Inward remittances to India are expected to grow from $124 billion in 2024 to $129 billion in 2025, reflecting a 4% annual increase. With this growth, knowing the tax implications has never been more important.

Whether foreign remittances are taxable in India depends on several factors, like your residential status, the purpose of the remittance, and whether you're sending or receiving money. Some remittances are completely tax-free, while others attract Tax Collected at Source (TCS) or may be taxable as income.

In this guide, we break down everything you need to know about foreign remittance tax in India. Find out more about TCS rates, inward remittance rules, tax exemptions, and how to stay compliant with proper documentation.

Faster global payments: PayGlocal helps you collect international payments seamlessly with instant compliance documents like FIRC, transparent tracking, and zero fixed costs.

Foreign remittance taxation in India depends on whether you're receiving money (inward remittance) or sending money abroad (outward remittance), your residential status, and the nature of the funds.

For resident Indians receiving money from abroad, the tax treatment varies based on the purpose. If the remittance is a gift from a relative like your parents, spouse, or siblings, it's completely tax-free regardless of the amount.

However, if you receive a gift from a non-relative and the total value exceeds ₹50,000 in a financial year, the entire amount becomes taxable as income from other sources.

If the money you receive represents income like salary, freelance earnings, or consultancy fees, it is taxable in India. For instance, if you're a resident Indian working remotely for a US company and receiving your salary in India, that income is taxable. The same applies to freelancers receiving payments from overseas clients.

For outward remittances, when you send money abroad under the Liberalized Remittance Scheme (LRS), Tax Collected at Source (TCS) applies on amounts exceeding ₹10 lakh per financial year. The TCS rate varies from 5% to 20% depending on the purpose of the transfer.

NRIs sending money to India from their foreign earnings are not taxed on these remittances since the funds come from tax-paid sources in their country of residence.

TCS stands for Tax Collected at Source. It's an advance tax collected by authorized dealers like banks when you remit money abroad under the Liberalized Remittance Scheme (LRS). This is not a final tax but can be adjusted against your total tax liability when you file your income tax return.

TCS rates depend on the purpose of your remittance and the amount transferred. For education expenses funded by yourself, no TCS applies on amounts up to ₹10 lakh per financial year. A 5% TCS applies on amounts exceeding ₹10 lakh.

If your education is funded by a loan from a specified financial institution, no TCS is charged regardless of the amount. This is a significant exemption introduced in April 2025.

For medical treatment abroad, no TCS applies to amounts up to ₹10 lakh. A 5% TCS is collected on amounts above ₹10 lakh. For overseas tour packages, a 5% TCS is charged on amounts up to ₹10 lakh, and 20% TCS applies to the amounts above ₹10 lakh.

For other purposes like buying property abroad or investing in foreign assets, no TCS is collected on amounts up to ₹10 lakh. A 20% TCS applies to amounts above ₹10 lakh.

Note: The TCS collected is not an additional cost. You can claim credit for this amount when filing your income tax return, and if your total tax liability is less than the TCS collected, you'll receive a refund.

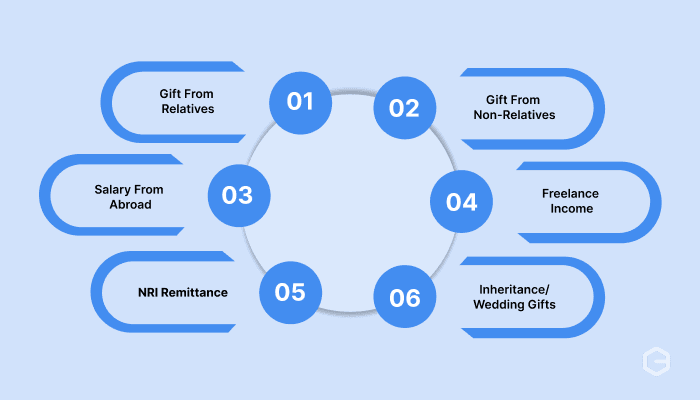

Inward remittances refer to money received in India from abroad. The tax treatment depends on whether you're a resident Indian or an NRI, and the nature of the remittance.

Here's how different types of inward remittances are taxed:

Let's look at each category in detail so that you can know your tax obligations.

