code. This reduces follow-ups, speeds up collections, and improves working capital management, especially when managing multiple orders and cash cycles.

These systems work well for both domestic and international transfers. They are fast, usually free or low-cost, and help businesses simplify payouts and collections. For exporters, freelancers, and finance teams, real-time payments make it easier to manage cash flow and reduce delays.

Digital wallets like PayPal, Google Pay, and PhonePe store payment information securely and make transactions quick and easy. Users can pay with just a few taps on their phone or computer.

For instance, an exporter can receive payments from multiple clients worldwide through PayGlocal and withdraw the money to their local bank account in their preferred currency.

Freelancers and small businesses often prefer digital wallets because they're simple to set up and use. They're also great for smaller transactions where the convenience outweighs slightly higher fees compared to direct bank transfers.

Traditional bank transfers remain important for large business transactions. In India, NEFT (National Electronic Funds Transfer) and RTGS (Real Time Gross Settlement) handle domestic transfers, while ACH (Automated Clearing House) and SWIFT facilitate international transfers between banks.

For example, a manufacturing company making a ₹50 lakh payment to a supplier would typically use RTGS for immediate settlement, while smaller routine payments might use NEFT.

These methods are most effective for business payments and payroll, as they can safely handle large amounts. ACH payments are particularly popular for international transactions due to their reliability and lower costs compared to wire transfers.

Virtual cards are digital-only payment cards that businesses use for controlled spending. They can be created instantly, set with spending limits, and canceled anytime, making them perfect for online purchases and vendor payments.

For instance, a marketing agency can create separate virtual cards for each advertising platform, like Google Ads and Facebook Ads, with specific monthly limits to control campaign spending.

Companies use virtual cards to pay for software subscriptions, advertising campaigns, and supplier invoices. They provide better security than sharing actual card numbers and give finance teams more control over business spending.

Businesses are using electronic payments for financial transactions for cross border transactions to grow faster. Here are some of the top examples of how businesses are using electronic payment systems:

A web developer in India working for US clients can receive payments in USD through multi-currency accounts and get the money converted to INR at competitive rates. This removes the hassle of international wire transfers and reduces waiting time from weeks to days.

A handicrafts exporter in India can send invoices to European buyers and accept payments through multiple methods, including cards, bank transfers, and local payment options. International payment platforms handle currency conversion and compliance automatically, making global sales as easy as domestic ones.

A software company can set up recurring payments for its monthly subscription service, automatically charging customers in their local currency. This improves customer experience and ensures consistent revenue without manual billing each month.

Online travel agencies can offer customers multiple payment options, including local methods, cards, and digital wallets, through a dynamic checkout system. This increases conversion rates because customers can pay using their preferred method.

E-commerce platforms can use payment links and split settlement features to distribute payments between multiple vendors after a sale automatically. This eliminates the need for manual calculations, ensuring everyone receives payment quickly and accurately.

Studies show that India's fintech sector will reach $155.67 billion in 2025 and grow to $990.45 billion by 2032, showing how rapidly businesses are adopting digital payment solutions. Here are the top advantages of electronic payments:

- Faster payments and settlements: Money moves in hours or days instead of weeks, improving cash flow and reducing the time between completing work and getting paid.

- Lower operational costs: Processing electronic payments costs less than handling checks, cash deposits, or wire transfers, especially for businesses handling many transactions.

- Better tracking and transparency: Every electronic payment creates a digital record, making it easier to track money, match payments with invoices, and provide payment status updates to customers.

- Supports international expansion: Electronic payments make it practical to serve customers worldwide without setting up banking relationships in every country.

- Easier compliance and record-keeping: Digital payment records integrate with accounting software, reducing manual data entry and making tax filing and financial reporting more accurate.

While electronic payments offer numerous advantages, businesses often encounter specific challenges that can disrupt operations and impact customer satisfaction.

Here are the main challenges and effective approaches to solve them:

- Payment failures and declined transactions: International payments fail more often due to different banking systems and fraud prevention rules. Choose payment providers with high success rates and multiple routing options to reduce declines.

- Currency conversion complexity: Exchange rates change constantly, and fees vary between providers, making it hard to predict final amounts. Use platforms that offer transparent currency conversion rates and real-time fee calculations.

- Settlement delays in cross-border payments: Money can take 3-7 days to arrive due to different banking hours and compliance checks. Work with providers that offer faster settlement times and clear tracking throughout the process.

