Digital payments are growing rapidly in India for business transactions. According to recent data, UPI transaction values grew from ₹21.3 lakh crore in 2019-20 to ₹213.8 lakh crore by January 2025, with businesses receiving ₹59.3 lakh crore through merchant payments.

The merchant payment system allows modern businesses to collect money from customers through various electronic methods. From credit card transactions to digital wallets, these payment systems make it possible for customers to pay you quickly and securely, no matter where they are in the world.

In this guide, we cover everything you need to know about merchant payments, from basic definitions to choosing the right payment solution for your business needs.

A merchant payment is any transaction where a customer pays your business for goods or services using electronic payment methods. Instead of handling cash, you can accept payments through credit cards, debit cards, digital wallets, bank transfers, and other electronic channels.

For instance, when a customer buys from your online store and pays with their credit card, that's a merchant payment. Your business receives the payment through your payment processing system, which handles the transaction securely and transfers the money to your business account.

Merchant payments work through a network of financial institutions, payment processors, and technology systems that verify, authorize, and settle transactions. This process typically takes seconds for your customer but involves multiple steps behind the scenes to ensure the payment is legitimate and the funds are available.

A merchant payment gateway is the technology that connects your business to the payment processing network. Its role is to securely transmit payment information between your customer, their bank, and your business account.

When a customer enters their payment details on your website or at your checkout, the payment gateway encrypts this information and sends it through the proper channels for authorization. The gateway then receives the approval or decline response and communicates this back to you and your customer instantly.

Popular payment gateways in India include PayGlocal for global businesses, Razorpay for complete digital payment solutions, and Paytm for digital wallet integration.

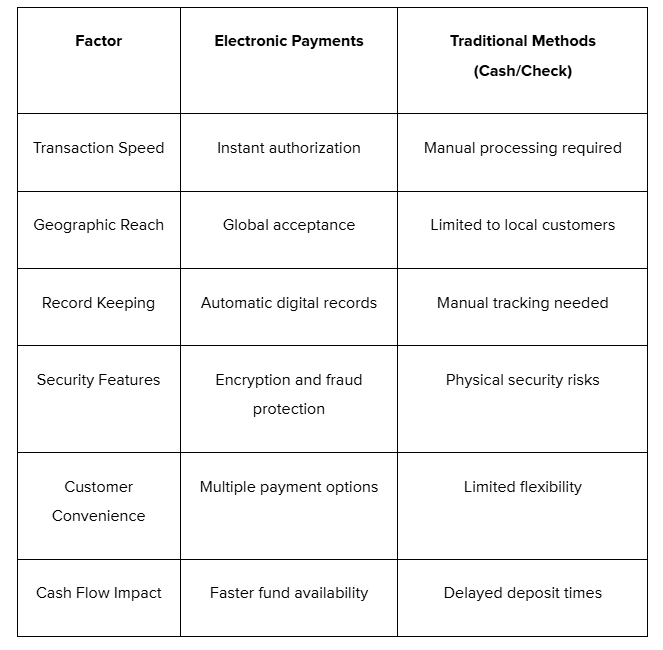

Modern customers expect convenient payment options, and businesses that can't accept electronic payments risk losing sales. Cash-only businesses limit their customer base and miss opportunities for growth, especially in today's digital economy.

Here’s why businesses need electronic merchant payments as compared to traditional payment methods:

Electronic merchant payment systems provide several advantages for business operations. Some of their top benefits include:

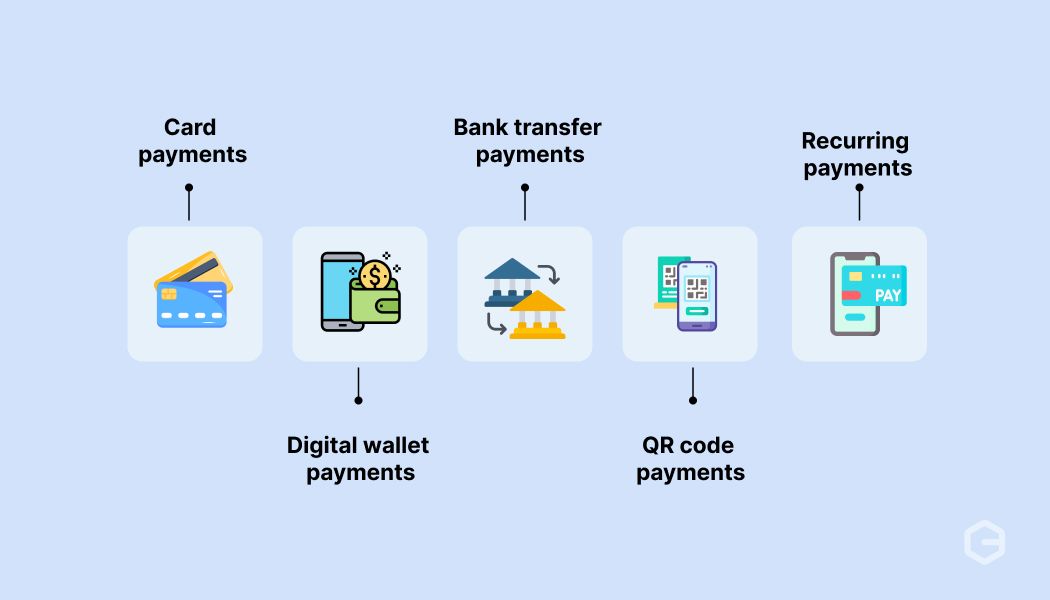

Merchant payments come in several forms, each designed for specific business needs and customer preferences. Here’s how the common types compare:

Let’s take a detailed look at each of these merchant payment types:

Credit and debit card payments remain the most popular merchant payment method globally. Your customers enter their card details, and the payment processor verifies the information with the card issuer before approving the transaction.

For example, when a customer buys a product from your online store using their Visa card, the payment gateway encrypts their card information, sends it to Visa for authorization, and returns an approval or decline decision within seconds.

Digital wallets like Apple Pay, Google Pay, and PayPal store customer payment information securely, allowing for quick checkout experiences. Your customers can pay with a simple tap or click without entering their card details each time.

These payment methods work particularly well for mobile commerce, where typing card information on a phone can be difficult. Digital wallets also add an extra security layer since the actual card numbers aren't shared with your business.

Direct bank transfers allow customers to pay directly from their bank accounts to your business account through methods like NEFT, RTGS, or net banking. This method works well for large purchases or B2B transactions where customers prefer not to use credit cards.

For instance, if you're a consultant working with international clients, you might receive payment via wire transfer or domestically through net banking for project-based work or consulting services that involve significant amounts.

QR code payments allow customers to scan a code with their mobile device and complete transactions instantly through UPI or digital wallet apps. This payment method has become extremely popular in India and other markets where mobile-first payment adoption is high.

For example, if you run a retail store, you can display a QR code at checkout that customers scan with their UPI apps like Google Pay, PhonePe, or Paytm to pay directly from their bank accounts. This method works particularly well for small businesses since it requires minimal setup and no expensive hardware.

Subscription businesses rely on recurring payment systems to automatically charge customers on a regular schedule. This payment type works well for software subscriptions, membership services, and other ongoing business models.

The system stores customer payment information securely and processes charges according to the agreed schedule, reducing manual work for both you and your customers.

Merchant payment processing involves several parties working together to move money from your customer's account to your business account safely and efficiently.

The process typically follows these steps:

1. Authorization: When a customer submits payment information, the payment gateway encrypts the data and sends it to the payment processor, which forwards it to the customer's bank or card issuer for approval.

2. Authentication: The customer's bank verifies that the account has sufficient funds and that the payment information is correct, then sends an approval or decline response back through the network.

3. Capture: For approved transactions, the payment processor captures the authorized amount and initiates the transfer process.

4. Settlement: The funds move from the customer's account through the payment network to your merchant account, typically within 1-3 business days.

5. Reconciliation: Your payment system updates transaction records and provides reporting so you can track payments and manage your finances.

This entire process happens automatically and usually completes within seconds for the customer, though the actual money transfer takes longer to finalize.

Merchant payment services are the complete range of solutions and support that payment companies provide to help businesses accept and manage customer payments. These services go beyond just processing transactions to include the tools and features you need to run your payment operations effectively.

Most merchant payment service providers offer these essential components:

Point-of-sale systems: Hardware and software solutions for accepting in-person payments at retail locations or events.