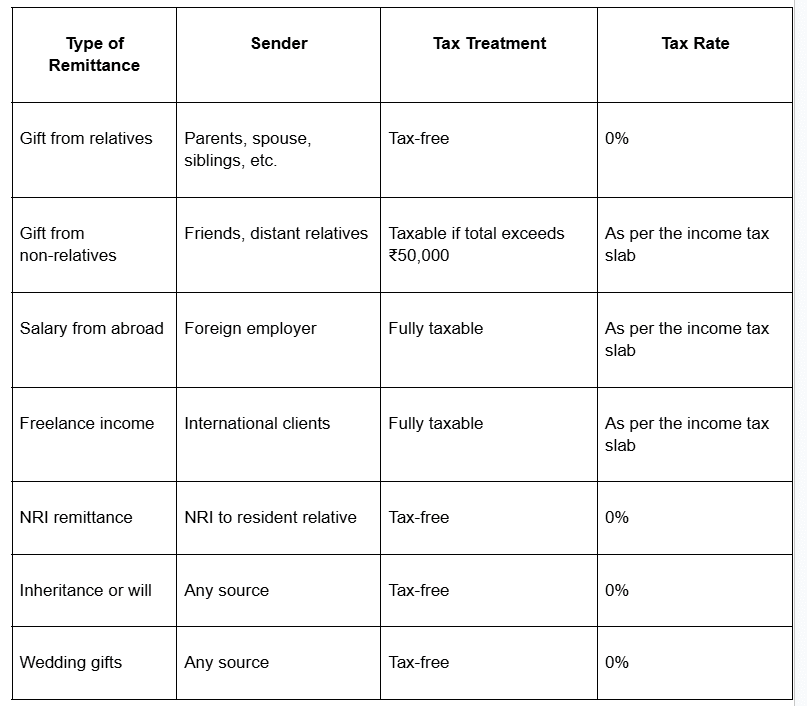

Gifts received from relatives defined under the Income Tax Act are completely tax-exempt regardless of the amount. Relatives include your spouse, parents, siblings, spouse's parents, and lineal ascendants or descendants.

Gifts from non-relatives are tax-free only if the total value received in a financial year is below ₹50,000. If the aggregate value exceeds ₹50,000, the entire amount is taxed as income from other sources at your applicable income tax slab rate.

Gifts received on occasions like your wedding, through a will or inheritance, or in contemplation of death are tax-exempt regardless of the sender.

Any foreign remittance that represents income earned abroad is taxable. This includes salary for services provided in India but paid from abroad, fees for consultancy or technical services, freelance earnings from international clients, interest from foreign bank accounts, and capital gains from the sale of foreign assets.

If you already paid tax on this income in the country where it was earned, you can claim relief under India's Double Taxation Avoidance Agreement (DTAA) if one exists between India and that country. You'll need to provide proof of foreign tax paid to claim this benefit.

NRIs are not taxed in India on remittances they send from their foreign earnings. The money transferred comes from tax-paid sources in their country of residence. Interest earned on NRE (Non-Resident External) accounts is tax-exempt in India, while interest on NRO (Non-Resident Ordinary) accounts is taxable.

There is no upper limit on how much you can receive as an inward remittance in India, but you must maintain proper documentation for amounts received to ensure compliance and avoid scrutiny.

In India, there’s no maximum limit on receiving foreign remittances, especially for personal transfers. You can receive any amount from abroad as long as the transaction is legitimate and properly documented.

Banks offer direct transfers for any amount, while services like Western Union or MoneyGram, under MTSS (Money Transfer Service Scheme) work well for smaller, quick transfers. However, these MTSS transfers let you receive up to 30 payments per year, with each transaction capped at USD 2,500. This channel suits personal needs like family support, but won't work for business payments or investments.

For business or trade payments, the RDA (Rupee Drawing Arrangement) lets you receive larger amounts. Personal transfers through this method have no upper limit, while trade-related payments do have a limit of up to ₹15 lakh per transaction. Your bank will need specific details about why you're receiving the money, as FEMA (Foreign Exchange Management Act) requires proper documentation for all transfers.

Banks require additional documentation, like purpose codes, proof of relationship for gifts, or invoices for business payments for larger amounts.

All inward remittances must be reported by banks to the tax authorities. If you receive large sums that appear inconsistent with your known sources of income, you may receive inquiries from tax authorities asking you to explain the source and nature of the funds.

For gifts exceeding ₹50,000 from non-relatives, you must report them in your income tax return and pay applicable taxes. For income received from abroad, it is important to declare it in your income tax return even if no tax was deducted at source.

