India’s digital payments landscape is experiencing unprecedented growth, with the market projected to triple from $131 billion in FY24 to $439 billion by FY29. This surge is driven mainly by the widespread adoption of the Unified Payments Interface (UPI), which now accounts for over 80% of retail digital transactions in the country.

Amid this expansion, Payment Aggregators (PAs) have emerged as key players, facilitating digital transactions for businesses and consumers. However, as the volume of transactions escalates, so does the need for robust regulatory frameworks to ensure security, transparency, and consumer protection.

In this blog, we delve into the role of Payment Aggregators in India's digital payment ecosystem and explore the regulatory landscape that governs their operations.

Payment Aggregators (PAs) are third-party service providers that allow businesses to accept, process, and manage payments on their behalf. They act as intermediaries between merchants and financial institutions, streamlining the payment process and making it easier for businesses to accept multiple types of payments (credit/debit cards, digital wallets, UPI, etc.) without establishing individual payment gateways with each financial provider.

The role of a payment aggregator is key for businesses to accept payments from customers through various channels, such as cards, wallets, UPI, and fraud detection. Here's a breakdown of their key roles:

A Payment Aggregator (PA) facilitates the transfer of funds from the customer to the merchant, handling the entire transaction process, from payment authorization to settlement and the fund transfer.

PAs onboard businesses to accept digital payments without setting up separate agreements, thus simplifying the process for merchants for documentation collection and verification, merchant nodal codes setup process, activation & maintenance activities.

They offer a single platform on which merchants can accept multiple types of payments (credit cards, debit cards, e-wallets, UPI, etc.) and even local payment methods for global transactions.

Payment aggregators manage and track all transactions for merchants, ideally with a dashboard that offers detailed reports on payment activities, manages payments, refunds, and chargebacks.

PAs ensure that transactions are secure by following industry standards such as PCI-DSS (Payment Card Industry Data Security Standard), fraud detection protocols, and regulatory requirements, safeguarding merchants and customers.

PAs integrate payment options directly into the merchant's website or app, eliminating the need for customers to be redirected to external pages. This integration reduces friction during checkout, increases conversion rates, and minimizes cart abandonment.

PayGlocal, a leading payments platform from India, has introduced its innovative product, 'Xpress PayFlow', designed to streamline card payments for merchants. This solution allows customers to enter their card details directly on the platform, eliminating the need for redirection to third-party pages.

It is important to understand how payment aggregators work because they play a central role in streamlining the payment process, ensuring the smooth flow of transactions, and safeguarding business and customer data.

The process begins with merchants signing up for payment aggregator services. During onboarding, merchants provide essential business information, submit identification and banking documents, and undergo a risk assessment.

They also agree to the aggregator’s terms and conditions before proceeding w.r.t transaction fees, settlement timelines, dispute resolution, and compliance with data security standards.

Once the merchant is onboarded, the payment aggregator equips them with the necessary tools to integrate payment functionality into their sales channels, such as websites and mobile apps.

This also involves APIs or plugins that ensure secure data transmission between the merchant's platform and the aggregator’s system.

When a customer purchases, the payment aggregator processes the transaction by securely capturing and encrypting the customer’s payment details.

The encrypted data is then tokenized, replacing sensitive information with a unique identifier or "token," which can be safely used for transaction processing without exposing actual card details. This method protects customer information, thus shielding it from fraud and data breaches.

After deducting the fees, the payment aggregator holds the funds in a settlement account. Funds from multiple transactions are aggregated and transferred to the merchant’s designated bank account after a predefined settlement period, such as daily or weekly.

In International transactions, PayGlocal provides merchants with electronic Foreign Inward Remittance Certificates (eFIRCs) for cross-border transactions, aiding in compliance with regulatory requirements.

Payment aggregators play a critical role in managing risks by using tools to detect fraud, monitor suspicious activity, and comply with industry regulations like PCI DSS to ensure secure and reliable payment processing.

To mitigate risks, payment aggregators implement a risk management framework. This framework includes conducting thorough Know Your Customer (KYC) checks and assessing the merchant's business model, transaction volume, and industry risk profile.

Payment aggregators offer merchants access to valuable reports and analytics, enabling them to track transactions, monitor sales, and gain insights into business performance.

The reporting and Advanced analytics features must also allow merchants to identify patterns in customer spending, monitor chargeback rates, and assess the effectiveness of promotional campaigns.

