The way we pay for things today would seem like magic to someone from just 50 years ago. Tap your phone, scan a code, or click a button, and money moves instantly across the globe.

But this didn't happen overnight. The history of online payments spans over 150 years of innovation, from telegraph-based transfers to today's AI-powered systems.

Each breakthrough solved real problems that businesses and consumers faced, making transactions faster, safer, and more accessible.

Online payments are digital transactions that transfer money between parties through electronic systems rather than physical cash or checks. These transactions work through a network of financial institutions, payment processors, and technology platforms that verify, authorize, and settle transactions securely.

When you buy something online or send money to someone, multiple systems work together to move funds from your account to the recipient's account within seconds or minutes through various payment processing types.

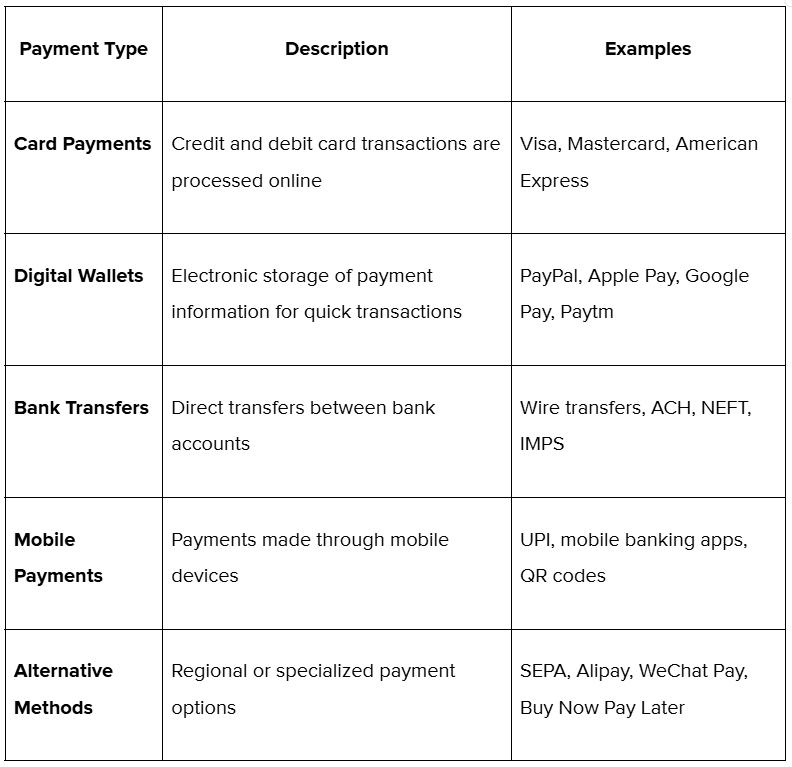

Online payments are divided into multiple categories, each serving different needs and preferences:

Each type serves specific markets and needs. While card payments dominate global e-commerce, mobile payments like UPI have revolutionized transactions in markets like India, and alternate payment methods help businesses reach customers who prefer local payment options.

The journey from cash-only commerce to today's instant digital payments happened through distinct phases. Here's how online payments developed across different time periods:

Each era solved specific problems while building the foundation for what came next.

The story begins in 1871 when Western Union introduced the first electronic fund transfer in the United States. This telegraph-based system allowed people to send money without physical transportation for the first time. Banks began connecting through telecommunication networks in the 1960s, creating the infrastructure that would later support digital payments.

These early systems were slow and expensive, but they proved that money could move electronically. The concept of international money transfer without physical currency transportation became a reality, setting the stage for everything that followed.

Bank of America launched BankAmericard in 1958, which later became Visa. This marked the beginning of plastic money and established the four-party model (cardholder, merchant, issuer, acquirer) that still powers card payments today. Mastercard followed in 1966, creating competition that drove innovation.

The 1970s saw the development of POS (Point-of-Sale) terminals and magnetic stripe technology that made card processing faster and more reliable. These innovations created the foundation for electronic commerce that would rapidly expand with the internet's arrival.

The public internet's availability in 1991 changed everything. In 1994, Phil Brandenberger made the first secure online purchase through NetMarket using encrypted credit card data. That same year, First Virtual Holdings created the first dedicated online payment system for credit card transactions.

Stanford Federal Credit Union launched the first comprehensive online banking service in 1994, while Presidential Bank offered online account access in 1995. Companies like Amazon and eBay popularized online shopping during the late 1990s, creating massive demand for secure digital payment methods.

