You've heard the term LLP. Maybe your accountant mentioned it, or you saw it while researching business structures. But what does an LLP company actually mean?

An LLP (Limited Liability Partnership) is suitable for professionals running service businesses. As India's services sector grows to drive 55% of the economy, consultants, accountants, designers, and agencies are building bigger businesses that need proper protection. That’s where LLPs come in.

In this guide, we break down what LLP means, how it works, and who should choose it. We'll also cover how the right payment infrastructure can help your LLP collect money from global clients.

LLP stands for Limited Liability Partnership. It's a business structure that mixes features from both partnerships and companies to give you flexibility without excessive personal risk.

In a traditional partnership, if your business faces a lawsuit or debt, your personal assets, like your house or savings, can be claimed. In an LLP, that doesn't happen. Your liability is limited to what you've invested in the business. The LLP itself is a separate legal entity, which means it can own property, enter contracts, and be sued in its own name.

For example, if you run a digital marketing agency as an LLP with two partners, and the business owes money to a vendor, only the LLP's assets are at risk.

Your personal bank account stays protected. This is what makes LLP attractive for professionals like consultants, software developers, and chartered accountants who want to work together without risking everything they own.

An LLP comes with specific characteristics that make it different from other business structures. Here are the main features you need to know:

These features make LLP a practical choice when you want professional operations without the heavy compliance load of a private limited company.

LLPs offer clear advantages, especially for service-based businesses and professionals who work with multiple clients or partners. Here's why businesses choose LLP:

_ Personal asset protection: Your home, car, and savings stay separate from business liabilities. This protection matters when you're taking on projects with financial risk.

For instance, a software development firm working with clients in the US and Europe can operate as an LLP, protect partners from client disputes, and still maintain flexibility in how they run projects.

An LLP operates through a formal agreement between partners and follows defined legal processes for formation and management.

You start by filing incorporation documents with the Ministry of Corporate Affairs. The process requires a designated partner (at least one must be an Indian resident), a unique name, and a registered office address. Once approved, you get a Limited Liability Partnership Identification Number (LLPIN) and can start operations.

Partners contribute capital as agreed and share profits based on the LLP agreement. This agreement is a crucial document that outlines each partner's role, profit distribution, decision-making authority, and exit procedures. Unlike companies with rigid structures, you have freedom to customize these terms.

For example, in a content marketing LLP with three partners, one might handle client relationships, another manages content creation, and the third oversees finance. They could agree to split profits 40-30-30 based on contribution rather than equal shares.

The LLP files annual returns and maintains basic accounting records. If turnover exceeds Rs 40 lakhs or contribution exceeds Rs 25 lakhs, you need a statutory audit. Tax is paid by individual partners on their profit share, not by the LLP itself.

Day-to-day management happens as partners decide. There's no requirement for board meetings or shareholder approvals. When you need to add a partner, you update the LLP agreement and file the necessary forms with the registrar.

This flexibility makes LLPs work well for businesses that need to adapt quickly. A design agency can bring in a specialist partner for a major project without restructuring the entire entity. The legal protection stays intact while operations remain agile.

Choosing the right structure means knowing how LLP compares to partnerships, private limited companies, and sole proprietorships. Here's how they compare:

The partnership firm works when you want minimal paperwork and plan to stay small. For instance, two friends running a local consulting practice might start as a partnership. But if they plan to scale or work with corporate clients, the unlimited liability becomes a problem.

Private limited companies suit businesses raising venture funding or planning an eventual exit. The structure supports equity distribution, employee stock options, and investor protections. A tech startup building a product would typically choose this route.

LLP fits service businesses, professional practices, and companies exporting knowledge work. For example, a team of chartered accountants serving clients in India and abroad would benefit from LLP's liability protection and operational flexibility without the compliance burden of a company.

If you're a freelancer or consultant working alone, a sole proprietorship keeps things simple until you're ready to bring in partners or formalize operations.

