Purpose of the blog: The purpose of the blog is to create awareness for our readers around payment methods, their types, benefits, and how to choose the right payment options for accepting payments from global customers efficiently, while also covering how PayGlocal simplifies global payment acceptance.

Over 40% of all payments in India happen digitally. In fact, over 18 billion UPI-based transactions occur every month.

Today's customers expect convenience, security, and flexibility when paying for goods and services. They want to pay using their preferred method, whether that's a credit card, digital wallet, bank transfer, or newer options like buy-now-pay-later.

Get a complete guide about payment methods, from traditional options to modern solutions that help you accept payments from customers worldwide.

- Payment diversity drives sales: Offering multiple payment methods can increase conversion rates as customers prefer familiar options.

- Global reach requires local methods: International customers trust local payment options over foreign alternatives, improving cross-border transactions.

- Security builds trust: Modern payment methods with built-in fraud protection and encryption help reduce chargebacks and build customer confidence.

- Best platform for global payments: PayGlocal offers 40+ global payment methods and multi-currency accounts to accept payments from 180+ countries effortlessly.

A payment method is the way money moves from a customer to a business when purchasing goods or services. Payment methods range from traditional cash and checks to modern digital wallets and bank transfers.

For businesses, payment methods determine how customers can pay for products or services. The options you offer can influence whether someone completes a purchase or abandons their cart. For example, a customer in Germany might prefer SEPA transfers, while someone in India would prefer UPI payments.

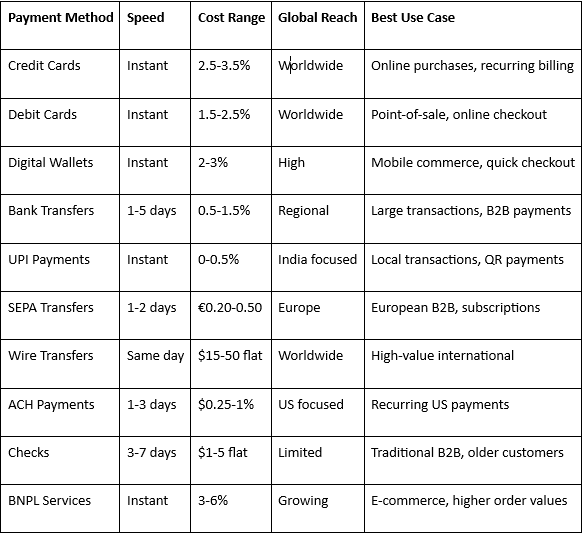

There are different payment methods with each offering various features. Some stand out for speed, while others are good for global reach. Here's how the most common payment method types compare:

Each payment method serves different customer needs and business requirements based on geography, transaction size, and industry preferences. Let’s take a detailed look at them.

Credit cards allow customers to borrow money for purchases and pay later, either in full or through monthly payments. Major networks include Visa, Mastercard, and American Express, with acceptance in over 200 countries worldwide.

Key Features:

-Instant processing: Transactions complete within seconds, and funds arrive in 1-2 business days.

- Global acceptance: Works across borders with automatic currency conversion.

- Fraud protection: Built-in security features protect both merchants and customers.

- Reward programs: Many cards offer cashback or points that encourage customer loyalty.

- Chargeback capability: Customers can dispute transactions, providing buyer protection.

Cost: Credit card processing typically costs merchants 2.5-3.5% per transaction plus potential monthly fees and gateway charges.

Best for: Credit cards work well for online businesses, subscription services, and companies targeting international customers. For instance, a SaaS company can accept payments from clients worldwide while providing a familiar payment experience that builds trust.

Debit cards withdraw money directly from customers' bank accounts at the time of purchase. They use the same networks as credit cards but access existing funds rather than extending credit.

Key Features:

- Real-time fund transfer: Money moves immediately from the customer's account.

- Lower risk: No credit risk since funds must be available at purchase time.

- Wide acceptance: Accepted wherever credit cards work globally.

