You're finalizing a deal with an international client, but when you share your payment details, they pause. The international wire transfer process looks complicated on their end. High fees, unfamiliar account formats, and multi-day processing times create friction right when you need the payment to go through smoothly.

A multi-currency wallet solves this by providing local payment details that clients can easily recognize. Indian businesses are exporting at record levels, with exports jumping by up to 67% in the last decade. As more companies scale globally, there's a growing need for a better way to handle foreign currency payments.

This guide breaks down how multi-currency wallets work and how they can save you money on international sales. We will also highlight the key features to consider when selecting a provider, so you can choose a solution that helps you keep more of what you earn.

A multi-currency wallet is a digital account that allows you to receive and manage money in different currencies. You get local bank account details for major currencies, which means your international clients can pay you as if you have a bank account in their country.

For example, a freelance designer working with clients in the UK and Canada can receive GBP and CAD payments directly. Instead of each payment going through currency conversion and international wire fees, the funds land in their multi-currency wallet. They track everything from one dashboard and move money to their Indian account when it makes sense for their cash flow.

This setup works for exporters too. If you sell products to customers across Europe, you can accept EUR payments locally. Your customers see familiar payment details, which builds trust and improves payment success rates.

A multi-currency wallet essentially gives you a digital home base in every market you serve. Instead of your money traveling across oceans through multiple expensive intermediary banks, it moves within local banking systems, giving a much smoother experience for your clients.

Here's what happens step by step:

The whole process removes the friction of international payments. Your clients pay locally, you receive efficiently, and you control when and how much to convert based on your business needs.

While traditional banks are built for domestic stability, they often struggle with the speed and cost requirements of global trade. Choosing a multi-currency wallet over a traditional bank account offers several direct advantages that protect your profit margins and save you time:

Here's how these benefits stack up when compared to traditional banking:

The real value shows up in your daily operations. You spend less time on payment admin, lose less money to fees, and get paid faster.

Tip: Track your current payment costs for one month. Calculate total fees, time spent on reconciliation, and average settlement time. Compare this against what a multi-currency wallet would cost. The difference often justifies switching immediately.

Not every business needs a multi-currency wallet from day one. However, as your international volume grows, the inefficiencies of traditional banking, like high markups and slow clearing times, become a significant drain on your time and profits.

The right time to switch is when you fall into one of these six categories:

Designers, developers, writers, and consultants billing clients in the US, UK, Europe, or other countries benefit from receiving payments in local currencies. Instead of losing money to conversion fees on every invoice, you collect USD or GBP directly and settle when rates work in your favor.

Exporters shipping products internationally or SaaS companies selling subscriptions globally need efficient ways to collect payments across currencies. Multi-currency wallets give you local account details that make it easier for customers to pay and reduce transaction failures.

Amazon Global, Etsy, eBay, or other platforms often pay sellers in foreign currencies. A multi-currency wallet lets you receive these payments without paying high bank fees for each settlement.

Subscription businesses, agencies with retainer clients, or companies with ongoing contracts abroad need reliable recurring payment collection. Multi-currency wallets handle this without forcing currency conversion on every transaction.

If you're paying high percentages on international transfers or losing money to poor exchange rates, calculate what you're actually spending monthly. When these costs exceed what a wallet charges, switching saves money immediately.

Traditional international bank transfers take days to clear. If cash flow matters and you can't wait a week for payments to arrive, multi-currency wallets settle faster.

Tip: The right time to switch is when the cost of staying with traditional banking exceeds the effort of moving to a wallet. For instance, if you're a freelancer receiving two or three international payments monthly and losing significant amounts to fees, that's your signal.

The best multi-currency wallet isn't necessarily the one with the most features; it's the one that eliminates your specific operational friction. Here is what to evaluate before you commit:

Check which currencies the wallet supports and whether they provide local account details for your main markets. If most of your clients are in the US and Europe, you need USD, GBP, and EUR at a minimum. Some wallets support 10 currencies, others support 30+. Match this to where your revenue comes from.

For example, if you're a SaaS company with customers across North America, Europe, and Australia, look for a wallet that gives you local details in USD, CAD, GBP, EUR, and AUD. This covers your major markets without forcing clients through international transfers.

Know exactly what you'll pay. Look at transaction fees, conversion rates, monthly charges, and any hidden costs. The cheapest option isn't always best if it has surprise fees or poor exchange rates.

Compare the total cost per transaction, not just the headline rate. A wallet charging 2% with good exchange rates might be cheaper than one charging 1.5% with marked-up conversion rates.

Your wallet should handle compliance automatically. Look for instant FIRC generation, transaction records that match GST requirements, and proper audit trails. For instance, exporters need FIRC for every settlement to claim tax benefits. If your wallet generates this automatically, it saves you hours every month.

