You send an invoice to an international client and wonder when you'll actually see the money. Will it take days or weeks? How much will fees affect your profit margins? Payment networks determine all of this, and choosing the right one can make the difference between quick, affordable payments and costly delays.

According to studies, around 49% of all global real-time payments occur in India. With the rise of international payments, it’s more important than ever to select the right payment network that can handle multiple currencies, deliver high success rates, and track payments clearly.

In this guide, we cover everything about payment networks. Find out what they are, how they work, and which features can improve your payment processes.

A payment network connects financial institutions, merchants, and customers to handle electronic transactions. These networks make sure funds move safely from your customer's account to your business account through approved channels.

For example, when someone uses a Visa card at your store, the Visa network processes the transaction by talking to their bank and your bank. The network makes sure the customer has enough money and approves the payment.

Payment networks follow a well-structured process to ensure secure money transfers between parties. Multiple participants work together to complete each transaction. Here's how the process works:

1. Transaction starts: Your customer begins a payment using their card, digital wallet, or bank transfer. Your system captures the payment details and sends them to your payment processor.

2. Authorization request: The payment processor sends transaction details to the right payment network. The network routes this information to the customer's bank for checking.

3. Verification and approval: The customer's bank checks their account balance, credit limit, and risk indicators. If everything looks good, the bank sends an approval code back through the network.

4. Transaction completes: You receive the approval and complete the sale. Your customer gets confirmation, and you can fulfill the order or provide the service.

5. Settlement happens: Later, usually within 1-3 business days, the actual money transfer occurs. The customer's bank sends money through the network to your bank, which puts it in your account.

6. Final record keeping: Everyone gets transaction records for accounting and compliance. This includes detailed reports showing fees, exchange rates, and settlement amounts.

Different payment networks serve various transaction needs and customer preferences. Each type offers specific advantages for different situations.

Let's look at each network type and how they serve different business needs.

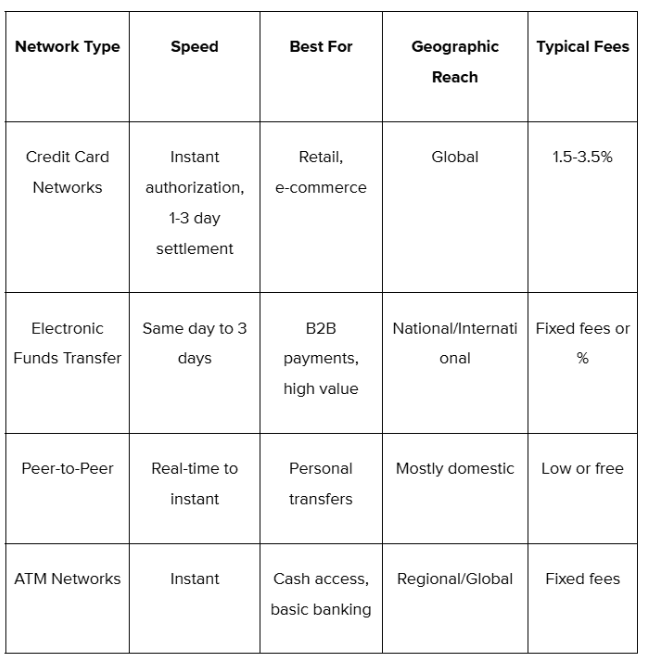

Credit card networks like Visa, Mastercard, American Express, and Discover enable card transactions worldwide. These networks set standards for card creation, transaction processing, and security rules.

Visa and Mastercard work as open networks, partnering with thousands of banks to issue cards and process payments. American Express operates as a closed-loop system, handling both card issuance and network processing.

These networks offer several important capabilities:

For instance, when you use a Visa card from HDFC Bank, Visa handles the network processing while HDFC manages your account relationship.

EFT (Electronic Funds Transfer) networks handle direct bank-to-bank transfers without cards. This includes systems like NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), ACH (Automated Clearing House), and international SWIFT (Society for Worldwide Interbank Financial Telecommunication) networks.

These networks work well for business payments and high-value transactions. They offer lower fees for large amounts but may take longer to process than card payments.

Different EFT systems serve specific purposes:

For example, when an exporter receives payment from an international client, SWIFT networks coordinate the cross-border transfer between correspondent banks.

P2P networks enable direct transfers between individuals using simple identifiers like phone numbers or email addresses. UPI in India, Venmo in the US, and similar systems let users send money instantly.