While you cannot avoid legitimate tax obligations, you can optimize your tax liability through proper planning and taking advantage of available exemptions.

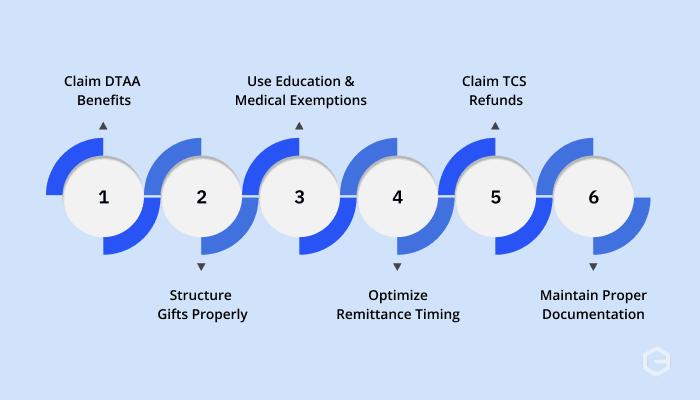

Here are effective ways to reduce your tax burden on foreign remittances:

Claim DTAA benefits: If you paid tax on foreign income in another country, claim credit for foreign taxes paid under India's Double Taxation Avoidance Agreement. This prevents you from paying tax twice on the same income. You'll need to obtain a Tax Residency Certificate from the foreign country and Form 67 when filing your Indian tax return.

Structure gifts properly: If you're receiving gifts from abroad, ensure they come from defined relatives to enjoy complete tax exemption. If receiving from non-relatives, consider timing multiple gifts across different financial years to stay within the ₹50,000 annual exemption limit.

Use education and medical exemptions: When sending money abroad for education or medical treatment, take advantage of lower or zero TCS rates by providing proper documentation to your bank. For education funded by loans from specified financial institutions, no TCS applies regardless of the amount.

Optimize remittance timing: If you need to send more than ₹10 lakh abroad for purposes other than education or medical treatment, consider spreading the remittance across different financial years to benefit from the ₹10 lakh threshold each year where no TCS applies.

Claim TCS refunds: Remember that TCS is not a final tax. When filing your income tax return, claim credit for TCS collected on your foreign remittances. If your actual tax liability is lower than the TCS paid, you'll receive a refund.

Maintain documentation: Proper documentation helps you claim all eligible exemptions and avoid unnecessary scrutiny. Keep records of FIRCs, invoices, contracts, and proof of foreign taxes paid.

Proper documentation ensures smooth processing of foreign remittances and helps you stay compliant with tax and regulatory requirements.

Here's what you need for different types of remittances:

FIRC or FIRA: Foreign Inward Remittance Certificate or Advice issued by your bank confirming receipt of foreign funds. This document is essential for income tax filing, GST claims, and export incentives.

Purpose documentation: Invoices for business payments, gift deeds for large gifts from non-relatives, or employment contracts for salary payments.

Proof of relationship: For gifts from relatives, maintain documents proving the relationship, like birth certificates, marriage certificates, or family tree documentation.

Tax payment proof: If you paid tax on the income abroad, obtain proof of foreign tax payment and a Tax Residency Certificate to claim DTAA benefits.

Purpose code declaration: Form A2 declaring the purpose of remittance as per RBI guidelines.

PAN card: Mandatory for all remittances under LRS.

Supporting documents: Invoices for business payments, admission letters for education, medical certificates for treatment, property documents for real estate purchases, or investment documents for financial assets.

TCS certificate: Form 27D issued by your bank showing TCS collected, which you'll need when filing your income tax return.

Export invoices: Commercial invoices detailing goods or services exported.

Shipping documents: Bill of lading, airway bills, or courier receipts for goods exports.

Service contracts: Agreements with foreign clients for service exports.

Bank certificates: Statements showing receipt of foreign funds and currency conversion details.

Managing foreign remittances and staying compliant with tax regulations can feel overwhelming, especially when you're trying to grow your business across borders. Between tracking payments, generating compliance documents, and dealing with hidden charges from traditional banks, the process often becomes a bottleneck.

PayGlocal simplifies international payment collection for freelancers, exporters, and businesses of all sizes. You get a complete solution that handles payments, compliance, and tracking in one place.

Here's how PayGlocal helps:

Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD.

Instant compliance documents: Receive Foreign Inward Remittance Certificates (FIRC) directly in your inbox after settlement, ensuring you have all necessary documentation for tax filing and audits.