Check if the wallet integrates with your invoicing software, accounting tools, or e-commerce platform. Manual data entry creates errors and wastes time. The wallet should fit into your existing workflow, not force you to change everything.

The dashboard should be clear enough that you can check balances, track payments, and initiate settlements without confusion. If it takes 10 clicks to do something simple, you'll waste time.

Real-time updates matter when you're managing cash flow. Your wallet should notify you when payments arrive, show you the status of settlements, and let you download transaction reports easily.

Your money sits in this wallet, so security can't be optional. Look for encryption, two-factor authentication, and regulatory authorization. Check if the provider is licensed for payment operations in India.

Note: Before committing to any wallet, test it with small transactions. See how the dashboard works, check settlement speed, and experience their support. This tells you more than any feature list.

You've seen what multi-currency wallets can do and what to look for when choosing one. Indian businesses face specific challenges that generic international payment tools don't address well. PayGlocal is designed for companies operating from India and collecting payments globally. Here's what you get:

PayGlocal helps you collect payments faster, track them easier, and keep more of your money. Whether you're a freelancer billing global clients or an exporter managing marketplace settlements, you get the tools you need without the complexity.

Multi-currency wallets remove the biggest friction points in international payments. You get lower fees, faster settlements, and simpler compliance than traditional banking offers. For businesses accepting payments from multiple countries, this isn't a nice-to-have anymore.

The right wallet depends on your business model, transaction volume, and where your clients are located. Look for supported currencies that match your markets, transparent pricing without hidden fees, automatic compliance documentation, and integration with your existing tools. Test the platform before committing to make sure it fits your workflow.

If you're ready to collect global payments without unnecessary costs or delays, PayGlocal gives you everything you need in one platform. Contact us today to see how it works for your business.

A multi-currency wallet solves this by providing local payment details that clients can easily recognize. Indian businesses are exporting at record levels, with exports jumping by up to 67% in the last decade. As more companies scale globally, there's a growing need for a better way to handle foreign currency payments.

This guide breaks down how multi-currency wallets work and how they can save you money on international sales. We will also highlight the key features to consider when selecting a provider, so you can choose a solution that helps you keep more of what you earn.

Key takeaways

- Multi-currency wallet: It is a digital account that lets you accept and manage payments in multiple currencies without opening separate bank accounts.

- Main benefit: You pay lower fees compared to traditional banks and get faster access to your funds with transparent pricing.

- How it works: You receive payments in local currencies like USD, GBP, or EUR, hold them in the wallet, and settle to your Indian bank account when you need.

- Key features matter: Look for local account details, transparent fee structure, compliance automation, real-time tracking, and integration with your existing tools.

- PayGlocal features: Multi-currency accounts in 33+ currencies with local details in USD, GBP, EUR, and CAD, instant Foreign Inward Remittance Certificate (FIRC) generation, zero fixed costs, and complete payment tracking.

What is a multi-currency wallet?

A multi-currency wallet is a digital account that allows you to receive and manage money in different currencies. You get local bank account details for major currencies, which means your international clients can pay you as if you have a bank account in their country.

For example, a freelance designer working with clients in the UK and Canada can receive GBP and CAD payments directly. Instead of each payment going through currency conversion and international wire fees, the funds land in their multi-currency wallet. They track everything from one dashboard and move money to their Indian account when it makes sense for their cash flow.

This setup works for exporters too. If you sell products to customers across Europe, you can accept EUR payments locally. Your customers see familiar payment details, which builds trust and improves payment success rates.

How does a multi-currency wallet work?

A multi-currency wallet essentially gives you a digital home base in every market you serve. Instead of your money traveling across oceans through multiple expensive intermediary banks, it moves within local banking systems, giving a much smoother experience for your clients.

Here's what happens step by step:

- You get local account details: The wallet provider gives you real bank account numbers and routing codes for currencies like USD, GBP, EUR, or CAD. These look like regular local accounts to your clients.

- Clients pay in their currency: Your US client pays USD to your US account details. Your European client pays EUR to your European account details. The payment flows through local banking channels, which is faster and cheaper.

- Funds arrive in your wallet: The money lands in your multi-currency wallet in the original currency. You can see your balance in each currency separately.

- You decide when to settle: When you need the money in your Indian bank account, you initiate a settlement. The wallet converts the currency at the prevailing rate and transfers INR to your account.

- Compliance happens automatically: The system generates required documents like FIRC for your settlements, keeping you compliant without manual paperwork.

The whole process removes the friction of international payments. Your clients pay locally, you receive efficiently, and you control when and how much to convert based on your business needs.