These networks focus on user experience and convenience over business features. They typically offer lower fees but may have transaction limits.

P2P networks provide several user-friendly features:

ATM (Automated Teller Machine) networks connect cash machines to banks and card networks, enabling customers to access their accounts worldwide. Major ATM networks include Plus, Cirrus, and regional networks like Mastercard ATM Network and Visa Plus.

ATM networks provide important banking services beyond cash withdrawal, including balance inquiries, fund transfers, and bill payments. These networks offer various banking services:

These networks charge interchange fees for cross-bank transactions but provide crucial access to banking services, especially in areas with limited branch presence.

Payment networks provide important advantages that enable modern business and financial transactions.

Despite their advantages, payment networks deal with several operational and strategic challenges.

How to choose the right payment network?

Selecting the right payment network depends on your business model, customer base, and growth goals.

Check security and compliance features: Verify that networks meet industry standards like PCI DSS (Payment Card Industry Data Security Standard) and support required compliance documentation for your business type.

Payment networks are evolving rapidly to meet changing consumer expectations and technological advances. The industry is moving toward faster, more secure, and user-friendly payment experiences:

Traditional payment networks often create complexity for businesses operating across borders. Multiple currencies, varying compliance requirements, and inconsistent success rates can slow growth and increase operational work.

PayGlocal makes international payments easy to manage, fast, and efficient by providing a single platform that handles global payment network complexity. Here are some of the PayGlocal can help you:

Real-time tracking and notifications: Monitor payment status at every stage with detailed reporting and automated updates for complete transaction visibility.

Whether you're a freelancer receiving payments from global clients or an enterprise managing complex international transactions, PayGlocal provides the network connectivity and compliance support needed for smooth operations.

Payment networks enable digital transactions by connecting financial institutions, merchants, and customers across the globe. The right payment network choice depends on your specific business needs, customer base, and expansion plans. Modern businesses require networks that offer global reach, strong security, transparent pricing, and complete reporting capabilities.

While traditional networks serve most businesses well, companies scaling globally need solutions that handle international payment complexity seamlessly. PayGlocal provides the infrastructure, compliance support, and transparent pricing that growing businesses need to succeed globally.

Ready to simplify your international payment processes and start collecting payments from customers worldwide? Get started with PayGlocal today.

According to studies, around 49% of all global real-time payments occur in India. With the rise of international payments, it’s more important than ever to select the right payment network that can handle multiple currencies, deliver high success rates, and track payments clearly.

In this guide, we cover everything about payment networks. Find out what they are, how they work, and which features can improve your payment processes.

Key takeaways:

- Payment networks: They connect banks, merchants, and customers so electronic money transfers work securely across different financial institutions.

- Different network types: There are various payment networks, each serving different needs, like credit card networks (Visa, Mastercard), peer-to-peer systems, and international transfer networks.

- Modern networks: They provide better security and speed through real-time processing, risk detection, and encrypted data transmission.

- PayGlocal offers complete payment network access: With PayGlocal, you get multi-currency support, global payment methods, and instant compliance documentation for international businesses.

What is a payment network?

A payment network connects financial institutions, merchants, and customers to handle electronic transactions. These networks make sure funds move safely from your customer's account to your business account through approved channels.

For example, when someone uses a Visa card at your store, the Visa network processes the transaction by talking to their bank and your bank. The network makes sure the customer has enough money and approves the payment.

How does a payment network work?

Payment networks follow a well-structured process to ensure secure money transfers between parties. Multiple participants work together to complete each transaction. Here's how the process works:

1. Transaction starts: Your customer begins a payment using their card, digital wallet, or bank transfer. Your system captures the payment details and sends them to your payment processor.

2. Authorization request: The payment processor sends transaction details to the right payment network. The network routes this information to the customer's bank for checking.

3. Verification and approval: The customer's bank checks their account balance, credit limit, and risk indicators. If everything looks good, the bank sends an approval code back through the network.

4. Transaction completes: You receive the approval and complete the sale. Your customer gets confirmation, and you can fulfill the order or provide the service.

5. Settlement happens: Later, usually within 1-3 business days, the actual money transfer occurs. The customer's bank sends money through the network to your bank, which puts it in your account.

6. Final record keeping: Everyone gets transaction records for accounting and compliance. This includes detailed reports showing fees, exchange rates, and settlement amounts.