Certain types of businesses and professionals get the most value from an LLP structure.

LLP works best for:

For instance, a consulting firm with partners in Mumbai, Bangalore, and Delhi can operate as an LLP. Each partner handles clients in their region, shares profits based on contribution, and stays protected from liability if one partner faces a client dispute.

Getting your LLP registered requires specific documents from each partner and details about the business. Here's what you need to prepare:

For example, if you're setting up a digital marketing LLP with two partners, you'd need both partners' identity and address proofs, a rental agreement for your office space, DSCs for filing, and a clear LLP agreement defining who handles what.

Operating an LLP that serves global clients means dealing with cross-border payments, currency conversion, and compliance documentation. Traditional banking channels make this harder than it needs to be.

Opening foreign currency accounts with regular banks involves extensive paperwork, long approval times, and high transaction fees. SWIFT transfers take days to arrive, with multiple intermediaries taking cuts along the way. You lose money on unfavorable exchange rates and struggle to track where payments are in the process.

PayGlocal solves these problems by giving LLPs a complete international payment stack built for service exporters. Here's what you get:

LLPs need speed, transparency, and compliance without the complexity. With PayGlocal, you get local accounts in major currencies, competitive conversion rates, and real-time tracking. The platform handles the technical complexity of international payments while you focus on serving clients and growing your practice.

LLP offers liability protection, operational flexibility, and manageable compliance. For professionals and service businesses, especially those working with international clients, it's often the right choice.

Before registering, talk to a chartered accountant about tax implications for your specific situation. Make sure your LLP agreement clearly defines partner roles, profit sharing, and exit procedures. These foundations matter as your business grows.

If your LLP serves global clients, don't let payment complications slow you down. The right payment infrastructure means faster collections, better tracking, and easier compliance.

Get started with PayGlocal today. Collect from clients worldwide, settle in INR, and spend less time chasing payments.

An LLP (Limited Liability Partnership) is suitable for professionals running service businesses. As India's services sector grows to drive 55% of the economy, consultants, accountants, designers, and agencies are building bigger businesses that need proper protection. That’s where LLPs come in.

In this guide, we break down what LLP means, how it works, and who should choose it. We'll also cover how the right payment infrastructure can help your LLP collect money from global clients.

Key takeaways

- Partnership flexibility with built-in protection: Your personal assets stay safe from business debts while you keep operational freedom.

- Minimum two partners, no maximum: You need at least two people to start, but you can add as many partners as needed.

- Lower compliance than private companies: Fewer forms to file, no mandatory audit for smaller operations, simpler annual requirements.

- Built for professionals and service businesses: Accountants, consultants, and service exporters commonly choose this structure.

- International payments made simple: PayGlocal helps LLPs collect from global clients in multiple currencies and settle in INR.

What does LLP company mean?

LLP stands for Limited Liability Partnership. It's a business structure that mixes features from both partnerships and companies to give you flexibility without excessive personal risk.

In a traditional partnership, if your business faces a lawsuit or debt, your personal assets, like your house or savings, can be claimed. In an LLP, that doesn't happen. Your liability is limited to what you've invested in the business. The LLP itself is a separate legal entity, which means it can own property, enter contracts, and be sued in its own name.

For example, if you run a digital marketing agency as an LLP with two partners, and the business owes money to a vendor, only the LLP's assets are at risk.

Your personal bank account stays protected. This is what makes LLP attractive for professionals like consultants, software developers, and chartered accountants who want to work together without risking everything they own.

What are the key features of an LLP?

