Electronic and digital payments have been rapidly growing in India. In fact, nearly 40% of all payments in India happen digitally.

Electronic Fund Transfer (EFT) has become the foundation of modern business payments, enabling everything from salary deposits to international transactions.

Whether you're a freelancer collecting payments from global clients or a business managing supplier payments, knowing about EFT is essential to ensure smooth transactions.

In this guide, we break down everything you need to know about EFT, including how it works and why it matters for your business. Let’s get started!

Electronic Fund Transfer (EFT) refers to the digital movement of money from one bank account to another using electronic systems instead of paper checks or cash. EFT includes various payment methods, including direct deposits, wire transfers, ACH transfers, debit card transactions, and online banking transfers.

The key feature of EFT is that it processes payments electronically through secure networks, removing the need for physical paperwork.

For example, when your employer deposits your salary directly into your bank account, that's an EFT. Similarly, when you pay a supplier through online banking or when customers pay through your website using their debit cards, these are all forms of electronic fund transfers.

EFT systems connect banks and financial institutions through networks like ACH (Automated Clearing House) in the US or SWIFT for international transfers, enabling secure and efficient money movement across the globe.

EFT systems operate through secure networks that connect banks, payment processors, and other financial institutions. The electronic fund transfer process follows these key steps:

For example, when a freelancer receives payment from an international client, the client's bank initiates the transfer, routing it through SWIFT networks to correspondent banks, which then deliver funds to the freelancer's local account. The entire process creates digital records at each step, ensuring transparency and compliance.

Different EFT types help businesses choose the right payment method for specific needs. Each type serves different purposes and operates with varying speeds, costs, and security levels.

Here's a comparison of the main EFT types:

Each EFT type offers distinct advantages depending on your business requirements and customer preferences.

ACH (Automated Clearing House) transfers process payments in batches through a network that handles millions of transactions daily. These transfers work well for recurring payments like subscriptions, employee salaries, or vendor payments. For instance, when you set up automatic bill payments for utilities, the system uses ACH to debit your account monthly. ACH transfers typically take 1-3 business days but cost significantly less than wire transfers.

Wire transfers provide fast, secure money movement for high-value transactions. Banks process these transfers individually rather than in batches, enabling same-day or next-day completion. For example, businesses often use wire transfers for large supplier payments or international transactions where speed matters more than cost. However, wire transfer fees can range from $15-50 per transaction.

Debit card transactions let customers pay directly from their bank accounts at point-of-sale terminals or online. These payments process instantly, providing immediate confirmation to both businesses and customers. For instance, when customers use debit cards on e-commerce sites, the payment typically completes within seconds, improving the shopping experience.

Online banking platforms enable direct account-to-account transfers through web or mobile interfaces. Businesses can send payments to vendors or receive payments from customers without visiting bank branches. For example, many freelancers receive project payments through online bank transfers, which offer convenience and digital payment tracking.

ATM networks facilitate cash withdrawals, deposits, and account inquiries through electronic systems. While primarily for cash access, ATMs also enable account transfers and bill payments. For instance, business owners can deposit checks or transfer funds between accounts using ATM networks, extending banking hours beyond traditional branch operations.

Direct deposit systems automatically transfer funds into designated accounts on scheduled dates. Employers commonly use direct deposits for payroll, while government agencies use them for benefits distribution. For example, businesses save time and costs by avoiding paper checks through direct deposit systems, while employees enjoy faster access to their earnings.

EFT offers significant advantages over traditional payment methods, making it essential for modern business operations. These benefits impact both operational efficiency and financial management.

Many people use EFT and ACH interchangeably, but knowing their relationship helps businesses choose appropriate payment methods. EFT serves as the broader category, while ACH represents one specific type of electronic fund transfer.

EFT includes all electronic money transfers, including wire transfers, debit card payments, online banking transfers, and ACH transactions. For example, when you transfer money through your banking app, use a debit card, or receive a wire transfer, these are all EFT transactions using different networks and processing methods.

ACH transfers represent a subset of EFT that specifically uses the Automated Clearing House network to process payments in batches. For instance, direct deposit payroll, automatic bill payments, and business-to-business transfers often use ACH networks because they prioritize cost efficiency over speed.

The choice between different EFT methods depends on your business needs. ACH works well for routine, recurring payments where lower costs matter more than immediate processing.

EFT methods like wire transfers suit urgent, high-value transactions despite higher fees. Debit card payments serve customer-facing transactions requiring instant confirmation.

Traditional EFT methods work well for domestic transactions, but international businesses face challenges with currency conversions, compliance requirements, and complex routing processes. Managing multiple banking relationships and handling different regulatory frameworks can slow down global growth.