What are the types of payment networks?

Different payment networks serve various transaction needs and customer preferences. Each type offers specific advantages for different situations.

Let's look at each network type and how they serve different business needs.

1. Credit card networks

Credit card networks like Visa, Mastercard, American Express, and Discover enable card transactions worldwide. These networks set standards for card creation, transaction processing, and security rules.

Visa and Mastercard work as open networks, partnering with thousands of banks to issue cards and process payments. American Express operates as a closed-loop system, handling both card issuance and network processing.

These networks offer several important capabilities:

- Global acceptance: Cards work at millions of merchants worldwide for maximum customer convenience.

- Dispute resolution: Built-in processes help resolve payment conflicts between customers and merchants.

- Security features: Advanced protection like tokenization keeps card data safe during transactions.

- Contactless payments: Support for tap-to-pay and mobile wallet payments for faster checkout.

- Reward programs: Customer benefits and loyalty features that encourage repeat usage.

For instance, when you use a Visa card from HDFC Bank, Visa handles the network processing while HDFC manages your account relationship.

2. Electronic funds transfer networks

EFT (Electronic Funds Transfer) networks handle direct bank-to-bank transfers without cards. This includes systems like NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), ACH (Automated Clearing House), and international SWIFT (Society for Worldwide Interbank Financial Telecommunication) networks.

These networks work well for business payments and high-value transactions. They offer lower fees for large amounts but may take longer to process than card payments.

Different EFT systems serve specific purposes:

- ACH transfers: Handle domestic bulk payments like payroll and recurring bills with low cost.

- Wire transfers: Process urgent, high-value transactions with same-day delivery for important payments.

- SWIFT transfers: Connect banks globally for international business payments and trade finance.

- NEFT/RTGS systems: Provide domestic transfer options in India with different speed and value limits.

- SEPA (Single Euro Payments Area): Make euro transactions simple across 36 European countries with standard processing.

For example, when an exporter receives payment from an international client, SWIFT networks coordinate the cross-border transfer between correspondent banks.

Peer-to-peer payment networks

P2P networks enable direct transfers between individuals using simple identifiers like phone numbers or email addresses. UPI in India, Venmo in the US, and similar systems let users send money instantly.

These networks focus on user experience and convenience over business features. They typically offer lower fees but may have transaction limits.

P2P networks provide several user-friendly features:

- Simple setup: Easy registration process with basic personal information and bank account linking.

- Real-time transfers: Instant or near-instant money movement between users for immediate access.

- Low fees: Most basic transfers cost nothing or charge minimal fees for standard transactions.

- Social integration: Features like payment notes and contact sharing make transactions more personal.

- Mobile design: Apps built specifically for smartphones with intuitive interfaces and quick access.

4. ATM networks

ATM (Automated Teller Machine) networks connect cash machines to banks and card networks, enabling customers to access their accounts worldwide. Major ATM networks include Plus, Cirrus, and regional networks like Mastercard ATM Network and Visa Plus.

ATM networks provide important banking services beyond cash withdrawal, including balance inquiries, fund transfers, and bill payments. These networks offer various banking services:

- Cash transactions: Withdrawal and deposit capabilities for immediate access to physical money.

- Account information: Balance inquiries and transaction history to check account status.

- Fund transfers: Inter-bank transfers between accounts for money management needs.

- Bill payments: Utility and service payments directly from ATM for convenient access.

- Account updates: Mini statements and recent transaction details for record keeping.

These networks charge interchange fees for cross-bank transactions but provide crucial access to banking services, especially in areas with limited branch presence.

What are the benefits of payment networks?

Payment networks provide important advantages that enable modern business and financial transactions.

- Global reach: Networks connect you with customers worldwide, letting your business accept payments from any country. This global connectivity is essential for e-commerce and international trade.

- Better security: Modern networks use multiple security layers including encryption, tokenization, and risk detection algorithms. These systems monitor transactions in real-time and block suspicious activities.

- Speed and efficiency: Electronic networks process transactions in seconds rather than days. Real-time payment systems can complete transfers instantly, improving cash flow for your business.

- Cost effectiveness: While networks charge processing fees, they cut many costs related to cash handling, check processing, and manual record keeping. The automation reduces operational work significantly.

- Standardization: Networks establish common rules that let different banks and financial institutions work together easily. This standardization enables global business without complex individual agreements.

