Your internet goes down right when a customer wants to pay. Sound familiar? You're not alone. While technology has made payments faster and easier, there are still times when you need backup options like the offline transaction systems that work without an internet connection.

In fact, studies show that 54% of transactions in India still happen through cash at point-of-sale locations, even as digital payments grow rapidly. Offline transactions serve as safety nets when digital systems fail.

Whether it's a simple cash payment or a card swipe that processes later, offline methods ensure you never have to turn away paying customers. Let’s take a closer look at offline transactions, their different types, benefits, and better options for global growth.

An offline transaction is any payment that happens without requiring an active internet connection at the time of purchase.

Instead of processing payments immediately through online networks, these transactions either use physical methods, such as cash, or store digital information locally until the system can connect to banking networks later.

For instance, when a card reader at a small shop loses internet connection, it can still accept card payments by storing the transaction data locally.

The payment gets processed hours later when the connection returns, but the customer can leave immediately with their purchase. The transaction is confirmed once the system reconnects and successfully syncs with the payment network, allowing the issuer to authorize the payment.

These methods often serve as backup options when primary digital systems fail.

When internet connections fail or are unavailable, offline payment systems have smart solutions to keep business moving. Here’s how it works:

Offline is great as a backup. But if you're collecting payments from clients overseas or need multi-currency, low-friction options, switch to platforms like PayGlocal. You can collect in USD, EUR, GBP, and settle in INR without any hassle.

Businesses use different offline payment methods depending on their needs, customer preferences, and the situation they're operating in. Here's a comparison of the most common offline payment methods:

Studies show that 62% of Indians still visit physical stores for shopping discovery, highlighting the continued importance of offline payment acceptance for retail businesses.

Each offline transaction method has specific advantages and works better in certain situations:

Cash remains the most straightforward offline payment method. No technology required, just physical money changing hands. It works everywhere and gives customers immediate proof of purchase through receipts.

For instance, a local grocery store can serve customers even during complete power outages, accepting cash and manually recording sales in a logbook.

Cash payments offer complete independence from digital systems but create challenges for businesses trying to track sales, manage inventory, or serve customers who don't carry physical money. Many retailers still keep cash as a backup option while focusing on digital methods for daily operations.

Cheques involve written instructions to banks for transferring money from one account to another. They're commonly used for larger business transactions where companies need paper trails and formal payment records.

For example, a manufacturing company pays suppliers using company cheques that require authorized signatures and provide clear audit trails for accounting teams.

While cheques offer good security and legal protection, they're slow to process and carry risks of bouncing if insufficient funds are available.

Manual bank transfers happen when someone visits a bank branch to initiate money transfers using paper forms and bank staff assistance. These transfers use systems like NEFT or RTGS but require physical presence rather than online banking.

For instance, a small business owner visits their bank monthly to process supplier payments that require special authorization or documentation.

This method works well for businesses that need human verification for large payments or operate in areas where online banking isn't widely adopted. The process ensures proper documentation and verification for high-value transactions.

Offline card processing happens when payment terminals can't connect to banking networks but still accept card payments by storing transaction data locally. The terminal captures card information, processes the payment authorization offline using stored rules, and uploads everything once connectivity returns.

For example, a food truck operating in remote areas can accept card payments all day and process them when returning to areas with network coverage.

These systems work well as backup options but carry a higher risk since they can't verify account balances in real-time. Some transactions fail later if customers don't have sufficient funds when the processing finally happens.

Offline UPI allows people with basic feature phones to make digital payments without internet connectivity. The system works through USSD codes that connect directly to telecom networks rather than requiring data connections.

For instance, a farmer at a remote market can pay vendors using simple codes dialed on their feature phone, with the transaction processing through cellular networks.

This technology bridges the gap between digital convenience and rural accessibility, helping businesses serve customers who have limited access to smartphones or reliable internet connections. It's particularly useful for businesses serving rural markets where smartphone adoption remains limited.

Offline transactions provide important advantages that keep businesses running smoothly in challenging situations. Here are the main benefits businesses gain from accepting offline payments:

Both online and offline payment types help businesses choose the right mix for their operations and customer needs. Here's how these transactions compare across key factors:

While offline methods serve important backup roles, businesses serious about global expansion need reliable online payment solutions that work globally across different currencies, and time zones.

Building for global scale? Relying on offline won’t get you there. If you're exporting services or goods, you need payments that are trackable, tax-compliant, and fast, from freelance to enterprise invoices. That’s where PayGlocal comes in.

Here are some of the ways it solves offline payment limitations:

Whether you're scaling a travel platform or invoicing an international client, PayGlocal helps you get paid faster, clearer, and in your preferred currency.

