India's economy is on track to grow faster, with GDP growth expected to reach 6.3% to 6.8% in 2025-26. With rise in economic growth and more businesses going global, choosing the right business structure matters more than ever.

While registering your business, you come across terms like sole proprietorship and One Person Company (OPC). But which one actually makes sense for your business? The choice between sole proprietorship and OPC affects everything from your personal liability to how you collect payments and file taxes.

In this guide, we break down the differences between sole proprietorship and OPC so you can make an effective decision that fits your business stage, goals, and plans for growth.

A sole proprietorship is the simplest business structure in India. One person owns and runs the business. There's no legal separation between you and your business. You are the business.

You don't need to formally register a sole proprietorship as a business entity. However, you might need registrations like GST or shop licenses depending on your turnover and activity. For example, if you're a freelance graphic designer earning from international clients, you operate as a sole proprietor by default unless you register a different structure.

The main appeal is simplicity. Minimal paperwork, no mandatory audits, and full control. But here's the catch: you personally own all the profits, and you also personally carry all the liability. If your business faces a legal issue or debt, your personal assets can be used to settle it.

A One Person Company (OPC) is a hybrid structure that combines the benefits of a sole proprietorship (single ownership) with the benefits of a private limited company (limited liability and separate legal identity).

An OPC is a registered company, which means it's a separate legal entity from you. You own 100% of it, but the company itself can own assets, enter contracts, and carry liabilities independently. For instance, if you're an IT consultant setting up an OPC, the company can sign agreements with international clients, and you're protected if something goes wrong. Your personal assets stay separate.

Unlike a sole proprietorship, an OPC requires formal registration with the Ministry of Corporate Affairs (MCA), annual filings, and compliance with company law.

You also need to appoint a nominee who will take over if something happens to you. The tradeoff for this structure is more paperwork and compliance, but stronger legal protection and better credibility with clients, banks, and investors.

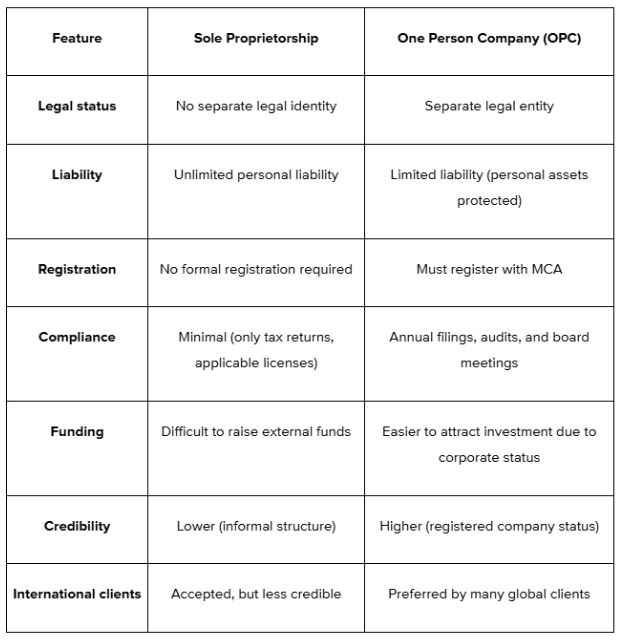

Here's how sole proprietorship and OPC stack up against each other.

Each structure comes with its own strengths and limitations. Let's look deeper at what they mean in practice.

Your legal status determines how much personal risk you carry when running your business.

In a sole proprietorship, you and your business are one. Your name is the business. There's no separate legal identity. Any contract, invoice, or legal notice comes directly to you. This also means you have unlimited liability.

If your business owes money or faces a legal claim, creditors can come after your personal savings, property, or other assets. For example, if a client sues you for breach of contract and wins, your personal home could be at risk.

In an OPC, the company is a separate legal person. It can own property, file lawsuits, and be sued independently of you. This separation is important when dealing with international clients or entering into contracts. OPC offers limited liability.

Your financial risk is limited to the amount you invested in the company. Your personal assets stay protected. If your OPC faces a lawsuit or debt, only the company's assets are on the line, not your personal savings or property.