PayGlocal simplifies international electronic fund transfers by providing a complete payment platform designed for businesses collecting from global markets. Whether you're a freelancer invoicing clients worldwide or an exporter managing supplier payments, PayGlocal handles the complexity while you focus on growth.

* Global payment methods: Accept payments through local methods your customers prefer, from credit cards to regional payment systems, increasing conversion rates and customer satisfaction.

* Instant compliance documentation: Receive FIRC and other compliance documents automatically after settlements, removing paperwork delays and ensuring regulatory compliance.

* Real-time payment tracking: Monitor every transaction from initiation to settlement with transparent dashboards and automated notifications at each step.

* Zero fixed costs: Pay only for successful transactions with transparent pricing and no hidden fees, setup costs, or monthly charges.

* One platform management: Handle all payment types, currencies, and compliance requirements through a single dashboard instead of managing multiple banking relationships.

PayGlocal's electronic fund transfer capabilities combine the reliability of traditional banking with the flexibility modern international businesses need.

Electronic Fund Transfer has changed how businesses handle payments, offering speed, security, and cost advantages over traditional paper-based methods. From ACH transfers for routine payments to wire transfers for urgent transactions, EFT provides flexible options for different business needs.

Knowing EFT types and benefits helps businesses choose appropriate payment methods for their specific requirements. However, companies operating internationally need solutions like PayGlocal that go beyond basic EFT capabilities to handle multiple currencies, global compliance, and diverse payment preferences.

Ready to upgrade your payment capabilities beyond basic EFT? Get started with PayGlocal today and collect payments efficiently from anywhere in the world.

Electronic Fund Transfer (EFT) has become the foundation of modern business payments, enabling everything from salary deposits to international transactions.

Whether you're a freelancer collecting payments from global clients or a business managing supplier payments, knowing about EFT is essential to ensure smooth transactions.

In this guide, we break down everything you need to know about EFT, including how it works and why it matters for your business. Let’s get started!

Key Takeaways:

- EFT definition: Electronic Fund Transfer moves money digitally between accounts without paper checks or cash, covering everything from direct deposits to wire transfers.

- Multiple EFT types: Includes ACH transfers, wire transfers, ATM transactions, debit card payments, and online transfers, each serving different business needs.

- Cost and speed advantages: EFT transactions typically cost less and process faster than traditional payment methods, improving business cash flow.

- Global payment solution: PayGlocal offers comprehensive EFT capabilities with multi-currency accounts, 40+ payment methods, and instant compliance documentation.

What is EFT?

Electronic Fund Transfer (EFT) refers to the digital movement of money from one bank account to another using electronic systems instead of paper checks or cash. EFT includes various payment methods, including direct deposits, wire transfers, ACH transfers, debit card transactions, and online banking transfers.

The key feature of EFT is that it processes payments electronically through secure networks, removing the need for physical paperwork.

For example, when your employer deposits your salary directly into your bank account, that's an EFT. Similarly, when you pay a supplier through online banking or when customers pay through your website using their debit cards, these are all forms of electronic fund transfers.

EFT systems connect banks and financial institutions through networks like ACH (Automated Clearing House) in the US or SWIFT for international transfers, enabling secure and efficient money movement across the globe.

How do electronic fund transfers work?

EFT systems operate through secure networks that connect banks, payment processors, and other financial institutions. The electronic fund transfer process follows these key steps:

- Payment initiation: The sender authorizes a payment through various channels like online banking, mobile apps, or payment terminals. The system captures transaction details, including sender account, recipient account, amount, and payment purpose.

- Authentication and verification: The originating bank verifies account ownership, available funds, and transaction legitimacy. Security systems check for fraud indicators and ensure the payment meets regulatory requirements.

- Network routing: The payment routes through appropriate networks based on transaction type. ACH payments go through clearing houses, wire transfers use SWIFT or Fedwire networks, while card payments route through card network systems.

- Processing and clearing: The receiving bank processes the incoming payment, validates the recipient account, and prepares for fund settlement. Both banks update their internal records and prepare settlement instructions.

- Settlement and confirmation: Networks facilitate the actual money movement between financial institutions. Both sender and recipient receive confirmation notifications, and account balances update to reflect the completed transaction.

For example, when a freelancer receives payment from an international client, the client's bank initiates the transfer, routing it through SWIFT networks to correspondent banks, which then deliver funds to the freelancer's local account. The entire process creates digital records at each step, ensuring transparency and compliance.

What are the types of electronic funds transfer?