Offline transactions still matter in certain environments but they're often slow and hard to scale. They work as backup options during emergencies or for serving customers in areas with limited connectivity, but they shouldn't be your primary strategy for business growth.

If you're doing business internationally or want to improve your success rates, global-first online solutions are the way forward. Modern payment systems offer better tracking, faster processing, and the reliability needed for international commerce.

Make your payments smarter, no matter where your clients are. Ready to collect globally, settle locally, and grow confidently? Get started with PayGlocal today.

In fact, studies show that 54% of transactions in India still happen through cash at point-of-sale locations, even as digital payments grow rapidly. Offline transactions serve as safety nets when digital systems fail.

Whether it's a simple cash payment or a card swipe that processes later, offline methods ensure you never have to turn away paying customers. Let’s take a closer look at offline transactions, their different types, benefits, and better options for global growth.

Key Takeaways:

- Offline transactions work without the internet: They often involve delays and manual processes that can slow your business down.

- Multiple offline methods exist: These include cash, checks, and card terminals that store data locally until they reconnect.

- Benefits include business continuity: Offline methods keep business running during outages, but lack the tracking and scalability needed for global growth.

- Smart businesses use solutions like PayGlocal to collect payments: This allows them to serve international customers reliably with high success rates and real-time tracking.

What is an offline transaction?

An offline transaction is any payment that happens without requiring an active internet connection at the time of purchase.

Instead of processing payments immediately through online networks, these transactions either use physical methods, such as cash, or store digital information locally until the system can connect to banking networks later.

For instance, when a card reader at a small shop loses internet connection, it can still accept card payments by storing the transaction data locally.

The payment gets processed hours later when the connection returns, but the customer can leave immediately with their purchase. The transaction is confirmed once the system reconnects and successfully syncs with the payment network, allowing the issuer to authorize the payment.

These methods often serve as backup options when primary digital systems fail.

How does an offline transaction work?

When internet connections fail or are unavailable, offline payment systems have smart solutions to keep business moving. Here’s how it works:

- Transaction is initiated: A customer wants to pay using a card at a POS terminal that has lost network connection, or makes a cash payment that needs manual recording.

- Data is stored locally: The payment terminal saves transaction details like card information, amount, and time stamp in its internal memory for processing later.

- Risk thresholds are applied: The system checks if the transaction amount falls within safe limits set by the merchant or card network to reduce fraud risk.

- System reconnects later: When the internet returns, the terminal automatically connects to banking networks and uploads all stored transaction data.

- Transaction is submitted and processed: Banks verify the payments, check account balances, and complete the money transfers, sending confirmations back to merchants.

Offline is great as a backup. But if you're collecting payments from clients overseas or need multi-currency, low-friction options, switch to platforms like PayGlocal. You can collect in USD, EUR, GBP, and settle in INR without any hassle.