This is a big deal if you're working with international clients, handling large contracts, or operating in industries with higher legal or financial risks.

The registration and compliance process is where sole proprietorship and OPC differ the most.

However, depending on your business activity and turnover, you may need GST registration if your turnover exceeds the threshold, a Shop and Establishment license if you have a physical location, professional tax registration in certain states, and an Import Export Code (IEC) if you're exporting goods or services.

That's it. No annual audits. No board meetings. You just file your income tax return every year.

Once registered, OPCs have ongoing compliance requirements. These include annual financial statements and audits, annual return filing, board meetings and resolutions, and income tax returns for the company.

The compliance burden is higher, but it comes with stronger legal standing and better credibility.

Your business structure affects how your income is taxed.

In a sole proprietorship, your business income is treated as personal income. You file under your individual PAN, and profits are taxed according to income tax slabs. Any business expense you claim reduces your taxable income, but the tax calculation happens at the individual level.

For example, if you earn as a freelance consultant, you'll pay tax on that amount based on the slab rates applicable to individuals. You also handle your own TDS (Tax Deducted at Source) and advance tax payments.

In an OPC, the company pays corporate tax, which is a flat rate. The company files its own tax return, separate from your personal return.

You can also take a salary from your OPC (which is tax-deductible for the company), and that salary is taxed as personal income. This gives you some flexibility in structuring your income. Dividends paid by an OPC to the owner are taxable in the owner's hands.

So, which is better? It depends on your income level and how you want to structure withdrawals. Both have their own advantages at different revenue stages.

The right choice depends on where you are now and where you're heading. Here's how you can pick the right option based on your situation.

For example, a freelance content writer earning from international clients doesn't need the complexity of an OPC. A sole proprietorship keeps things lean and manageable.

For instance, a SaaS founder building a subscription product for global users benefits from OPC's structure. It makes the business look more legitimate, helps with contracts, and prepares for future funding rounds.

Accept global payments faster and easily with PayGlocal

Choosing between sole proprietorship and OPC is an important decision, but it's just the starting point. Once you have your structure, you need a way to collect payments from international clients that's fast, affordable, and compliant.

That's where PayGlocal comes in. PayGlocal is built for Indian businesses doing global work. Whether you're a freelancer, exporter, or growing company, you get everything you need to accept payments from 180+ countries and settle in INR.

Here's what you get:

PayGlocal helps you get paid faster, with full transparency, and at rates that make sense for your business, whether you're starting out or scaling internationally.

Sole proprietorship and OPC both work for solo business owners, but they're designed for different stages, risk levels, and growth goals.

Sole proprietorship gives you simplicity, low costs, and full control. It's perfect if you're just starting, testing ideas, or keeping your business small and manageable. OPC gives you limited liability, a corporate structure, and credibility. It's better if you're working with international clients, handling contracts, or planning to scale.

Neither structure blocks you from accepting international payments or serving global customers. What matters is choosing a structure that fits your current needs and future goals, and ensuring you have the right tools to collect payments smoothly.

Ready to collect globally and settle locally, no matter which structure you choose? Get started with PayGlocal today and take control of your international payments.

Yes, you can accept payments from international clients through wire transfers, payment gateways, or platforms like PayGlocal that offer multi-currency accounts. You'll receive an FIRC (Foreign Inward Remittance Certificate) for compliance. However, some larger clients prefer contracting with registered companies instead of individuals.

No formal business registration is required to accept international payments as a sole proprietor. However, you may need GST registration, an Import Export Code (IEC), or a PAN for tax compliance, depending on your activity and turnover. Using a platform like PayGlocal simplifies the process.

It depends on your income and risk level. If you're earning less with low liability risk, sole proprietorship keeps things simple. If you're earning more, handling larger contracts, or want limited liability protection, OPC makes more sense.

The main advantage is limited liability protection. In an OPC, your personal assets are protected if the business faces legal issues or debts. Only the company's assets are at risk. In a sole proprietorship, you have unlimited liability, meaning your personal savings and property can be used to settle business debts.