Why is a multi-currency wallet better than traditional banking for your business?

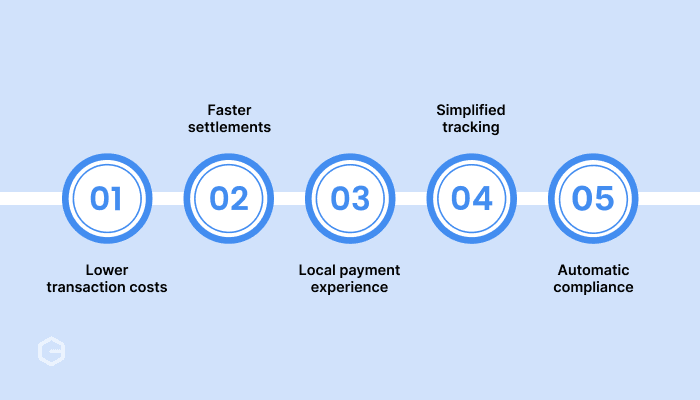

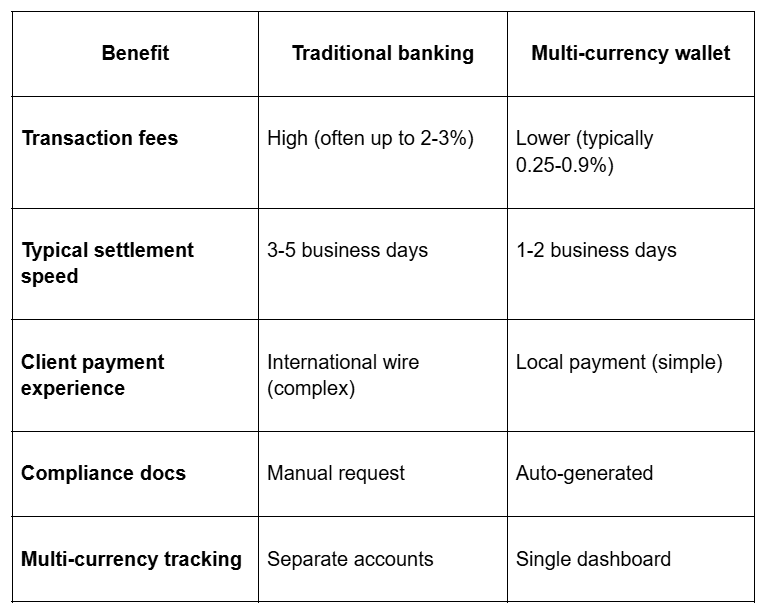

While traditional banks are built for domestic stability, they often struggle with the speed and cost requirements of global trade. Choosing a multi-currency wallet over a traditional bank account offers several direct advantages that protect your profit margins and save you time:

- Lower transaction costs: Traditional banks charge high fees for international wire transfers and currency conversion. Multi-currency wallets typically offer transparent, lower fees. For instance, receiving a $5,000 payment might cost you $50-75 through a bank but only $25-35 through a wallet with better rates.

- Faster settlements: Bank transfers can take 3-5 business days for international payments. Multi-currency wallets often settle within 1-2 business days, improving your cash flow when you need to pay suppliers or manage expenses.

- Local payment experience: When you provide local account details to your clients, they pay through their regular banking system. This means lower fees for them too, and higher success rates because the transaction doesn't get flagged as international.

- Simplified tracking: One dashboard shows all your currencies, transactions, and settlements. You don't log into multiple bank accounts or reconcile payments from different sources manually.

- Automatic compliance: Documents like the FIRC are generated automatically when you settle funds. This saves hours of work and removes the headache of chasing paperwork for tax purposes.

Here's how these benefits stack up when compared to traditional banking:

The real value shows up in your daily operations. You spend less time on payment admin, lose less money to fees, and get paid faster.

Tip: Track your current payment costs for one month. Calculate total fees, time spent on reconciliation, and average settlement time. Compare this against what a multi-currency wallet would cost. The difference often justifies switching immediately.

When do you need a multi-currency wallet?

Not every business needs a multi-currency wallet from day one. However, as your international volume grows, the inefficiencies of traditional banking, like high markups and slow clearing times, become a significant drain on your time and profits.

The right time to switch is when you fall into one of these six categories:

- Working as a freelancer for international clients

Designers, developers, writers, and consultants billing clients in the US, UK, Europe, or other countries benefit from receiving payments in local currencies. Instead of losing money to conversion fees on every invoice, you collect USD or GBP directly and settle when rates work in your favor.

- Exporting goods or services regularly

Exporters shipping products internationally or SaaS companies selling subscriptions globally need efficient ways to collect payments across currencies. Multi-currency wallets give you local account details that make it easier for customers to pay and reduce transaction failures.