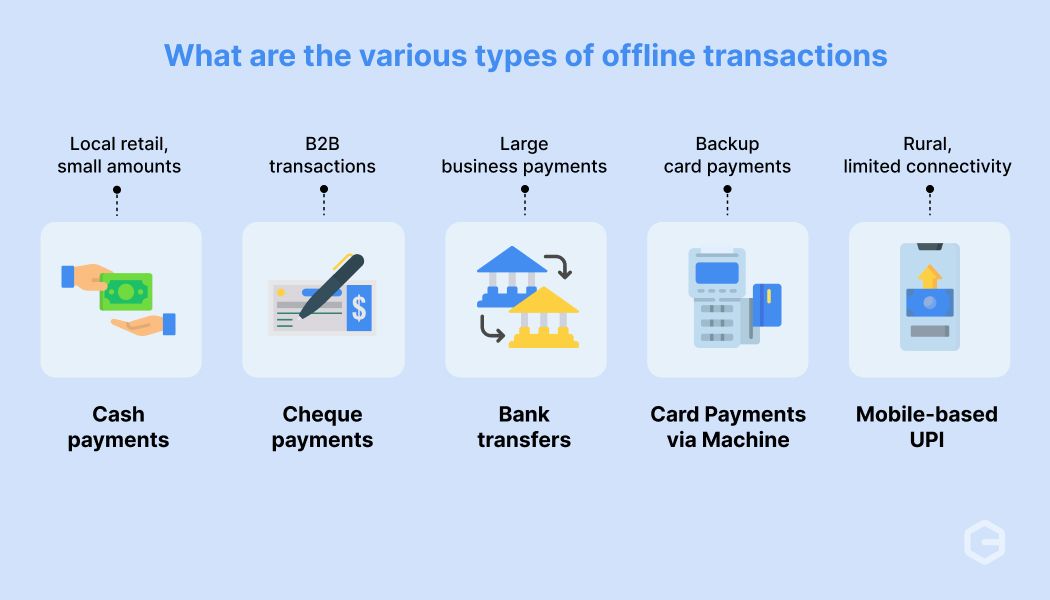

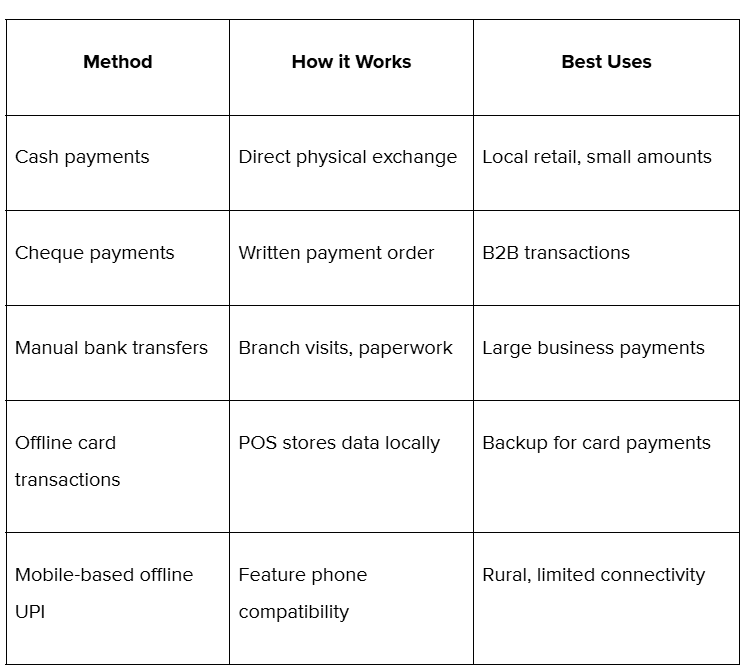

What are the various types of offline transactions?

Businesses use different offline payment methods depending on their needs, customer preferences, and the situation they're operating in. Here's a comparison of the most common offline payment methods:

Studies show that 62% of Indians still visit physical stores for shopping discovery, highlighting the continued importance of offline payment acceptance for retail businesses.

Each offline transaction method has specific advantages and works better in certain situations:

Cash payments

Cash remains the most straightforward offline payment method. No technology required, just physical money changing hands. It works everywhere and gives customers immediate proof of purchase through receipts.

For instance, a local grocery store can serve customers even during complete power outages, accepting cash and manually recording sales in a logbook.

Cash payments offer complete independence from digital systems but create challenges for businesses trying to track sales, manage inventory, or serve customers who don't carry physical money. Many retailers still keep cash as a backup option while focusing on digital methods for daily operations.

Cheque payments

Cheques involve written instructions to banks for transferring money from one account to another. They're commonly used for larger business transactions where companies need paper trails and formal payment records.

For example, a manufacturing company pays suppliers using company cheques that require authorized signatures and provide clear audit trails for accounting teams.

While cheques offer good security and legal protection, they're slow to process and carry risks of bouncing if insufficient funds are available.

Manual bank transfers

Manual bank transfers happen when someone visits a bank branch to initiate money transfers using paper forms and bank staff assistance. These transfers use systems like NEFT or RTGS but require physical presence rather than online banking.

For instance, a small business owner visits their bank monthly to process supplier payments that require special authorization or documentation.

This method works well for businesses that need human verification for large payments or operate in areas where online banking isn't widely adopted. The process ensures proper documentation and verification for high-value transactions.

Offline card transactions

Offline card processing happens when payment terminals can't connect to banking networks but still accept card payments by storing transaction data locally. The terminal captures card information, processes the payment authorization offline using stored rules, and uploads everything once connectivity returns.

For example, a food truck operating in remote areas can accept card payments all day and process them when returning to areas with network coverage.

These systems work well as backup options but carry a higher risk since they can't verify account balances in real-time. Some transactions fail later if customers don't have sufficient funds when the processing finally happens.

Mobile-based offline UPI transaction

Offline UPI allows people with basic feature phones to make digital payments without internet connectivity. The system works through USSD codes that connect directly to telecom networks rather than requiring data connections.

For instance, a farmer at a remote market can pay vendors using simple codes dialed on their feature phone, with the transaction processing through cellular networks.

This technology bridges the gap between digital convenience and rural accessibility, helping businesses serve customers who have limited access to smartphones or reliable internet connections. It's particularly useful for businesses serving rural markets where smartphone adoption remains limited.