Both structures work for service and product businesses. The choice depends more on your growth plans and risk level. Service businesses (consulting, design, IT) often start as sole proprietorships because liability is lower. Product businesses sometimes prefer OPC for liability protection if dealing with inventory or suppliers.

While registering your business, you come across terms like sole proprietorship and One Person Company (OPC). But which one actually makes sense for your business? The choice between sole proprietorship and OPC affects everything from your personal liability to how you collect payments and file taxes.

In this guide, we break down the differences between sole proprietorship and OPC so you can make an effective decision that fits your business stage, goals, and plans for growth.

Key takeaways

- Sole proprietorship: In a sole proprietorship, there’s no separate legal identity means unlimited personal liability. Your home, savings, and assets are at risk if your business faces legal or financial trouble.

- OPC: With OPC, you get limited liability, which protects your personal assets. Only the company's money is on the line, not yours.

- Registration effort differs: Sole proprietorship needs no formal registration. OPC requires annual filings, audits, and board meetings.

- Tax treatment splits by structure: Sole proprietors pay individual income tax on profits. OPCs pay flat corporate tax rates, which can work better at certain income levels.

- Global payments made easy: PayGlocal makes it easy to collect international payments with multi-currency accounts, instant FIRC, and zero setup fees, regardless of which option you choose.

What is a sole proprietorship?

A sole proprietorship is the simplest business structure in India. One person owns and runs the business. There's no legal separation between you and your business. You are the business.

You don't need to formally register a sole proprietorship as a business entity. However, you might need registrations like GST or shop licenses depending on your turnover and activity. For example, if you're a freelance graphic designer earning from international clients, you operate as a sole proprietor by default unless you register a different structure.

The main appeal is simplicity. Minimal paperwork, no mandatory audits, and full control. But here's the catch: you personally own all the profits, and you also personally carry all the liability. If your business faces a legal issue or debt, your personal assets can be used to settle it.

What is a one person company?

A One Person Company (OPC) is a hybrid structure that combines the benefits of a sole proprietorship (single ownership) with the benefits of a private limited company (limited liability and separate legal identity).

An OPC is a registered company, which means it's a separate legal entity from you. You own 100% of it, but the company itself can own assets, enter contracts, and carry liabilities independently. For instance, if you're an IT consultant setting up an OPC, the company can sign agreements with international clients, and you're protected if something goes wrong. Your personal assets stay separate.

Unlike a sole proprietorship, an OPC requires formal registration with the Ministry of Corporate Affairs (MCA), annual filings, and compliance with company law.

You also need to appoint a nominee who will take over if something happens to you. The tradeoff for this structure is more paperwork and compliance, but stronger legal protection and better credibility with clients, banks, and investors.

What is difference between a sole proprietorship and a one person company?

Here's how sole proprietorship and OPC stack up against each other.

Each structure comes with its own strengths and limitations. Let's look deeper at what they mean in practice.

Legal status and liability protection

Your legal status determines how much personal risk you carry when running your business.

In a sole proprietorship, you and your business are one. Your name is the business. There's no separate legal identity. Any contract, invoice, or legal notice comes directly to you. This also means you have unlimited liability.

If your business owes money or faces a legal claim, creditors can come after your personal savings, property, or other assets. For example, if a client sues you for breach of contract and wins, your personal home could be at risk.

In an OPC, the company is a separate legal person. It can own property, file lawsuits, and be sued independently of you. This separation is important when dealing with international clients or entering into contracts. OPC offers limited liability.

Your financial risk is limited to the amount you invested in the company. Your personal assets stay protected. If your OPC faces a lawsuit or debt, only the company's assets are on the line, not your personal savings or property.

This is a big deal if you're working with international clients, handling large contracts, or operating in industries with higher legal or financial risks.

Registration and compliance requirements

The registration and compliance process is where sole proprietorship and OPC differ the most.

Registration process for a sole proprietorship

There's no formal registration process to start a sole proprietorship. You can start operating immediately.However, depending on your business activity and turnover, you may need GST registration if your turnover exceeds the threshold, a Shop and Establishment license if you have a physical location, professional tax registration in certain states, and an Import Export Code (IEC) if you're exporting goods or services.

