With Indian service exports surging to $387.5 billion in 2024-25, the opportunity for global growth has never been greater. Yet, for many businesses, the excitement of winning an international contract is quickly dampened by the reality of collecting the payment.

When you deal with global clients, you aren't just a service provider; you inadvertently become a currency manager. Between high bank markups, unpredictable exchange rates, and delayed cross-border settlements, a significant portion of your margin can vanish before it reaches your account. Multi-currency payouts solve this problem.

In this guide, we break down in detail what multi-currency payouts are, how they work, their benefits, challenges, and how to choose the right solution for your business.

Multi-currency payouts are a payment solution that allows businesses to receive and manage funds in multiple currencies through a single account. Instead of maintaining separate bank accounts in different countries, you can accept payments in the currency your client uses.

For example, if you're an Indian SaaS company with clients in the US, UK, and Europe, you can receive payments in USD, GBP, and EUR directly.

Multi-currency accounts provide local bank details for major currencies. This means your US client can pay you using a local USD account. Your UK client uses GBP, and so on. The payment appears as a domestic transfer on their end. This often processes faster and with fewer fees.

Some businesses need multi-currency accounts immediately. Others can manage fine with traditional banking. The decision depends on how often you collect international payments and what those conversion fees cost you monthly. Here's when they make the most sense:

If these situations sound like your business, then you are likely at a stage where a basic bank account isn't enough.

Multi-currency payouts operate through a specialized payment platform. The platform provides you with virtual or physical bank accounts in different currencies. Here's how the process works:

Each incoming payment appears in your dashboard, showing the amount, currency, sender details, and expected settlement date. You can track funds moving from received to cleared to converted stages in real-time.

Multi-currency payouts improve several parts of your payment collection process at once. You'll notice the difference in speed, cost, and how much easier it becomes to manage international transactions. Some of the top benefits when you switch to multi-currency payouts include:

These benefits add up to real cost savings and operational efficiency. The value grows as your international business expands.

Multi-currency accounts work well when you choose the right provider. Pick the wrong one, and you'll face surprise fees, slow settlements, and missing compliance documents. Here are some of the key challenges you need to consider:

Tip: Good planning and the right platform help manage these challenges. Choose a solution that minimizes these friction points through transparent pricing, fast settlements, and automated compliance.

Whether you are a high-volume SaaS firm, an independent consultant, or a marketplace seller, how your money flows will differ. Choosing the right model is about aligning your payment infrastructure with where your clients and your growth are located.

Now let's look at each model in more detail.

These give you actual local bank account details in major currencies. For instance, you get a US routing number and account number for USD. You get a UK sort code and account number for GBP, and so on. When clients send payments, they use these local details.

The advantage is speed and cost. Local transfers typically process within 24 hours. They cost less than international wires. Your clients also find it easier since they're making a domestic payment from their perspective.

Virtual accounts work similarly. The account details route payments to a centralized master account held by your payment provider. You still receive local-looking account numbers for each currency. But they're not tied to individual bank accounts in each country.

Virtual accounts offer more flexibility. Providers can support more currencies without establishing physical banking relationships in every region. Setup is usually faster. The technology allows for better tracking and automation.

If you sell on global marketplaces like Amazon Global Selling, this model works well. If you receive payments through freelance platforms, marketplace settlement models integrate directly with these platforms. Your earnings in different currencies flow to your multi-currency account automatically.

This model works well for e-commerce businesses and freelancers who use specific platforms regularly. It reduces manual payment collection and keeps everything in one place.

These accounts accept payments in multiple currencies through the SWIFT network. They use a single account identifier. Any international transfer in supported currencies lands in your account. This works regardless of the sender's location.

SWIFT-based accounts work well for businesses that receive payments from diverse sources. However, they can involve higher fees and longer processing times compared to local transfer methods.

Moving to a multi-currency payout system is significantly faster than traditional international banking. By following a structured launch sequence, you can move from a local-only setup to a global financial footprint in just a few days:

For instance, if you're an agency receiving USD payments, the setup can typically take a few days from application to receiving your USD account details. You can then invoice your next US client with these local banking details.

