Indian businesses are collecting more international payments than before. Recent figures show service exports grew by 8.65% from April to August 2025. This growth brings more payment pathways that need proper tracking and reconciliation.

When you're managing payments from multiple clients across different countries, matching each transaction to the right invoice becomes time-consuming work. Miss one detail and your cash flow tracking falls apart.

Virtual accounts solve this problem. They give you unique account numbers for different payment sources while everything settles into one main account. No more guessing which payment came from which client or marketplace.

In this guide, we break down what virtual accounts are, how they work, their benefits, and why they matter for businesses handling multiple payment streams. You'll also learn how to choose the right solution for your needs. So, let’s get started.

A virtual account is a unique account number linked to your main bank account. It acts as a digital identifier that helps you track payments from different sources without opening separate physical bank accounts.

When someone sends money to a virtual account number, the funds automatically transfer to your primary account. The system logs who sent the payment, when it arrived, and which virtual account received it. You get complete visibility into every transaction without manual tracking.

Virtual accounts don't hold money themselves. They work as pass-through identifiers. The funds move immediately to your actual bank account while the system maintains a clear record of the payment source. This makes reconciliation automatic and accurate.

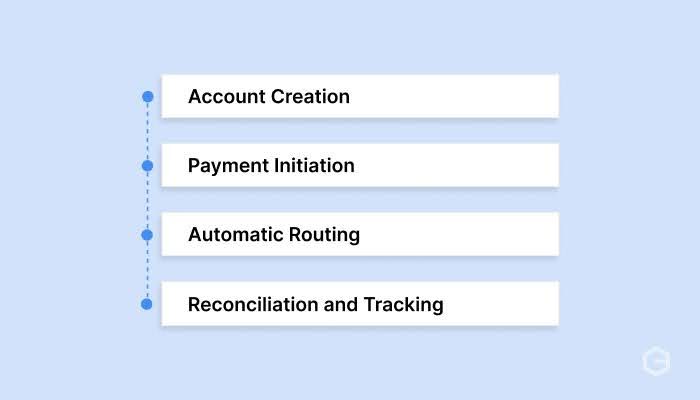

Virtual accounts operate through a simple four-step process that connects payers to your main account while maintaining clear transaction records.

Here's what happens during a typical virtual account transaction:

Account creation: You or your payment provider generates a unique virtual account number for a specific purpose. This could be for an individual customer, a particular invoice, or a revenue stream like marketplace settlements.

Payment initiation: Your client or payer receives the virtual account number as their payment destination. They send funds using standard methods like bank transfer, NEFT, RTGS, or SWIFT, depending on the currency and location.

Automatic routing: When the payment arrives at the virtual account, the system immediately identifies the source and purpose. The funds transfer to your primary physical bank account within minutes or seconds, depending on the payment method.

Reconciliation and tracking: The system logs all payment details, including sender information, amount, timestamp, and the specific virtual account used. You can view these details on your dashboard and match them to invoices or customers automatically. This banking reconciliation happens instantly without manual effort.

This process removes manual reconciliation work. Instead of checking bank statements and matching payments to a list of expected transactions, the system does it for you. You see exactly which customer paid, how much they sent, and when you'll receive the settlement.

Virtual accounts significantly enhance how businesses handle payment collection and reconciliation. Here's what makes them valuable for growing companies.

Lower error rates: Automatic reconciliation means fewer misallocated payments. When errors do occur, you can identify and fix them quickly because every transaction has clear source information.

Multi-currency capability: For businesses collecting international payments, virtual accounts can support multiple currencies while settling everything into your local account.