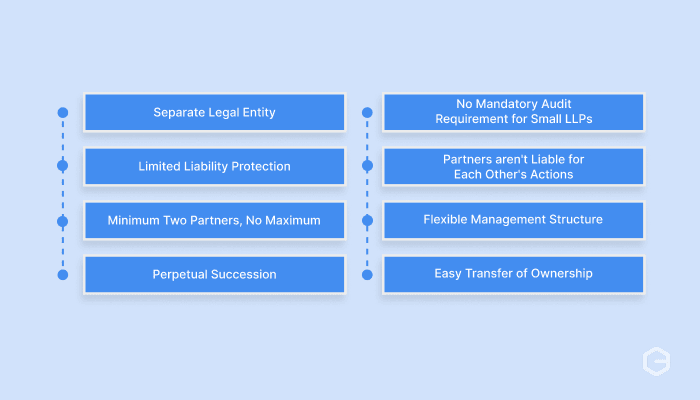

An LLP comes with specific characteristics that make it different from other business structures. Here are the main features you need to know:

- Separate legal entity: The LLP exists independently from its partners. It can own assets, sign contracts, and handle legal matters in its own name. This separation means business operations continue smoothly even when partners change.

- Limited liability protection: Your personal liability is restricted to your capital contribution. If the LLP faces financial trouble or legal action, creditors can't come after your personal savings or property.

- Minimum two partners, no maximum: You need at least two partners to start an LLP. There's no upper limit, so you can add partners as your business grows without restructuring.

- Perpetual succession: The LLP doesn't dissolve when a partner exits or passes away. The business continues operating, which gives stability to clients and employees.

- No mandatory audit requirement for small LLPs: If your annual turnover is below Rs 40 lakhs or capital contribution is below Rs 25 lakhs, you don't need a statutory audit. This reduces compliance costs.

- Partners aren't liable for each other's actions: Unlike traditional partnerships, one partner's misconduct or negligence doesn't make other partners personally liable. You're only responsible for your own actions.

- Flexible management structure: Partners can define roles, profit-sharing, and decision-making processes through an LLP agreement. There's no rigid board structure like in companies.

- Easy transfer of ownership: Partners can transfer their stake based on the terms in the LLP agreement, making it simpler to bring in new partners or exit the business.

These features make LLP a practical choice when you want professional operations without the heavy compliance load of a private limited company.

What are the benefits of choosing an LLP structure?

LLPs offer clear advantages, especially for service-based businesses and professionals who work with multiple clients or partners. Here's why businesses choose LLP:

_ Personal asset protection: Your home, car, and savings stay separate from business liabilities. This protection matters when you're taking on projects with financial risk.

- Lower setup and maintenance costs: Registration costs less than a private limited company. Annual compliance is simpler, which means lower accounting and legal fees.

- Flexibility in operations: You and your partners decide how to split profits, assign responsibilities, and make decisions. There's no mandatory board meeting or shareholder approval process.

- Tax benefits: LLPs don't face dividend distribution tax. Partners are taxed individually on their share of profits, which can work out more favorably depending on your income level.

- Credibility with clients and vendors: The LLP designation signals a formal business structure. International clients often prefer working with registered entities over sole proprietorships.

- Easier compliance compared to companies: No requirement for annual general meetings, fewer forms to file, and simplified record-keeping for smaller operations.

- Perpetual existence: The business doesn't shut down when a partner leaves. This continuity helps when bidding for long-term contracts or building client relationships.

- Suitable for professional services: Ideal for consultants, designers, software developers, accountants, and other knowledge workers who want structure without bureaucracy.

For instance, a software development firm working with clients in the US and Europe can operate as an LLP, protect partners from client disputes, and still maintain flexibility in how they run projects.

How does a Limited Liability Partnership work?

An LLP operates through a formal agreement between partners and follows defined legal processes for formation and management.

You start by filing incorporation documents with the Ministry of Corporate Affairs. The process requires a designated partner (at least one must be an Indian resident), a unique name, and a registered office address. Once approved, you get a Limited Liability Partnership Identification Number (LLPIN) and can start operations.

Partners contribute capital as agreed and share profits based on the LLP agreement. This agreement is a crucial document that outlines each partner's role, profit distribution, decision-making authority, and exit procedures. Unlike companies with rigid structures, you have freedom to customize these terms.