Note: Most platforms guide you through each step. Good providers offer support during onboarding to ensure a smooth setup.

Not all multi-currency platforms work the same way or cost the same amount. Your choice affects how much you pay per transaction, how fast funds settle, and whether the platform supports the currencies your clients use. Here's what to consider when evaluating options:

1 Currency coverage

Check which currencies the platform supports. Make sure they include the ones you actually need. If most of your clients pay in USD and EUR, you need strong support for those currencies. Some platforms offer 30+ currencies. Others focus on a smaller set of major currencies.

2 Pricing structure

Look beyond headline rates. Examine the complete fee structure. Some providers charge monthly account fees, transaction fees, conversion fees, and withdrawal fees separately. Others use a simple pay-per-transaction model with no fixed costs. Calculate your total cost based on your expected transaction volume and conversion frequency.

3. Settlement speed

Find out how long it takes from receiving a payment to having converted funds available in your Indian bank account. Some platforms settle within 24-48 hours. Others may take 5-7 business days. Faster settlement means better working capital management.

4. Compliance features

Your platform should generate FIRC documents immediately upon settlement. You shouldn't have to request them. Sanction screening and other checks should happen in the background. Good compliance support saves time and reduces audit stress.

5. Integration capabilities

Can the solution integrate with your accounting software? Does it offer APIs if you need custom integration? Can it work with your e-commerce platform or invoicing system? Smooth integration reduces manual data entry and errors.

6. Support quality

Check what kind of customer support the platform offers. Check during what hours they're available. For businesses dealing with time-sensitive international payments, responsive support in your timezone matters.

7. Track record and reliability

Look for platforms with proven experience in your industry or business type. Check reviews from similar businesses. Ask about uptime guarantees. Payment infrastructure needs to be dependable.

Managing payments across multiple currencies gets complex fast. You need a solution that handles the technical complexity while giving you simple, transparent access to your global earnings.

PayGlocal provides exactly that. Indian businesses use it to accept international payments smoothly and settle in INR without hidden fees or compliance headaches. Here's what you get with PayGlocal:

PayGlocal handles the complexity of multi-currency payments so you can focus on growing your business. Collect from clients worldwide and settle in INR with confidence.

The shift toward a multi-currency payout strategy is the tipping point for any business serious about global scale. By eliminating the banking friction that drains your margins and slows your cycles, you stop being a local vendor and start being a global contender.

The infrastructure for borderless trade is already here. With the right platform, you can offer your international clients a local payment experience while keeping your internal operations focused on what you do best: delivering world-class value.

Ready to reclaim your margins and speed up your global growth? Get started with PayGlocal today and experience the future of international settlements.

When you deal with global clients, you aren't just a service provider; you inadvertently become a currency manager. Between high bank markups, unpredictable exchange rates, and delayed cross-border settlements, a significant portion of your margin can vanish before it reaches your account. Multi-currency payouts solve this problem.

In this guide, we break down in detail what multi-currency payouts are, how they work, their benefits, challenges, and how to choose the right solution for your business.

Key Takeaways

- Single account for multiple currencies: Multi-currency payouts let businesses receive and manage payments in different currencies without separate bank accounts.

- Best for global businesses: Multi-currency payouts work best for exporters, freelancers, D2C brands, and businesses with recurring international clients.

- Local bank details: Multi-currency accounts provide local bank details in major currencies like USD, GBP, EUR, and CAD for faster client payments.

- Choose based on your needs: Choosing the right solution depends on supported currencies, pricing transparency, settlement speed, and compliance features.

- Global payments platform: PayGlocal offers multi-currency accounts in 33+ currencies with zero fixed costs and an instant Foreign Inward Remittance Certificate (FIRC) for compliance.

What are Multi-Currency Payouts?

Multi-currency payouts are a payment solution that allows businesses to receive and manage funds in multiple currencies through a single account. Instead of maintaining separate bank accounts in different countries, you can accept payments in the currency your client uses.

For example, if you're an Indian SaaS company with clients in the US, UK, and Europe, you can receive payments in USD, GBP, and EUR directly.