- PIN security: Additional security layer through PIN verification for in-person transactions.

- Spending limits: Natural spending controls based on available account balance.

Cost: Debit card processing costs merchants 1.5-2.5% per transaction, generally lower than credit cards due to reduced risk.

Best for: Debit cards suit businesses with cost-conscious customers and point-of-sale transactions. For example, grocery stores and retail shops benefit from lower processing fees while serving customers who prefer spending their own money.

Digital wallets store payment information securely and enable quick transactions through mobile apps or websites. Popular options include Apple Pay, Google Pay, PayPal, and regional favorites like Paytm in India.

Key Features:

- One-tap payments: Customers pay without entering card details repeatedly.

- Biometric security: Fingerprint or face recognition adds security layers.

- Multi-payment source: You can link to multiple cards or bank accounts.

- Contactless transactions: Works for both online and in-store purchases.

- Cross-platform compatibility: Available on various devices and operating systems.

Cost: Digital wallet processing typically costs 2-3% per transaction, similar to credit cards but often with better conversion rates.

Best for: Digital wallets excel for mobile commerce and businesses targeting tech-savvy customers. An e-commerce store offering Apple Pay can reduce checkout friction and increase mobile conversions significantly.

Bank transfers move money directly between accounts through banking networks like NEFT and RTGS in India, SEPA in Europe, or ACH in the US. These transfers bypass card networks entirely.

Key Features:

- Direct bank-to-bank: No intermediary payment processors required.

- High transaction limits: It can handle large amounts without restrictions.

- Lower fraud risk: Difficult to reverse or manipulate once processed.

- Account verification: Requires valid bank account details for completion.

- Batch processing: Often processed in scheduled batches throughout the day.

Cost: Bank transfers typically cost 0.5-1.5% or flat fees ranging from $1-25, depending on the network and transfer type.

Best for: Bank transfers work well for B2B payments, large transactions, and recurring billing. For instance, a consulting firm receiving monthly retainers from enterprise clients benefits from lower costs and higher limits.

UPI (Unified Payments Interface) enables instant bank-to-bank transfers in India using mobile numbers, QR codes, or virtual payment addresses. It connects directly to bank accounts without requiring cards.

Key Features:

- Instant settlement: Money transfers immediately between bank accounts.

- QR code support: Customers scan codes to pay without entering details.

- 24/7 availability: Works around the clock, including weekends and holidays.

- Multi-bank support: A single app can access multiple bank accounts.

- Transaction limits: Daily limits ensure security while allowing regular use.

Cost: UPI transactions cost merchants 0-0.5%, making it one of the most affordable payment methods available.

Best for: UPI is perfect for Indian businesses, small transactions, and offline-to-online commerce. A local restaurant can display QR codes for customers to pay instantly without handling cash or cards.

SEPA (Single Euro Payments Area) transfers enable euro payments across 41 countries using standardized payment processes. Both instant and regular SEPA transfers are available.

Key Features:

- Euro zone coverage: Works across all EU countries plus several others.

- Standardized processing: Consistent rules and timelines across participating countries.

- Instant SEPA option: Funds transfer within seconds for urgent payments.

- IBAN-based: Uses International Bank Account Number (IBAN) for accuracy.

- Regulatory protection: Strong consumer rights and dispute resolution processes.

Cost: SEPA transfers typically cost €0.20-0.50 per transaction, making them very affordable for European businesses.

Best for: SEPA transfers suit European businesses, subscription services, and B2B payments within the euro zone. A European SaaS company can collect recurring payments cost-effectively from customers across multiple countries.

Wire transfers send money internationally through correspondent banking networks like SWIFT. They provide secure, traceable transfers for high-value transactions across borders.

Key Features:

- Global reach: You can send money to virtually any country with banking infrastructure.

- High security: Multiple verification steps and encryption protect large transfers.

- Detailed tracking: Full transaction trail from sender to receiver.

- Same-day processing: Often complete within hours for urgent transfers.

