You're about to make a payment, but you suddenly hit a transaction limit. The payment fails. You're not sure if it's your bank, the app, or UPI itself. Sounds familiar?

According to recent data, over 18 billion payment transactions happen through UPI every month. In fact, around 85% of all digital payments in the country are UPI-based. With this level of usage, transaction limits are essential to ensure proper security.

In this guide, we cover everything you need to know about UPI transaction limits, including daily caps, per-transaction limits, and special category rules, along with effective tips for managing high-value payments. So, let’s get into it.

The UPI transaction limit is the maximum amount you can send or receive through Unified Payments Interface (UPI) in a single transaction or within a specific timeframe, like 24 hours.

The National Payments Corporation of India (NPCI) sets the base limits for all UPI transactions across India.

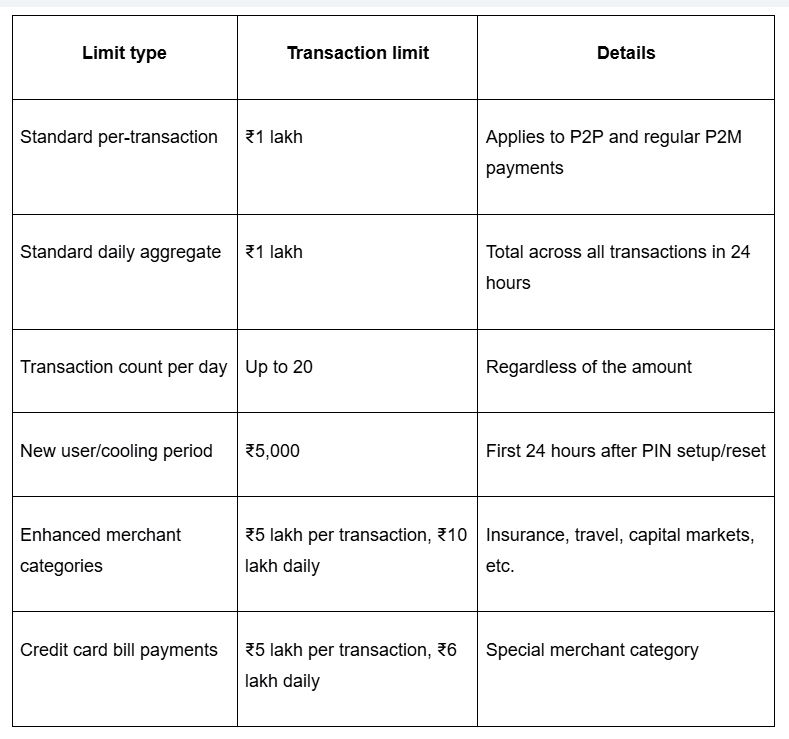

For most users, the standard cap is ₹1 lakh per transaction and ₹1 lakh per day for person-to-person (P2P) and regular person-to-merchant (P2M) payments. This means you can send up to ₹1 lakh in a single payment, and your total UPI spending in any 24-hour period cannot exceed ₹1 lakh.

However, these limits aren't universal. Individual banks and payment apps can set stricter caps based on their risk assessment. For example, some banks limit new users to ₹25,000 or ₹50,000 per day.

Also, NPCI recently introduced enhanced limits for specific verified merchant categories, allowing transactions up to ₹5 lakh with daily caps reaching ₹10 lakh.

For instance, if you're paying an insurance premium through a verified merchant account, you can now pay up to ₹5 lakh in one go instead of splitting it into multiple transactions.

Here’s a quick breakdown of UPI limits across different scenarios.

Tip: Your actual limits may be lower depending on your bank's risk policy. Check your banking app or contact customer service for your specific caps.

Starting September 15, 2025, NPCI increased transaction limits for specific high-value merchant categories.

These enhanced limits apply only to verified merchant accounts under approved categories. The per-transaction limit for these categories increased to ₹5 lakh, and the daily cumulative limit reached ₹10 lakh.

Here are the categories that qualify for higher limits:

For example, if you're booking a family vacation package worth ₹4.5 lakh through a verified travel merchant, you can now pay the full amount in one UPI transaction instead of splitting it into five separate ₹90,000 payments.

Note: These higher limits only work when the merchant is properly categorized and verified by their payment service provider. Regular person-to-person transfers still follow the standard ₹1 lakh limit.

Each bank has its own risk management policy. Some banks set conservative limits to ensure better security, especially for customers with shorter banking histories. Others align closely with NPCI's maximum allowable limits.

Here’s what varies across banks:

For instance, State Bank of India (SBI) generally allows the full ₹1 lakh per transaction and per day for established customers, while some smaller cooperative banks restrict transactions to ₹25,000 per day.