This decade proved that consumers would trust digital transactions if they were secure and convenient.

PayPal's launch in 1998 changed online payments by creating a secure, user-friendly platform for both peer-to-peer and merchant transactions. This proved that specialized payment companies could compete with traditional banks by focusing on user experience and security.

The introduction of Apple Pay, Google Pay, and Samsung Pay brought mobile payment solutions to mainstream consumers. NFC (Near Field Communication) technology enabled tap-and-go payments, while QR (Quick Response) codes became popular in Asian markets for their simplicity and low implementation costs. The iPhone's launch in 2007 accelerated mobile commerce and payment app development significantly.

India's UPI (Unified Payments Interface) launch in 2016 showed how government-backed payment systems could achieve massive scale rapidly. UPI processed over 131 billion transactions in 2023, demonstrating that real-time, free, and interoperable payments could work at a national scale.

Recent years have accelerated digital payment adoption globally, with contactless payments becoming standard. Today's systems process transactions in milliseconds, support multiple currencies, and use AI (Artificial Intelligence) to enhance reliability and security.

AI reviews transaction patterns in real time, checking factors like location, amount, and user behavior. This helps identify irregularities and supports smoother, more accurate processing without slowing down regular transactions.

The global digital payment transaction value reached $8.5 trillion in 2024, with over 2 billion people worldwide using digital wallets. The market is projected to reach $36.75 trillion by 2029, showing the massive growth still ahead.

India's path to digital payments leadership involved deliberate infrastructure building, government initiatives, and rapid consumer adoption. The country went from cash-dependent transactions to processing nearly half the world's real-time payments in just three decades.

Here's how India's digital payment journey unfolded:

Let’s take a closer look at each one of these phases in more detail.

India's digital payment journey began with basic electronic banking infrastructure. HSBC installed the first ATM in 1987, introducing Indians to electronic cash access. The Central Bank of India had issued the country's first credit card in 1980, but adoption remained limited to urban areas and higher-income segments.

ICICI Bank pioneered online banking in 1996, allowing customers to check balances and transfer funds through the internet. This early adoption by private banks pushed public sector banks to modernize their technology infrastructure.

BillDesk launched in 2003 as India's first payment aggregator, enabling online bill payments and merchant transactions. Oxigen Wallet followed in 2004 as the country's first e-wallet, though smartphone adoption was still years away.

The Reserve Bank of India established NEFT (National Electronic Funds Transfer) in 2005, creating a nationwide electronic fund transfer system that connected all banks. IMPS (Immediate Payment Service) followed in 2010, enabling instant 24/7 transfers and laying the groundwork for real-time payment systems.

Digital payment volume in India increased from 20.71 billion transactions in FY 2017-18 to 187.37 billion in FY 2023-24, showing a remarkable 44% annual growth.

NPCI (National Payments Corporation of India) developed the RuPay card scheme in 2012, creating a domestic alternative to international card networks and reducing dependence on foreign payment systems. Mobile wallets like Paytm and MobiKwik gained traction as smartphone adoption accelerated rapidly.

The BBPS (Bharat Bill Pay System) was launched in 2013, standardizing bill payments across the country. Oxigen launched a semi-closed wallet in 2014, enabling peer-to-peer transfers via social networks and messaging platforms - a first in India. These initiatives created the ecosystem necessary for India's digital payment growth that would follow.

UPI's launch in 2016 by RBI Governor Dr. Raghuram Rajan revolutionized Indian payments. The demonetization drive that same year accelerated adoption as cash became scarce, pushing millions toward digital alternatives.

UPI's growth has been remarkable. It went from 920 million transactions in FY 2017-18 to over 131 billion in FY 2023-24, achieving a 129% CAGR (Compound Annual Growth Rate). India now processes 49% of the world's real-time payments, with UPI accounting for 84% of retail digital payment volumes. In October 2024 alone, UPI processed 16.58 billion transactions.

India's digital payment market reached $85 billion in 2024 and is projected to hit $135 billion by 2027. The country leads global real-time payment adoption, with businesses increasingly requiring sophisticated payment infrastructure for international expansion.

e-RUPI's introduction in 2021 showed India's continued innovation in digital payments - a cashless and contactless digital voucher system for targeted welfare payments.