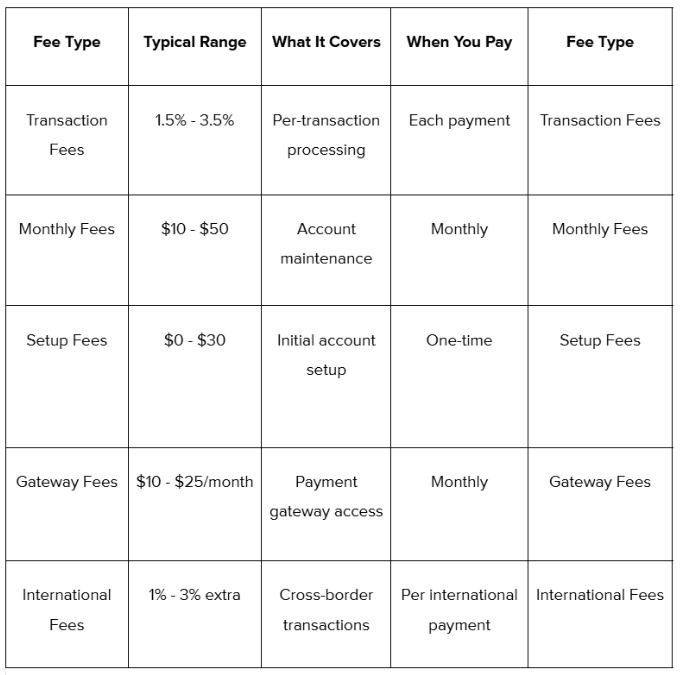

Merchant payment costs vary significantly based on your business type, transaction volume, and the payment methods you accept. Most providers use a combination of percentage-based fees and fixed charges that can add up quickly if you don't choose carefully.

Here's what typical merchant payment pricing looks like across different fee structures:

Refunds are an important part of merchant payment operations that allow you to return money to customers when needed. Whether it's for product returns, service cancellations, or resolving customer complaints, having a smooth refund process helps maintain customer satisfaction and trust.

A refund happens when you voluntarily return money to a customer through your payment system. This process reverses the original transaction and sends the funds back to the customer's original payment method, whether that was a credit card, digital wallet, or bank account.

Here's how the refund process typically works:

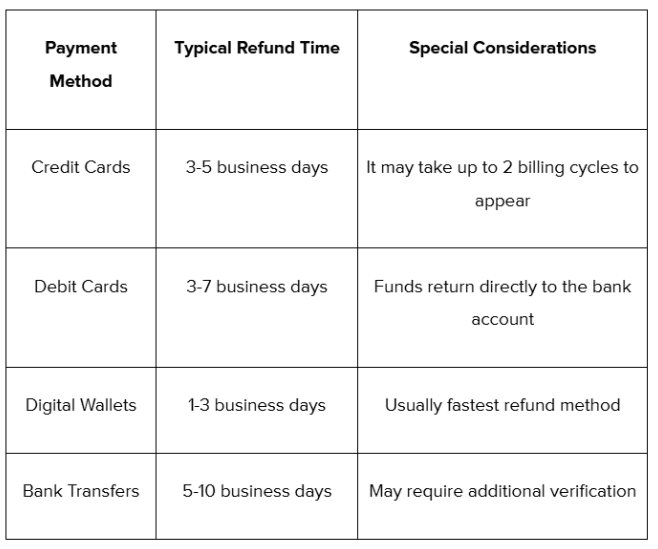

Different payment methods have varying refund timelines and considerations:

Choosing the right merchant payment solution affects your customer experience, operational efficiency, and bottom line. Here are key factors to consider when evaluating options:

Managing payments across borders often means dealing with multiple currencies, complex compliance requirements, and inconsistent success rates. Traditional payment systems can create friction for international customers and delay your cash flow when you need it most.

PayGlocal simplifies global payment acceptance by providing a complete solution designed for businesses that serve customers worldwide. Whether you're a freelancer working with international clients or an e-commerce business expanding globally, PayGlocal handles the complexity so you can focus on growing your business.

Here's how PayGlocal improves your payment experience:

Multi-currency accounts: Accept payments locally in USD, GBP, EUR, and CAD, making it easier for international customers to pay you while you maintain local banking relationships.

Global payment method coverage: Support 40+ payment methods, including cards, digital wallets, and local payment options that customers prefer in different regions.

Dynamic checkout: Provide customers with payment options tailored to their location and preferences, improving conversion rates and reducing cart abandonment.