You can usually check your UPI limit within your banking app under UPI settings or by contacting your bank's customer service.

Here’s how to work within UPI limits without disrupting your payments.

For businesses collecting payments from customers, especially international clients, traditional payment systems can create bottlenecks. You'll need a payment solution that handles higher volumes and supports multiple currencies for global customers.

If you export goods or services, accept payments from international customers, or process high-volume transactions, you need a payment solution built for scale. That’s where PayGlocal comes in, helping businesses collect global payments easily.

Here’s how PayGlocal can support you:

Whether you're a freelancer invoicing US clients, an exporter shipping to Europe, or a SaaS company serving global customers, PayGlocal gives you the payment infrastructure to scale without limits. Your customers get a seamless payment experience, and you get faster settlements in your preferred currency.

UPI transaction limits serve an important purpose in preventing fraud and managing risk. For standard transactions, the ₹1 lakh daily cap works for most personal needs. The enhanced limits for specific merchant categories, now up to ₹10 lakh daily, address the need for higher-value digital payments in insurance, travel, and investments.

But if you're building a business globally, you need payment acceptance that scales across countries, handles multiple currencies, and removes daily transaction barriers.

Ready to accept payments from anywhere in a fast and secure way? Get started with PayGlocal today and give your business the payment infrastructure it needs to grow globally.

According to recent data, over 18 billion payment transactions happen through UPI every month. In fact, around 85% of all digital payments in the country are UPI-based. With this level of usage, transaction limits are essential to ensure proper security.

In this guide, we cover everything you need to know about UPI transaction limits, including daily caps, per-transaction limits, and special category rules, along with effective tips for managing high-value payments. So, let’s get into it.

Key takeaways

- Standard UPI limit: ₹1 lakh per transaction and ₹1 lakh per day for person-to-person and regular person-to-merchant payments.

- Enhanced merchant limits: Up to ₹5 lakh per transaction and ₹10 lakh per day for verified merchants in categories like insurance, capital markets, travel, and government payments (effective September 15, 2025).

- Bank-specific variations: Individual banks can set lower limits than NPCI's maximum cap based on their risk policies.

- New user restrictions: First-time UPI users or those who reset their PIN may face lower limits (around ₹5,000) during a cooling period for security verification.

- Accepting global payments: For businesses accepting international payments or needing higher transaction volumes, PayGlocal offers multi-currency accounts with transparent pricing.

What is the UPI transaction limit?

The UPI transaction limit is the maximum amount you can send or receive through Unified Payments Interface (UPI) in a single transaction or within a specific timeframe, like 24 hours.

The National Payments Corporation of India (NPCI) sets the base limits for all UPI transactions across India.

For most users, the standard cap is ₹1 lakh per transaction and ₹1 lakh per day for person-to-person (P2P) and regular person-to-merchant (P2M) payments. This means you can send up to ₹1 lakh in a single payment, and your total UPI spending in any 24-hour period cannot exceed ₹1 lakh.

However, these limits aren't universal. Individual banks and payment apps can set stricter caps based on their risk assessment. For example, some banks limit new users to ₹25,000 or ₹50,000 per day.

Also, NPCI recently introduced enhanced limits for specific verified merchant categories, allowing transactions up to ₹5 lakh with daily caps reaching ₹10 lakh.

For instance, if you're paying an insurance premium through a verified merchant account, you can now pay up to ₹5 lakh in one go instead of splitting it into multiple transactions.

Here’s a quick breakdown of UPI limits across different scenarios.

Tip: Your actual limits may be lower depending on your bank's risk policy. Check your banking app or contact customer service for your specific caps.

What are the enhanced UPI limits for special merchant categories?

Starting September 15, 2025, NPCI increased transaction limits for specific high-value merchant categories.

These enhanced limits apply only to verified merchant accounts under approved categories. The per-transaction limit for these categories increased to ₹5 lakh, and the daily cumulative limit reached ₹10 lakh.

Here are the categories that qualify for higher limits:

- Capital markets and investments: Payments to brokerages, mutual fund purchases, IPO applications, and deposits can now go up to ₹5 lakh per transaction with a daily cap of ₹10 lakh.

- Insurance premiums: Both life and general insurance premium payments to verified insurers qualify for the enhanced limits.

- Government e-Marketplace (GeM): Payments for government procurement, tax payments, and earnest money deposits fall under this category.

- Travel bookings: Flight tickets, hotel reservations, and travel packages through verified travel merchants can accept up to ₹5 lakh per transaction.