- Complete reporting: Networks provide detailed transaction data that helps you track sales, spot trends, and manage finances more effectively.

What challenges do payment networks face?

Despite their advantages, payment networks deal with several operational and strategic challenges.

- Security threats and risk management: Payment networks face constant security issues from unauthorized access attempts. Networks must invest heavily in security infrastructure and regularly update protection methods.

- Regulatory compliance: Different countries impose varying rules on payment processing. Networks operating globally must navigate complex compliance requirements across multiple locations.

- Transaction fees and cost pressure: Merchants often view processing fees as a significant expense. Networks face pressure to reduce costs while maintaining service quality and security standards.

- Technology infrastructure maintenance: Payment networks require substantial ongoing investment in technology upgrades, server capacity, and network reliability to handle growing transaction volumes.

- Competition from new technologies: New fintech solutions and digital payment methods challenge traditional payment network models.

How to choose the right payment network?

Selecting the right payment network depends on your business model, customer base, and growth goals.

- Check your customer demographics: Identify where your customers live and their preferred payment methods. For example, if you serve European customers, make sure your network supports SEPA transfers and popular European digital wallets.

- Look at transaction volumes and values: High-volume businesses need networks with strong processing capacity and volume discounts. High-value transactions require networks with solid risk prevention and compliance features.

- Consider geographic coverage: International businesses need networks that operate in their target markets with local capabilities. Domestic-only networks won't support global expansion plans.

- Compare fee structures: Look at processing fees, setup costs, monthly charges, and currency conversion rates. Check beyond the basic rates to evaluate the total cost.

- Review integration requirements: Make sure the network offers APIs, plugins, or integration tools that work with your existing systems. Complex integrations can delay launch times and increase development costs.

Check security and compliance features: Verify that networks meet industry standards like PCI DSS (Payment Card Industry Data Security Standard) and support required compliance documentation for your business type.

What is the future of payment networks?

Payment networks are evolving rapidly to meet changing consumer expectations and technological advances. The industry is moving toward faster, more secure, and user-friendly payment experiences:

- Real-time payments: More networks are offering instant settlement capabilities, reducing the traditional 1-3 day wait times for fund availability.

- Embedded finance: Payment capabilities are being built directly into software platforms, letting businesses offer financial services without separate banking relationships.

- Open banking integration: APIs (Application Programming Interfaces) allow third-party services to connect directly with bank accounts, creating new payment possibilities.

- Biometric authentication: Fingerprint, facial recognition, and voice authentication are replacing traditional passwords and PINs for more secure access.

- Central Bank Digital Currencies: Governments are exploring digital versions of national currencies that could reshape how payment networks operate.

- Enhanced data analytics: Networks are using artificial intelligence to provide better risk assessment, personalized experiences, and business insights.

Get paid globally and scale your business with PayGlocal

Traditional payment networks often create complexity for businesses operating across borders. Multiple currencies, varying compliance requirements, and inconsistent success rates can slow growth and increase operational work.

PayGlocal makes international payments easy to manage, fast, and efficient by providing a single platform that handles global payment network complexity. Here are some of the PayGlocal can help you:

- Multi-currency account support: Accept payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD for reduced processing costs.

- Complete payment method coverage: Support 40+ global payment methods, including cards, digital wallets, and regional payment systems, through unified integration.

- Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) and other regulatory documents automatically upon settlement, cutting out manual paperwork and delays.

- Zero setup costs: Pay only for successful transactions with no setup fees, monthly charges, or hidden costs, making budget planning straightforward.

Real-time tracking and notifications: Monitor payment status at every stage with detailed reporting and automated updates for complete transaction visibility.

Whether you're a freelancer receiving payments from global clients or an enterprise managing complex international transactions, PayGlocal provides the network connectivity and compliance support needed for smooth operations.

Final thoughts

Payment networks enable digital transactions by connecting financial institutions, merchants, and customers across the globe. The right payment network choice depends on your specific business needs, customer base, and expansion plans. Modern businesses require networks that offer global reach, strong security, transparent pricing, and complete reporting capabilities.

While traditional networks serve most businesses well, companies scaling globally need solutions that handle international payment complexity seamlessly. PayGlocal provides the infrastructure, compliance support, and transparent pricing that growing businesses need to succeed globally.

Ready to simplify your international payment processes and start collecting payments from customers worldwide? Get started with PayGlocal today.