Multi-currency accounts provide local bank details for major currencies. This means your US client can pay you using a local USD account. Your UK client uses GBP, and so on. The payment appears as a domestic transfer on their end. This often processes faster and with fewer fees.

When Should You Use Multi-Currency Payouts?

Some businesses need multi-currency accounts immediately. Others can manage fine with traditional banking. The decision depends on how often you collect international payments and what those conversion fees cost you monthly. Here's when they make the most sense:

- Regular international clients: If you invoice clients in different countries every month, multi-currency accounts save you from converting each payment immediately.

- High transaction volumes: Businesses processing multiple international payments daily or weekly benefit from consolidated currency management and lower per-transaction costs.

- Foreign currency expenses: If you pay for software, advertising, or services in USD or EUR, keeping funds in those currencies avoids double conversion.

- Freelancers on global platforms: Those receiving payments from Upwork, Fiverr, or similar platforms can collect in the platform's native currency and convert strategically.

- E-commerce exporters: Online sellers shipping to multiple countries need efficient ways to receive payments in local currencies from various marketplaces.

If these situations sound like your business, then you are likely at a stage where a basic bank account isn't enough.

How do Multi-Currency Payouts Work?

Multi-currency payouts operate through a specialized payment platform. The platform provides you with virtual or physical bank accounts in different currencies. Here's how the process works:

- Account setup: You create a multi-currency account with a payment provider and receive local account details for supported currencies like USD, GBP, EUR, and CAD.

- Share account details: When a client needs to pay you, you provide the relevant currency account details so they can make a local bank transfer.

- Receive payments: The client sends payment in their local currency, which arrives in your multi-currency account and sits there until you decide to convert it.

- Settlement: Converted funds transfer to your Indian bank account according to your provider's schedule.

- Track and comply: You receive notifications about payment receipt, fund status, and settlement completion, plus automatic FIRC documents for compliance.

Each incoming payment appears in your dashboard, showing the amount, currency, sender details, and expected settlement date. You can track funds moving from received to cleared to converted stages in real-time.

What are the Benefits of Multi-Currency Payouts?

Multi-currency payouts improve several parts of your payment collection process at once. You'll notice the difference in speed, cost, and how much easier it becomes to manage international transactions. Some of the top benefits when you switch to multi-currency payouts include:

- Faster payment collection: Local bank details mean your client's payments are processed as domestic transfers, settling faster than international wire transfers.

- Simplified fund management: You manage all currencies through one platform with a single dashboard showing balances, transaction history, and conversion options.

- Better cash flow control: You decide when to convert currencies based on your business needs and market conditions.

- Compliance made easy: The platform handles compliance documentation automatically, providing FIRC certificates and required documents without manual follow-up.

- Professional client experience: Providing local currency account details makes you appear more established and simplifies the payment process for international clients.

These benefits add up to real cost savings and operational efficiency. The value grows as your international business expands.

What are the Challenges with Multi-Currency Payouts?

Multi-currency accounts work well when you choose the right provider. Pick the wrong one, and you'll face surprise fees, slow settlements, and missing compliance documents. Here are some of the key challenges you need to consider:

- Platform fees vary: Different providers charge different transaction fees, conversion fees, and withdrawal fees that can add up if you're not careful about comparing total costs.

- Compliance documentation: While good platforms automate this, you still need to maintain proper records and ensure FIRC generation happens correctly for tax purposes.

- Managing multiple balances: Tracking balances across several currencies requires attention, especially during financial planning and reporting periods.

- Minimum balance requirements: Some platforms require you to maintain minimum balances in certain currencies or charge inactivity fees.

- Accounting complexity: Your finance team needs to handle multi-currency bookkeeping, which can complicate month-end closings and reconciliation.

- Settlement delays: Not all platforms settle funds quickly, and delays can impact your working capital if you need INR urgently.

Tip: Good planning and the right platform help manage these challenges. Choose a solution that minimizes these friction points through transparent pricing, fast settlements, and automated compliance.

What Types of Multi-Currency Payout Models Exist?