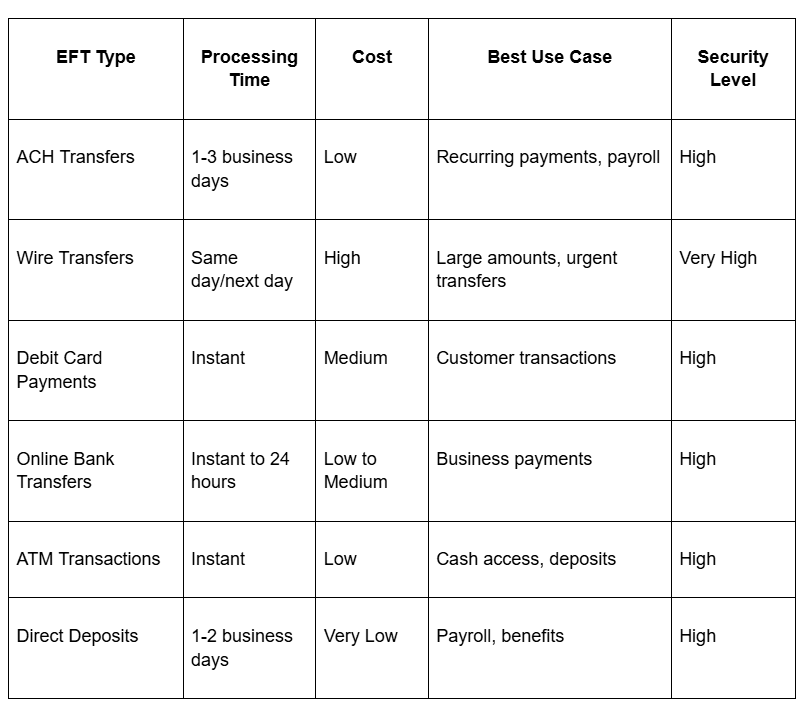

Different EFT types help businesses choose the right payment method for specific needs. Each type serves different purposes and operates with varying speeds, costs, and security levels.

Here's a comparison of the main EFT types:

Each EFT type offers distinct advantages depending on your business requirements and customer preferences.

ACH transfers

ACH (Automated Clearing House) transfers process payments in batches through a network that handles millions of transactions daily. These transfers work well for recurring payments like subscriptions, employee salaries, or vendor payments. For instance, when you set up automatic bill payments for utilities, the system uses ACH to debit your account monthly. ACH transfers typically take 1-3 business days but cost significantly less than wire transfers.

Wire transfers

Wire transfers provide fast, secure money movement for high-value transactions. Banks process these transfers individually rather than in batches, enabling same-day or next-day completion. For example, businesses often use wire transfers for large supplier payments or international transactions where speed matters more than cost. However, wire transfer fees can range from $15-50 per transaction.

Debit card payments

Debit card transactions let customers pay directly from their bank accounts at point-of-sale terminals or online. These payments process instantly, providing immediate confirmation to both businesses and customers. For instance, when customers use debit cards on e-commerce sites, the payment typically completes within seconds, improving the shopping experience.

Online bank transfers

Online banking platforms enable direct account-to-account transfers through web or mobile interfaces. Businesses can send payments to vendors or receive payments from customers without visiting bank branches. For example, many freelancers receive project payments through online bank transfers, which offer convenience and digital payment tracking.

ATM transactions

ATM networks facilitate cash withdrawals, deposits, and account inquiries through electronic systems. While primarily for cash access, ATMs also enable account transfers and bill payments. For instance, business owners can deposit checks or transfer funds between accounts using ATM networks, extending banking hours beyond traditional branch operations.

Direct deposits

Direct deposit systems automatically transfer funds into designated accounts on scheduled dates. Employers commonly use direct deposits for payroll, while government agencies use them for benefits distribution. For example, businesses save time and costs by avoiding paper checks through direct deposit systems, while employees enjoy faster access to their earnings.

What are the benefits of electronic fund transfer?

EFT offers significant advantages over traditional payment methods, making it essential for modern business operations. These benefits impact both operational efficiency and financial management.

- Faster processing times: EFT transactions complete within minutes to days, compared to weeks for paper checks. Businesses receive payments faster, improving cash flow and reducing collection cycles.

- Lower transaction costs: Electronic transfers typically cost $0.50-3.00 per transaction, while paper check processing can cost $5-15 per transaction, including printing, mailing, and handling expenses.

- Enhanced security features: EFT systems use encryption, authentication protocols, and fraud monitoring to protect transactions. Digital payments create detailed audit trails, making them more secure than cash or check payments.

- 24/7 availability: Electronic payment systems operate continuously, allowing businesses to process transactions outside traditional banking hours. Customers can make payments anytime, improving satisfaction and reducing payment delays.