What are the benefits of offline transactions?

Offline transactions provide important advantages that keep businesses running smoothly in challenging situations. Here are the main benefits businesses gain from accepting offline payments:

- Business continuity: You can still accept payments during internet failures, power outages, or system maintenance. This prevents lost sales and keeps customers happy even when technology doesn't cooperate.

- Remote-friendly: Offline methods work in areas with poor or no internet connectivity, helping businesses serve customers in rural locations or during travel to remote areas.

- Customer trust: Many people feel more comfortable with familiar payment methods like cash or cheques, especially for large purchases or in industries where personal relationships matter more than convenience.

- Fallback in emergencies: When digital payment systems experience outages or security issues, offline methods ensure business operations can continue without interruption.

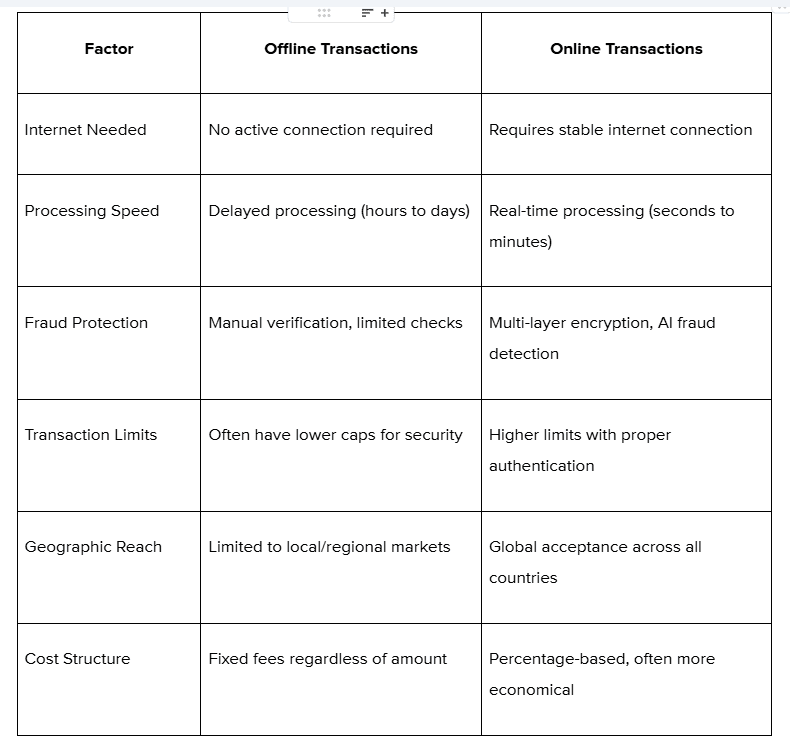

What is the difference between offline and online transactions?

Both online and offline payment types help businesses choose the right mix for their operations and customer needs. Here's how these transactions compare across key factors:

While offline methods serve important backup roles, businesses serious about global expansion need reliable online payment solutions that work globally across different currencies, and time zones.

Move beyond offline limits with PayGlocal

Building for global scale? Relying on offline won’t get you there. If you're exporting services or goods, you need payments that are trackable, tax-compliant, and fast, from freelance to enterprise invoices. That’s where PayGlocal comes in.

Here are some of the ways it solves offline payment limitations:

- Collect in 33+ currencies: Accept payments from 180+ countries through our alternate payment methods without worrying about local payment method compatibility or currency conversion hassles.

- Local accounts in USD, GBP, EUR, CAD: Look local to your international clients through multi-currency accounts while maintaining one unified system for all your global collections.

- Instant compliance docs: Auto-FIRA generation eliminates paperwork delays and ensures you meet Indian regulations for international transactions without manual effort.

- Track every payment: Transparent dashboards with fund status alerts through our international payments platform mean you always know where your money is and when it will arrive.

- Zero fixed cost: Pay only when you transact through our transparent pricing, making it affordable for businesses of all sizes to accept global payments professionally.

Whether you're scaling a travel platform or invoicing an international client, PayGlocal helps you get paid faster, clearer, and in your preferred currency.

Final thoughts

Offline transactions still matter in certain environments but they're often slow and hard to scale. They work as backup options during emergencies or for serving customers in areas with limited connectivity, but they shouldn't be your primary strategy for business growth.

If you're doing business internationally or want to improve your success rates, global-first online solutions are the way forward. Modern payment systems offer better tracking, faster processing, and the reliability needed for international commerce.

Make your payments smarter, no matter where your clients are. Ready to collect globally, settle locally, and grow confidently? Get started with PayGlocal today.