You've landed your first international client, but now you're stuck figuring out how to actually get paid. The payment methods you've heard about either charge excessive fees, take weeks to process, or come with confusing compliance requirements.

Getting paid from overseas clients is important for scaling your business globally. Your payment method choice affects how much money you actually receive, how quickly you get paid, and whether you stay compliant with the regulations.

In this guide, we break down all the methods to accept international payments in India efficiently and cost-effectively. Find out which option fits your business needs and how to set everything up without the usual complications.

Accepting international payments in India refers to receiving funds from customers, clients, businesses, or individuals outside India, typically in foreign currencies such as USD, EUR, or GBP. These transactions involve cross-border fund transfers and require currency conversion, compliance, and proper documentation.

For instance, if you're a software developer in India billing a client in New York for a project, you're accepting an international payment. The process involves the client's payment traveling through banking networks, currency conversion, compliance checks, and finally settlement in your Indian bank account.

Accepting international payments opens significant opportunities for Indian businesses across all sectors. These benefits extend beyond just revenue growth to include competitive advantages and market expansion.

Indian businesses have several options for accepting international payments, each with distinct advantages and limitations:

Let’s take a detailed look at each method and see how they work.

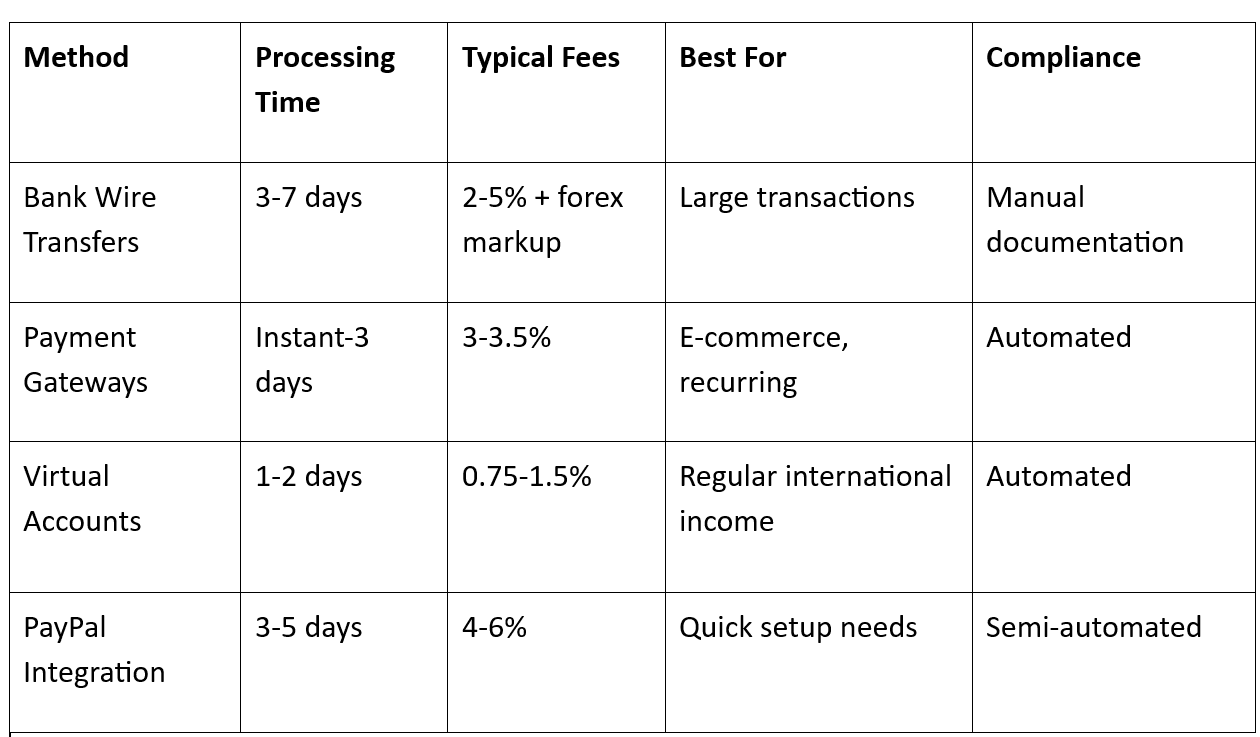

Traditional bank-to-bank transfers using the SWIFT network remain the most established method for international payments. Your client initiates a wire transfer through their bank, and the funds pass through intermediary banks before reaching your Indian account after conversion to the local currency.

For instance, when a US client sends $10,000 via SWIFT, the money travels from their bank to a correspondent bank, then to your Indian bank, with each institution potentially deducting fees along the way. Processing typically takes 3-7 business days.