- No amount limits: You can handle very large corporate transactions.

Cost: Wire transfers typically cost $15-50 flat fee plus potential currency conversion charges and receiving bank fees.

Best for: Wire transfers work best for large international transactions, real estate purchases, and enterprise payments. An export business receiving payment for large shipments benefits from the security and traceability.

ACH (Automated Clearing House) payments process electronic transfers between US bank accounts through the Federal Reserve's network. They handle both one-time and recurring payments efficiently.

Key Features:

Batch processing: Transactions are processed in scheduled batches for efficiency.

Same-day ACH: A faster processing option is available for urgent payments.

Reversible transactions: They can be returned for insufficient funds or disputes.

Direct deposit capability: Supports both debits and credits to accounts.

Regulatory oversight: Governed by NACHA (National Automated Clearing House Association) rules for consistency and security.

Cost: ACH payments typically cost $0.25-1% or flat fees under $5, making them very affordable for US businesses.

Best for: ACH payments excel for US recurring billing, payroll, and B2B transactions. A subscription business can collect monthly payments automatically while keeping costs low.

Checks are paper-based payment instruments that authorize banks to transfer specified amounts from one account to another. While declining in usage, they remain relevant in certain industries and regions.

Key Features:

- Physical verification: Signed paper provides legal payment authorization.

- Delayed processing: Funds don't transfer until the check is deposited and cleared.

- Stop payment option: Can be cancelled before processing if needed.

- Detailed records: Provides a paper trail for accounting and tax purposes.

- No technology required: Works without internet or electronic systems.

Cost: Check processing typically costs $1-5 per transaction plus potential bank fees for deposits and collections.

Best for: Checks work for traditional B2B payments, older customer demographics, and industries requiring paper documentation. A law firm might accept checks from clients who prefer traditional payment methods.

BNPL services let customers split purchases into installments without traditional credit checks. Popular providers include Klarna, Afterpay, and Sezzle across different markets.

Key Features:

Instant approval: Customers get approved within seconds during checkout.

Flexible terms: Options from 4 weekly payments to longer monthly plans.

Merchant protection: BNPL provider handles collection and default risk.

Interest-free periods: Often no charges if customers pay on time.

Credit building: Some services help customers build credit history.

Cost: BNPL services typically cost merchants 3-6% per transaction plus potential flat fees for each installment.

Best for: BNPL works well for e-commerce, fashion, electronics, and higher-ticket items. An online furniture store can increase average order values by letting customers pay over time.

Providing diverse payment options creates competitive advantages and directly impacts your business profits. Here's why payment method variety matters for your business.

- Higher conversion rates: Customers abandon purchases when their preferred payment method isn't available.

- Global market access: Different regions prefer different payment methods. European customers favor SEPA transfers, while Southeast Asian customers prefer digital wallets and bank transfers.

- Reduced cart abandonment: Familiar payment methods build trust and reduce friction at checkout. Customers are more likely to complete purchases using methods they know and trust.

- Improved cash flow: Instant payment methods like cards and digital wallets provide immediate access to funds, improving working capital compared to slower methods like checks.

- Enhanced customer experience: Offering choice shows you understand and care about customer preferences, building loyalty, and encouraging repeat purchases.

Selecting payment methods requires balancing customer needs, business costs, and operational requirements. The right mix depends on your specific situation and growth goals.

Start by learning where your customers are located and how they prefer to pay. Research payment preferences in your target markets. For instance, German customers often prefer direct bank transfers, while US customers favor credit cards.

Survey existing customers about their payment preferences and analyze checkout abandonment data to identify gaps. Look for patterns in failed transactions that might indicate missing payment options.

Different payment methods have varying costs and settlement times. Credit cards typically cost 2-4% but process instantly, while bank transfers cost less but take days to settle. Calculate the total cost, including processing fees, currency conversion, and operational overhead.

Consider how processing times affect your cash flow and customer satisfaction. Instant payments improve customer experience but might cost more, while slower methods can strain working capital.