Transparent tracking: Monitor your payment status at every step with real-time notifications and a comprehensive dashboard.

Zero fixed costs: Pay only when you transact with transparent pricing and no hidden charges, setup fees, or monthly commitments.

Complete payment suite: Accept payments through cards, global payment methods, recurring billing, and payment links from a single platform.

Whether you're a freelancer receiving payments from international clients, an exporter managing marketplace settlements, or a SaaS business collecting subscriptions globally, PayGlocal gives you the tools to collect payments faster and stay compliant effortlessly.

Foreign remittance taxation in India depends on multiple factors, including your residential status, the nature of the funds, and whether you're sending or receiving money. While inward remittances as gifts from relatives are tax-free, gifts from non-relatives above ₹50,000 and income earned abroad are taxable for resident Indians.

For outward remittances, TCS applies under the Liberalized Remittance Scheme with rates varying based on purpose and amount. The threshold increased to ₹10 lakh in April 2025, and education remittances funded by loans from specified institutions now attract zero TCS regardless of amount. Remember that TCS is not a final tax and can be claimed as a credit when filing your income tax return.

If you're collecting payments from overseas clients or managing international transactions regularly, having the right payment partner makes a big difference. PayGlocal handles documentation, provides instant FIRC, and gives you complete visibility over your international money transfers. Get started with PayGlocal today and grow your business globally.

Whether foreign remittances are taxable in India depends on several factors, like your residential status, the purpose of the remittance, and whether you're sending or receiving money. Some remittances are completely tax-free, while others attract Tax Collected at Source (TCS) or may be taxable as income.

In this guide, we break down everything you need to know about foreign remittance tax in India. Find out more about TCS rates, inward remittance rules, tax exemptions, and how to stay compliant with proper documentation.

Key Takeaways

- Tax on inward remittances: Money received from abroad as a gift from relatives is tax-free, but gifts from non-relatives above ₹50,000 are taxable as income.

- Income from abroad is taxable: Salary, freelance earnings, or consultancy fees earned overseas are taxable for resident Indians, even if already taxed abroad.

- TCS applies to outward remittances: When you send money abroad under the Liberalized Remittance Scheme (LRS), TCS rates range from 0% to 20% depending on the purpose and amount, with no TCS on amounts up to ₹10 lakh.

- NRIs are not taxed on remittances to India: Money sent by NRIs from their foreign earnings is not taxable in India as it comes from tax-paid sources.

Faster global payments: PayGlocal helps you collect international payments seamlessly with instant compliance documents like FIRC, transparent tracking, and zero fixed costs.

Is foreign remittance taxable in India?

Foreign remittance taxation in India depends on whether you're receiving money (inward remittance) or sending money abroad (outward remittance), your residential status, and the nature of the funds.

For resident Indians receiving money from abroad, the tax treatment varies based on the purpose. If the remittance is a gift from a relative like your parents, spouse, or siblings, it's completely tax-free regardless of the amount.

However, if you receive a gift from a non-relative and the total value exceeds ₹50,000 in a financial year, the entire amount becomes taxable as income from other sources.

If the money you receive represents income like salary, freelance earnings, or consultancy fees, it is taxable in India. For instance, if you're a resident Indian working remotely for a US company and receiving your salary in India, that income is taxable. The same applies to freelancers receiving payments from overseas clients.

For outward remittances, when you send money abroad under the Liberalized Remittance Scheme (LRS), Tax Collected at Source (TCS) applies on amounts exceeding ₹10 lakh per financial year. The TCS rate varies from 5% to 20% depending on the purpose of the transfer.

NRIs sending money to India from their foreign earnings are not taxed on these remittances since the funds come from tax-paid sources in their country of residence.

What is TCS on foreign remittance?

TCS stands for Tax Collected at Source. It's an advance tax collected by authorized dealers like banks when you remit money abroad under the Liberalized Remittance Scheme (LRS). This is not a final tax but can be adjusted against your total tax liability when you file your income tax return.

TCS rates depend on the purpose of your remittance and the amount transferred. For education expenses funded by yourself, no TCS applies on amounts up to ₹10 lakh per financial year. A 5% TCS applies on amounts exceeding ₹10 lakh.

If your education is funded by a loan from a specified financial institution, no TCS is charged regardless of the amount. This is a significant exemption introduced in April 2025.