- Reduced administrative work: EFT removes manual check processing, deposit trips, and paper record keeping. Businesses save staff time on payment handling and reconciliation tasks.

- Better cash flow management: Real-time payment processing and automated notifications help businesses track incoming and outgoing funds more effectively, enabling better financial planning.

- Global reach capabilities: EFT systems connect to international networks, enabling cross-border payments without complex correspondent banking relationships.

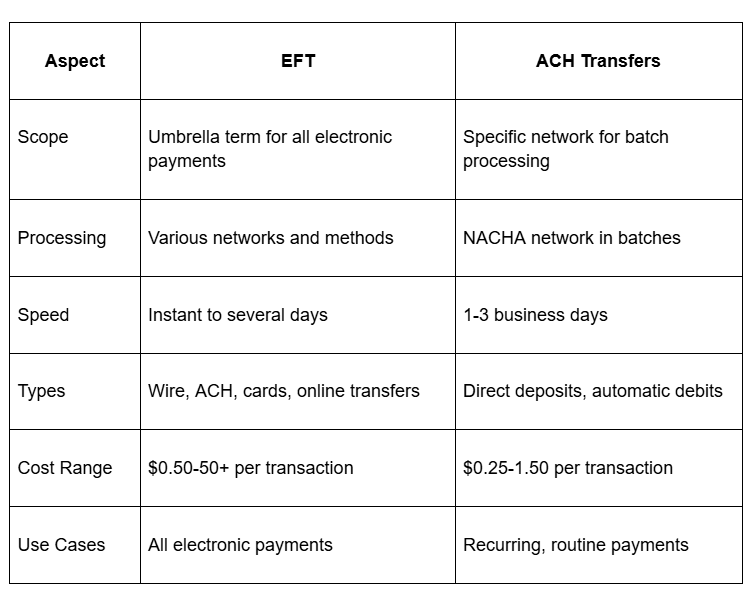

What is the difference between EFT and ACH transfers?

Many people use EFT and ACH interchangeably, but knowing their relationship helps businesses choose appropriate payment methods. EFT serves as the broader category, while ACH represents one specific type of electronic fund transfer.

EFT includes all electronic money transfers, including wire transfers, debit card payments, online banking transfers, and ACH transactions. For example, when you transfer money through your banking app, use a debit card, or receive a wire transfer, these are all EFT transactions using different networks and processing methods.

ACH transfers represent a subset of EFT that specifically uses the Automated Clearing House network to process payments in batches. For instance, direct deposit payroll, automatic bill payments, and business-to-business transfers often use ACH networks because they prioritize cost efficiency over speed.

The choice between different EFT methods depends on your business needs. ACH works well for routine, recurring payments where lower costs matter more than immediate processing.

EFT methods like wire transfers suit urgent, high-value transactions despite higher fees. Debit card payments serve customer-facing transactions requiring instant confirmation.

Collect global payments faster and smarter with PayGlocal

Traditional EFT methods work well for domestic transactions, but international businesses face challenges with currency conversions, compliance requirements, and complex routing processes. Managing multiple banking relationships and handling different regulatory frameworks can slow down global growth.

PayGlocal simplifies international electronic fund transfers by providing a complete payment platform designed for businesses collecting from global markets. Whether you're a freelancer invoicing clients worldwide or an exporter managing supplier payments, PayGlocal handles the complexity while you focus on growth.

* Global payment methods: Accept payments through local methods your customers prefer, from credit cards to regional payment systems, increasing conversion rates and customer satisfaction.

* Instant compliance documentation: Receive FIRC and other compliance documents automatically after settlements, removing paperwork delays and ensuring regulatory compliance.

* Real-time payment tracking: Monitor every transaction from initiation to settlement with transparent dashboards and automated notifications at each step.

* Zero fixed costs: Pay only for successful transactions with transparent pricing and no hidden fees, setup costs, or monthly charges.

* One platform management: Handle all payment types, currencies, and compliance requirements through a single dashboard instead of managing multiple banking relationships.

PayGlocal's electronic fund transfer capabilities combine the reliability of traditional banking with the flexibility modern international businesses need.

Final thoughts

Electronic Fund Transfer has changed how businesses handle payments, offering speed, security, and cost advantages over traditional paper-based methods. From ACH transfers for routine payments to wire transfers for urgent transactions, EFT provides flexible options for different business needs.

Knowing EFT types and benefits helps businesses choose appropriate payment methods for their specific requirements. However, companies operating internationally need solutions like PayGlocal that go beyond basic EFT capabilities to handle multiple currencies, global compliance, and diverse payment preferences.

Ready to upgrade your payment capabilities beyond basic EFT? Get started with PayGlocal today and collect payments efficiently from anywhere in the world.