The integration of UPI with international payment systems demonstrates the country's growing influence in global payment standards. Transaction volume is expected to triple from 159 billion in FY24 to 481 billion by FY29, with value doubling from ₹265 trillion to ₹593 trillion.

Online payments have transformed how businesses and consumers handle transactions, offering advantages that extend far beyond simple convenience.

The shift to digital payments brings measurable benefits for all stakeholders:

Despite their advantages, online payments face several significant challenges that businesses must handle carefully. These obstacles help companies prepare better solutions and choose reliable payment partners:

The future of online payments promises even more innovation as technology advances and consumer expectations continue evolving.

Several trends are shaping the next generation of payment systems:

While payment technology continues advancing rapidly, businesses need reliable platforms that can handle this complexity and deliver results today. PayGlocal combines modern payment innovation with effective solutions that work for companies expanding globally.

Here's how PayGlocal solves modern payment challenges:

PayGlocal combines the innovation of modern payment technology with the reliability and support that growing businesses need. Whether you're a freelancer collecting international payments or an enterprise scaling globally, PayGlocal provides the best infrastructure you need to succeed.

The history of online payments reveals a consistent pattern: successful innovations solve real problems while making transactions simpler and more accessible. From Western Union's telegraph transfers to today's instant mobile payments, each breakthrough built upon previous foundations while addressing new challenges.

Today's businesses operate in the most connected payment environment in history, with options ranging from traditional cards to cutting-edge digital currencies. However, this abundance of choice creates new challenges in selecting the right payment infrastructure for global growth.

PayGlocal represents the next evolution in this journey - a payment partner built specifically for Indian businesses expanding globally, offering modern technology with practical solutions that work from day one.

Ready to try a better way to handle international payments? Get started with PayGlocal today and experience the future of global payment processing.

But this didn't happen overnight. The history of online payments spans over 150 years of innovation, from telegraph-based transfers to today's AI-powered systems.

Each breakthrough solved real problems that businesses and consumers faced, making transactions faster, safer, and more accessible.

Key takeaways:

- Digital payment has a long history: From telegraph transfers in 1871 to today's AI-powered systems, each innovation solved specific problems while building upon previous foundations.

- Mobile and real-time payments drive current growth: UPI in India and similar systems globally prove that instant payment solutions can achieve massive scale when properly designed and implemented.

- PayGlocal offers modern solutions: With multi-currency accounts, transparent pricing, and 40+ payment methods, PayGlocal addresses the specific needs of Indian businesses expanding globally.

- Future payments will be smarter and effective: AI personalization, biometric security, and embedded finance will make payment experiences seamless while maintaining security and compliance requirements.

What are online payments?

Online payments are digital transactions that transfer money between parties through electronic systems rather than physical cash or checks. These transactions work through a network of financial institutions, payment processors, and technology platforms that verify, authorize, and settle transactions securely.

When you buy something online or send money to someone, multiple systems work together to move funds from your account to the recipient's account within seconds or minutes through various payment processing types.

What are the types of online payments?

Online payments are divided into multiple categories, each serving different needs and preferences:

Each type serves specific markets and needs. While card payments dominate global e-commerce, mobile payments like UPI have revolutionized transactions in markets like India, and alternate payment methods help businesses reach customers who prefer local payment options.

How have online payments evolved over the years?

