You just landed your first international client. They agreed to your rate, the contract is signed, and the invoice is sent. But when the payment arrives, it's less than expected. That missing chunk isn't a bank error. It's withholding tax.

With India's total exports growing by 4.84% in late 2025, more service providers and exporters are entering the global arena than ever before. However, in the rush to scale, many are caught off guard by the tax treaties and domestic laws of their client's home country. What starts as a profitable deal can quickly turn into a margin-draining headache if you aren't prepared for tax deductions at the source.

In this guide, you'll get a detailed breakdown of what withholding tax is and how it works. Let's get into it.

Withholding tax is income tax that gets deducted directly from a payment before it reaches you. Instead of you paying tax later, the person or company making the payment withholds a portion and sends it straight to the tax authorities on your behalf.

This system works as a prepayment mechanism. It helps governments collect revenue upfront and reduces the chance of tax evasion. For you as the recipient, the withheld amount counts as a credit against your total annual tax liability. If more tax was withheld than you actually owe, you can claim a refund when filing your return.

Withholding tax applies to various income types, including salaries, professional fees, rent, interest, dividends, and payments to non-residents. It's particularly important for businesses dealing with international transactions, where rates and rules can vary significantly.

Managing withholding tax is more than just a filing requirement; it is a critical component of your profit margin and operational health. Failing to account for it can lead to surprises on payments, filing errors, and potential penalties. Here's why it matters:

Mastering these tax levers ensures that the "gross" amount on your invoice actually translates into the highest possible "net" profit in your bank account.

Withholding tax operates as a closed-loop cycle where the responsibility of tax collection is shifted from the earner to the payer. Understanding this flow is essential to ensuring you aren't taxed twice on the same revenue:

For international payments, this process can involve multiple jurisdictions. Your overseas client may withhold tax in their country, and you'll need proper documentation to claim foreign tax credits back home. This is where having clear payment tracking becomes valuable.

Different transactions trigger different withholding obligations. Understanding these categories allows you to anticipate deductions before they impact your liquidity.

Now let's look at each type more closely:

This applies to payments made to individuals or businesses located in the same country as the payer. Rates are generally lower because both parties operate under the same tax system.

For example, if an Indian company pays you for consulting services and you're based in India, they'll withhold tax at applicable resident rates (typically 10% for professional fees). This withheld amount appears on your Form 26AS, and you claim credit against it when filing returns.

When you make payments to foreign individuals or businesses located outside your country, withholding rates are usually higher. If you're an Indian business paying a non-resident consultant, software developer, or service provider, you need to withhold tax before sending the payment.

For instance, if you hire a freelance designer based in the UK and pay them for branding work, you'll need to withhold tax at non-resident rates (often 10% to 40%) before transferring funds. The exact rate depends on the service type and whether a tax treaty exists between India and the UK.

Employers withhold tax from employee salaries based on income slabs. This is the most common form of withholding tax and happens automatically every month. Your employer calculates your projected annual income, applies tax rates, and deducts accordingly.

Certain transactions trigger mandatory withholding regardless of who's involved. Interest from fixed deposits, dividend distributions, rent payments above thresholds, and payments to contractors all fall into this category. Rates and rules vary, but the principle stays the same. Tax gets deducted before you see the money.

Calculating withholding tax starts with identifying the payment type and applicable rate. Once you know the percentage, multiply it by the gross payment amount to get the withheld tax.

For example, if you're paying a consultant 100,000 INR for professional services and the withholding rate is 10%, you deduct 10,000 INR. You transfer 90,000 INR to the consultant and deposit 10,000 INR with the tax authorities.

For non-resident payments, check if a tax treaty applies first. For instance, a payment to a designer based outside India might have a standard 20% rate, but a Double Taxation Avoidance Agreement (DTAA) could reduce it to 10%. Always verify treaty rates and get proper documentation before calculating the final withholding amount.

Withholding tax and TDS (Tax Deducted at Source) are the same concept with different names. In India, TDS is the term used to refer to withholding tax on domestic transactions. Here's how they compare:

Both systems aim to collect tax before income reaches the recipient. The key difference is terminology and documentation. If you're dealing with international clients, you'll hear "withholding tax." If you're working within India, you'll come across "TDS."

For practical purposes, when a foreign client withholds tax from your payment, that's withholding tax. When an Indian company deducts tax before paying you, that's TDS. The tax credit mechanism works the same way. You claim what was withheld against your total tax liability.

One important distinction is that cross-border withholding tax may involve navigating two tax systems. You might face withholding in the payer's country and again when bringing funds into India, unless treaty provisions prevent double taxation.

