Moving money across countries is now a regular part of doing business. Whether you're receiving payments from overseas clients or paying foreign suppliers, you're dealing with remittances.

According to data reports, remittances from Indians working abroad reached $106.6 billion in FY24, rising from $101.8 billion the year before. In fact, recent data shows that India is the top receiver of remittances worldwide. But what exactly does remittance mean, and what are its different types?

In this guide, we break down the types of remittances in detail, with examples and different remittance methods to help you choose the right option for your business. You'll also see how modern payment solutions can speed up the process and make it more efficient and smooth. Let’s get into it.

A remittance is a transfer of money from one party to another, typically across borders. The term usually refers to international payments, though it can also apply to domestic transfers.

For businesses, remittances happen in two directions. You receive money from international clients (inward remittances) or send money to foreign suppliers and contractors (outward remittances). The flow depends on your business model and where your customers or vendors are located.

For instance, a software developer in Mumbai receiving payment from a US client through a freelance platform is an inward remittance. A manufacturer in Delhi paying a Chinese supplier for raw materials is an outward remittance. Both are cross-border money movements, but they serve different purposes in your business operations.

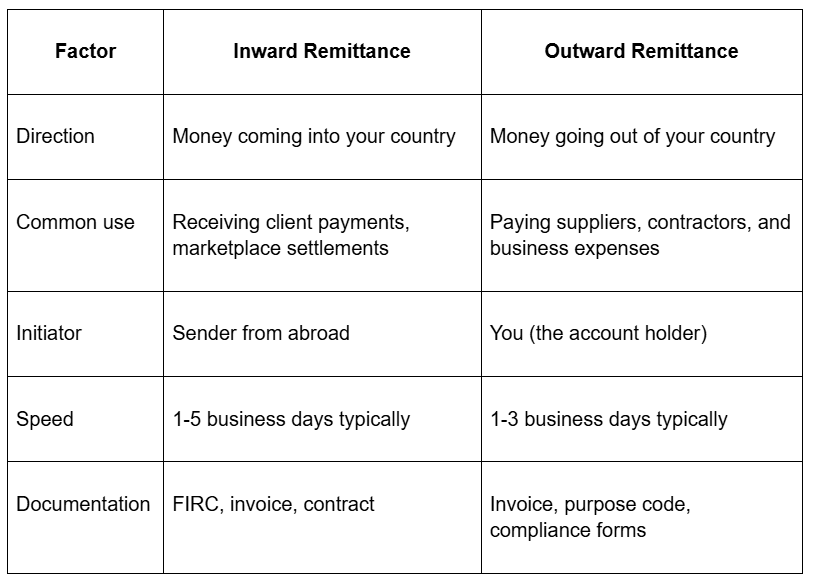

Remittances are categorized based on the direction of money flow. The two primary types are inward and outward remittances.

Here's how they compare:

Both types involve currency conversion, banking intermediaries, and compliance requirements. The method you choose affects the speed, cost, and ease of tracking.

Inward remittance means receiving money from a foreign country into your domestic account. This is how you collect payments from international clients, marketplaces, or business partners.

For example, an exporter in Bangalore receives $5,000 from a US buyer for goods sold. The money travels from the buyer's US bank account to the exporter's Indian bank account. This is an inward remittance, and the exporter receives a FIRC (Foreign Inward Remittance Certificate) as proof of the transaction for tax and compliance purposes.

Businesses that rely on inward remittances include exporters, freelancers, SaaS companies, consultants, and anyone providing services or goods to international markets. The challenge is often in the fees charged by intermediary banks and the time it takes for funds to settle.

Outward remittance is the transfer of funds from your domestic account to a foreign account. This happens when you pay overseas suppliers, contractors, or make business investments abroad.

For instance, an Indian company importing machinery from Germany sends EUR 10,000 to the supplier's German bank account. The payment leaves India and arrives in the supplier's account after currency conversion and bank processing. This is an outward remittance.

Outward remittances require additional documentation, including purpose codes and compliance forms, especially for amounts above certain thresholds. Banks scrutinize these transactions more closely for financial security.