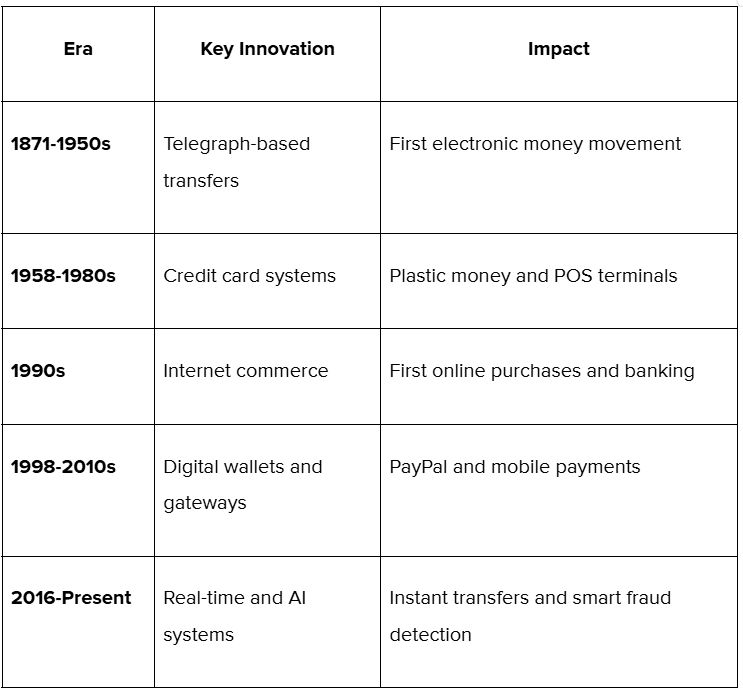

The journey from cash-only commerce to today's instant digital payments happened through distinct phases. Here's how online payments developed across different time periods:

Each era solved specific problems while building the foundation for what came next.

1. Telegraph transfers lay the foundation (1871-1950s)

The story begins in 1871 when Western Union introduced the first electronic fund transfer in the United States. This telegraph-based system allowed people to send money without physical transportation for the first time. Banks began connecting through telecommunication networks in the 1960s, creating the infrastructure that would later support digital payments.

These early systems were slow and expensive, but they proved that money could move electronically. The concept of international money transfer without physical currency transportation became a reality, setting the stage for everything that followed.

2. Credit cards enter the scene (1958-1980s)

Bank of America launched BankAmericard in 1958, which later became Visa. This marked the beginning of plastic money and established the four-party model (cardholder, merchant, issuer, acquirer) that still powers card payments today. Mastercard followed in 1966, creating competition that drove innovation.

The 1970s saw the development of POS (Point-of-Sale) terminals and magnetic stripe technology that made card processing faster and more reliable. These innovations created the foundation for electronic commerce that would rapidly expand with the internet's arrival.

3. The Internet enables online commerce (1990s)

The public internet's availability in 1991 changed everything. In 1994, Phil Brandenberger made the first secure online purchase through NetMarket using encrypted credit card data. That same year, First Virtual Holdings created the first dedicated online payment system for credit card transactions.

Stanford Federal Credit Union launched the first comprehensive online banking service in 1994, while Presidential Bank offered online account access in 1995. Companies like Amazon and eBay popularized online shopping during the late 1990s, creating massive demand for secure digital payment methods.

This decade proved that consumers would trust digital transactions if they were secure and convenient.

4. Payment gateways and digital wallets emerge (1998-2010s)

PayPal's launch in 1998 changed online payments by creating a secure, user-friendly platform for both peer-to-peer and merchant transactions. This proved that specialized payment companies could compete with traditional banks by focusing on user experience and security.

The introduction of Apple Pay, Google Pay, and Samsung Pay brought mobile payment solutions to mainstream consumers. NFC (Near Field Communication) technology enabled tap-and-go payments, while QR (Quick Response) codes became popular in Asian markets for their simplicity and low implementation costs. The iPhone's launch in 2007 accelerated mobile commerce and payment app development significantly.

5. Real-time and mobile-first payments (2016-present)

India's UPI (Unified Payments Interface) launch in 2016 showed how government-backed payment systems could achieve massive scale rapidly. UPI processed over 131 billion transactions in 2023, demonstrating that real-time, free, and interoperable payments could work at a national scale.

Recent years have accelerated digital payment adoption globally, with contactless payments becoming standard. Today's systems process transactions in milliseconds, support multiple currencies, and use AI (Artificial Intelligence) to enhance reliability and security.

AI reviews transaction patterns in real time, checking factors like location, amount, and user behavior. This helps identify irregularities and supports smoother, more accurate processing without slowing down regular transactions.

The global digital payment transaction value reached $8.5 trillion in 2024, with over 2 billion people worldwide using digital wallets. The market is projected to reach $36.75 trillion by 2029, showing the massive growth still ahead.

What is the history of online payments in India?

India's path to digital payments leadership involved deliberate infrastructure building, government initiatives, and rapid consumer adoption. The country went from cash-dependent transactions to processing nearly half the world's real-time payments in just three decades.

