You just received a payment from an overseas client. Everything looks good until you notice the amount doesn't match your invoice. Or worse, your client says they paid three days ago, but you see nothing in your account.

A payment reference ID can help you solve these problems. This unique code tracks every payment you send or receive, whether through bank transfer, card payment, or UPI.

According to recent data, UPI transaction values grew from ₹21.3 lakh crore in FY2019-20 to ₹213.8 lakh crore by January 2025. With nearly ten times more digital payments flowing through the system, tracking individual transactions has become critical for businesses handling multiple payment methods and currencies.

In this guide, we break down everything you need to know about payment reference IDs, how they work, plus some effective tips to find them.

A payment reference ID is a unique alphanumeric code assigned to every financial transaction. Banks, payment gateways, and digital platforms generate this code automatically when you send or receive money.

Think of it as a tracking number for your payment. Just like you track a shipped package, you can track your money using this reference ID. The code helps banks and payment services identify your specific transaction among millions of others processed daily.

For UPI transactions in India, this code is called a UTR (Unique Transaction Reference) number and typically contains 12 digits. For international card payments, you might see it called a transaction ID or authorization code. Bank transfers use reference numbers that vary in format depending on whether you used NEFT, RTGS, or SWIFT.

The key difference between a payment reference ID and other transaction details is automation. You don't create this code yourself. The system generates it the moment your payment begins processing. This automatic generation makes it reliable for tracking and verification.

When you initiate a payment, the system creates a reference ID before any money moves. This happens in seconds, but several steps occur behind the scenes. Here's what happens during the process:

For instant payment methods like UPI, this entire process takes seconds. For bank transfers, especially international ones, the same reference ID tracks your payment across multiple days and banking systems.

Each reference ID serves the same basic purpose but follows specific formats based on the payment system. Here's how various payment reference IDs compare:

1. UPI Reference Numbers (UTR)

UPI transactions generate a 12-digit UTR number that appears instantly in your payment app. You can find this in apps like Google Pay, PhonePe, or Paytm under your transaction history. The number helps you track payments to merchants, friends, or business accounts.

For instance, if you pay a supplier via UPI and they claim non-receipt, you can share this 12-digit code. They can verify it with their bank or payment app to locate the exact transaction.

2. Bank Transfer Reference Numbers

NEFT and RTGS transfers create longer reference numbers that include the bank code, date, and transaction sequence. These numbers appear in your bank statement and transaction receipts. You need them when following up on delayed transfers or confirming payment to overseas partners who use Indian bank accounts.

3. Card Payment Transaction IDs

When you pay using international credit or debit cards, the payment gateway assigns a unique transaction ID. This appears on your confirmation page, email receipt, and card statement. Card transaction IDs become critical when dealing with failed payments, duplicate charges, or refund requests.

4. International Wire Reference Numbers

SWIFT transfers for cross-border payments generate reference numbers in MT103 format. These track your payment through multiple correspondent banks. You'll find them in your bank's remittance advice or transfer confirmation. For example, when paying international suppliers or collecting payments from foreign clients, these references help prove payment completion.

5. E-commerce Platform References

Platforms like Amazon, eBay, or export marketplaces create their own reference numbers for seller payouts. These internal references link to underlying bank transaction IDs. You need both when reconciling marketplace earnings with actual bank deposits.

Payment reference IDs solve real problems that affect your daily operations. Here's what they help you achieve:

The value multiplies when you handle dozens or hundreds of transactions monthly. Without reference IDs, you'd spend hours chasing payment confirmations and resolving disputes that could be settled in minutes.

The location of your payment reference ID depends on where and how you made the transaction. Here's where to look for different payment methods:

Tracking payments manually takes time you could spend growing your business. Each reference ID you look for, every support call you make, every reconciliation error you fix adds up to hours of administrative work.

International payments add another layer of complexity. Multiple currencies, different banking systems, varying processing times, and compliance requirements make simple payment tracking feel like complex work.