Whether you are a high-volume SaaS firm, an independent consultant, or a marketplace seller, how your money flows will differ. Choosing the right model is about aligning your payment infrastructure with where your clients and your growth are located.

Now let's look at each model in more detail.

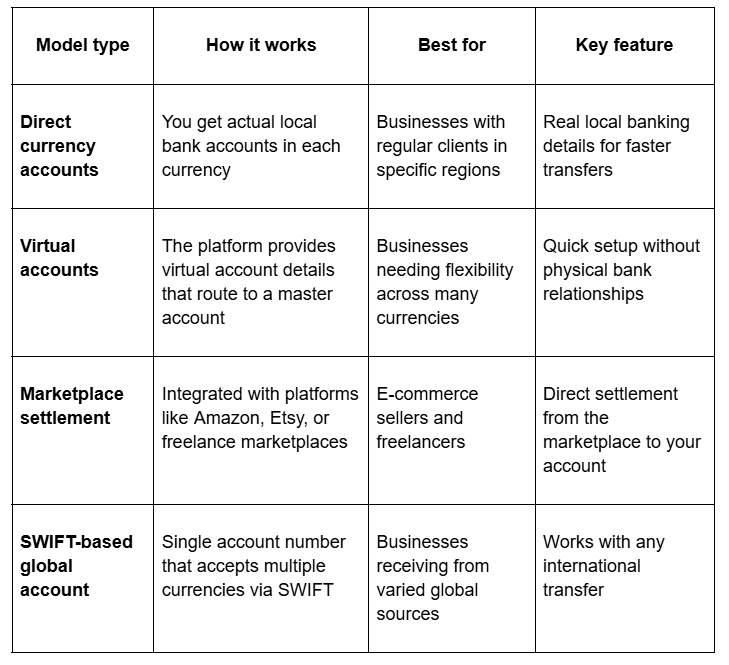

Direct Currency Accounts

These give you actual local bank account details in major currencies. For instance, you get a US routing number and account number for USD. You get a UK sort code and account number for GBP, and so on. When clients send payments, they use these local details.

The advantage is speed and cost. Local transfers typically process within 24 hours. They cost less than international wires. Your clients also find it easier since they're making a domestic payment from their perspective.

Virtual Accounts

Virtual accounts work similarly. The account details route payments to a centralized master account held by your payment provider. You still receive local-looking account numbers for each currency. But they're not tied to individual bank accounts in each country.

Virtual accounts offer more flexibility. Providers can support more currencies without establishing physical banking relationships in every region. Setup is usually faster. The technology allows for better tracking and automation.

Marketplace Settlement

If you sell on global marketplaces like Amazon Global Selling, this model works well. If you receive payments through freelance platforms, marketplace settlement models integrate directly with these platforms. Your earnings in different currencies flow to your multi-currency account automatically.

This model works well for e-commerce businesses and freelancers who use specific platforms regularly. It reduces manual payment collection and keeps everything in one place.

SWIFT-based Global Accounts

These accounts accept payments in multiple currencies through the SWIFT network. They use a single account identifier. Any international transfer in supported currencies lands in your account. This works regardless of the sender's location.

SWIFT-based accounts work well for businesses that receive payments from diverse sources. However, they can involve higher fees and longer processing times compared to local transfer methods.

How to Get Started with Multi-Currency Payouts?

Moving to a multi-currency payout system is significantly faster than traditional international banking. By following a structured launch sequence, you can move from a local-only setup to a global financial footprint in just a few days:

- Assess your needs: List which currencies you receive payments in most frequently and estimate your monthly transaction volumes in each currency.

- Research platform options: Compare 3-5 providers based on currency support, pricing, settlement speed, and compliance features relevant to your business.

- Check eligibility requirements: Verify you meet the provider's business verification requirements, which typically include incorporation documents and business banking details.

- Submit your application: Complete the signup process with the necessary documentation, like PAN, GST registration, incorporation certificate, and business bank account proof.

- Complete verification: Most platforms verify your business within 24-72 hours, though some may require additional documentation or video KYC.