The method you choose affects how quickly your payment arrives, how much you pay in fees, and how easy it is to track the transaction.

Each method has trade-offs between speed, cost, and convenience.

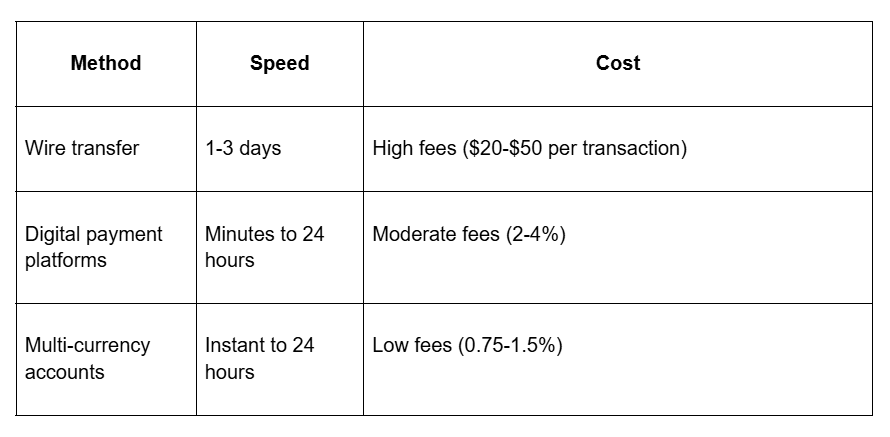

Wire transfers move money directly between banks using networks like SWIFT. They're reliable but expensive, with fees ranging from $20 to $50 per transaction, plus currency conversion markups.

Banks take 1-3 business days to process wire transfers. You need the recipient's bank details, SWIFT code, and purpose of payment. For instance, sending $10,000 via wire might cost you $40 in fees and a 2-3% currency markup, reducing the amount the beneficiary receives.

Wire transfers work well for large, one-time payments where reliability matters more than cost. However, the high fees make them impractical for frequent, smaller transactions.

Digital platforms like PayGlocal, PayPal, and Wise offer faster, more transparent remittances. They typically charge transaction fees with clear exchange rates.

These platforms connect directly to bank accounts and use technology to reduce intermediary banks, which lowers costs. For example, a freelancer receiving $1,000 through a digital platform might pay $30-$40 in fees, compared to $50-$80 through traditional banking.

The advantage is speed and transparency. You can track payments in real time, and funds often arrive within 24 hours. Many platforms also offer multi-currency wallets, letting you hold money in different currencies without immediate conversion.

Multi-currency accounts give you local bank details in multiple countries. You receive payments as if you have a local bank account in the US, UK, or Europe, without the need for intermediary banks.

For instance, a SaaS company in India can provide USD account details to US clients. The client pays as a domestic transfer in the US, and the money arrives in your multi-currency account within 1-2 days. You then convert and settle the funds in INR when you need them.

This method reduces fees significantly (typically 0.75-1.5% compared to 3-5% with traditional banks) and improves payment success rates because clients aren't making international transfers from their end.

Your choice depends on transaction frequency, amounts, speed requirements, and cost sensitivity.

If you're receiving frequent payments from international clients, multi-currency accounts offer the best balance of speed and cost. You get local bank details in major currencies, which makes it easier for clients to pay you, and you save on transaction fees.

For one-time large payments, wire transfers provide reliability despite higher costs. When paying suppliers abroad, compare digital platforms against wire transfers based on the amount and urgency.

Consider these factors:

Managing cross-border payments through traditional banks means high fees, long wait times, and complicated tracking. If you're collecting from multiple countries or paying suppliers abroad, you need a solution that makes the process simple and cost-effective.

PayGlocal helps businesses collect payments in 33+ currencies from 180+ countries with transparent pricing and instant compliance documentation.

Here's what you get:

PayGlocal reduces your transaction costs by up to compared to traditional payment methods while providing better visibility and faster settlements.

Remittances come in two main types: inward (receiving money from abroad) and outward (sending money abroad). The method you choose depends on your business needs, transaction frequency, and cost sensitivity.