Getting back excess withheld tax is straightforward if you have proper documentation and file returns accurately. Here's the process:

For international withholding, you may need to file in multiple jurisdictions or use tax treaties to claim foreign tax credits. This can get complex, which is why having clear payment records and compliance documentation makes the process much smoother.

If you're handling international payments, withholding tax is just one piece of a complex puzzle. You need transparency, compliance, and speed without drowning in paperwork or losing money to hidden fees and unclear deductions.

PayGlocal is built for businesses like yours. Whether you're a freelancer receiving payments from global clients, an exporter shipping goods worldwide, or a service provider working across borders, PayGlocal makes international payment collection clear, compliant, and cost-effective.

Here's how PayGlocal helps you manage payments better:

When withholding tax and compliance feel overwhelming, PayGlocal gives you clarity. You get paid faster, track every detail, and file taxes with confidence. No guesswork, no hidden surprises, just payments that work.

Withholding tax is part of doing business, especially when you're working internationally. It's not something to fear. It's a prepayment system that keeps you compliant and gives you credit against your annual tax liability. The key is knowing how it works, tracking what's withheld, and claiming your credits accurately.

Whether you're dealing with domestic TDS or cross-border withholding, having clear records and proper documentation makes everything easier. You can plan cash flow better, avoid surprises, and file returns with confidence when you know exactly what's been deducted and where.

If you're collecting payments from international clients, choosing the right payment platform matters. PayGlocal gives you transparent pricing, instant compliance documentation, and complete visibility into every transaction, so withholding tax becomes one less thing to worry about.

Get started with PayGlocal today and turn international payment complexity into your competitive advantage.

With India's total exports growing by 4.84% in late 2025, more service providers and exporters are entering the global arena than ever before. However, in the rush to scale, many are caught off guard by the tax treaties and domestic laws of their client's home country. What starts as a profitable deal can quickly turn into a margin-draining headache if you aren't prepared for tax deductions at the source.

In this guide, you'll get a detailed breakdown of what withholding tax is and how it works. Let's get into it.

Key Takeaways

- Tax deducted at source: Withholding tax is income tax deducted at the payment source, ensuring governments receive revenue upfront before funds reach the recipient.

- Payer's responsibility: The payer is responsible for deducting and depositing the tax with the authorities, while the recipient receives a certificate to claim credit when filing returns.

- Wide application scope: Withholding tax applies to salaries, professional fees, rent, interest, dividends, and cross-border payments to non-residents.

- Refund eligibility: You can claim refunds if excess tax is withheld by showing certificates and filing accurate returns at year-end.

- PayGlocal simplifies compliance: PayGlocal offers transparent multi-currency payment collection with clear documentation, helping you track withheld amounts and maintain compliance effortlessly.

What is Withholding Tax?

Withholding tax is income tax that gets deducted directly from a payment before it reaches you. Instead of you paying tax later, the person or company making the payment withholds a portion and sends it straight to the tax authorities on your behalf.

This system works as a prepayment mechanism. It helps governments collect revenue upfront and reduces the chance of tax evasion. For you as the recipient, the withheld amount counts as a credit against your total annual tax liability. If more tax was withheld than you actually owe, you can claim a refund when filing your return.

Withholding tax applies to various income types, including salaries, professional fees, rent, interest, dividends, and payments to non-residents. It's particularly important for businesses dealing with international transactions, where rates and rules can vary significantly.

Why Does Withholding Tax Matter for Your Business?

Managing withholding tax is more than just a filing requirement; it is a critical component of your profit margin and operational health. Failing to account for it can lead to surprises on payments, filing errors, and potential penalties. Here's why it matters:

- Cash flow planning: You receive less upfront than invoiced, so you need to account for withheld amounts when projecting revenue and expenses.

- Tax compliance: Proper tracking ensures you claim all credits during filing, preventing overpayment and reducing your final tax liability.

- Client relationships: Knowing withholding rules helps you quote accurate rates and set clear payment expectations with international clients.

- Documentation requirements: You need certificates and records for every withheld amount to claim credits, making organized tracking essential.

- International payment complexity: International payments can face double withholding unless you understand tax treaties and provide proper documentation.

Mastering these tax levers ensures that the "gross" amount on your invoice actually translates into the highest possible "net" profit in your bank account.

How Does Withholding Tax Work?

Withholding tax operates as a closed-loop cycle where the responsibility of tax collection is shifted from the earner to the payer. Understanding this flow is essential to ensuring you aren't taxed twice on the same revenue:

- The payer calculates the tax: When making a payment, the payer checks applicable withholding tax rates based on the payment type and recipient status. This could be your client, employer, or any entity paying you.