Automated compliance documentation: Receive FIRC documents instantly upon settlement, eliminating paperwork delays and ensuring you stay compliant with regulations.

Real-time payment tracking: Monitor every transaction from initiation to settlement with detailed dashboards and automatic notifications.

PayGlocal handles the complexity of global payments while providing you all the tools and features you need to manage your international payments effectively.

Merchant payments form the foundation of modern business transactions, enabling companies to serve customers globally while maintaining efficient operations. From simple card payments to complex multi-currency processing, the right payment solution can make the difference between a sale and a lost opportunity.

Success in today's market requires payment systems that work seamlessly across borders, currencies, and customer preferences. PayGlocal provides all the tools and support you need to accept payments globally while settling locally.

Ready to improve your payment experience and reach customers worldwide? Get started with PayGlocal today.

The merchant payment system allows modern businesses to collect money from customers through various electronic methods. From credit card transactions to digital wallets, these payment systems make it possible for customers to pay you quickly and securely, no matter where they are in the world.

In this guide, we cover everything you need to know about merchant payments, from basic definitions to choosing the right payment solution for your business needs.

Key Takeaways:

- Electronic payment acceptance: Merchant payments enable businesses to accept payments from customers using credit cards, debit cards, and digital payment methods.

- Connected processing systems: Payment gateways and merchant accounts work together to process transactions securely between customers and businesses.

- Multiple transaction types: Different payment types exist, including retail payments, e-commerce payments, and recurring billing options for various business models.

- Complete payment solutions: PayGlocal offers complete merchant payment solutions with multi-currency accounts, global payment methods, and seamless international transaction processing.

What is a merchant payment?

A merchant payment is any transaction where a customer pays your business for goods or services using electronic payment methods. Instead of handling cash, you can accept payments through credit cards, debit cards, digital wallets, bank transfers, and other electronic channels.

For instance, when a customer buys from your online store and pays with their credit card, that's a merchant payment. Your business receives the payment through your payment processing system, which handles the transaction securely and transfers the money to your business account.

Merchant payments work through a network of financial institutions, payment processors, and technology systems that verify, authorize, and settle transactions. This process typically takes seconds for your customer but involves multiple steps behind the scenes to ensure the payment is legitimate and the funds are available.

What is a merchant payment gateway?

A merchant payment gateway is the technology that connects your business to the payment processing network. Its role is to securely transmit payment information between your customer, their bank, and your business account.

When a customer enters their payment details on your website or at your checkout, the payment gateway encrypts this information and sends it through the proper channels for authorization. The gateway then receives the approval or decline response and communicates this back to you and your customer instantly.

Popular payment gateways in India include PayGlocal for global businesses, Razorpay for complete digital payment solutions, and Paytm for digital wallet integration.

Why do businesses need merchant payment systems?

Modern customers expect convenient payment options, and businesses that can't accept electronic payments risk losing sales. Cash-only businesses limit their customer base and miss opportunities for growth, especially in today's digital economy.

Here’s why businesses need electronic merchant payments as compared to traditional payment methods:

Electronic merchant payment systems provide several advantages for business operations. Some of their top benefits include:

- Customer convenience: Customers can pay using their preferred method, whether that's a credit card, digital wallet, or bank transfer.

- Faster transactions: Electronic payments process instantly, speeding up checkout and improving customer experience.

- Global reach: Accept payments from customers anywhere in the world, not just those who have local currency or can visit your physical location.

- Better cash flow: Receive payments faster than waiting for checks to clear or handling cash deposits.

- Reduced fraud risk: Electronic payments include security features and fraud detection that protect both you and your customers.

- Automatic record keeping: Digital transactions create automatic records for accounting and tax purposes.

What are the different types of merchant payments?