That's it. No annual audits. No board meetings. You just file your income tax return every year.

Registration process for an OPC

Registering an OPC requires more steps. You need to apply for a Digital Signature Certificate (DSC) and a Director Identification Number (DIN), reserve your company name with MCA, file incorporation documents (MOA and AOA), register with the Registrar of Companies (RoC), and obtain PAN and TAN for the company.Once registered, OPCs have ongoing compliance requirements. These include annual financial statements and audits, annual return filing, board meetings and resolutions, and income tax returns for the company.

The compliance burden is higher, but it comes with stronger legal standing and better credibility.

How profits are taxed

Your business structure affects how your income is taxed.

In a sole proprietorship, your business income is treated as personal income. You file under your individual PAN, and profits are taxed according to income tax slabs. Any business expense you claim reduces your taxable income, but the tax calculation happens at the individual level.

For example, if you earn as a freelance consultant, you'll pay tax on that amount based on the slab rates applicable to individuals. You also handle your own TDS (Tax Deducted at Source) and advance tax payments.

In an OPC, the company pays corporate tax, which is a flat rate. The company files its own tax return, separate from your personal return.

You can also take a salary from your OPC (which is tax-deductible for the company), and that salary is taxed as personal income. This gives you some flexibility in structuring your income. Dividends paid by an OPC to the owner are taxable in the owner's hands.

So, which is better? It depends on your income level and how you want to structure withdrawals. Both have their own advantages at different revenue stages.

Sole proprietorship vs. OPC: Which one should you choose?

The right choice depends on where you are now and where you're heading. Here's how you can pick the right option based on your situation.

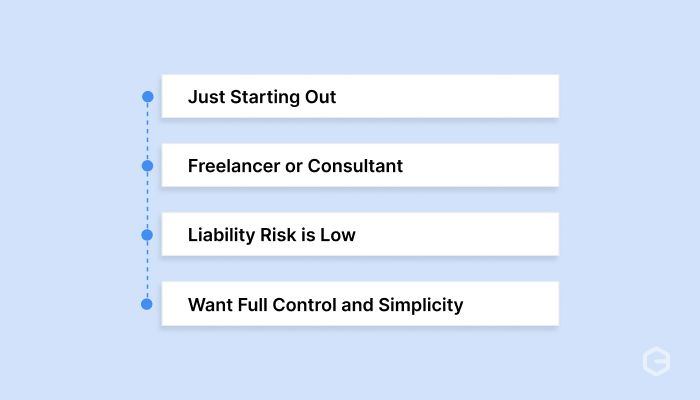

Choose sole proprietorship if:

- You're just starting out: Low or unpredictable income, testing business ideas, and you want to keep costs and paperwork minimal.

- You're a freelancer or consultant: Working solo, no plans to hire a team or raise funding, and you want simple tax filing.

- Your liability risk is low: You're offering services (writing, design, consulting) where legal and financial risks are manageable.

- You want full control and simplicity: No board meetings, no annual filings beyond tax returns, no formal structure.

For example, a freelance content writer earning from international clients doesn't need the complexity of an OPC. A sole proprietorship keeps things lean and manageable.

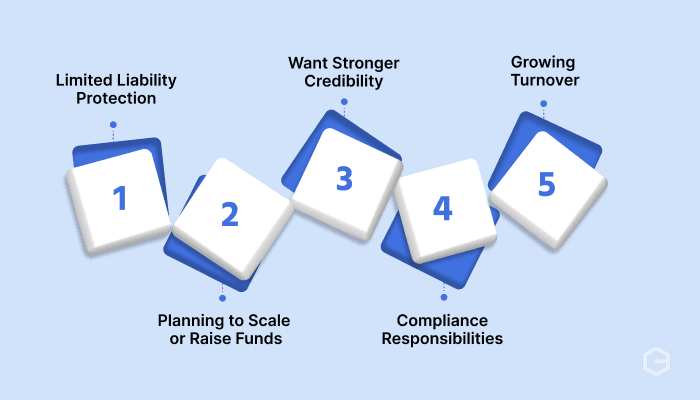

Choose OPC if:

- You want limited liability protection: Your business involves contracts, inventory, employees, or higher financial risk, and you want to protect your personal assets.

