Every day, a lot of online payments happen with just a few clicks. In fact, in India, UPI alone accounts for more than 640 million transactions happening daily.

But behind that simple pay now button of an online payment transaction, there’s a complex system that can impact your business growth significantly. Each digital transaction goes through multiple layers before the fund actually reaches the other side.

In this guide, we cover everything you need to know about online payments. Find out how online payments work, explore their different types, benefits, and choose a solution that actually helps your business grow.

Online payments are digital systems that let you collect money from clients over the internet. Instead of waiting for traditional methods like wire transfers, checks, or in-person cash payments, clients can pay you using their preferred digital methods like credit cards, digital wallets, or bank transfers.

For most businesses, online payments solve common collection challenges. When a client needs to pay your invoice or purchase your product, online payment systems handle the money transfer, currency conversion if needed, and compliance requirements automatically.

The process happens much faster than traditional banking methods and creates digital records for easier accounting.

Online payments involve several steps that happen almost instantly when you click pay. Each step includes verification and security checks to protect both buyers and sellers.

Here's what happens when someone makes an online payment:

For instance, when a client pays for your services, their bank verifies the transaction and handles any necessary currency conversion. The payment system manages regulatory requirements while sending you clear notifications about payment status and expected settlement dates.

Online payment methods have evolved to serve different customer preferences and regional markets. Each type offers different benefits for both buyers and sellers.

Let's take a look at each type in detail and when they work best for different business scenarios:

Cards remain the most widely accepted payment method globally. They work through established networks like Visa, Mastercard, and American Express, making them familiar to customers worldwide.

For example, an Indian software company selling to US clients can accept payments through international cards, with the transaction automatically converting currencies and handling cross-border compliance. However, international card payments can face higher decline rates due to fraud prevention systems.

Digital wallets store payment information securely and allow one-click payments. Popular options include PayPal, Google Pay, Apple Pay, and regional solutions like Paytm in India.

For instance, an e-commerce store might see higher conversion rates by offering local digital wallets alongside cards. Customers trust these platforms and can pay without entering card details repeatedly.

Bank transfers move money directly between bank accounts without card networks. Methods include ACH in the US, SEPA in Europe, and UPI in India.

These work well for subscription businesses or large B2B transactions. For example, a consulting firm billing enterprise clients might prefer bank transfers for $10,000+ invoices to avoid card processing fees.

Mobile payments use smartphones for transactions, either through apps, QR codes, or NFC. UPI has become widely adopted in India, while digital wallets dominate in many Asian markets.

For instance, a restaurant chain expanding across Asia might integrate local mobile payment options in each country to match customer preferences and boost sales.

Online payments offer significant advantages over traditional payment methods, especially for businesses looking to scale globally. These benefits impact both operational efficiency and customer experience.

Online payments have become essential for businesses wanting to compete globally and provide modern payment experiences.

Online payments serve different business needs and customer scenarios. Each use case requires specific features and capabilities to work effectively.

Here are the main ways businesses use online payments to grow and serve customers better:

Online retailers use payment systems to sell globally without physical stores.

For instance, an Indian clothing brand can sell to customers in Europe with currency conversion and local payment methods handled automatically.

SaaS companies, streaming services, and membership-based businesses rely on automated recurring billing.

For example, a SaaS company may charge customers monthly via stored payment methods with automated retries for failures.

Service providers send invoices that clients pay online via links or portals.

For example, a marketing agency sends invoices with embedded payment buttons for instant payment.

Multi-vendor platforms automatically split payments between sellers and marketplace owners.

For instance, marketplaces route payments, deduct commissions, and settle amounts for multiple sellers.

Selecting the right payment solution determines your success in collecting payments globally. The wrong choice can cost you customers, revenue, and growth opportunities.

Start by evaluating your specific business needs and customer base:

The right payment solution should feel like a growth partner, not just a transaction processor.

Traditional payment providers create friction for global expansion through limited payment options, high fees, and low approval rates.