Merchant payments come in several forms, each designed for specific business needs and customer preferences. Here’s how the common types compare:

Let’s take a detailed look at each of these merchant payment types:

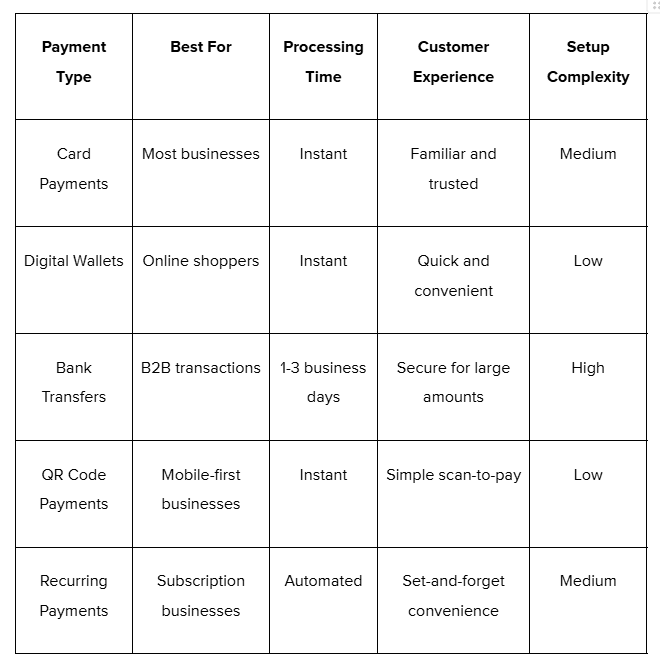

1. Card payments

Credit and debit card payments remain the most popular merchant payment method globally. Your customers enter their card details, and the payment processor verifies the information with the card issuer before approving the transaction.

For example, when a customer buys a product from your online store using their Visa card, the payment gateway encrypts their card information, sends it to Visa for authorization, and returns an approval or decline decision within seconds.

2. Digital wallet payments

Digital wallets like Apple Pay, Google Pay, and PayPal store customer payment information securely, allowing for quick checkout experiences. Your customers can pay with a simple tap or click without entering their card details each time.

These payment methods work particularly well for mobile commerce, where typing card information on a phone can be difficult. Digital wallets also add an extra security layer since the actual card numbers aren't shared with your business.

3. Bank transfer payments

Direct bank transfers allow customers to pay directly from their bank accounts to your business account through methods like NEFT, RTGS, or net banking. This method works well for large purchases or B2B transactions where customers prefer not to use credit cards.

For instance, if you're a consultant working with international clients, you might receive payment via wire transfer or domestically through net banking for project-based work or consulting services that involve significant amounts.

4. QR code payments

QR code payments allow customers to scan a code with their mobile device and complete transactions instantly through UPI or digital wallet apps. This payment method has become extremely popular in India and other markets where mobile-first payment adoption is high.

For example, if you run a retail store, you can display a QR code at checkout that customers scan with their UPI apps like Google Pay, PhonePe, or Paytm to pay directly from their bank accounts. This method works particularly well for small businesses since it requires minimal setup and no expensive hardware.

5. Recurring payments

Subscription businesses rely on recurring payment systems to automatically charge customers on a regular schedule. This payment type works well for software subscriptions, membership services, and other ongoing business models.

The system stores customer payment information securely and processes charges according to the agreed schedule, reducing manual work for both you and your customers.

How does merchant payment processing work?

Merchant payment processing involves several parties working together to move money from your customer's account to your business account safely and efficiently.

The process typically follows these steps:

1. Authorization: When a customer submits payment information, the payment gateway encrypts the data and sends it to the payment processor, which forwards it to the customer's bank or card issuer for approval.

2. Authentication: The customer's bank verifies that the account has sufficient funds and that the payment information is correct, then sends an approval or decline response back through the network.

3. Capture: For approved transactions, the payment processor captures the authorized amount and initiates the transfer process.

4. Settlement: The funds move from the customer's account through the payment network to your merchant account, typically within 1-3 business days.

5. Reconciliation: Your payment system updates transaction records and provides reporting so you can track payments and manage your finances.

This entire process happens automatically and usually completes within seconds for the customer, though the actual money transfer takes longer to finalize.

What are merchant payment services?

Merchant payment services are the complete range of solutions and support that payment companies provide to help businesses accept and manage customer payments. These services go beyond just processing transactions to include the tools and features you need to run your payment operations effectively.

Most merchant payment service providers offer these essential components:

- Payment processing: The basic service of handling credit card, debit card, and alternative payment transactions from authorization to settlement.

- Merchant accounts:** Specialized business bank accounts designed to hold funds from customer payments before transferring them to your main business account.

- Payment gateways: The technology that securely transmits payment data between your business, customers, and financial institutions.

Point-of-sale systems: Hardware and software solutions for accepting in-person payments at retail locations or events.