Modern payment gateways like PayGlocal , Razorpay, and Stripe allow businesses to accept international card payments and alternative payment methods. These platforms handle currency conversion automatically and provide faster settlement than traditional banking.

For example, an e-commerce store using international payment gateways can accept payments in 100+ currencies, with automatic conversion to INR and settlement within 2-3 days.

Virtual accounts provide local bank details in major currencies (USD, EUR, GBP) without opening physical overseas accounts. Clients can make local transfers, which are faster and cheaper than international wires.

Consider a freelance marketing consultant using virtual accounts. They get USD account details to share with American clients, who can then send payments as domestic US transfers, arriving faster and with lower fees.

Services like PayGlocal , PayPal, Wise, and Payoneer offer quick setup and familiar interfaces for international clients. While convenient, they often carry higher fees and less favorable exchange rates compared to dedicated business solutions.

Setting up an international payment acceptance system involves several key steps to ensure compliance and optimal functionality.

1.Business registration and documentation: Ensure your business has all necessary documentation, such as GSTIN, and a current bank account in your business name. For physical goods exports, obtain an Importer Exporter Code (IEC) from the Director General of Foreign Trade (DGFT).

2. Choose your payment method and provider:Evaluate providers based on your business needs, such as transaction volume, customer locations, required features, and cost structure. Consider whether you need recurring payment capabilities, multi-currency settlement, or specific integrations.

3. Complete compliance requirements: Every international payment requires an RBI purpose code (like P0802 for software services or P1002 for trade services) and proper invoicing. Your payment provider should help automate this compliance documentation.

4. Integration and testing: Whether using payment buttons, hosted checkout pages, or API integration, thoroughly test the payment flow with small amounts before going live with customers.

5. Set up monitoring and reporting: Establish processes to track payment status, manage foreign exchange exposure, and maintain compliance records for tax and audit purposes.

International payment costs vary significantly between providers and methods. You need to consider all fees and charges to calculate your actual receiving amount.

For instance, a $10,000 payment could cost you anywhere from $150 to $60,0 depending on your chosen method, making provider selection crucial for your profitability.

While traditional options have served Indian businesses for years, they often come with high costs, slow processing, and complex compliance requirements. Modern businesses need payment solutions that match their growth ambitions.

PayGlocal enhances international payment acceptance by combining the reliability of traditional banking with the speed and transparency of modern fintech. Whether you're a startup receiving your first international payment or an enterprise managing thousands of transactions, PayGlocal scales with your needs.

Whether you're scaling a SaaS platform across multiple countries or managing e-commerce operations with global customers, PayGlocal provides the payment infrastructure you need to grow confidently and efficiently.

Accepting international payments in India has evolved from a complex, expensive process to an efficient business capability. The key is choosing the right method for your specific needs, considering costs, speed, compliance requirements, and customer preferences.

While multiple options exist, platforms like PayGlocal combine competitive pricing, fast settlement, automated compliance, and an excellent customer experience.

Ready to accept international payments and scale globally? PayGlocal offers everything you need to collect globally, settle locally, and grow without limits. Get started with PayGlocal today and see how easy international payments can be.

Getting paid from overseas clients is important for scaling your business globally. Your payment method choice affects how much money you actually receive, how quickly you get paid, and whether you stay compliant with the regulations.

In this guide, we break down all the methods to accept international payments in India efficiently and cost-effectively. Find out which option fits your business needs and how to set everything up without the usual complications.

Key Takeaways:

- Multiple payment methods available: Banks, payment gateways, and virtual accounts each offer different advantages for accepting international payments in India.

- Costs vary significantly: While some methods charge 4-5% in total fees, others offer transparent flat rates under 2% with better exchange rates.

- PayGlocal simplifies the process: Multi-currency accounts with competitive rates, instant compliance documentation, and payment acceptance in 33+ currencies from 180+ countries.

- Choose based on business needs: Your optimal method depends on transaction volume, customer preferences, and required features like recurring payments.

What does it mean to accept international payments in India?

Accepting international payments in India refers to receiving funds from customers, clients, businesses, or individuals outside India, typically in foreign currencies such as USD, EUR, or GBP. These transactions involve cross-border fund transfers and require currency conversion, compliance, and proper documentation.

For instance, if you're a software developer in India billing a client in New York for a project, you're accepting an international payment. The process involves the client's payment traveling through banking networks, currency conversion, compliance checks, and finally settlement in your Indian bank account.

What are the top benefits of accepting international payments?

Accepting international payments opens significant opportunities for Indian businesses across all sectors. These benefits extend beyond just revenue growth to include competitive advantages and market expansion.