Additionally, these insights assist in optimizing cash flow management and improving overall business performance.

Also Read: Understanding Chargeback Fraud: Insights and Prevention Strategies

Recognizing different types of payment aggregators will help you choose the most suitable one based on your requirements.

Non-banking entities approved by the Reserve Bank of India (RBI) serve as payment aggregators and intermediaries between merchants and financial institutions. These aggregators are specialists in payment processing and facilitate transactions.

Examples of prominent non-bank payment aggregators in India include PayU and Instamojo.

Large e-commerce platforms like Amazon, Flipkart, and Snapdeal operate their own payment aggregation systems. These platforms help merchants to process payments, offering integrated solutions for businesses to accept online payments directly from customers.

Mobile wallet providers in India, like Paytm and Google Pay, also function as payment aggregators. These platforms allow businesses to accept payments through mobile wallets, whether online or in-store, by integrating with their respective payment systems.

They have become pivotal in facilitating international transactions, especially for businesses engaged in global trade. These entities bridge the gap between merchants and financial institutions, ensuring seamless and secure cross-border payments. Example: Payglocal that supports international payment needs in 33+ currencies.

Also Read: Zero-Knowledge Proof: Redefining Data Privacy

Both of these payment providers differ in their functionality. As a business, it’s important for you to understand these differences so that you're selecting the right solution for your payment needs.

The Indian payment aggregator landscape is constantly evolving, with new players likely to emerge in the future. Understanding the regulatory framework is crucial, as it ensures compliance.

In the News: How PayGlocal Is Bridging The Gap Between Indian Businesses And The Global Market - BW Businessworld

PayGlocal is a payment aggregator that offers secure, compliant, and efficient international payment solutions for your business. With its robust infrastructure and adherence to India's stringent regulatory standards, PayGlocal simplifies cross-border payments, allowing you to accept payments in 30+ currencies.

Here are some key features that make PayGlocal the ideal choice for your payment aggregation needs:

You get access to a dashboard that provides real-time analytics and insights into your transactions. This tool allows you to track your sales performance, identify trends, and optimize strategies, helping you make informed business decisions.

Integrated by PayGlocal, is a robust sanction screening solution that simplifies navigating the complexities of global markets. This privacy-first Zero-Knowledge Proof (ZKP) solution ensures your business remains compliant with international regulations while securing sensitive customer data.

Managing recurring payments and subscriptions is made easy with PayGlocal. The platform provides tailored solutions for subscription-based businesses, allowing you to set up and manage recurring payments efficiently, ensuring smooth transactions for both you and your customers.

This feature enables you to accept payments through UPI, digital wallets, and other local payment systems like Giropay for Germany, Grabpay for Singapore and more.

Understanding the regulatory and operational aspects of payment aggregators is crucial for businesses to navigate the complexities of digital payment systems effectively. By comprehending the legal requirements, compliance standards, and technical features, businesses can ensure seamless payment processing, reduce risks, and enhance customer satisfaction. Strategically using payment aggregators can further help in your payment processes, reduce operational costs, and allow you to focus on core business activities.

Choose PayGlocal as your trusted payment aggregator for secure, and scalable payment solutions for your business. Start optimizing your payment processes today and take your business to the next level! Get Started Now!

Amid this expansion, Payment Aggregators (PAs) have emerged as key players, facilitating digital transactions for businesses and consumers. However, as the volume of transactions escalates, so does the need for robust regulatory frameworks to ensure security, transparency, and consumer protection.

In this blog, we delve into the role of Payment Aggregators in India's digital payment ecosystem and explore the regulatory landscape that governs their operations.

What are Payment Aggregators?

Payment Aggregators (PAs) are third-party service providers that allow businesses to accept, process, and manage payments on their behalf. They act as intermediaries between merchants and financial institutions, streamlining the payment process and making it easier for businesses to accept multiple types of payments (credit/debit cards, digital wallets, UPI, etc.) without establishing individual payment gateways with each financial provider.

Key Benefits of an Online Payment Aggregator

The role of a payment aggregator is key for businesses to accept payments from customers through various channels, such as cards, wallets, UPI, and fraud detection. Here's a breakdown of their key roles:

Payment Processing

A Payment Aggregator (PA) facilitates the transfer of funds from the customer to the merchant, handling the entire transaction process, from payment authorization to settlement and the fund transfer.