- Online payment tools: Integration options for websites, mobile apps, and e-commerce platforms to accept digital payments.

- Reporting and analytics: Dashboard tools that help you track sales, identify trends, and manage your payment data.

- Payment protection: Security measures and monitoring systems that detect and prevent suspicious payment activity.

- Customer support: Technical assistance and account management to help resolve payment issues and optimize your setup.

How much do merchant payment services cost?

Merchant payment costs vary significantly based on your business type, transaction volume, and the payment methods you accept. Most providers use a combination of percentage-based fees and fixed charges that can add up quickly if you don't choose carefully.

Here's what typical merchant payment pricing looks like across different fee structures:

How do merchant payment refunds work?

Refunds are an important part of merchant payment operations that allow you to return money to customers when needed. Whether it's for product returns, service cancellations, or resolving customer complaints, having a smooth refund process helps maintain customer satisfaction and trust.

A refund happens when you voluntarily return money to a customer through your payment system. This process reverses the original transaction and sends the funds back to the customer's original payment method, whether that was a credit card, digital wallet, or bank account.

Here's how the refund process typically works:

- Customer request: A customer contacts you requesting a refund for their purchase, either through your website, email, or customer service channels.

- Review and approval: You evaluate the request based on your return policy, the reason for the refund, and any relevant circumstances before deciding whether to approve it.

- Processing initiation: Once approved, you initiate the refund through your payment gateway or merchant dashboard, which creates a reverse transaction for the original payment.

- Fund transfer: The payment processor deducts the refund amount from your merchant account and sends it back to the customer's original payment method.

- Customer notification: The customer receives confirmation that the refund has been processed and typically sees the credit appear within 3-5 business days.

Different payment methods have varying refund timelines and considerations:

What should you look for in a merchant payment solution?

Choosing the right merchant payment solution affects your customer experience, operational efficiency, and bottom line. Here are key factors to consider when evaluating options:

- Payment method variety: Look for solutions that accept multiple payment types, including cards, digital wallets, and local payment methods for international customers.

- Geographic coverage: If you serve international customers, ensure your payment solution can handle multiple currencies and comply with regional regulations.

- Transaction fees: Compare pricing structures, including per-transaction fees, monthly charges, and currency conversion costs.

- Security features: Verify that the solution includes fraud protection, data encryption, and compliance with payment industry standards.

- Integration capabilities: Choose a solution that integrates smoothly with your existing e-commerce platform, accounting software, and business tools.

- Settlement speed: Consider how quickly funds will be available in your business account after customers make payments.

- Customer support: Ensure you'll have access to help when you need it, especially if you process payments across different time zones.

Accept global payments faster and scale your business

Managing payments across borders often means dealing with multiple currencies, complex compliance requirements, and inconsistent success rates. Traditional payment systems can create friction for international customers and delay your cash flow when you need it most.

PayGlocal simplifies global payment acceptance by providing a complete solution designed for businesses that serve customers worldwide. Whether you're a freelancer working with international clients or an e-commerce business expanding globally, PayGlocal handles the complexity so you can focus on growing your business.

Here's how PayGlocal improves your payment experience:

Multi-currency accounts: Accept payments locally in USD, GBP, EUR, and CAD, making it easier for international customers to pay you while you maintain local banking relationships.

Global payment method coverage: Support 40+ payment methods, including cards, digital wallets, and local payment options that customers prefer in different regions.

Dynamic checkout: Provide customers with payment options tailored to their location and preferences, improving conversion rates and reducing cart abandonment.

Automated compliance documentation: Receive FIRC documents instantly upon settlement, eliminating paperwork delays and ensuring you stay compliant with regulations.

Real-time payment tracking: Monitor every transaction from initiation to settlement with detailed dashboards and automatic notifications.

PayGlocal handles the complexity of global payments while providing you all the tools and features you need to manage your international payments effectively.

Final thoughts

Merchant payments form the foundation of modern business transactions, enabling companies to serve customers globally while maintaining efficient operations. From simple card payments to complex multi-currency processing, the right payment solution can make the difference between a sale and a lost opportunity.

Success in today's market requires payment systems that work seamlessly across borders, currencies, and customer preferences. PayGlocal provides all the tools and support you need to accept payments globally while settling locally.

Ready to improve your payment experience and reach customers worldwide? Get started with PayGlocal today.