Subscription businesses need recurring payment capabilities, while e-commerce stores benefit from different one-time payment options. B2B companies might prioritize bank transfers and invoicing, while B2C businesses focus on cards and digital wallets.

For example, a SaaS company targeting enterprises might emphasize bank transfers and invoicing, while a consumer app would prioritize cards and mobile wallets.

If you're selling globally or plan to expand internationally, research payment preferences in target markets early. Some regions have strong preferences for local payment methods that international cards can't replace.

Consider currency requirements and compliance needs for different markets. European businesses need GDPR compliance, while some countries require local payment processing.

Managing multiple payment methods across different countries creates complexity that can slow your growth. Currency conversions, compliance requirements, and integration challenges often overwhelm businesses trying to scale internationally.

PayGlocal simplifies global payment acceptance by providing everything you need in one platform. Whether you're a freelancer receiving payments from international clients or an enterprise expanding globally, you get the tools to accept payments efficiently.

- Global payment methods: Accept payments via credit cards, digital wallets, bank transfers, and local payment methods across 180+ countries without separate integrations.

- Multi-currency accounts in USD, EUR, GBP, CAD: Receive payments in local currencies and settle in INR, reducing conversion costs and improving customer trust.

- Dynamic checkout: Automatically show customers their preferred payment methods based on location and device, increasing conversion rates.

- Instant compliance documentation: Get FIRC and other compliance documents automatically, saving time on paperwork and regulatory requirements.

- Transparent pricing with no hidden fees: Pay only when you transact with competitive rates and no setup costs, monthly fees, or surprise charges.

PayGlocal scales with your business while keeping payment acceptance simple and cost-effective, so you can focus on growing your business while the platform handles the complexity of global payments.

Payment methods are the foundation of customer experience and business growth. The options you offer determine who can buy from you and how smoothly transactions are completed. While traditional methods like cards remain important, digital wallets and local payment methods are becoming essential for global competitiveness.

Choosing the right payment methods requires knowing your customers, evaluating costs, and planning for growth. Businesses that offer diverse, localized payment options consistently outperform those with limited choices. PayGlocal helps companies accept payments globally while maintaining simplicity and transparency.

The fastest-growing businesses have already solved payment complexity by choosing platforms that handle multiple methods and currencies effortlessly. Don't let payment limitations slow your growth when global customers are ready to buy. Get started with PayGlocal today.

Over 40% of all payments in India happen digitally. In fact, over 18 billion UPI-based transactions occur every month.

Today's customers expect convenience, security, and flexibility when paying for goods and services. They want to pay using their preferred method, whether that's a credit card, digital wallet, bank transfer, or newer options like buy-now-pay-later.

Get a complete guide about payment methods, from traditional options to modern solutions that help you accept payments from customers worldwide.

Key takeaways:

- Payment diversity drives sales: Offering multiple payment methods can increase conversion rates as customers prefer familiar options.

- Global reach requires local methods: International customers trust local payment options over foreign alternatives, improving cross-border transactions.

- Security builds trust: Modern payment methods with built-in fraud protection and encryption help reduce chargebacks and build customer confidence.

- Best platform for global payments: PayGlocal offers 40+ global payment methods and multi-currency accounts to accept payments from 180+ countries effortlessly.

What are payment methods?

A payment method is the way money moves from a customer to a business when purchasing goods or services. Payment methods range from traditional cash and checks to modern digital wallets and bank transfers.

For businesses, payment methods determine how customers can pay for products or services. The options you offer can influence whether someone completes a purchase or abandons their cart. For example, a customer in Germany might prefer SEPA transfers, while someone in India would prefer UPI payments.

What are the main types of payment methods?

There are different payment methods with each offering various features. Some stand out for speed, while others are good for global reach. Here's how the most common payment method types compare:

Each payment method serves different customer needs and business requirements based on geography, transaction size, and industry preferences. Let’s take a detailed look at them.