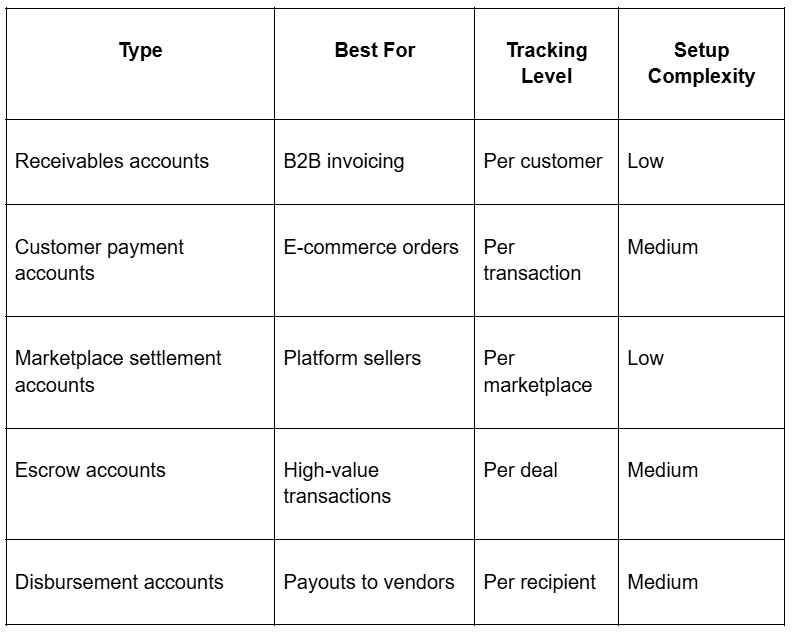

There are different types of virtual accounts. Before choosing a type, consider how you collect payments and what level of detail you need for tracking. Here's how they compare:

Each type serves specific payment scenarios while maintaining the core benefit of automatic reconciliation.

1. Receivables accounts

These accounts link to specific customers or invoices. When you send an invoice, you include a unique virtual account number. The customer pays to that number and your system automatically marks the invoice as paid.

For instance, a software company with 200 enterprise clients creates one virtual account per client. When renewals come due, each client pays to their assigned account. The finance team sees exactly which clients have paid without checking email confirmations or bank statements.

2. Customer payment accounts

E-commerce businesses use these for individual orders or transactions. Each purchase gets its own virtual account number that appears on the checkout page or payment confirmation.

A fashion export brand selling globally might generate a virtual account for each international order. When the customer completes payment, the system matches it to the order, triggers fulfillment, and updates inventory automatically. This helps avoid international payment challenges that slow down order processing.

3. Marketplace settlement accounts

If you sell on multiple platforms like Amazon Global, Etsy, or B2B marketplaces, virtual accounts help separate revenue streams. Each marketplace pays into a dedicated virtual account, making it easy to track performance by platform.

For example, an electronics exporter working with three marketplaces creates three virtual accounts. Settlement data flows into one main account, but reports clearly show revenue and margins for each platform separately. This clarity helps with invoices for businesses and financial planning.

4. Escrow accounts

High-value transactions or projects with milestone payments benefit from escrow-style virtual accounts. Funds are received and held in separate tracking buckets until conditions are met.

A manufacturing exporter might use this for large orders with payment terms like 30% advance, 40% on production completion, and 30% on delivery. Each milestone has its own virtual account for clear tracking.

5. Disbursement accounts

These handle outgoing payments to contractors, vendors, or partners. While less common for receivables, they help businesses track who received payouts and when.

An IT services company paying multiple freelancers across countries can use disbursement virtual accounts to maintain clear records of all contractor payments for tax and audit purposes.

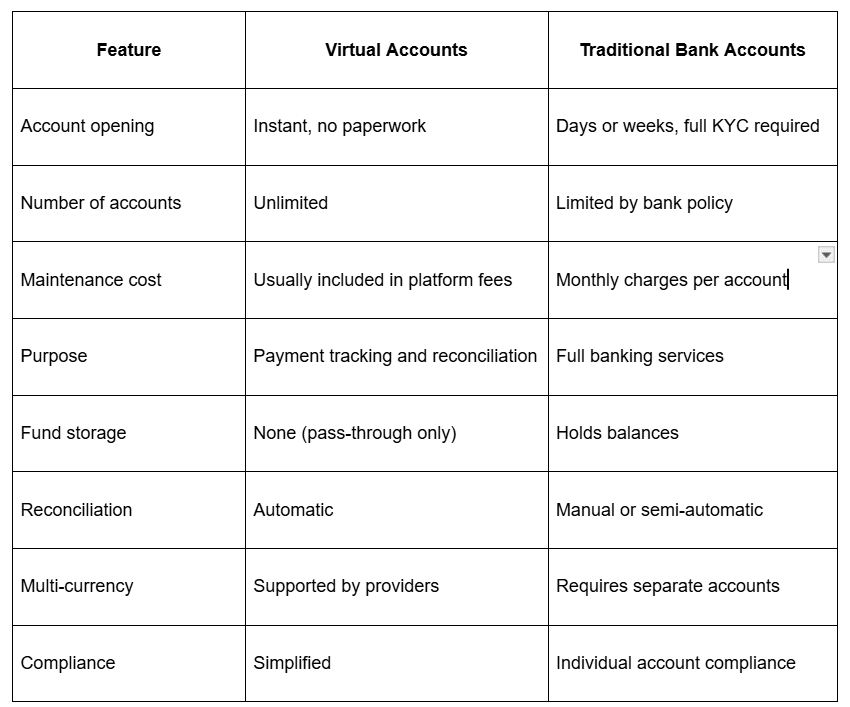

Virtual accounts and traditional bank accounts serve different purposes in your payment infrastructure. Here's what sets them apart.