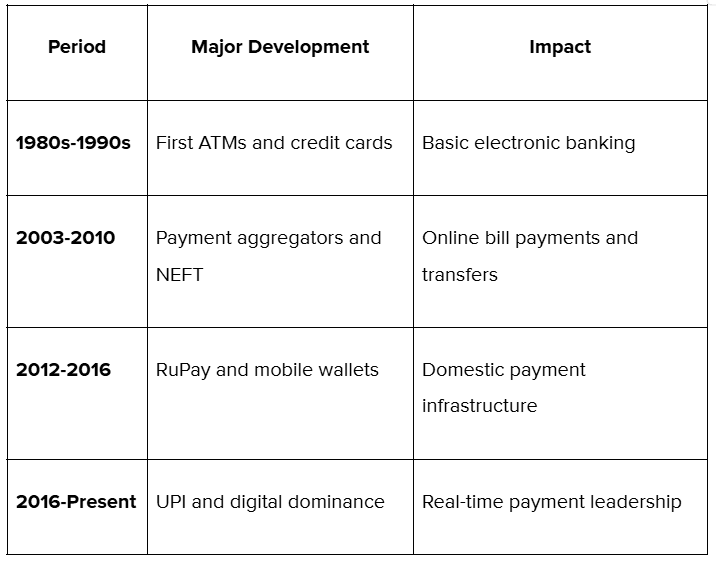

Here's how India's digital payment journey unfolded:

Let’s take a closer look at each one of these phases in more detail.

Pre-digital foundations (1980s-1990s)

India's digital payment journey began with basic electronic banking infrastructure. HSBC installed the first ATM in 1987, introducing Indians to electronic cash access. The Central Bank of India had issued the country's first credit card in 1980, but adoption remained limited to urban areas and higher-income segments.

ICICI Bank pioneered online banking in 1996, allowing customers to check balances and transfer funds through the internet. This early adoption by private banks pushed public sector banks to modernize their technology infrastructure.

Early digital infrastructure (2003-2010)

BillDesk launched in 2003 as India's first payment aggregator, enabling online bill payments and merchant transactions. Oxigen Wallet followed in 2004 as the country's first e-wallet, though smartphone adoption was still years away.

The Reserve Bank of India established NEFT (National Electronic Funds Transfer) in 2005, creating a nationwide electronic fund transfer system that connected all banks. IMPS (Immediate Payment Service) followed in 2010, enabling instant 24/7 transfers and laying the groundwork for real-time payment systems.

Digital payment volume in India increased from 20.71 billion transactions in FY 2017-18 to 187.37 billion in FY 2023-24, showing a remarkable 44% annual growth.

Mobile and digital wallet revolution (2012-2016)

NPCI (National Payments Corporation of India) developed the RuPay card scheme in 2012, creating a domestic alternative to international card networks and reducing dependence on foreign payment systems. Mobile wallets like Paytm and MobiKwik gained traction as smartphone adoption accelerated rapidly.

The BBPS (Bharat Bill Pay System) was launched in 2013, standardizing bill payments across the country. Oxigen launched a semi-closed wallet in 2014, enabling peer-to-peer transfers via social networks and messaging platforms - a first in India. These initiatives created the ecosystem necessary for India's digital payment growth that would follow.

UPI transforms the landscape (2016-present)

UPI's launch in 2016 by RBI Governor Dr. Raghuram Rajan revolutionized Indian payments. The demonetization drive that same year accelerated adoption as cash became scarce, pushing millions toward digital alternatives.

UPI's growth has been remarkable. It went from 920 million transactions in FY 2017-18 to over 131 billion in FY 2023-24, achieving a 129% CAGR (Compound Annual Growth Rate). India now processes 49% of the world's real-time payments, with UPI accounting for 84% of retail digital payment volumes. In October 2024 alone, UPI processed 16.58 billion transactions.

Current dominance and global leadership (2020-2025)

India's digital payment market reached $85 billion in 2024 and is projected to hit $135 billion by 2027. The country leads global real-time payment adoption, with businesses increasingly requiring sophisticated payment infrastructure for international expansion.

e-RUPI's introduction in 2021 showed India's continued innovation in digital payments - a cashless and contactless digital voucher system for targeted welfare payments.

The integration of UPI with international payment systems demonstrates the country's growing influence in global payment standards. Transaction volume is expected to triple from 159 billion in FY24 to 481 billion by FY29, with value doubling from ₹265 trillion to ₹593 trillion.

What are the benefits of online payments?

Online payments have transformed how businesses and consumers handle transactions, offering advantages that extend far beyond simple convenience.

The shift to digital payments brings measurable benefits for all stakeholders:

- Speed and efficiency - Transactions complete in seconds rather than days, enabling faster business cycles and improved cash flow management.