- You're planning to scale or raise funds: OPCs can attract investment more easily than sole proprietorships and convert to a private limited company if needed.

- You want stronger credibility: Many international clients, banks, and investors prefer dealing with a registered company over an individual.

- You're prepared to hand compliance responsibilities: You understand that annual filings, audits, and formalities are part of the package.

- Your turnover is growing: If your annual turnover or paid-up capital crosses certain limits, an OPC must convert to a private limited company anyway, so starting with an OPC prepares you for that transition.

For instance, a SaaS founder building a subscription product for global users benefits from OPC's structure. It makes the business look more legitimate, helps with contracts, and prepares for future funding rounds.

Accept global payments faster and easily with PayGlocal

Choosing between sole proprietorship and OPC is an important decision, but it's just the starting point. Once you have your structure, you need a way to collect payments from international clients that's fast, affordable, and compliant.

That's where PayGlocal comes in. PayGlocal is built for Indian businesses doing global work. Whether you're a freelancer, exporter, or growing company, you get everything you need to accept payments from 180+ countries and settle in INR.

Here's what you get:

- Multi-currency accounts: Collect payments in 33+ currencies from clients worldwide.

- Instant FIRC (Foreign Inward Remittance Certificate) on settlement: Stay compliant with all necessary documentation.

- Zero setup fees: You only pay when you do the transaction, with no fixed monthly costs or hidden charges.

- Dynamic checkout: Accept payments through cards, local payment methods, and recurring billing options.

- One platform for everything: Manage all your international payments, compliance documents, and settlements from a single dashboard.

PayGlocal helps you get paid faster, with full transparency, and at rates that make sense for your business, whether you're starting out or scaling internationally.

Final thoughts

Sole proprietorship and OPC both work for solo business owners, but they're designed for different stages, risk levels, and growth goals.

Sole proprietorship gives you simplicity, low costs, and full control. It's perfect if you're just starting, testing ideas, or keeping your business small and manageable. OPC gives you limited liability, a corporate structure, and credibility. It's better if you're working with international clients, handling contracts, or planning to scale.

Neither structure blocks you from accepting international payments or serving global customers. What matters is choosing a structure that fits your current needs and future goals, and ensuring you have the right tools to collect payments smoothly.

Ready to collect globally and settle locally, no matter which structure you choose? Get started with PayGlocal today and take control of your international payments.

FAQs

1. Can a sole proprietorship collect international payments in India?

Yes, you can accept payments from international clients through wire transfers, payment gateways, or platforms like PayGlocal that offer multi-currency accounts. You'll receive an FIRC (Foreign Inward Remittance Certificate) for compliance. However, some larger clients prefer contracting with registered companies instead of individuals.

2. Do I need to register my business to accept international payments?

No formal business registration is required to accept international payments as a sole proprietor. However, you may need GST registration, an Import Export Code (IEC), or a PAN for tax compliance, depending on your activity and turnover. Using a platform like PayGlocal simplifies the process.

3. Which structure is better for freelancers accepting payments from abroad

It depends on your income and risk level. If you're earning less with low liability risk, sole proprietorship keeps things simple. If you're earning more, handling larger contracts, or want limited liability protection, OPC makes more sense.

4. What is the main advantage of OPC over a sole proprietorship?

The main advantage is limited liability protection. In an OPC, your personal assets are protected if the business faces legal issues or debts. Only the company's assets are at risk. In a sole proprietorship, you have unlimited liability, meaning your personal savings and property can be used to settle business debts.

5. Which structure works better for service businesses compared to product businesses?

Both structures work for service and product businesses. The choice depends more on your growth plans and risk level. Service businesses (consulting, design, IT) often start as sole proprietorships because liability is lower. Product businesses sometimes prefer OPC for liability protection if dealing with inventory or suppliers.