- Higher revenue potential: Foreign currencies typically convert to more INR, giving you better margins.

- Expanded market reach: Access global customers without establishing a physical presence in international markets, reducing expansion costs and complexity.

- Improved cash flow diversity: Reduce dependence on domestic market fluctuations by diversifying revenue sources across multiple countries and currencies.

- Enhanced business credibility: International payment acceptance signals professionalism and reliability to global clients, improving your competitive position.

- Future-proof business growth: Build a scalable payment infrastructure that supports expansion as your business grows into new markets.

How to accept international payments in India?

Indian businesses have several options for accepting international payments, each with distinct advantages and limitations:

Let’s take a detailed look at each method and see how they work.

1.Bank wire transfers (SWIFT)

Traditional bank-to-bank transfers using the SWIFT network remain the most established method for international payments. Your client initiates a wire transfer through their bank, and the funds pass through intermediary banks before reaching your Indian account after conversion to the local currency.

For instance, when a US client sends $10,000 via SWIFT, the money travels from their bank to a correspondent bank, then to your Indian bank, with each institution potentially deducting fees along the way. Processing typically takes 3-7 business days.

2. Payment gateways and processors

Modern payment gateways like PayGlocal , Razorpay, and Stripe allow businesses to accept international card payments and alternative payment methods. These platforms handle currency conversion automatically and provide faster settlement than traditional banking.

For example, an e-commerce store using international payment gateways can accept payments in 100+ currencies, with automatic conversion to INR and settlement within 2-3 days.

3. Virtual international accounts

Virtual accounts provide local bank details in major currencies (USD, EUR, GBP) without opening physical overseas accounts. Clients can make local transfers, which are faster and cheaper than international wires.

Consider a freelance marketing consultant using virtual accounts. They get USD account details to share with American clients, who can then send payments as domestic US transfers, arriving faster and with lower fees.

4. Digital wallets and money transfer services

Services like PayGlocal , PayPal, Wise, and Payoneer offer quick setup and familiar interfaces for international clients. While convenient, they often carry higher fees and less favorable exchange rates compared to dedicated business solutions.

How to set up an international payment acceptance system in India?