PayGlocal significantly enhances the entire payment processing and tracking approach. Here's how:

= Multi-currency accounts: Collect payments in USD, GBP, EUR, and CAD with local account details in each currency. Your clients pay locally while you track everything from one dashboard with consolidated reference IDs.

= Automatic compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) directly in your inbox after each settlement. No manual requests, no paperwork delays, just automatic compliance.

= Real-time payment tracking: Get instant notifications on your fund status at every step. From initiation to settlement, you know exactly where your money is without searching for reference numbers.

PayGlocal helps you collect payments faster, track them easier, and reconcile them accurately. You spend less time managing payment details and more time focusing on growing your business globally.

Payment reference IDs are your proof of every transaction you make or receive. They help you track payments, resolve disputes, maintain compliance, and reconcile your books with confidence.

The challenge is not having reference IDs but managing them efficiently across multiple payment methods, currencies, and banking systems. Manual tracking works until it doesn't. As your transaction volume grows, so does the time you spend chasing payment confirmations.

Modern payment solutions handle this tracking automatically. They give you consolidated views, instant notifications, and easy access to all the reference IDs you need. This matters even more for international payments, where delays, disputes, and compliance requirements are higher.

The businesses growing fastest internationally already use systems that handle their tracking. Get started with PayGlocal today and spend your time closing deals instead of chasing payment confirmations.

A payment reference ID can help you solve these problems. This unique code tracks every payment you send or receive, whether through bank transfer, card payment, or UPI.

According to recent data, UPI transaction values grew from ₹21.3 lakh crore in FY2019-20 to ₹213.8 lakh crore by January 2025. With nearly ten times more digital payments flowing through the system, tracking individual transactions has become critical for businesses handling multiple payment methods and currencies.

In this guide, we break down everything you need to know about payment reference IDs, how they work, plus some effective tips to find them.

Key Takeaways

- Unique transaction identifier: Each payment reference ID is a unique code assigned to a specific transaction, helping you track and verify payments across different systems and platforms.

- Multiple names, same purpose: Payment reference IDs are also called UTR numbers (for UPI), transaction IDs, or bank reference numbers, depending on the payment method and provider you use.

- Essential for dispute resolution: When payments fail, or amounts don't match, your payment reference ID is the first thing customer support will ask for to resolve the issue.

- Tracking keeps processes smooth: Regular tracking using reference IDs helps you reconcile payments with invoices, maintain audit trails, and catch issues before they affect your cash flow.

- Better systems reduce manual work: Modern payment platforms like PayGlocal provide automatic tracking and consolidated dashboards, reducing the time you spend hunting for reference numbers.

What is a Payment Reference ID?

A payment reference ID is a unique alphanumeric code assigned to every financial transaction. Banks, payment gateways, and digital platforms generate this code automatically when you send or receive money.

Think of it as a tracking number for your payment. Just like you track a shipped package, you can track your money using this reference ID. The code helps banks and payment services identify your specific transaction among millions of others processed daily.

For UPI transactions in India, this code is called a UTR (Unique Transaction Reference) number and typically contains 12 digits. For international card payments, you might see it called a transaction ID or authorization code. Bank transfers use reference numbers that vary in format depending on whether you used NEFT, RTGS, or SWIFT.

The key difference between a payment reference ID and other transaction details is automation. You don't create this code yourself. The system generates it the moment your payment begins processing. This automatic generation makes it reliable for tracking and verification.

How Does a Payment Reference ID Work?

When you initiate a payment, the system creates a reference ID before any money moves. This happens in seconds, but several steps occur behind the scenes. Here's what happens during the process:

- Automatic generation: The payment system assigns a unique reference ID the moment your transaction begins, before any money actually moves.

- Validation checks: The system verifies account numbers, available balance, and transaction limits while logging the reference ID for tracking.

- Multi-stage tracking: The reference ID travels with your payment through every stage, from your bank to intermediary systems to the recipient's bank.

- Duplicate prevention: Each system uses the reference ID to ensure the same transaction doesn't process twice, protecting both sender and recipient.