- Selling on international marketplaces

Amazon Global, Etsy, eBay, or other platforms often pay sellers in foreign currencies. A multi-currency wallet lets you receive these payments without paying high bank fees for each settlement.

- Managing recurring international payments

Subscription businesses, agencies with retainer clients, or companies with ongoing contracts abroad need reliable recurring payment collection. Multi-currency wallets handle this without forcing currency conversion on every transaction.

- High bank fees eating into margins

If you're paying high percentages on international transfers or losing money to poor exchange rates, calculate what you're actually spending monthly. When these costs exceed what a wallet charges, switching saves money immediately.

- Need faster access to funds

Traditional international bank transfers take days to clear. If cash flow matters and you can't wait a week for payments to arrive, multi-currency wallets settle faster.

Tip: The right time to switch is when the cost of staying with traditional banking exceeds the effort of moving to a wallet. For instance, if you're a freelancer receiving two or three international payments monthly and losing significant amounts to fees, that's your signal.

How to choose the right multi-currency wallet?

The best multi-currency wallet isn't necessarily the one with the most features; it's the one that eliminates your specific operational friction. Here is what to evaluate before you commit:

Supported currencies and regions

Check which currencies the wallet supports and whether they provide local account details for your main markets. If most of your clients are in the US and Europe, you need USD, GBP, and EUR at a minimum. Some wallets support 10 currencies, others support 30+. Match this to where your revenue comes from.

For example, if you're a SaaS company with customers across North America, Europe, and Australia, look for a wallet that gives you local details in USD, CAD, GBP, EUR, and AUD. This covers your major markets without forcing clients through international transfers.

Fee structure and transparency

Know exactly what you'll pay. Look at transaction fees, conversion rates, monthly charges, and any hidden costs. The cheapest option isn't always best if it has surprise fees or poor exchange rates.

Compare the total cost per transaction, not just the headline rate. A wallet charging 2% with good exchange rates might be cheaper than one charging 1.5% with marked-up conversion rates.

Compliance and documentation

Your wallet should handle compliance automatically. Look for instant FIRC generation, transaction records that match GST requirements, and proper audit trails. For instance, exporters need FIRC for every settlement to claim tax benefits. If your wallet generates this automatically, it saves you hours every month.

Integration and ease of use

Check if the wallet integrates with your invoicing software, accounting tools, or e-commerce platform. Manual data entry creates errors and wastes time. The wallet should fit into your existing workflow, not force you to change everything.

The dashboard should be clear enough that you can check balances, track payments, and initiate settlements without confusion. If it takes 10 clicks to do something simple, you'll waste time.

Payment tracking and notifications

Real-time updates matter when you're managing cash flow. Your wallet should notify you when payments arrive, show you the status of settlements, and let you download transaction reports easily.

Security and reliability

Your money sits in this wallet, so security can't be optional. Look for encryption, two-factor authentication, and regulatory authorization. Check if the provider is licensed for payment operations in India.

Note: Before committing to any wallet, test it with small transactions. See how the dashboard works, check settlement speed, and experience their support. This tells you more than any feature list.

Start accepting global payments without all the complexity

You've seen what multi-currency wallets can do and what to look for when choosing one. Indian businesses face specific challenges that generic international payment tools don't address well. PayGlocal is designed for companies operating from India and collecting payments globally. Here's what you get:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries. Get local account details in USD, GBP, EUR, and CAD so your clients pay you like you're local to them.

- Card payments: Process international credit and debit cards with high approval rates and enhanced messaging to global issuers.

- Global payment methods: Accept 40+ local payment methods so customers can pay using what they trust.

- Recurring payments: Set up subscriptions and recurring billing for international cards with network-compliant solutions.

- One platform: Manage everything from one dashboard with real-time tracking, custom reports, and payment notifications.

PayGlocal helps you collect payments faster, track them easier, and keep more of your money. Whether you're a freelancer billing global clients or an exporter managing marketplace settlements, you get the tools you need without the complexity.

Final thoughts

Multi-currency wallets remove the biggest friction points in international payments. You get lower fees, faster settlements, and simpler compliance than traditional banking offers. For businesses accepting payments from multiple countries, this isn't a nice-to-have anymore.

The right wallet depends on your business model, transaction volume, and where your clients are located. Look for supported currencies that match your markets, transparent pricing without hidden fees, automatic compliance documentation, and integration with your existing tools. Test the platform before committing to make sure it fits your workflow.

If you're ready to collect global payments without unnecessary costs or delays, PayGlocal gives you everything you need in one platform. Contact us today to see how it works for your business.