Merchant Onboarding

PAs onboard businesses to accept digital payments without setting up separate agreements, thus simplifying the process for merchants for documentation collection and verification, merchant nodal codes setup process, activation & maintenance activities.

Multi-payment Acceptance

They offer a single platform on which merchants can accept multiple types of payments (credit cards, debit cards, e-wallets, UPI, etc.) and even local payment methods for global transactions.

Transaction Management

Payment aggregators manage and track all transactions for merchants, ideally with a dashboard that offers detailed reports on payment activities, manages payments, refunds, and chargebacks.

Security and Compliance

PAs ensure that transactions are secure by following industry standards such as PCI-DSS (Payment Card Industry Data Security Standard), fraud detection protocols, and regulatory requirements, safeguarding merchants and customers.

Smooth Checkout Experience

PAs integrate payment options directly into the merchant's website or app, eliminating the need for customers to be redirected to external pages. This integration reduces friction during checkout, increases conversion rates, and minimizes cart abandonment.

PayGlocal, a leading payments platform from India, has introduced its innovative product, 'Xpress PayFlow', designed to streamline card payments for merchants. This solution allows customers to enter their card details directly on the platform, eliminating the need for redirection to third-party pages.

How Payment Aggregators Work?

It is important to understand how payment aggregators work because they play a central role in streamlining the payment process, ensuring the smooth flow of transactions, and safeguarding business and customer data.

Step 1: Onboarding and Account Setup

The process begins with merchants signing up for payment aggregator services. During onboarding, merchants provide essential business information, submit identification and banking documents, and undergo a risk assessment.

They also agree to the aggregator’s terms and conditions before proceeding w.r.t transaction fees, settlement timelines, dispute resolution, and compliance with data security standards.

Step 2: Payment Integration

Once the merchant is onboarded, the payment aggregator equips them with the necessary tools to integrate payment functionality into their sales channels, such as websites and mobile apps.

This also involves APIs or plugins that ensure secure data transmission between the merchant's platform and the aggregator’s system.

Step 3: Payment Collection and Fraud Checks

When a customer purchases, the payment aggregator processes the transaction by securely capturing and encrypting the customer’s payment details.

The encrypted data is then tokenized, replacing sensitive information with a unique identifier or "token," which can be safely used for transaction processing without exposing actual card details. This method protects customer information, thus shielding it from fraud and data breaches.

Step 4: Funds Settlement

After deducting the fees, the payment aggregator holds the funds in a settlement account. Funds from multiple transactions are aggregated and transferred to the merchant’s designated bank account after a predefined settlement period, such as daily or weekly.

In International transactions, PayGlocal provides merchants with electronic Foreign Inward Remittance Certificates (eFIRCs) for cross-border transactions, aiding in compliance with regulatory requirements.

Step 5: Risk Management and Security

Payment aggregators play a critical role in managing risks by using tools to detect fraud, monitor suspicious activity, and comply with industry regulations like PCI DSS to ensure secure and reliable payment processing.

To mitigate risks, payment aggregators implement a risk management framework. This framework includes conducting thorough Know Your Customer (KYC) checks and assessing the merchant's business model, transaction volume, and industry risk profile.

Step 6: Reporting and Analytics

Payment aggregators offer merchants access to valuable reports and analytics, enabling them to track transactions, monitor sales, and gain insights into business performance.

The reporting and Advanced analytics features must also allow merchants to identify patterns in customer spending, monitor chargeback rates, and assess the effectiveness of promotional campaigns.

Additionally, these insights assist in optimizing cash flow management and improving overall business performance.

Also Read: Understanding Chargeback Fraud: Insights and Prevention Strategies

Types of Payment Aggregators

Recognizing different types of payment aggregators will help you choose the most suitable one based on your requirements.

Non-Banking Payment Aggregators

Non-banking entities approved by the Reserve Bank of India (RBI) serve as payment aggregators and intermediaries between merchants and financial institutions. These aggregators are specialists in payment processing and facilitate transactions.

Examples of prominent non-bank payment aggregators in India include PayU and Instamojo.

E-commerce Platform Payment Aggregators

Large e-commerce platforms like Amazon, Flipkart, and Snapdeal operate their own payment aggregation systems. These platforms help merchants to process payments, offering integrated solutions for businesses to accept online payments directly from customers.

Mobile Wallet Payment Aggregators

Mobile wallet providers in India, like Paytm and Google Pay, also function as payment aggregators. These platforms allow businesses to accept payments through mobile wallets, whether online or in-store, by integrating with their respective payment systems.