Credit cards

Credit cards allow customers to borrow money for purchases and pay later, either in full or through monthly payments. Major networks include Visa, Mastercard, and American Express, with acceptance in over 200 countries worldwide.

Key Features:

-Instant processing: Transactions complete within seconds, and funds arrive in 1-2 business days.

- Global acceptance: Works across borders with automatic currency conversion.

- Fraud protection: Built-in security features protect both merchants and customers.

- Reward programs: Many cards offer cashback or points that encourage customer loyalty.

- Chargeback capability: Customers can dispute transactions, providing buyer protection.

Cost: Credit card processing typically costs merchants 2.5-3.5% per transaction plus potential monthly fees and gateway charges.

Best for: Credit cards work well for online businesses, subscription services, and companies targeting international customers. For instance, a SaaS company can accept payments from clients worldwide while providing a familiar payment experience that builds trust.

Debit cards

Debit cards withdraw money directly from customers' bank accounts at the time of purchase. They use the same networks as credit cards but access existing funds rather than extending credit.

Key Features:

- Real-time fund transfer: Money moves immediately from the customer's account.

- Lower risk: No credit risk since funds must be available at purchase time.

- Wide acceptance: Accepted wherever credit cards work globally.

- PIN security: Additional security layer through PIN verification for in-person transactions.

- Spending limits: Natural spending controls based on available account balance.

Cost: Debit card processing costs merchants 1.5-2.5% per transaction, generally lower than credit cards due to reduced risk.

Best for: Debit cards suit businesses with cost-conscious customers and point-of-sale transactions. For example, grocery stores and retail shops benefit from lower processing fees while serving customers who prefer spending their own money.

Digital wallets

Digital wallets store payment information securely and enable quick transactions through mobile apps or websites. Popular options include Apple Pay, Google Pay, PayPal, and regional favorites like Paytm in India.

Key Features:

- One-tap payments: Customers pay without entering card details repeatedly.

- Biometric security: Fingerprint or face recognition adds security layers.

- Multi-payment source: You can link to multiple cards or bank accounts.

- Contactless transactions: Works for both online and in-store purchases.

- Cross-platform compatibility: Available on various devices and operating systems.

Cost: Digital wallet processing typically costs 2-3% per transaction, similar to credit cards but often with better conversion rates.

Best for: Digital wallets excel for mobile commerce and businesses targeting tech-savvy customers. An e-commerce store offering Apple Pay can reduce checkout friction and increase mobile conversions significantly.

Bank transfers

Bank transfers move money directly between accounts through banking networks like NEFT and RTGS in India, SEPA in Europe, or ACH in the US. These transfers bypass card networks entirely.

Key Features:

- Direct bank-to-bank: No intermediary payment processors required.

- High transaction limits: It can handle large amounts without restrictions.

- Lower fraud risk: Difficult to reverse or manipulate once processed.

- Account verification: Requires valid bank account details for completion.

- Batch processing: Often processed in scheduled batches throughout the day.

Cost: Bank transfers typically cost 0.5-1.5% or flat fees ranging from $1-25, depending on the network and transfer type.

Best for: Bank transfers work well for B2B payments, large transactions, and recurring billing. For instance, a consulting firm receiving monthly retainers from enterprise clients benefits from lower costs and higher limits.

UPI payments

UPI (Unified Payments Interface) enables instant bank-to-bank transfers in India using mobile numbers, QR codes, or virtual payment addresses. It connects directly to bank accounts without requiring cards.

Key Features:

- Instant settlement: Money transfers immediately between bank accounts.

- QR code support: Customers scan codes to pay without entering details.

- 24/7 availability: Works around the clock, including weekends and holidays.

- Multi-bank support: A single app can access multiple bank accounts.

- Transaction limits: Daily limits ensure security while allowing regular use.

Cost: UPI transactions cost merchants 0-0.5%, making it one of the most affordable payment methods available.

Best for: UPI is perfect for Indian businesses, small transactions, and offline-to-online commerce. A local restaurant can display QR codes for customers to pay instantly without handling cash or cards.