- Credit card bill payments: This category has a slightly different structure with a per-transaction limit of ₹5 lakh but a daily cap of ₹6 lakh instead of ₹10 lakh.

- Loan EMIs and collections: Payments to financial institutions for loan repayments and EMI collections qualify for the ₹10 lakh daily limit.

- Educational institutions and hospitals: Verified educational and healthcare providers can accept payments up to ₹5 lakh per transaction.

For example, if you're booking a family vacation package worth ₹4.5 lakh through a verified travel merchant, you can now pay the full amount in one UPI transaction instead of splitting it into five separate ₹90,000 payments.

Note: These higher limits only work when the merchant is properly categorized and verified by their payment service provider. Regular person-to-person transfers still follow the standard ₹1 lakh limit.

How do bank-specific UPI limits vary?

Each bank has its own risk management policy. Some banks set conservative limits to ensure better security, especially for customers with shorter banking histories. Others align closely with NPCI's maximum allowable limits.

Here’s what varies across banks:

- Per-transaction caps: While NPCI allows ₹1 lakh, some banks might restrict this to ₹25,000 or ₹50,000 per transaction.

- Daily limits: Even if NPCI permits ₹1 lakh daily, your bank might cap your daily UPI spending at ₹40,000 or ₹60,000.

- Transaction count: The 20-transaction daily limit is common, but some banks may allow fewer transactions per day.

- New customer restrictions: Banks often impose stricter limits on newly opened accounts or recently activated UPI services.

For instance, State Bank of India (SBI) generally allows the full ₹1 lakh per transaction and per day for established customers, while some smaller cooperative banks restrict transactions to ₹25,000 per day.

You can usually check your UPI limit within your banking app under UPI settings or by contacting your bank's customer service.

What are the tips for managing UPI transaction limits?

Here’s how to work within UPI limits without disrupting your payments.

- Plan high-value payments in advance: If you know you need to make a large payment, check your limits beforehand. Split payments across multiple days if needed, or use the enhanced merchant category limits where applicable.

- Use the right payment method for the right purpose: For personal transfers under ₹1 lakh, UPI works perfectly. For business payments, insurance, or investments over ₹1 lakh, ensure the merchant is verified under special categories to access higher limits.

- Keep track of your daily spending: UPI limits reset every 24 hours from your first transaction of the day, not at midnight. Monitor your daily aggregate to avoid failed transactions.

- Verify merchant category codes: Before making high-value payments, confirm with the merchant that they're registered under the appropriate category to accept enhanced limit payments.

- Maintain multiple payment options: Don't rely solely on UPI for all payments. Have alternative methods like NEFT, RTGS, or international payment accounts ready for transactions that exceed UPI limits.

- Monitor your transaction count: Even if you haven't reached the ₹1 lakh cap, remember the 20-transaction daily limit. Consolidate smaller payments when possible.

For businesses collecting payments from customers, especially international clients, traditional payment systems can create bottlenecks. You'll need a payment solution that handles higher volumes and supports multiple currencies for global customers.

Accept international payments easily and scale your business

If you export goods or services, accept payments from international customers, or process high-volume transactions, you need a payment solution built for scale. That’s where PayGlocal comes in, helping businesses collect global payments easily.

Here’s how PayGlocal can support you:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries. No need to worry about daily transaction caps or splitting large payments.

- Local accounts in major currencies: Get local bank accounts in USD, GBP, EUR, and CAD. Your international clients pay you locally, making transactions faster and more familiar for them.

- Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) directly in your inbox after settlement. Stay compliant without manual paperwork.

- Complete payment tracking: Monitor every payment with real-time notifications and transparent dashboards. Know exactly where your funds are at every step.

- Pay only when you transact: No setup fees, no platform fees, no monthly charges. You only pay when you receive payments, with transparent pricing and no hidden costs.

Whether you're a freelancer invoicing US clients, an exporter shipping to Europe, or a SaaS company serving global customers, PayGlocal gives you the payment infrastructure to scale without limits. Your customers get a seamless payment experience, and you get faster settlements in your preferred currency.

Final thoughts

UPI transaction limits serve an important purpose in preventing fraud and managing risk. For standard transactions, the ₹1 lakh daily cap works for most personal needs. The enhanced limits for specific merchant categories, now up to ₹10 lakh daily, address the need for higher-value digital payments in insurance, travel, and investments.

But if you're building a business globally, you need payment acceptance that scales across countries, handles multiple currencies, and removes daily transaction barriers.

Ready to accept payments from anywhere in a fast and secure way? Get started with PayGlocal today and give your business the payment infrastructure it needs to grow globally.