Traditional wire transfers work for large one-time payments but are expensive for regular transactions. Digital platforms and multi-currency accounts offer better value, faster processing, and clearer tracking for businesses dealing with frequent cross-border payments.

Your competitors are already moving to more efficient payment systems. The right solution helps you collect payments faster, reduce costs, and maintain proper documentation.

Get started with PayGlocal today and turn international payments into a competitive advantage.

According to data reports, remittances from Indians working abroad reached $106.6 billion in FY24, rising from $101.8 billion the year before. In fact, recent data shows that India is the top receiver of remittances worldwide. But what exactly does remittance mean, and what are its different types?

In this guide, we break down the types of remittances in detail, with examples and different remittance methods to help you choose the right option for your business. You'll also see how modern payment solutions can speed up the process and make it more efficient and smooth. Let’s get into it.

Key takeaways

- Two main types exist: Remittances are classified into inward remittances (receiving money from abroad) and outward remittances (sending money abroad).

- Inward remittances power global revenue: Businesses use them to collect payments from international clients, marketplaces, and freelance platforms in multiple currencies.

- Outward remittances handle foreign expenses: These are used for paying foreign suppliers, contractors, business expenses, and international investments.

- Multiple payment methods available: Options include bank transfers, wire transfers, digital payment platforms, and multi-currency accounts, each with different speeds and costs.

- Modern solutions reduce costs significantly: PayGlocal offers multi-currency accounts that let you collect payments in USD, GBP, EUR, and CAD, with instant compliance documentation and transparent pricing.

What are remittances?

A remittance is a transfer of money from one party to another, typically across borders. The term usually refers to international payments, though it can also apply to domestic transfers.

For businesses, remittances happen in two directions. You receive money from international clients (inward remittances) or send money to foreign suppliers and contractors (outward remittances). The flow depends on your business model and where your customers or vendors are located.

For instance, a software developer in Mumbai receiving payment from a US client through a freelance platform is an inward remittance. A manufacturer in Delhi paying a Chinese supplier for raw materials is an outward remittance. Both are cross-border money movements, but they serve different purposes in your business operations.

What are the main types of remittances?

Remittances are categorized based on the direction of money flow. The two primary types are inward and outward remittances.

Here's how they compare:

Both types involve currency conversion, banking intermediaries, and compliance requirements. The method you choose affects the speed, cost, and ease of tracking.

Inward remittance

Inward remittance means receiving money from a foreign country into your domestic account. This is how you collect payments from international clients, marketplaces, or business partners.

For example, an exporter in Bangalore receives $5,000 from a US buyer for goods sold. The money travels from the buyer's US bank account to the exporter's Indian bank account. This is an inward remittance, and the exporter receives a FIRC (Foreign Inward Remittance Certificate) as proof of the transaction for tax and compliance purposes.

Businesses that rely on inward remittances include exporters, freelancers, SaaS companies, consultants, and anyone providing services or goods to international markets. The challenge is often in the fees charged by intermediary banks and the time it takes for funds to settle.

Outward remittance

Outward remittance is the transfer of funds from your domestic account to a foreign account. This happens when you pay overseas suppliers, contractors, or make business investments abroad.

For instance, an Indian company importing machinery from Germany sends EUR 10,000 to the supplier's German bank account. The payment leaves India and arrives in the supplier's account after currency conversion and bank processing. This is an outward remittance.

Outward remittances require additional documentation, including purpose codes and compliance forms, especially for amounts above certain thresholds. Banks scrutinize these transactions more closely for financial security.

What are the different methods of remittance?

The method you choose affects how quickly your payment arrives, how much you pay in fees, and how easy it is to track the transaction.

Each method has trade-offs between speed, cost, and convenience.

Wire transfers

Wire transfers move money directly between banks using networks like SWIFT. They're reliable but expensive, with fees ranging from $20 to $50 per transaction, plus currency conversion markups.

Banks take 1-3 business days to process wire transfers. You need the recipient's bank details, SWIFT code, and purpose of payment. For instance, sending $10,000 via wire might cost you $40 in fees and a 2-3% currency markup, reducing the amount the beneficiary receives.