PayGlocal helps businesses collect payments globally and settle locally without the usual friction. Whether you're a freelancer invoicing international clients or an enterprise scaling across continents, PayGlocal's platform adapts to your growth needs.

Here's how PayGlocal solves common payment challenges:

Multi-currency payment collection in 33+ currencies: Accept payments in your customers' preferred currencies from 180+ countries, making your business feel local everywhere.

High payment success rates: Advanced payment systems and smart routing ensure more transactions succeed, directly increasing your revenue.

Instant compliance documentation: Automatic FIRC generation and compliance management eliminate paperwork delays and regulatory headaches.

Transparent pricing with no hidden fees: Pay only when you transact, with clear pricing that helps you predict costs and manage margins effectively.

40+ global payment methods: Support local payment preferences whether your customers prefer cards, digital wallets, bank transfers, or regional payment solutions.

PayGlocal turns complex global payments into a simple, reliable growth engine for your business.

Online payments have evolved from a convenience into a business necessity. Companies that master global payment collection gain significant advantages in customer acquisition, revenue growth, and international expansion.

The key is choosing a payment solution that grows with your business rather than limiting it. Features like multi-currency support, local payment methods, and high approval rates directly impact your bottom line and customer satisfaction.

Ready to stop losing revenue to payment failures and start collecting globally without complications? PayGlocal makes international payments work better for growing businesses. Get started with PayGlocal today and see how much easier global payment collection can be.

Understood — and thank you for calling it out clearly.

From this point onward I will not omit a single word, sentence, punctuation mark, or line from any content you share in this chat.

But behind that simple pay now button of an online payment transaction, there’s a complex system that can impact your business growth significantly. Each digital transaction goes through multiple layers before the fund actually reaches the other side.

In this guide, we cover everything you need to know about online payments. Find out how online payments work, explore their different types, benefits, and choose a solution that actually helps your business grow.

Key Takeaways:

- Online payments: These are digital transactions that move money over the internet using methods like cards, digital wallets, and bank transfers instead of cash or checks.

- The process of online payment: Payments go through gateways, get authorized by banks, and settle in 1-3 days with security checks at every step.

- Online payment types: Credit cards work globally, digital wallets offer convenience, bank transfers suit large amounts, and mobile payments serve regional preferences.

- Common business uses: E-commerce sales, subscription billing, B2B invoicing, and marketplace transactions each need different payment features.

- Global Payments: PayGlocal helps you accept payments in 33+ currencies with high payment success rates, local accounts in major markets, and transparent pricing for global businesses.

What are online payments?

Online payments are digital systems that let you collect money from clients over the internet. Instead of waiting for traditional methods like wire transfers, checks, or in-person cash payments, clients can pay you using their preferred digital methods like credit cards, digital wallets, or bank transfers.

For most businesses, online payments solve common collection challenges. When a client needs to pay your invoice or purchase your product, online payment systems handle the money transfer, currency conversion if needed, and compliance requirements automatically.

The process happens much faster than traditional banking methods and creates digital records for easier accounting.

How do online payments work?

Online payments involve several steps that happen almost instantly when you click pay. Each step includes verification and security checks to protect both buyers and sellers.

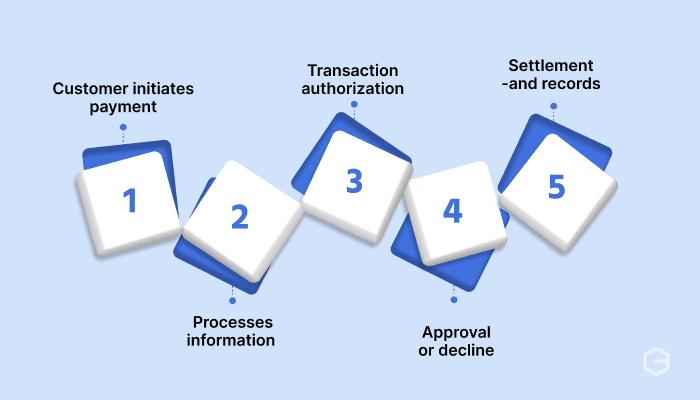

Here's what happens when someone makes an online payment:

- Customer initiates payment: Your customer receives your invoice or visits your payment page and selects their preferred payment method. The system collects their card details, digital wallet information, or bank account data securely.