SEPA transfers

SEPA (Single Euro Payments Area) transfers enable euro payments across 41 countries using standardized payment processes. Both instant and regular SEPA transfers are available.

Key Features:

- Euro zone coverage: Works across all EU countries plus several others.

- Standardized processing: Consistent rules and timelines across participating countries.

- Instant SEPA option: Funds transfer within seconds for urgent payments.

- IBAN-based: Uses International Bank Account Number (IBAN) for accuracy.

- Regulatory protection: Strong consumer rights and dispute resolution processes.

Cost: SEPA transfers typically cost €0.20-0.50 per transaction, making them very affordable for European businesses.

Best for: SEPA transfers suit European businesses, subscription services, and B2B payments within the euro zone. A European SaaS company can collect recurring payments cost-effectively from customers across multiple countries.

Wire transfers

Wire transfers send money internationally through correspondent banking networks like SWIFT. They provide secure, traceable transfers for high-value transactions across borders.

Key Features:

- Global reach: You can send money to virtually any country with banking infrastructure.

- High security: Multiple verification steps and encryption protect large transfers.

- Detailed tracking: Full transaction trail from sender to receiver.

- Same-day processing: Often complete within hours for urgent transfers.

- No amount limits: You can handle very large corporate transactions.

Cost: Wire transfers typically cost $15-50 flat fee plus potential currency conversion charges and receiving bank fees.

Best for: Wire transfers work best for large international transactions, real estate purchases, and enterprise payments. An export business receiving payment for large shipments benefits from the security and traceability.

ACH payments

ACH (Automated Clearing House) payments process electronic transfers between US bank accounts through the Federal Reserve's network. They handle both one-time and recurring payments efficiently.

Key Features:

Batch processing: Transactions are processed in scheduled batches for efficiency.

Same-day ACH: A faster processing option is available for urgent payments.

Reversible transactions: They can be returned for insufficient funds or disputes.

Direct deposit capability: Supports both debits and credits to accounts.

Regulatory oversight: Governed by NACHA (National Automated Clearing House Association) rules for consistency and security.

Cost: ACH payments typically cost $0.25-1% or flat fees under $5, making them very affordable for US businesses.

Best for: ACH payments excel for US recurring billing, payroll, and B2B transactions. A subscription business can collect monthly payments automatically while keeping costs low.

Checks

Checks are paper-based payment instruments that authorize banks to transfer specified amounts from one account to another. While declining in usage, they remain relevant in certain industries and regions.

Key Features:

- Physical verification: Signed paper provides legal payment authorization.

- Delayed processing: Funds don't transfer until the check is deposited and cleared.

- Stop payment option: Can be cancelled before processing if needed.

- Detailed records: Provides a paper trail for accounting and tax purposes.

- No technology required: Works without internet or electronic systems.

Cost: Check processing typically costs $1-5 per transaction plus potential bank fees for deposits and collections.

Best for: Checks work for traditional B2B payments, older customer demographics, and industries requiring paper documentation. A law firm might accept checks from clients who prefer traditional payment methods.

Buy Now Pay Later services

BNPL services let customers split purchases into installments without traditional credit checks. Popular providers include Klarna, Afterpay, and Sezzle across different markets.

Key Features:

Instant approval: Customers get approved within seconds during checkout.

Flexible terms: Options from 4 weekly payments to longer monthly plans.

Merchant protection: BNPL provider handles collection and default risk.

Interest-free periods: Often no charges if customers pay on time.

Credit building: Some services help customers build credit history.

Cost: BNPL services typically cost merchants 3-6% per transaction plus potential flat fees for each installment.

Best for: BNPL works well for e-commerce, fashion, electronics, and higher-ticket items. An online furniture store can increase average order values by letting customers pay over time.

What are the benefits of offering multiple payment methods?

Providing diverse payment options creates competitive advantages and directly impacts your business profits. Here's why payment method variety matters for your business.

- Higher conversion rates: Customers abandon purchases when their preferred payment method isn't available.