Traditional accounts give you a place to store and manage money with full banking features like checkbooks, cards, and branch access. Virtual accounts focus purely on payment identification and routing.

You need a traditional account as your settlement destination. Virtual accounts sit on top of it to make payment collection cleaner and more efficient. Think of traditional accounts as your vault and virtual accounts as labeled drawers that help you organize what goes into them.

For businesses handling multiple payment sources, the combination works best. Your main account holds all funds, while virtual accounts track where each payment came from.

Selecting a virtual account provider depends on your payment volume, currencies needed, and business model. Here's what matters most.

Currency support: Check which currencies the provider supports and whether they offer local account numbers in those currencies. For instance, if you collect payments from US and UK clients, you need USD and GBP virtual accounts that look local to those payers.

Integration options: The solution should connect with your existing accounting software, ERP, or e-commerce platform. API access matters if you want to automate account creation or pull reconciliation data into your systems.

Settlement speed: Find out how quickly funds move from virtual accounts to your main account. Same-day settlement keeps your cash flow healthy, while multi-day delays can create problems for businesses with tight working capital.

Compliance documentation: For export businesses, automatic FIRC (Foreign Inward Remittance Certificate) generation saves significant time. The provider should deliver compliance documents without manual requests.

Pricing structure: Compare transaction fees, setup costs, and monthly charges. Some providers charge per virtual account, while others include unlimited accounts in their platform fees. Calculate total costs based on your expected transaction volume.

Customer support: Payment issues need fast resolution. Check if the provider offers responsive support through your preferred channels and whether they handle queries in your timezone.

Scalability: Your payment volume will grow. Make sure the provider can handle increased transactions without performance issues or requiring you to switch platforms later.

Managing international payments shouldn't require multiple bank accounts, confusing reconciliation, or delayed settlements. You need a solution that tracks every payment clearly while handling multiple currencies without complexity.

PayGlocal gives you the payment infrastructure designed for businesses collecting payments globally and settling locally. Whether you're an exporter, freelancer, or service provider, you get all the tools you need to manage global transactions effectively.

Here's what you get with PayGlocal:

Multi-currency accounts: Collect payments in USD, GBP, EUR, and CAD with local account numbers that look familiar to your international clients. Receive payments from 180+ countries across 33 currencies.

Card payments: Process international credit and debit cards with industry-leading approval rates through smart payment orchestration and enhanced messaging.

Global payment methods: Offer 40+ local payment methods to build trust with international customers and increase sales in markets with low card adoption.

Instant compliance documents: Get FIRC automatically delivered to your inbox after every settlement. No manual requests, no paperwork delays.

Zero fixed costs: Pay only when you transact. No setup fees, no platform charges, no monthly maintenance costs.

PayGlocal helps you collect globally, track automatically, and settle in INR without the complexity of traditional banking infrastructure.

Virtual accounts have changed how businesses collect payments. Instead of handling multiple bank accounts or spending hours on reconciliation, you get automatic tracking and instant payment identification.

For businesses working across borders, virtual accounts become even more valuable. Collecting in multiple currencies while maintaining clear records requires infrastructure that traditional banking can't provide efficiently. Modern payment platforms make this simple.

If you're ready to collect payments globally without the manual work, PayGlocal gives you virtual accounts across major currencies with automatic compliance documentation. Your international clients pay easily while you settle in INR with complete visibility.

Get started with PayGlocal today and handle international payments with the security and speed your business deserves.

When you're managing payments from multiple clients across different countries, matching each transaction to the right invoice becomes time-consuming work. Miss one detail and your cash flow tracking falls apart.

Virtual accounts solve this problem. They give you unique account numbers for different payment sources while everything settles into one main account. No more guessing which payment came from which client or marketplace.

In this guide, we break down what virtual accounts are, how they work, their benefits, and why they matter for businesses handling multiple payment streams. You'll also learn how to choose the right solution for your needs. So, let’s get started.

Key takeaways

- Unique tracking made simple: Virtual accounts assign unique account numbers to each payer, making payment identification instant and automatic.

- No physical accounts needed: All funds route to one main bank account while maintaining separate tracking for each payment source.