Wire transfers work well for large, one-time payments where reliability matters more than cost. However, the high fees make them impractical for frequent, smaller transactions.

Digital payment platforms

Digital platforms like PayGlocal, PayPal, and Wise offer faster, more transparent remittances. They typically charge transaction fees with clear exchange rates.

These platforms connect directly to bank accounts and use technology to reduce intermediary banks, which lowers costs. For example, a freelancer receiving $1,000 through a digital platform might pay $30-$40 in fees, compared to $50-$80 through traditional banking.

The advantage is speed and transparency. You can track payments in real time, and funds often arrive within 24 hours. Many platforms also offer multi-currency wallets, letting you hold money in different currencies without immediate conversion.

Multi-currency accounts

Multi-currency accounts give you local bank details in multiple countries. You receive payments as if you have a local bank account in the US, UK, or Europe, without the need for intermediary banks.

For instance, a SaaS company in India can provide USD account details to US clients. The client pays as a domestic transfer in the US, and the money arrives in your multi-currency account within 1-2 days. You then convert and settle the funds in INR when you need them.

This method reduces fees significantly (typically 0.75-1.5% compared to 3-5% with traditional banks) and improves payment success rates because clients aren't making international transfers from their end.

How to choose the right remittance method for your business?

Your choice depends on transaction frequency, amounts, speed requirements, and cost sensitivity.

If you're receiving frequent payments from international clients, multi-currency accounts offer the best balance of speed and cost. You get local bank details in major currencies, which makes it easier for clients to pay you, and you save on transaction fees.

For one-time large payments, wire transfers provide reliability despite higher costs. When paying suppliers abroad, compare digital platforms against wire transfers based on the amount and urgency.

Consider these factors:

- Transaction frequency: High-frequency payments benefit from lower per-transaction costs of digital platforms or multi-currency accounts.

- Payment amounts: Large amounts justify wire transfer fees; smaller amounts need cost-effective solutions.

- Speed requirements: Emergency payments need same-day or next-day options; regular payments can use slower, cheaper methods.

- Client preferences: Make it easy for clients to pay you by offering their preferred local payment methods.

- Compliance needs: Ensure your method provides proper documentation, like FIRC for tax purposes.

- Currency exposure: If you deal in multiple currencies, holding funds in a multi-currency account lets you time conversions better.

Get paid globally in 33+ currencies with PayGlocal

Managing cross-border payments through traditional banks means high fees, long wait times, and complicated tracking. If you're collecting from multiple countries or paying suppliers abroad, you need a solution that makes the process simple and cost-effective.

PayGlocal helps businesses collect payments in 33+ currencies from 180+ countries with transparent pricing and instant compliance documentation.

Here's what you get:

- Multi-currency accounts: Get local accounts in USD, GBP, EUR, and CAD to receive payments as domestic transfers, reducing costs and improving success rates.

- Global payment methods: Accept 40+ local payment methods, including cards, wallets, and bank transfers, that your international clients prefer.

- Instant compliance: Receive FIRC automatically in your inbox after settlement, with no manual paperwork or follow-up needed.

- Complete tracking: Monitor every payment with transparent dashboards and instant notifications on fund status throughout the transfer process.

- Zero fixed costs: Pay only when you do the transaction, with no setup fees, platform fees, or documentation charges.

PayGlocal reduces your transaction costs by up to compared to traditional payment methods while providing better visibility and faster settlements.

Final thoughts

Remittances come in two main types: inward (receiving money from abroad) and outward (sending money abroad). The method you choose depends on your business needs, transaction frequency, and cost sensitivity.

Traditional wire transfers work for large one-time payments but are expensive for regular transactions. Digital platforms and multi-currency accounts offer better value, faster processing, and clearer tracking for businesses dealing with frequent cross-border payments.

Your competitors are already moving to more efficient payment systems. The right solution helps you collect payments faster, reduce costs, and maintain proper documentation.

Get started with PayGlocal today and turn international payments into a competitive advantage.