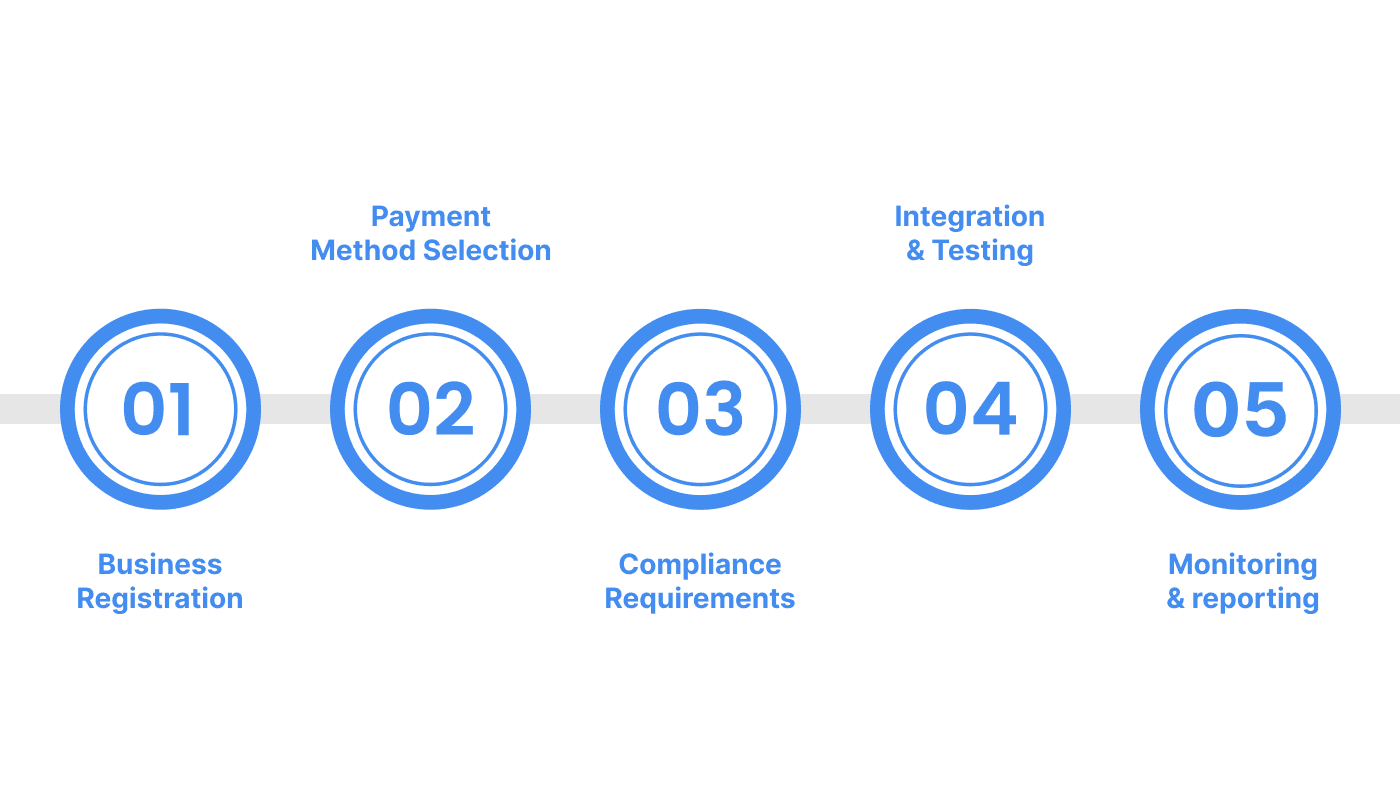

Setting up an international payment acceptance system involves several key steps to ensure compliance and optimal functionality.

1.Business registration and documentation: Ensure your business has all necessary documentation, such as GSTIN, and a current bank account in your business name. For physical goods exports, obtain an Importer Exporter Code (IEC) from the Director General of Foreign Trade (DGFT).

2. Choose your payment method and provider:Evaluate providers based on your business needs, such as transaction volume, customer locations, required features, and cost structure. Consider whether you need recurring payment capabilities, multi-currency settlement, or specific integrations.

3. Complete compliance requirements: Every international payment requires an RBI purpose code (like P0802 for software services or P1002 for trade services) and proper invoicing. Your payment provider should help automate this compliance documentation.

4. Integration and testing: Whether using payment buttons, hosted checkout pages, or API integration, thoroughly test the payment flow with small amounts before going live with customers.

5. Set up monitoring and reporting: Establish processes to track payment status, manage foreign exchange exposure, and maintain compliance records for tax and audit purposes.

What are the costs involved in accepting international payments?

International payment costs vary significantly between providers and methods. You need to consider all fees and charges to calculate your actual receiving amount.

- Bank wire transfers: $15-50 fixed fee plus 2-4% in total charges, including currency conversion.

- Payment gateways: 3-3.5% per transaction with automatic currency conversion included.

- Virtual accounts: 0.75-1.5% flat fee with competitive exchange rates.

- Digital wallets: 4-6% total cost, including transaction and conversion fees.

- Exchange rate markups: Most providers add 1-4% above mid-market rates, significantly impacting large transactions.

For instance, a $10,000 payment could cost you anywhere from $150 to $60,0 depending on your chosen method, making provider selection crucial for your profitability.

Get paid globally without all the hassle with PayGlocal

While traditional options have served Indian businesses for years, they often come with high costs, slow processing, and complex compliance requirements. Modern businesses need payment solutions that match their growth ambitions.

PayGlocal enhances international payment acceptance by combining the reliability of traditional banking with the speed and transparency of modern fintech. Whether you're a startup receiving your first international payment or an enterprise managing thousands of transactions, PayGlocal scales with your needs.

- Collect in 33+ currencies: Accept payments from 180+ countries with local account details in USD, GBP, EUR, and CAD.

- Global payment methods: Support cards, bank transfers, and local payment options that your international customers prefer.

- [Dynamic checkout experience](https://payglocal.in/dynamic-checkout: Provide localized payment flows that increase conversion rates and customer trust.

- No fixed costs: Pay only when you transact, with no setup fees, monthly charges, or documentation costs.

- Clear fee structure: 0.75% for multi-currency accounts, 3.5% for international cards, with no hidden markups or surprise charges.

- Instant FIRA generation: Receive compliance certificates automatically after each settlement, directly in your inbox.

Whether you're scaling a SaaS platform across multiple countries or managing e-commerce operations with global customers, PayGlocal provides the payment infrastructure you need to grow confidently and efficiently.

Final Thoughts

Accepting international payments in India has evolved from a complex, expensive process to an efficient business capability. The key is choosing the right method for your specific needs, considering costs, speed, compliance requirements, and customer preferences.

While multiple options exist, platforms like PayGlocal combine competitive pricing, fast settlement, automated compliance, and an excellent customer experience.

Ready to accept international payments and scale globally? PayGlocal offers everything you need to collect globally, settle locally, and grow without limits. Get started with PayGlocal today and see how easy international payments can be.