For medical treatment abroad, no TCS applies to amounts up to ₹10 lakh. A 5% TCS is collected on amounts above ₹10 lakh. For overseas tour packages, a 5% TCS is charged on amounts up to ₹10 lakh, and 20% TCS applies to the amounts above ₹10 lakh.

For other purposes like buying property abroad or investing in foreign assets, no TCS is collected on amounts up to ₹10 lakh. A 20% TCS applies to amounts above ₹10 lakh.

Note: The TCS collected is not an additional cost. You can claim credit for this amount when filing your income tax return, and if your total tax liability is less than the TCS collected, you'll receive a refund.

How are inward remittances taxed in India?

Inward remittances refer to money received in India from abroad. The tax treatment depends on whether you're a resident Indian or an NRI, and the nature of the remittance.

Here's how different types of inward remittances are taxed:

Let's look at each category in detail so that you can know your tax obligations.

For resident Indians receiving gifts

Gifts received from relatives defined under the Income Tax Act are completely tax-exempt regardless of the amount. Relatives include your spouse, parents, siblings, spouse's parents, and lineal ascendants or descendants.

Gifts from non-relatives are tax-free only if the total value received in a financial year is below ₹50,000. If the aggregate value exceeds ₹50,000, the entire amount is taxed as income from other sources at your applicable income tax slab rate.

Gifts received on occasions like your wedding, through a will or inheritance, or in contemplation of death are tax-exempt regardless of the sender.

For resident Indians receiving income

Any foreign remittance that represents income earned abroad is taxable. This includes salary for services provided in India but paid from abroad, fees for consultancy or technical services, freelance earnings from international clients, interest from foreign bank accounts, and capital gains from the sale of foreign assets.

If you already paid tax on this income in the country where it was earned, you can claim relief under India's Double Taxation Avoidance Agreement (DTAA) if one exists between India and that country. You'll need to provide proof of foreign tax paid to claim this benefit.

For NRIs

NRIs are not taxed in India on remittances they send from their foreign earnings. The money transferred comes from tax-paid sources in their country of residence. Interest earned on NRE (Non-Resident External) accounts is tax-exempt in India, while interest on NRO (Non-Resident Ordinary) accounts is taxable.

There is no upper limit on how much you can receive as an inward remittance in India, but you must maintain proper documentation for amounts received to ensure compliance and avoid scrutiny.

What are the inward remittance limits in India?

In India, there’s no maximum limit on receiving foreign remittances, especially for personal transfers. You can receive any amount from abroad as long as the transaction is legitimate and properly documented.

Banks offer direct transfers for any amount, while services like Western Union or MoneyGram, under MTSS (Money Transfer Service Scheme) work well for smaller, quick transfers. However, these MTSS transfers let you receive up to 30 payments per year, with each transaction capped at USD 2,500. This channel suits personal needs like family support, but won't work for business payments or investments.

For business or trade payments, the RDA (Rupee Drawing Arrangement) lets you receive larger amounts. Personal transfers through this method have no upper limit, while trade-related payments do have a limit of up to ₹15 lakh per transaction. Your bank will need specific details about why you're receiving the money, as FEMA (Foreign Exchange Management Act) requires proper documentation for all transfers.

Banks require additional documentation, like purpose codes, proof of relationship for gifts, or invoices for business payments for larger amounts.

All inward remittances must be reported by banks to the tax authorities. If you receive large sums that appear inconsistent with your known sources of income, you may receive inquiries from tax authorities asking you to explain the source and nature of the funds.

For gifts exceeding ₹50,000 from non-relatives, you must report them in your income tax return and pay applicable taxes. For income received from abroad, it is important to declare it in your income tax return even if no tax was deducted at source.

How can you save tax on foreign remittances?

While you cannot avoid legitimate tax obligations, you can optimize your tax liability through proper planning and taking advantage of available exemptions.

Here are effective ways to reduce your tax burden on foreign remittances:

Claim DTAA benefits: If you paid tax on foreign income in another country, claim credit for foreign taxes paid under India's Double Taxation Avoidance Agreement. This prevents you from paying tax twice on the same income. You'll need to obtain a Tax Residency Certificate from the foreign country and Form 67 when filing your Indian tax return.

Structure gifts properly: If you're receiving gifts from abroad, ensure they come from defined relatives to enjoy complete tax exemption. If receiving from non-relatives, consider timing multiple gifts across different financial years to stay within the ₹50,000 annual exemption limit.