For example, in a content marketing LLP with three partners, one might handle client relationships, another manages content creation, and the third oversees finance. They could agree to split profits 40-30-30 based on contribution rather than equal shares.

The LLP files annual returns and maintains basic accounting records. If turnover exceeds Rs 40 lakhs or contribution exceeds Rs 25 lakhs, you need a statutory audit. Tax is paid by individual partners on their profit share, not by the LLP itself.

Day-to-day management happens as partners decide. There's no requirement for board meetings or shareholder approvals. When you need to add a partner, you update the LLP agreement and file the necessary forms with the registrar.

This flexibility makes LLPs work well for businesses that need to adapt quickly. A design agency can bring in a specialist partner for a major project without restructuring the entire entity. The legal protection stays intact while operations remain agile.

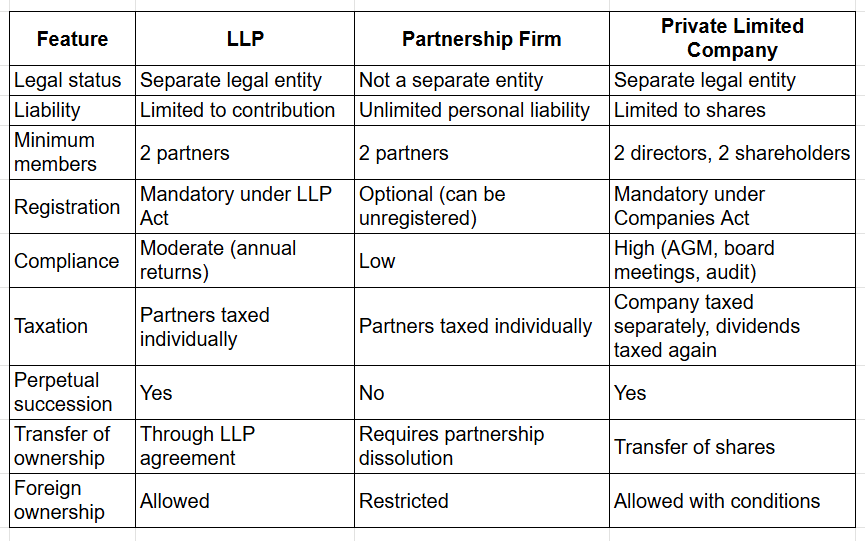

What's the difference between LLP and other business structures?

Choosing the right structure means knowing how LLP compares to partnerships, private limited companies, and sole proprietorships. Here's how they compare:

The partnership firm works when you want minimal paperwork and plan to stay small. For instance, two friends running a local consulting practice might start as a partnership. But if they plan to scale or work with corporate clients, the unlimited liability becomes a problem.

Private limited companies suit businesses raising venture funding or planning an eventual exit. The structure supports equity distribution, employee stock options, and investor protections. A tech startup building a product would typically choose this route.

LLP fits service businesses, professional practices, and companies exporting knowledge work. For example, a team of chartered accountants serving clients in India and abroad would benefit from LLP's liability protection and operational flexibility without the compliance burden of a company.

If you're a freelancer or consultant working alone, a sole proprietorship keeps things simple until you're ready to bring in partners or formalize operations.

Who should choose an LLP structure?

Certain types of businesses and professionals get the most value from an LLP structure.

LLP works best for:

- Professional service providers: Lawyers, chartered accountants, company secretaries, and architects who are required or prefer to operate through LLP rather than companies.

- Consulting firms: Management consultants, IT consultants, and business advisors who work with multiple clients and want liability protection.

- Digital agencies and creative studios: Marketing agencies, design firms, and content creators working with domestic and international clients.

- Software development companies: Development shops and SaaS providers building products or providing services to global markets.

- Export service businesses: BPOs, KPOs, and other service exporters who need a formal structure for international contracts and compliance.