- Lack of payment status visibility: Not knowing where the money is during transit creates uncertainty for both businesses and customers. Select payment solutions that provide real-time updates and detailed transaction tracking.

- Integration challenges with local banking: Connecting international payment systems with local banks can be complicated and time-consuming.

We know international payments can be challenging and complex. That's why PayGlocal builds solutions that actually work for growing businesses.

You focus on your work. We make sure your payments arrive safely. No delays, no guesswork, just reliable international payment collections in your currency.

Here's how PayGlocal solves payment problems:

- Multi-currency accounts in 4 countries: Collect payments locally in USD, GBP, EUR, and CAD without international transfer delays or high fees.

- Better payment success rates: Our smart routing and fraud prevention systems ensure more transactions go through successfully, even during peak seasons.

- Transparent pricing with no hidden fees: See exactly what you'll pay upfront with competitive rates and no surprise charges or monthly fees.

- Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) automatically after settlement to stay compliant with Indian regulations without extra paperwork.

- Real-time payment tracking: Know exactly where your money is at every step with notifications and dashboard updates throughout the payment process.

Get started with PayGlocal today and experience global payments the easy way.

Electronic payments have become essential for modern business, offering speed, security, and global reach that traditional methods simply can't match. Whether you're a freelancer, exporter, or growing company, understanding these payment methods helps you choose the right solution for your needs.

The key is finding a payment provider that understands your business challenges and offers real solutions, not just technology. PayGlocal specializes in helping Indian businesses collect payments globally with better success rates, transparent pricing, and automated compliance.

Ready to simplify your global payments? Get started with PayGlocal and see why leading businesses trust us for their international payment needs.

Research shows that global digital wallet spending will cross $10 trillion in 2025, marking a major jump from earlier years. In fact, research shows that digital wallets will handle $25 trillion in transactions by 2027, becoming the top choice for online payments globally.

In this guide, you’ll get a detailed breakdown of electronic payments, how they work, their different types, and how you can use them to grow your business.

Key Takeaways

- Electronic payments reduce costs and delays: Compared to traditional banking methods, they help businesses improve cash flow.

- Multiple payment types exist: To serve different business needs, from instant transfers to secure international collections.

- Smart businesses choose reliable payment partners: To avoid common problems like failed transactions and compliance issues.

- Solutions like PayGlocal help Indian businesses: Collect payments globally with higher success rates and transparent pricing.

What are electronic payments?

Electronic payments are digital transactions that transfer money from one account to another without the use of cash or physical checks.

Instead of handing over bills or writing cheques in the banks, payments are made through computer networks and digital systems that connect multiple banks, payment processors, and financial institutions worldwide.

When you make an electronic payment, your banking information gets encrypted and transmitted through secure networks to the recipient's financial institution. The entire process involves multiple security layers, verification steps, and automated systems that ensure money reaches the right destination safely.

For example, a freelancer in India can receive payment from a client in New York through payment gateways like PayGlocal, RazorPay, etc., and the money arrives in the account the same day. The complete transaction records and makes it highly feasible for customers to use it on a regular basis.

How do electronic payments work?

Studies show that cashless payments worldwide are expected to nearly double between 2024 and 2028, driven by the shift to real-time payment systems.

Here's how money moves electronically from sender to receiver:

- Customer initiates payment: The person or business starts the payment through their bank, app, or payment platform.

- The payment gateway processes the request: A secure system captures the payment details and verifies that everything is correct.

- The payment processor verifies and transfers funds: It confirms that the sender has sufficient funds, runs fraud checks, and processes the transaction through banking networks.

- The merchant receives payment settlement: The money arrives in the receiver's account, typically within 1-3 business days.