Use education and medical exemptions: When sending money abroad for education or medical treatment, take advantage of lower or zero TCS rates by providing proper documentation to your bank. For education funded by loans from specified financial institutions, no TCS applies regardless of the amount.

Optimize remittance timing: If you need to send more than ₹10 lakh abroad for purposes other than education or medical treatment, consider spreading the remittance across different financial years to benefit from the ₹10 lakh threshold each year where no TCS applies.

Claim TCS refunds: Remember that TCS is not a final tax. When filing your income tax return, claim credit for TCS collected on your foreign remittances. If your actual tax liability is lower than the TCS paid, you'll receive a refund.

Maintain documentation: Proper documentation helps you claim all eligible exemptions and avoid unnecessary scrutiny. Keep records of FIRCs, invoices, contracts, and proof of foreign taxes paid.

What documents do you need for foreign remittance compliance?

Proper documentation ensures smooth processing of foreign remittances and helps you stay compliant with tax and regulatory requirements.

Here's what you need for different types of remittances:

For receiving money from abroad (inward remittance):

FIRC or FIRA: Foreign Inward Remittance Certificate or Advice issued by your bank confirming receipt of foreign funds. This document is essential for income tax filing, GST claims, and export incentives.

Purpose documentation: Invoices for business payments, gift deeds for large gifts from non-relatives, or employment contracts for salary payments.

Proof of relationship: For gifts from relatives, maintain documents proving the relationship, like birth certificates, marriage certificates, or family tree documentation.

Tax payment proof: If you paid tax on the income abroad, obtain proof of foreign tax payment and a Tax Residency Certificate to claim DTAA benefits.

For sending money abroad (outward remittance):

Purpose code declaration: Form A2 declaring the purpose of remittance as per RBI guidelines.

PAN card: Mandatory for all remittances under LRS.

Supporting documents: Invoices for business payments, admission letters for education, medical certificates for treatment, property documents for real estate purchases, or investment documents for financial assets.

TCS certificate: Form 27D issued by your bank showing TCS collected, which you'll need when filing your income tax return.

For businesses collecting international payments:

Export invoices: Commercial invoices detailing goods or services exported.

Shipping documents: Bill of lading, airway bills, or courier receipts for goods exports.

Service contracts: Agreements with foreign clients for service exports.

Bank certificates: Statements showing receipt of foreign funds and currency conversion details.

Get paid globally faster with instant FIRC using PayGlocal

Managing foreign remittances and staying compliant with tax regulations can feel overwhelming, especially when you're trying to grow your business across borders. Between tracking payments, generating compliance documents, and dealing with hidden charges from traditional banks, the process often becomes a bottleneck.

PayGlocal simplifies international payment collection for freelancers, exporters, and businesses of all sizes. You get a complete solution that handles payments, compliance, and tracking in one place.

Here's how PayGlocal helps:

Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD.

Instant compliance documents: Receive Foreign Inward Remittance Certificates (FIRC) directly in your inbox after settlement, ensuring you have all necessary documentation for tax filing and audits.

Transparent tracking: Monitor your payment status at every step with real-time notifications and a comprehensive dashboard.

Zero fixed costs: Pay only when you transact with transparent pricing and no hidden charges, setup fees, or monthly commitments.

Complete payment suite: Accept payments through cards, global payment methods, recurring billing, and payment links from a single platform.

Whether you're a freelancer receiving payments from international clients, an exporter managing marketplace settlements, or a SaaS business collecting subscriptions globally, PayGlocal gives you the tools to collect payments faster and stay compliant effortlessly.

Final Thoughts

Foreign remittance taxation in India depends on multiple factors, including your residential status, the nature of the funds, and whether you're sending or receiving money. While inward remittances as gifts from relatives are tax-free, gifts from non-relatives above ₹50,000 and income earned abroad are taxable for resident Indians.

For outward remittances, TCS applies under the Liberalized Remittance Scheme with rates varying based on purpose and amount. The threshold increased to ₹10 lakh in April 2025, and education remittances funded by loans from specified institutions now attract zero TCS regardless of amount. Remember that TCS is not a final tax and can be claimed as a credit when filing your income tax return.

If you're collecting payments from overseas clients or managing international transactions regularly, having the right payment partner makes a big difference. PayGlocal handles documentation, provides instant FIRC, and gives you complete visibility over your international money transfers. Get started with PayGlocal today and grow your business globally.