- Small to medium professional partnerships: Groups of 2-10 professionals who want to work together without complex corporate governance.

- Businesses with multiple stakeholders: When you have several partners contributing different skills or capital and need clear agreements on roles and profit-sharing.

For instance, a consulting firm with partners in Mumbai, Bangalore, and Delhi can operate as an LLP. Each partner handles clients in their region, shares profits based on contribution, and stays protected from liability if one partner faces a client dispute.

When LLP might not be ideal:

- You're planning to raise venture capital funding. Investors prefer private limited companies because of the equity structure and exit options. An e-commerce startup looking for seed funding should probably skip LLP.

- You're running a product manufacturing business. LLPs work better for knowledge and service sectors. A company making physical goods typically needs the structure and funding options that come with incorporation as a company.

- You're a solo professional with no plans to add partners. A sole proprietorship or one-person company keeps things simpler until you actually need the partnership features.

What documents do you need for LLP registration?

Getting your LLP registered requires specific documents from each partner and details about the business. Here's what you need to prepare:

- Partner identification: PAN card, Aadhaar card, and passport-size photographs for all partners. At least one designated partner must be an Indian resident.

- Address proof for partners: Recent utility bill, bank statement, or rental agreement showing current residence address.

- Registered office proof: Rent agreement or ownership documents for the business address. You also need a no-objection certificate from the property owner.

- Digital signature certificates: At least one designated partner needs a DSC for filing forms online with the MCA portal.

- Name approval: Proposed names for the LLP (have 2-3 options ready). The name must include "LLP" or "Limited Liability Partnership" and shouldn't conflict with existing businesses.

- LLP agreement draft: Document outlining partner roles, capital contribution, profit sharing, decision-making process, and exit terms.

- Partner consent and declarations: Consent to act as designated partners and declarations confirming eligibility.

For example, if you're setting up a digital marketing LLP with two partners, you'd need both partners' identity and address proofs, a rental agreement for your office space, DSCs for filing, and a clear LLP agreement defining who handles what.

Manage international payments efficiently with PayGlocal

Operating an LLP that serves global clients means dealing with cross-border payments, currency conversion, and compliance documentation. Traditional banking channels make this harder than it needs to be.

Opening foreign currency accounts with regular banks involves extensive paperwork, long approval times, and high transaction fees. SWIFT transfers take days to arrive, with multiple intermediaries taking cuts along the way. You lose money on unfavorable exchange rates and struggle to track where payments are in the process.

PayGlocal solves these problems by giving LLPs a complete international payment stack built for service exporters. Here's what you get:

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD. Give clients local bank details so they can pay you like a domestic vendor.

- Global payment methods: Accept payments through 40+ local payment methods from 180+ countries. Clients pay using methods they trust.

- Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) automatically after settlement. No more chasing banks for the documentation you need for export incentives and tax filing.

- One platform for everything: Track all payments, view fund status, download reports, and manage compliance from a single dashboard.

- Transparent pricing with zero fixed costs: Pay only when you transact. No setup fees, monthly charges, or surprise deductions.

LLPs need speed, transparency, and compliance without the complexity. With PayGlocal, you get local accounts in major currencies, competitive conversion rates, and real-time tracking. The platform handles the technical complexity of international payments while you focus on serving clients and growing your practice.

Final thoughts

LLP offers liability protection, operational flexibility, and manageable compliance. For professionals and service businesses, especially those working with international clients, it's often the right choice.

Before registering, talk to a chartered accountant about tax implications for your specific situation. Make sure your LLP agreement clearly defines partner roles, profit sharing, and exit procedures. These foundations matter as your business grows.

If your LLP serves global clients, don't let payment complications slow you down. The right payment infrastructure means faster collections, better tracking, and easier compliance.

Get started with PayGlocal today. Collect from clients worldwide, settle in INR, and spend less time chasing payments.