- Automated reconciliation: Payments are matched to customers or invoices automatically, saving hours of manual work.

- Better cash flow visibility: Track exactly where money comes from and when it arrives without spreadsheet guesswork.

- Multi-currency support: Global payment solutions like PayGlocal offer accounts across multiple currencies for global payment collection.

What is a virtual account?

A virtual account is a unique account number linked to your main bank account. It acts as a digital identifier that helps you track payments from different sources without opening separate physical bank accounts.

When someone sends money to a virtual account number, the funds automatically transfer to your primary account. The system logs who sent the payment, when it arrived, and which virtual account received it. You get complete visibility into every transaction without manual tracking.

Virtual accounts don't hold money themselves. They work as pass-through identifiers. The funds move immediately to your actual bank account while the system maintains a clear record of the payment source. This makes reconciliation automatic and accurate.

How does a virtual account work?

Virtual accounts operate through a simple four-step process that connects payers to your main account while maintaining clear transaction records.

Here's what happens during a typical virtual account transaction:

Account creation: You or your payment provider generates a unique virtual account number for a specific purpose. This could be for an individual customer, a particular invoice, or a revenue stream like marketplace settlements.

Payment initiation: Your client or payer receives the virtual account number as their payment destination. They send funds using standard methods like bank transfer, NEFT, RTGS, or SWIFT, depending on the currency and location.

Automatic routing: When the payment arrives at the virtual account, the system immediately identifies the source and purpose. The funds transfer to your primary physical bank account within minutes or seconds, depending on the payment method.

Reconciliation and tracking: The system logs all payment details, including sender information, amount, timestamp, and the specific virtual account used. You can view these details on your dashboard and match them to invoices or customers automatically. This banking reconciliation happens instantly without manual effort.

This process removes manual reconciliation work. Instead of checking bank statements and matching payments to a list of expected transactions, the system does it for you. You see exactly which customer paid, how much they sent, and when you'll receive the settlement.

What are the benefits of virtual accounts?

Virtual accounts significantly enhance how businesses handle payment collection and reconciliation. Here's what makes them valuable for growing companies.

- Instant payment identification: Each payer gets a unique account number, so you know immediately who sent money. No more checking email threads or calling customers to confirm payments. The system matches every transaction to the right source automatically.

- Reduced reconciliation time: Manual matching can take hours or days depending on transaction volume. Virtual accounts cut this to zero. Your finance team stops spending time on spreadsheets and focuses on more important work.

- Better cash flow tracking: You see exactly where money comes from in real time. Track payments by customer, marketplace, invoice, or any other category you need. This visibility helps you make faster decisions about spending and growth.

- No maintenance overhead: Opening and managing multiple physical bank accounts requires paperwork, monthly fees, and ongoing administration. Virtual accounts eliminate this completely. Create as many as you need with no extra compliance burden.

- Scales effortlessly: Whether you have 10 clients or 10,000, virtual accounts handle growth without additional infrastructure. Add new account numbers instantly as your business expands into new markets or adds more customers.

Lower error rates: Automatic reconciliation means fewer misallocated payments. When errors do occur, you can identify and fix them quickly because every transaction has clear source information.

Multi-currency capability: For businesses collecting international payments, virtual accounts can support multiple currencies while settling everything into your local account.

What are the types of virtual accounts?

There are different types of virtual accounts. Before choosing a type, consider how you collect payments and what level of detail you need for tracking. Here's how they compare:

Each type serves specific payment scenarios while maintaining the core benefit of automatic reconciliation.

1. Receivables accounts

These accounts link to specific customers or invoices. When you send an invoice, you include a unique virtual account number. The customer pays to that number and your system automatically marks the invoice as paid.

For instance, a software company with 200 enterprise clients creates one virtual account per client. When renewals come due, each client pays to their assigned account. The finance team sees exactly which clients have paid without checking email confirmations or bank statements.

2. Customer payment accounts

E-commerce businesses use these for individual orders or transactions. Each purchase gets its own virtual account number that appears on the checkout page or payment confirmation.

A fashion export brand selling globally might generate a virtual account for each international order. When the customer completes payment, the system matches it to the order, triggers fulfillment, and updates inventory automatically. This helps avoid international payment challenges that slow down order processing.

3. Marketplace settlement accounts

If you sell on multiple platforms like Amazon Global, Etsy, or B2B marketplaces, virtual accounts help separate revenue streams. Each marketplace pays into a dedicated virtual account, making it easy to track performance by platform.