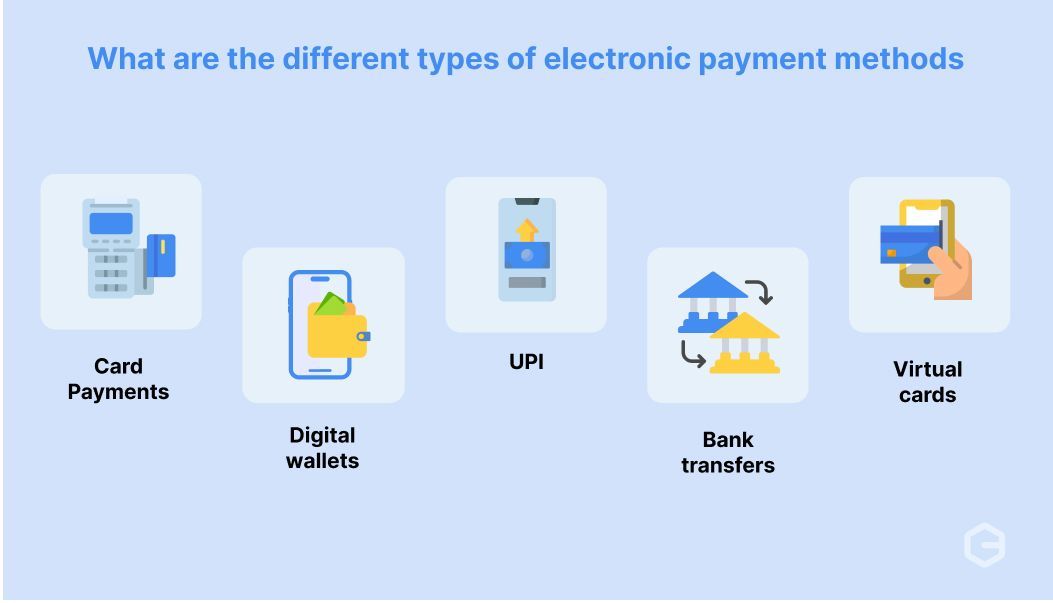

What are the different types of electronic payment methods?

Each payment method works differently and serves specific needs. Here’s a quick overview of the most common electronic payment methods and their key features:

Let's look at each payment method in detail:

1. Credit and debit card payments

Credit and debit cards remain the most popular payment methods for both online and offline transactions worldwide. They work through secure payment gateways that process transactions in real-time, making them ideal for e-commerce and international business.

For instance, an online retailer can accept Visa, Mastercard, and American Express payments from customers in over 200 countries without needing separate banking relationships in each location.

Cards are particularly useful for global transactions because they're accepted almost everywhere. Most card processing systems can handle multiple currencies, making it easy for businesses to serve customers from different countries without worrying about payment compatibility.

2. UPI and real-time payment systems

UPI (Unified Payments Interface) has transformed how people pay in India by enabling instant money transfers using just a phone number or QR code.

For example, an export business can collect payments from buyers instantly through UPI by sharing a simple payment link or QR code. This reduces follow-ups, speeds up collections, and improves working capital management, especially when managing multiple orders and cash cycles.

These systems work well for both domestic and international transfers. They are fast, usually free or low-cost, and help businesses simplify payouts and collections. For exporters, freelancers, and finance teams, real-time payments make it easier to manage cash flow and reduce delays.

3. Digital wallets

Digital wallets like PayPal, Google Pay, and PhonePe store payment information securely and make transactions quick and easy. Users can pay with just a few taps on their phone or computer.

For instance, an exporter can receive payments from multiple clients worldwide through PayGlocal and withdraw the money to their local bank account in their preferred currency.

Freelancers and small businesses often prefer digital wallets because they're simple to set up and use. They're also great for smaller transactions where the convenience outweighs slightly higher fees compared to direct bank transfers.

4. Bank transfers (NEFT, RTGS, ACH, wire transfers)

Traditional bank transfers remain important for large business transactions. In India, NEFT (National Electronic Funds Transfer) and RTGS (Real Time Gross Settlement) handle domestic transfers, while ACH (Automated Clearing House) and SWIFT facilitate international transfers between banks.

For example, a manufacturing company making a ₹50 lakh payment to a supplier would typically use RTGS for immediate settlement, while smaller routine payments might use NEFT.

These methods are most effective for business payments and payroll, as they can safely handle large amounts. ACH payments are particularly popular for international transactions due to their reliability and lower costs compared to wire transfers.

5. Virtual cards and commercial cards

Virtual cards are digital-only payment cards that businesses use for controlled spending. They can be created instantly, set with spending limits, and canceled anytime, making them perfect for online purchases and vendor payments.

For instance, a marketing agency can create separate virtual cards for each advertising platform, like Google Ads and Facebook Ads, with specific monthly limits to control campaign spending.

Companies use virtual cards to pay for software subscriptions, advertising campaigns, and supplier invoices. They provide better security than sharing actual card numbers and give finance teams more control over business spending.

How do businesses use electronic payment systems for cross-border transactions?