- Receive account details: Once approved, you get local bank account details for supported currencies that you can share with clients immediately.

- Test with small transactions: Before fully switching, test the platform with smaller payments to verify settlement times and check that compliance documents are generated correctly.

- Integrate with your systems: Connect the platform to your accounting software or invoicing system to automate reconciliation and reduce manual work.

- Inform your clients: Share the new payment details with international clients, explaining that using local currency accounts will speed up their payment processing.

For instance, if you're an agency receiving USD payments, the setup can typically take a few days from application to receiving your USD account details. You can then invoice your next US client with these local banking details.

Note: Most platforms guide you through each step. Good providers offer support during onboarding to ensure a smooth setup.

How to Choose the Right Multi-Currency Payout Solution?

Not all multi-currency platforms work the same way or cost the same amount. Your choice affects how much you pay per transaction, how fast funds settle, and whether the platform supports the currencies your clients use. Here's what to consider when evaluating options:

1 Currency coverage

Check which currencies the platform supports. Make sure they include the ones you actually need. If most of your clients pay in USD and EUR, you need strong support for those currencies. Some platforms offer 30+ currencies. Others focus on a smaller set of major currencies.

2 Pricing structure

Look beyond headline rates. Examine the complete fee structure. Some providers charge monthly account fees, transaction fees, conversion fees, and withdrawal fees separately. Others use a simple pay-per-transaction model with no fixed costs. Calculate your total cost based on your expected transaction volume and conversion frequency.

3. Settlement speed

Find out how long it takes from receiving a payment to having converted funds available in your Indian bank account. Some platforms settle within 24-48 hours. Others may take 5-7 business days. Faster settlement means better working capital management.

4. Compliance features

Your platform should generate FIRC documents immediately upon settlement. You shouldn't have to request them. Sanction screening and other checks should happen in the background. Good compliance support saves time and reduces audit stress.

5. Integration capabilities

Can the solution integrate with your accounting software? Does it offer APIs if you need custom integration? Can it work with your e-commerce platform or invoicing system? Smooth integration reduces manual data entry and errors.

6. Support quality

Check what kind of customer support the platform offers. Check during what hours they're available. For businesses dealing with time-sensitive international payments, responsive support in your timezone matters.

7. Track record and reliability

Look for platforms with proven experience in your industry or business type. Check reviews from similar businesses. Ask about uptime guarantees. Payment infrastructure needs to be dependable.

Accept Globally, Settle Locally with PayGlocal

Managing payments across multiple currencies gets complex fast. You need a solution that handles the technical complexity while giving you simple, transparent access to your global earnings.

PayGlocal provides exactly that. Indian businesses use it to accept international payments smoothly and settle in INR without hidden fees or compliance headaches. Here's what you get with PayGlocal:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries through a single platform. Get local account details in USD, GBP, EUR, and CAD so your clients can pay you like a domestic vendor.

- Zero fixed costs: You pay only when you transact. No monthly fees, no setup charges, no documentation fees. Clear pricing with no surprises allows you to scale without worrying about fixed overheads.

- Instant compliance documentation: Receive FIRC right in your inbox after every settlement. Stay compliant without manual follow-up or paperwork delays. All documentation is downloadable from your dashboard.

- Real-time payment tracking: Get notifications at every step from payment initiation to settlement completion. Know exactly where your money is and when it will arrive in your account.

- One platform: Manage all payment methods, currencies, and transactions from a single dashboard. View balances, download reports, and track fund status without switching between multiple systems.

PayGlocal handles the complexity of multi-currency payments so you can focus on growing your business. Collect from clients worldwide and settle in INR with confidence.

Final Thoughts

The shift toward a multi-currency payout strategy is the tipping point for any business serious about global scale. By eliminating the banking friction that drains your margins and slows your cycles, you stop being a local vendor and start being a global contender.

The infrastructure for borderless trade is already here. With the right platform, you can offer your international clients a local payment experience while keeping your internal operations focused on what you do best: delivering world-class value.

Ready to reclaim your margins and speed up your global growth? Get started with PayGlocal today and experience the future of international settlements.