For example, an electronics exporter working with three marketplaces creates three virtual accounts. Settlement data flows into one main account, but reports clearly show revenue and margins for each platform separately. This clarity helps with invoices for businesses and financial planning.

4. Escrow accounts

High-value transactions or projects with milestone payments benefit from escrow-style virtual accounts. Funds are received and held in separate tracking buckets until conditions are met.

A manufacturing exporter might use this for large orders with payment terms like 30% advance, 40% on production completion, and 30% on delivery. Each milestone has its own virtual account for clear tracking.

5. Disbursement accounts

These handle outgoing payments to contractors, vendors, or partners. While less common for receivables, they help businesses track who received payouts and when.

An IT services company paying multiple freelancers across countries can use disbursement virtual accounts to maintain clear records of all contractor payments for tax and audit purposes.

What is the difference between virtual accounts and traditional bank accounts?

Virtual accounts and traditional bank accounts serve different purposes in your payment infrastructure. Here's what sets them apart.

Traditional accounts give you a place to store and manage money with full banking features like checkbooks, cards, and branch access. Virtual accounts focus purely on payment identification and routing.

You need a traditional account as your settlement destination. Virtual accounts sit on top of it to make payment collection cleaner and more efficient. Think of traditional accounts as your vault and virtual accounts as labeled drawers that help you organize what goes into them.

For businesses handling multiple payment sources, the combination works best. Your main account holds all funds, while virtual accounts track where each payment came from.

How do you choose the right virtual account solution?

Selecting a virtual account provider depends on your payment volume, currencies needed, and business model. Here's what matters most.

Currency support: Check which currencies the provider supports and whether they offer local account numbers in those currencies. For instance, if you collect payments from US and UK clients, you need USD and GBP virtual accounts that look local to those payers.

Integration options: The solution should connect with your existing accounting software, ERP, or e-commerce platform. API access matters if you want to automate account creation or pull reconciliation data into your systems.

Settlement speed: Find out how quickly funds move from virtual accounts to your main account. Same-day settlement keeps your cash flow healthy, while multi-day delays can create problems for businesses with tight working capital.

Compliance documentation: For export businesses, automatic FIRC (Foreign Inward Remittance Certificate) generation saves significant time. The provider should deliver compliance documents without manual requests.

Pricing structure: Compare transaction fees, setup costs, and monthly charges. Some providers charge per virtual account, while others include unlimited accounts in their platform fees. Calculate total costs based on your expected transaction volume.

Customer support: Payment issues need fast resolution. Check if the provider offers responsive support through your preferred channels and whether they handle queries in your timezone.

Scalability: Your payment volume will grow. Make sure the provider can handle increased transactions without performance issues or requiring you to switch platforms later.

Accept global payments in multiple currencies with PayGlocal

Managing international payments shouldn't require multiple bank accounts, confusing reconciliation, or delayed settlements. You need a solution that tracks every payment clearly while handling multiple currencies without complexity.

PayGlocal gives you the payment infrastructure designed for businesses collecting payments globally and settling locally. Whether you're an exporter, freelancer, or service provider, you get all the tools you need to manage global transactions effectively.

Here's what you get with PayGlocal:

Multi-currency accounts: Collect payments in USD, GBP, EUR, and CAD with local account numbers that look familiar to your international clients. Receive payments from 180+ countries across 33 currencies.

Card payments: Process international credit and debit cards with industry-leading approval rates through smart payment orchestration and enhanced messaging.

Global payment methods: Offer 40+ local payment methods to build trust with international customers and increase sales in markets with low card adoption.

Instant compliance documents: Get FIRC automatically delivered to your inbox after every settlement. No manual requests, no paperwork delays.

Zero fixed costs: Pay only when you transact. No setup fees, no platform charges, no monthly maintenance costs.

PayGlocal helps you collect globally, track automatically, and settle in INR without the complexity of traditional banking infrastructure.

Final thoughts

Virtual accounts have changed how businesses collect payments. Instead of handling multiple bank accounts or spending hours on reconciliation, you get automatic tracking and instant payment identification.

For businesses working across borders, virtual accounts become even more valuable. Collecting in multiple currencies while maintaining clear records requires infrastructure that traditional banking can't provide efficiently. Modern payment platforms make this simple.

If you're ready to collect payments globally without the manual work, PayGlocal gives you virtual accounts across major currencies with automatic compliance documentation. Your international clients pay easily while you settle in INR with complete visibility.

Get started with PayGlocal today and handle international payments with the security and speed your business deserves.