Cross-border Payment Aggregators (PA-CBs)

They have become pivotal in facilitating international transactions, especially for businesses engaged in global trade. These entities bridge the gap between merchants and financial institutions, ensuring seamless and secure cross-border payments. Example: Payglocal that supports international payment needs in 33+ currencies.

Also Read: Zero-Knowledge Proof: Redefining Data Privacy

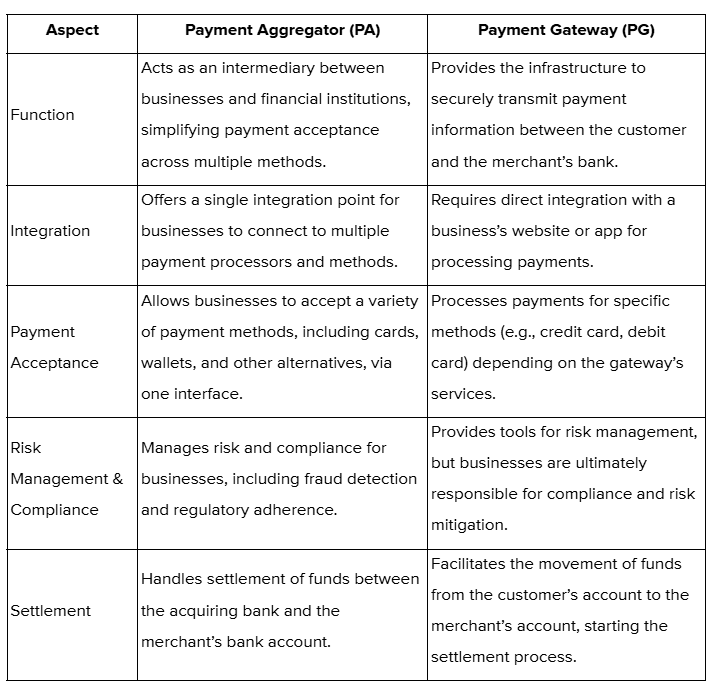

Difference Between Payment Aggregators and Payment Gateways

Both of these payment providers differ in their functionality. As a business, it’s important for you to understand these differences so that you're selecting the right solution for your payment needs.

The Indian payment aggregator landscape is constantly evolving, with new players likely to emerge in the future. Understanding the regulatory framework is crucial, as it ensures compliance.

In the News: How PayGlocal Is Bridging The Gap Between Indian Businesses And The Global Market - BW Businessworld

Why Choose Payglocal as Your Payment Aggregator?

PayGlocal is a payment aggregator that offers secure, compliant, and efficient international payment solutions for your business. With its robust infrastructure and adherence to India's stringent regulatory standards, PayGlocal simplifies cross-border payments, allowing you to accept payments in 30+ currencies.

Here are some key features that make PayGlocal the ideal choice for your payment aggregation needs:

Advanced Analytics & GCC Dashboard

You get access to a dashboard that provides real-time analytics and insights into your transactions. This tool allows you to track your sales performance, identify trends, and optimize strategies, helping you make informed business decisions.

Samruddhi X Screening

Integrated by PayGlocal, is a robust sanction screening solution that simplifies navigating the complexities of global markets. This privacy-first Zero-Knowledge Proof (ZKP) solution ensures your business remains compliant with international regulations while securing sensitive customer data.

Recurring Payments & Subscriptions

Managing recurring payments and subscriptions is made easy with PayGlocal. The platform provides tailored solutions for subscription-based businesses, allowing you to set up and manage recurring payments efficiently, ensuring smooth transactions for both you and your customers.

Alternate Payment Methods

This feature enables you to accept payments through UPI, digital wallets, and other local payment systems like Giropay for Germany, Grabpay for Singapore and more.

Conclusion

Understanding the regulatory and operational aspects of payment aggregators is crucial for businesses to navigate the complexities of digital payment systems effectively. By comprehending the legal requirements, compliance standards, and technical features, businesses can ensure seamless payment processing, reduce risks, and enhance customer satisfaction. Strategically using payment aggregators can further help in your payment processes, reduce operational costs, and allow you to focus on core business activities.

Choose PayGlocal as your trusted payment aggregator for secure, and scalable payment solutions for your business. Start optimizing your payment processes today and take your business to the next level! Get Started Now!