- Global market access: Different regions prefer different payment methods. European customers favor SEPA transfers, while Southeast Asian customers prefer digital wallets and bank transfers.

- Reduced cart abandonment: Familiar payment methods build trust and reduce friction at checkout. Customers are more likely to complete purchases using methods they know and trust.

- Improved cash flow: Instant payment methods like cards and digital wallets provide immediate access to funds, improving working capital compared to slower methods like checks.

- Enhanced customer experience: Offering choice shows you understand and care about customer preferences, building loyalty, and encouraging repeat purchases.

How do you choose the right payment methods for your business?

Selecting payment methods requires balancing customer needs, business costs, and operational requirements. The right mix depends on your specific situation and growth goals.

1. Consider your customer base and location

Start by learning where your customers are located and how they prefer to pay. Research payment preferences in your target markets. For instance, German customers often prefer direct bank transfers, while US customers favor credit cards.

Survey existing customers about their payment preferences and analyze checkout abandonment data to identify gaps. Look for patterns in failed transactions that might indicate missing payment options.

2. Evaluate transaction costs and processing times

Different payment methods have varying costs and settlement times. Credit cards typically cost 2-4% but process instantly, while bank transfers cost less but take days to settle. Calculate the total cost, including processing fees, currency conversion, and operational overhead.

Consider how processing times affect your cash flow and customer satisfaction. Instant payments improve customer experience but might cost more, while slower methods can strain working capital.

3. Match methods to your business model

Subscription businesses need recurring payment capabilities, while e-commerce stores benefit from different one-time payment options. B2B companies might prioritize bank transfers and invoicing, while B2C businesses focus on cards and digital wallets.

For example, a SaaS company targeting enterprises might emphasize bank transfers and invoicing, while a consumer app would prioritize cards and mobile wallets.

4. Plan for international expansion

If you're selling globally or plan to expand internationally, research payment preferences in target markets early. Some regions have strong preferences for local payment methods that international cards can't replace.

Consider currency requirements and compliance needs for different markets. European businesses need GDPR compliance, while some countries require local payment processing.

Get paid globally faster and at lower costs using PayGlocal

Managing multiple payment methods across different countries creates complexity that can slow your growth. Currency conversions, compliance requirements, and integration challenges often overwhelm businesses trying to scale internationally.

PayGlocal simplifies global payment acceptance by providing everything you need in one platform. Whether you're a freelancer receiving payments from international clients or an enterprise expanding globally, you get the tools to accept payments efficiently.

- Global payment methods: Accept payments via credit cards, digital wallets, bank transfers, and local payment methods across 180+ countries without separate integrations.

- Multi-currency accounts in USD, EUR, GBP, CAD: Receive payments in local currencies and settle in INR, reducing conversion costs and improving customer trust.

- Dynamic checkout: Automatically show customers their preferred payment methods based on location and device, increasing conversion rates.

- Instant compliance documentation: Get FIRC and other compliance documents automatically, saving time on paperwork and regulatory requirements.

- Transparent pricing with no hidden fees: Pay only when you transact with competitive rates and no setup costs, monthly fees, or surprise charges.

PayGlocal scales with your business while keeping payment acceptance simple and cost-effective, so you can focus on growing your business while the platform handles the complexity of global payments.

Final thoughts

Payment methods are the foundation of customer experience and business growth. The options you offer determine who can buy from you and how smoothly transactions are completed. While traditional methods like cards remain important, digital wallets and local payment methods are becoming essential for global competitiveness.

Choosing the right payment methods requires knowing your customers, evaluating costs, and planning for growth. Businesses that offer diverse, localized payment options consistently outperform those with limited choices. PayGlocal helps companies accept payments globally while maintaining simplicity and transparency.

The fastest-growing businesses have already solved payment complexity by choosing platforms that handle multiple methods and currencies effortlessly. Don't let payment limitations slow your growth when global customers are ready to buy. Get started with PayGlocal today.