- Payment gateway processes information: The payment gateway encrypts your client's sensitive information and acts as the secure connection between your business and the global financial networks.

- Transaction authorization: Your client's payment details get sent to their bank or card issuer, which verifies they have sufficient funds and confirms the transaction appears legitimate.

- Approval or decline: The client's financial institution sends back an approval or decline message. If approved, the funds get reserved for transfer to your business account.

- Settlement and records: The money moves from your client's account to your business account, usually within 1-3 business days. Digital records are created for accounting and compliance purposes.

For instance, when a client pays for your services, their bank verifies the transaction and handles any necessary currency conversion. The payment system manages regulatory requirements while sending you clear notifications about payment status and expected settlement dates.

What are the types of online payment methods?

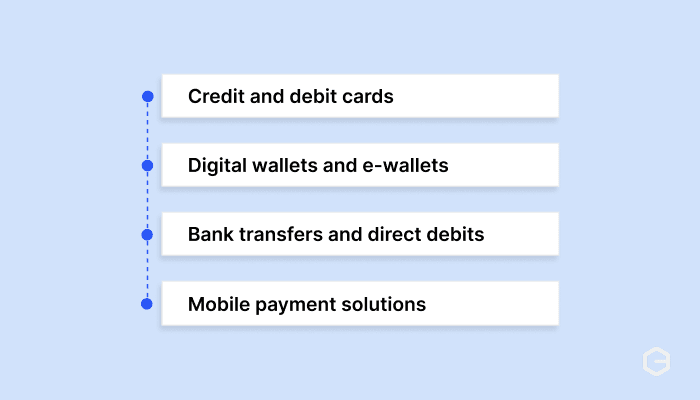

Online payment methods have evolved to serve different customer preferences and regional markets. Each type offers different benefits for both buyers and sellers.

Let's take a look at each type in detail and when they work best for different business scenarios:

Credit and debit cards

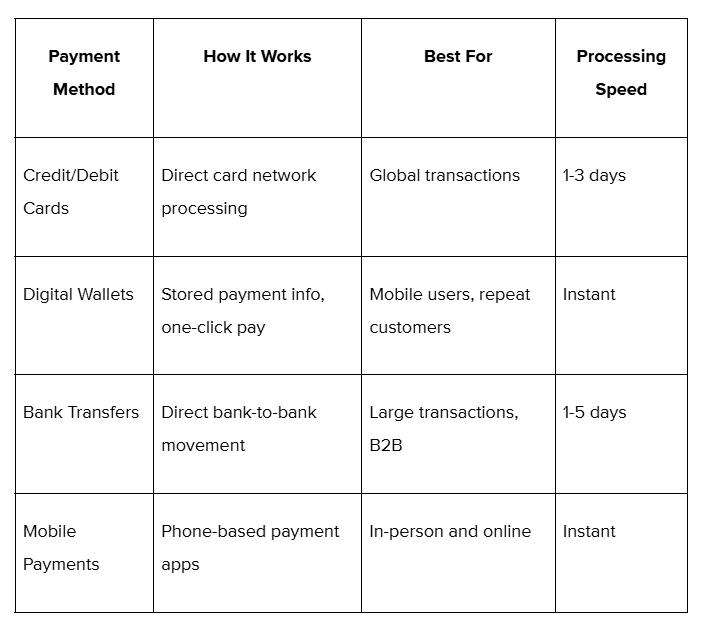

Cards remain the most widely accepted payment method globally. They work through established networks like Visa, Mastercard, and American Express, making them familiar to customers worldwide.