- Complete audit trail: Every system in the payment chain logs the reference ID, creating a permanent record you can use for tracking or disputes.

- Confirmation delivery: Once your payment completes, the reference ID appears in confirmation messages, bank statements, and transaction histories for both parties.

For instant payment methods like UPI, this entire process takes seconds. For bank transfers, especially international ones, the same reference ID tracks your payment across multiple days and banking systems.

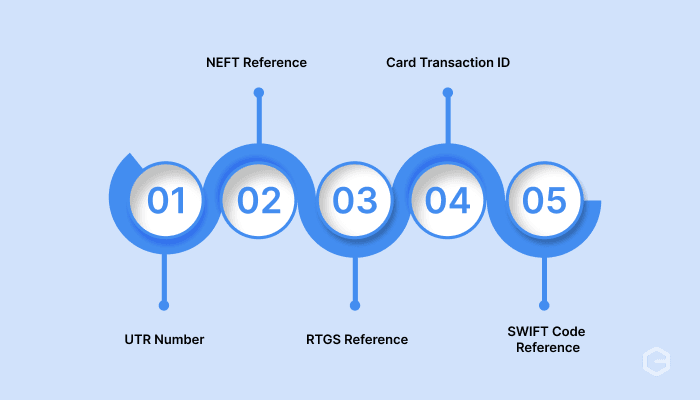

What Are the Types of Payment Reference IDs?

Each reference ID serves the same basic purpose but follows specific formats based on the payment system. Here's how various payment reference IDs compare:

1. UPI Reference Numbers (UTR)

UPI transactions generate a 12-digit UTR number that appears instantly in your payment app. You can find this in apps like Google Pay, PhonePe, or Paytm under your transaction history. The number helps you track payments to merchants, friends, or business accounts.

For instance, if you pay a supplier via UPI and they claim non-receipt, you can share this 12-digit code. They can verify it with their bank or payment app to locate the exact transaction.

2. Bank Transfer Reference Numbers

NEFT and RTGS transfers create longer reference numbers that include the bank code, date, and transaction sequence. These numbers appear in your bank statement and transaction receipts. You need them when following up on delayed transfers or confirming payment to overseas partners who use Indian bank accounts.

3. Card Payment Transaction IDs

When you pay using international credit or debit cards, the payment gateway assigns a unique transaction ID. This appears on your confirmation page, email receipt, and card statement. Card transaction IDs become critical when dealing with failed payments, duplicate charges, or refund requests.

4. International Wire Reference Numbers

SWIFT transfers for cross-border payments generate reference numbers in MT103 format. These track your payment through multiple correspondent banks. You'll find them in your bank's remittance advice or transfer confirmation. For example, when paying international suppliers or collecting payments from foreign clients, these references help prove payment completion.

5. E-commerce Platform References

Platforms like Amazon, eBay, or export marketplaces create their own reference numbers for seller payouts. These internal references link to underlying bank transaction IDs. You need both when reconciling marketplace earnings with actual bank deposits.

What Are the Benefits of Using Payment Reference IDs?

Payment reference IDs solve real problems that affect your daily operations. Here's what they help you achieve:

- Fast dispute resolution: When a client claims they paid but you received nothing, the reference ID settles the matter in minutes. You or your client can check with banks or payment providers using this code to locate the exact transaction status.

- Accurate reconciliation: Matching payments to invoices becomes simple when each transaction has a unique identifier. You can quickly verify which invoice a payment corresponds to, reducing errors in your books.

- Clear audit trails: Tax authorities and auditors need proof of all transactions. Reference IDs provide this proof. They show when money moved, how much, and through which channel. This matters especially for businesses handling multiple currencies or countries.

- Efficient customer support: When you contact your bank or payment provider about an issue, they'll ask for your reference ID first. Having it ready cuts your support time from hours to minutes.

- Fraud prevention: Reference IDs help identify duplicate transactions or unauthorized charges. If you see two charges with different reference IDs for the same amount, you know something went wrong.