- Global reach without borders - Businesses can accept payments from customers worldwide without establishing banking relationships in each country.

- Reduced operational costs - Digital payments eliminate expenses related to cash handling, check processing, and manual reconciliation.

- Enhanced security features - Modern payment systems use encryption, tokenization, and AI-powered fraud detection that surpasses traditional payment security.

- Automatic record keeping - Every transaction creates a digital trail that simplifies accounting, tax compliance, and financial reporting.

- 24/7 availability - Unlike traditional banking hours, online payments work around the clock, supporting global business operations across time zones.

What are the challenges of online payments?

Despite their advantages, online payments face several significant challenges that businesses must handle carefully. These obstacles help companies prepare better solutions and choose reliable payment partners:

- Security vulnerabilities - Cyber attacks, data breaches, and fraud attempts constantly threaten payment systems, requiring ongoing investment in security measures.

- Technical complexity - Integration challenges, system compatibility issues, and downtime can disrupt business operations and customer experience.

- Regulatory compliance burden - Different countries have varying rules for data protection, anti-money laundering, and payment processing that complicate international operations.

- High transaction costs - Processing fees, currency conversion charges, and gateway costs can significantly impact business margins, especially for small transactions.

- Customer trust barriers - Some consumers remain hesitant about sharing financial information online, particularly for new or unfamiliar merchants.

- Cross-border complications - International payment challenges, currency fluctuations, and varying settlement times create challenges for global businesses.

What's next in online payments?

The future of online payments promises even more innovation as technology advances and consumer expectations continue evolving.

Several trends are shaping the next generation of payment systems:

- AI-powered personalization: Machine learning will create customized payment experiences, suggesting optimal payment methods based on user behavior and transaction patterns, while improving fraud detection capabilities.

- Biometric authentication everywhere: Fingerprint, facial recognition, and voice verification will replace passwords, making payments both more secure and more convenient across all devices and platforms.

- Invisible payment experiences: IoT (Internet of Things) integration will enable automatic payments for services like parking, tolls, and subscriptions without any user interaction required.

- CBDC (Central Bank Digital Currencies): Government-issued digital currencies will provide new options for cross-border payments and give central banks more direct control over monetary policy.

- Embedded finance integration: Payment capabilities will be built directly into business software, social media platforms, and everyday applications through APIs (Application Programming Interfaces), making transactions seamless within existing workflows.

- BNPL (Buy Now, Pay Later) expansion: This flexible payment method will continue growing beyond e-commerce into in-store purchases, subscription services, and larger ticket items, offering consumers more payment flexibility.

Go Global, Get Paid Instantly with PayGlocal

While payment technology continues advancing rapidly, businesses need reliable platforms that can handle this complexity and deliver results today. PayGlocal combines modern payment innovation with effective solutions that work for companies expanding globally.

Here's how PayGlocal solves modern payment challenges:

- Multi-currency account system: Get local bank accounts in USD, GBP, EUR, and CAD to collect payments without international transfer delays or excessive conversion fees.

- 40+ global payment methods: Accept payments through cards, digital wallets, bank transfers, and regional payment options that your international customers prefer.

- Instant compliance management: Receive FIRC (Foreign Inward Remittance Certificate) automatically and stay compliant with regulations without manual paperwork.

- Dynamic checkout experience: Provide customers with customizable, fast checkout flows that adapt to different payment preferences and regional requirements, improving conversion rates.

- Recurring payment solutions: Manage subscription billing and automated collections efficiently, supporting business models that require regular payment cycles and customer retention.

PayGlocal combines the innovation of modern payment technology with the reliability and support that growing businesses need. Whether you're a freelancer collecting international payments or an enterprise scaling globally, PayGlocal provides the best infrastructure you need to succeed.

Final thoughts

The history of online payments reveals a consistent pattern: successful innovations solve real problems while making transactions simpler and more accessible. From Western Union's telegraph transfers to today's instant mobile payments, each breakthrough built upon previous foundations while addressing new challenges.

Today's businesses operate in the most connected payment environment in history, with options ranging from traditional cards to cutting-edge digital currencies. However, this abundance of choice creates new challenges in selecting the right payment infrastructure for global growth.

PayGlocal represents the next evolution in this journey - a payment partner built specifically for Indian businesses expanding globally, offering modern technology with practical solutions that work from day one.

Ready to try a better way to handle international payments? Get started with PayGlocal today and experience the future of global payment processing.