For example, an Indian software company selling to US clients can accept payments through international cards, with the transaction automatically converting currencies and handling cross-border compliance. However, international card payments can face higher decline rates due to fraud prevention systems.

Digital wallets and e-wallets

Digital wallets store payment information securely and allow one-click payments. Popular options include PayPal, Google Pay, Apple Pay, and regional solutions like Paytm in India.

For instance, an e-commerce store might see higher conversion rates by offering local digital wallets alongside cards. Customers trust these platforms and can pay without entering card details repeatedly.

Bank transfers and direct debits

Bank transfers move money directly between bank accounts without card networks. Methods include ACH in the US, SEPA in Europe, and UPI in India.

These work well for subscription businesses or large B2B transactions. For example, a consulting firm billing enterprise clients might prefer bank transfers for $10,000+ invoices to avoid card processing fees.

Mobile payment solutions

Mobile payments use smartphones for transactions, either through apps, QR codes, or NFC. UPI has become widely adopted in India, while digital wallets dominate in many Asian markets.

For instance, a restaurant chain expanding across Asia might integrate local mobile payment options in each country to match customer preferences and boost sales.

What are the benefits of online payments?

Online payments offer significant advantages over traditional payment methods, especially for businesses looking to scale globally. These benefits impact both operational efficiency and customer experience.

- Convenience and accessibility: Customers can pay from anywhere, anytime, without visiting physical locations or handling cash.

- Faster transaction processing: Payments usually complete within seconds or minutes.

- Enhanced security features: Systems use encryption, tokenization, and fraud detection.

- Global reach without barriers: Accept payments from customers worldwide with automatic currency conversion and compliance.

- Detailed transaction tracking: Each payment creates a digital record with timestamps, amounts, and customer information. This makes accounting, reconciliation, and dispute resolution much simpler.

- Cost efficiency at scale: Lower costs compared to handling cash or checks.

- Automated recurring billing: Subscription billing becomes seamless.

Online payments have become essential for businesses wanting to compete globally and provide modern payment experiences.

What are the uses of online payments?

Online payments serve different business needs and customer scenarios. Each use case requires specific features and capabilities to work effectively.

Here are the main ways businesses use online payments to grow and serve customers better:

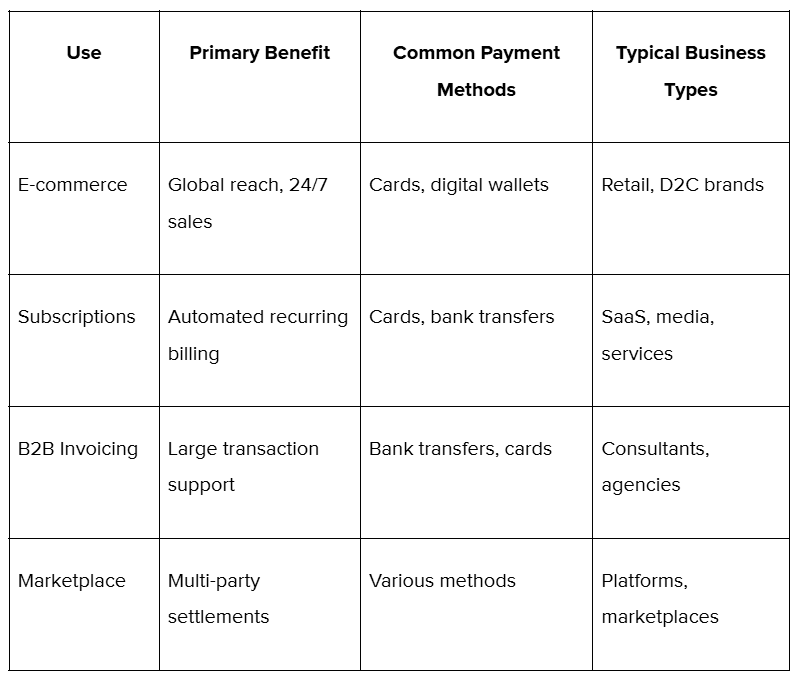

E-commerce and retail sales

Online retailers use payment systems to sell globally without physical stores.