Businesses are using electronic payments for financial transactions for cross border transactions to grow faster. Here are some of the top examples of how businesses are using electronic payment systems:

1. Freelancers getting paid globally

A web developer in India working for US clients can receive payments in USD through multi-currency accounts and get the money converted to INR at competitive rates. This removes the hassle of international wire transfers and reduces waiting time from weeks to days.

2. Exporters serving international customers

A handicrafts exporter in India can send invoices to European buyers and accept payments through multiple methods, including cards, bank transfers, and local payment options. International payment platforms handle currency conversion and compliance automatically, making global sales as easy as domestic ones.

3. SaaS companies billing overseas clients

A software company can set up recurring payments for its monthly subscription service, automatically charging customers in their local currency. This improves customer experience and ensures consistent revenue without manual billing each month.

4. Travel businesses offering flexible payments

Online travel agencies can offer customers multiple payment options, including local methods, cards, and digital wallets, through a dynamic checkout system. This increases conversion rates because customers can pay using their preferred method.

5. Marketplaces managing vendor payments

E-commerce platforms can use payment links and split settlement features to distribute payments between multiple vendors after a sale automatically. This eliminates the need for manual calculations, ensuring everyone receives payment quickly and accurately.

What are the benefits of electronic payments for businesses?

Studies show that India's fintech sector will reach $155.67 billion in 2025 and grow to $990.45 billion by 2032, showing how rapidly businesses are adopting digital payment solutions. Here are the top advantages of electronic payments:

- Faster payments and settlements: Money moves in hours or days instead of weeks, improving cash flow and reducing the time between completing work and getting paid.

- Lower operational costs: Processing electronic payments costs less than handling checks, cash deposits, or wire transfers, especially for businesses handling many transactions.

- Better tracking and transparency: Every electronic payment creates a digital record, making it easier to track money, match payments with invoices, and provide payment status updates to customers.

- Supports international expansion: Electronic payments make it practical to serve customers worldwide without setting up banking relationships in every country.

- Easier compliance and record-keeping: Digital payment records integrate with accounting software, reducing manual data entry and making tax filing and financial reporting more accurate.

What are the common challenges businesses face with electronic payments?

While electronic payments offer numerous advantages, businesses often encounter specific challenges that can disrupt operations and impact customer satisfaction.

Here are the main challenges and effective approaches to solve them:

- Payment failures and declined transactions: International payments fail more often due to different banking systems and fraud prevention rules. Choose payment providers with high success rates and multiple routing options to reduce declines.

- Currency conversion complexity: Exchange rates change constantly, and fees vary between providers, making it hard to predict final amounts. Use platforms that offer transparent currency conversion rates and real-time fee calculations.

- Settlement delays in cross-border payments: Money can take 3-7 days to arrive due to different banking hours and compliance checks. Work with providers that offer faster settlement times and clear tracking throughout the process.

- Lack of payment status visibility: Not knowing where the money is during transit creates uncertainty for both businesses and customers. Select payment solutions that provide real-time updates and detailed transaction tracking.

- Integration challenges with local banking: Connecting international payment systems with local banks can be complicated and time-consuming.

Electronic payments made easy with PayGlocal

We know international payments can be challenging and complex. That's why PayGlocal builds solutions that actually work for growing businesses.

You focus on your work. We make sure your payments arrive safely. No delays, no guesswork, just reliable international payment collections in your currency.

Here's how PayGlocal solves payment problems:

- Multi-currency accounts in 4 countries: Collect payments locally in USD, GBP, EUR, and CAD without international transfer delays or high fees.

- Better payment success rates: Our smart routing and fraud prevention systems ensure more transactions go through successfully, even during peak seasons.

- Transparent pricing with no hidden fees: See exactly what you'll pay upfront with competitive rates and no surprise charges or monthly fees.

- Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) automatically after settlement to stay compliant with Indian regulations without extra paperwork.

- Real-time payment tracking: Know exactly where your money is at every step with notifications and dashboard updates throughout the payment process.

Get started with PayGlocal today and experience global payments the easy way.

Final thoughts

Electronic payments have become essential for modern business, offering speed, security, and global reach that traditional methods simply can't match. Whether you're a freelancer, exporter, or growing company, understanding these payment methods helps you choose the right solution for your needs.

The key is finding a payment provider that understands your business challenges and offers real solutions, not just technology. PayGlocal specializes in helping Indian businesses collect payments globally with better success rates, transparent pricing, and automated compliance.

Ready to simplify your global payments? Get started with PayGlocal and see why leading businesses trust us for their international payment needs.