- Better cash flow tracking: You can track exactly when international payments clear, how long transfers take, and where delays occur. This helps you plan your cash flow more accurately.

- Multi-currency management: When you receive payments in USD, EUR, or GBP, reference IDs help you track the original transaction amount versus what you received after conversion. This transparency prevents confusion about exchange rates or fees.

The value multiplies when you handle dozens or hundreds of transactions monthly. Without reference IDs, you'd spend hours chasing payment confirmations and resolving disputes that could be settled in minutes.

How to Find Your Payment Reference ID?

The location of your payment reference ID depends on where and how you made the transaction. Here's where to look for different payment methods:

- In your banking app: Open your transaction history and tap on the specific payment. The details screen shows your reference number, labeled as UTR, transaction ID, or reference number. For example, in most banking apps, you'll see it right below the transaction amount and recipient details.

- In confirmation messages: Check the SMS or email you received immediately after the payment. Banks and payment apps send these confirmations automatically. The reference ID usually appears in the first few lines. For instance, a typical UPI confirmation reads: "Amount transferred. UTR: 123456789012."

- On payment receipts: If you downloaded or saved a payment receipt, the reference ID appears at the top or in a dedicated reference number field. Platforms like PayPal, Stripe, or Wise clearly mark this number on downloadable receipts.

- In bank statements: Your monthly statement lists reference numbers for all transactions. Look in the rightmost columns where banks typically place transaction IDs or reference codes. This becomes your backup source when you can't find the original confirmation.

- Through customer support: If you cannot locate your reference ID anywhere, contact your bank or payment provider. Give them the transaction date, amount, and recipient details. They can retrieve the reference number from their system and share it with you.

- On payment gateway dashboards: If you accepted a payment through a gateway, log in to your merchant dashboard. Each transaction listing shows the reference ID or transaction ID that you can share with customers when needed.

- For international wire transfers, you'll find the reference in your bank's international remittance section or in the SWIFT message confirmation your bank provides.

Simplify Your International Payment Tracking with PayGlocal

Tracking payments manually takes time you could spend growing your business. Each reference ID you look for, every support call you make, every reconciliation error you fix adds up to hours of administrative work.

International payments add another layer of complexity. Multiple currencies, different banking systems, varying processing times, and compliance requirements make simple payment tracking feel like complex work.

PayGlocal significantly enhances the entire payment processing and tracking approach. Here's how:

= Multi-currency accounts: Collect payments in USD, GBP, EUR, and CAD with local account details in each currency. Your clients pay locally while you track everything from one dashboard with consolidated reference IDs.

= Automatic compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) directly in your inbox after each settlement. No manual requests, no paperwork delays, just automatic compliance.

= Real-time payment tracking: Get instant notifications on your fund status at every step. From initiation to settlement, you know exactly where your money is without searching for reference numbers.

- One platform management: View all your transactions, reference IDs, and payment statuses from a single place instead of juggling multiple banking apps and payment dashboards.

- Transparent pricing: Pay only when you transact. No setup fees, no platform charges, no hidden costs. You know exactly what you'll pay before each transaction is processed.

PayGlocal helps you collect payments faster, track them easier, and reconcile them accurately. You spend less time managing payment details and more time focusing on growing your business globally.

Final Thoughts

Payment reference IDs are your proof of every transaction you make or receive. They help you track payments, resolve disputes, maintain compliance, and reconcile your books with confidence.

The challenge is not having reference IDs but managing them efficiently across multiple payment methods, currencies, and banking systems. Manual tracking works until it doesn't. As your transaction volume grows, so does the time you spend chasing payment confirmations.

Modern payment solutions handle this tracking automatically. They give you consolidated views, instant notifications, and easy access to all the reference IDs you need. This matters even more for international payments, where delays, disputes, and compliance requirements are higher.

The businesses growing fastest internationally already use systems that handle their tracking. Get started with PayGlocal today and spend your time closing deals instead of chasing payment confirmations.