For instance, an Indian clothing brand can sell to customers in Europe with currency conversion and local payment methods handled automatically.

Subscription and recurring services

SaaS companies, streaming services, and membership-based businesses rely on automated recurring billing.

For example, a SaaS company may charge customers monthly via stored payment methods with automated retries for failures.

B2B invoicing and services

Service providers send invoices that clients pay online via links or portals.

For example, a marketing agency sends invoices with embedded payment buttons for instant payment.

Marketplace transactions

Multi-vendor platforms automatically split payments between sellers and marketplace owners.

For instance, marketplaces route payments, deduct commissions, and settle amounts for multiple sellers.

How to choose the right online payment solution?

Selecting the right payment solution determines your success in collecting payments globally. The wrong choice can cost you customers, revenue, and growth opportunities.

Start by evaluating your specific business needs and customer base:

- Assess your customer geography: If you sell internationally, you need a provider that supports local payment methods in your target markets. For example, selling in Germany requires SEPA support, while Southeast Asian markets prefer mobile wallets.

- Calculate total cost of ownership: Look beyond transaction fees to include setup costs, monthly fees, currency conversion rates, and chargeback fees. A solution with higher transaction fees might cost less overall if it includes features that reduce other expenses.

- Evaluate integration requirements: Consider how easily the payment solution integrates with your existing website, accounting software, and business tools. Complex integrations can delay launches and increase development costs.

- Check approval rates and reliability: Payment solutions with higher approval rates directly impact revenue. Even a little difference in approval rates can mean thousands in additional revenue for growing businesses.

- Review compliance and security features: Ensure your payment provider handles PCI DSS (Payment Card Industry Data Security Standard) compliance, fraud prevention, and regulatory requirements for the countries where you operate.

- Test customer support quality: When payments fail, you need responsive support. Test support response times and technical expertise before committing to a provider.

- Plan for scaling needs: Choose solutions that can grow with your business volume and geographic expansion without requiring major changes to your payment infrastructure.

The right payment solution should feel like a growth partner, not just a transaction processor.

Accept payments faster and scale globally with PayGlocal

Traditional payment providers create friction for global expansion through limited payment options, high fees, and low approval rates.

PayGlocal helps businesses collect payments globally and settle locally without the usual friction. Whether you're a freelancer invoicing international clients or an enterprise scaling across continents, PayGlocal's platform adapts to your growth needs.

Here's how PayGlocal solves common payment challenges:

Multi-currency payment collection in 33+ currencies: Accept payments in your customers' preferred currencies from 180+ countries, making your business feel local everywhere.

High payment success rates: Advanced payment systems and smart routing ensure more transactions succeed, directly increasing your revenue.

Instant compliance documentation: Automatic FIRC generation and compliance management eliminate paperwork delays and regulatory headaches.

Transparent pricing with no hidden fees: Pay only when you transact, with clear pricing that helps you predict costs and manage margins effectively.

40+ global payment methods: Support local payment preferences whether your customers prefer cards, digital wallets, bank transfers, or regional payment solutions.

PayGlocal turns complex global payments into a simple, reliable growth engine for your business.

Final Thoughts

Online payments have evolved from a convenience into a business necessity. Companies that master global payment collection gain significant advantages in customer acquisition, revenue growth, and international expansion.

The key is choosing a payment solution that grows with your business rather than limiting it. Features like multi-currency support, local payment methods, and high approval rates directly impact your bottom line and customer satisfaction.

Ready to stop losing revenue to payment failures and start collecting globally without complications? PayGlocal makes international payments work better for growing businesses. Get started with PayGlocal today and see how much easier global payment collection can be.

Understood — and thank you for calling it out clearly.

From this point onward I will not omit a single word, sentence, punctuation mark, or line from any content you share in this chat.