- Tax is deducted at source: Before transferring funds to you, the payer withholds the required percentage. For instance, if you're owed 100,000 INR and withholding tax is 10%, the payer deducts 10,000 INR.

- Tax is deposited with the authorities: The payer sends the withheld amount to the tax department within specified timelines. This isn't optional. It's a required step.

- You receive the net amount: The remaining amount reaches your account. You don't get the full invoice value, but you're not losing money. It's already paid toward your tax liability.

- Certificate is issued: The payer provides you with a certificate (like Form 16A in India or Form W-2 in the US) showing how much was withheld. This document is critical for claiming credit later.

- You claim credit when filing returns: When you file your annual tax return, you report the withheld amount as tax already paid. If the total withheld exceeds your actual liability, you get a refund. If it's less, you pay the difference.

For international payments, this process can involve multiple jurisdictions. Your overseas client may withhold tax in their country, and you'll need proper documentation to claim foreign tax credits back home. This is where having clear payment tracking becomes valuable.

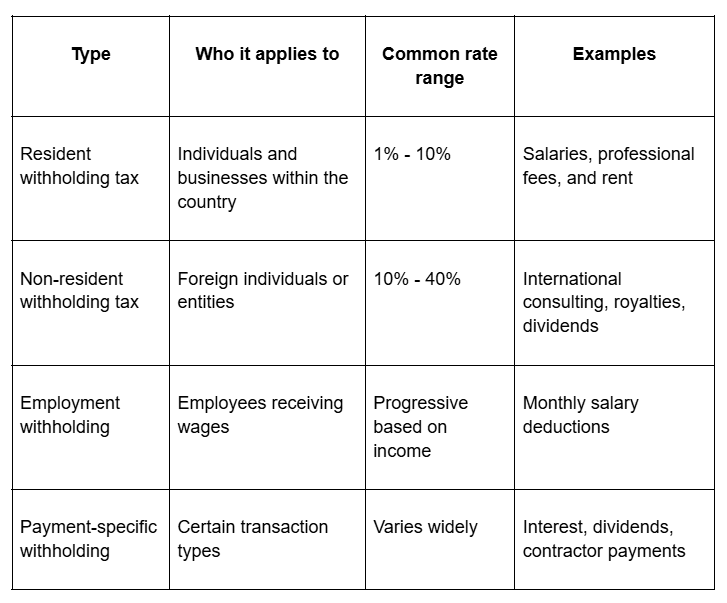

What are the Types of Withholding Tax?

Different transactions trigger different withholding obligations. Understanding these categories allows you to anticipate deductions before they impact your liquidity.

Now let's look at each type more closely:

Resident Withholding Tax

This applies to payments made to individuals or businesses located in the same country as the payer. Rates are generally lower because both parties operate under the same tax system.

For example, if an Indian company pays you for consulting services and you're based in India, they'll withhold tax at applicable resident rates (typically 10% for professional fees). This withheld amount appears on your Form 26AS, and you claim credit against it when filing returns.

Non-Resident Withholding Tax

When you make payments to foreign individuals or businesses located outside your country, withholding rates are usually higher. If you're an Indian business paying a non-resident consultant, software developer, or service provider, you need to withhold tax before sending the payment.

For instance, if you hire a freelance designer based in the UK and pay them for branding work, you'll need to withhold tax at non-resident rates (often 10% to 40%) before transferring funds. The exact rate depends on the service type and whether a tax treaty exists between India and the UK.

Withholding on Employment Income

Employers withhold tax from employee salaries based on income slabs. This is the most common form of withholding tax and happens automatically every month. Your employer calculates your projected annual income, applies tax rates, and deducts accordingly.

Withholding on Specific Payment Types

Certain transactions trigger mandatory withholding regardless of who's involved. Interest from fixed deposits, dividend distributions, rent payments above thresholds, and payments to contractors all fall into this category. Rates and rules vary, but the principle stays the same. Tax gets deducted before you see the money.

How to Calculate Withholding Tax Liability?

Calculating withholding tax starts with identifying the payment type and applicable rate. Once you know the percentage, multiply it by the gross payment amount to get the withheld tax.

For example, if you're paying a consultant 100,000 INR for professional services and the withholding rate is 10%, you deduct 10,000 INR. You transfer 90,000 INR to the consultant and deposit 10,000 INR with the tax authorities.

For non-resident payments, check if a tax treaty applies first. For instance, a payment to a designer based outside India might have a standard 20% rate, but a Double Taxation Avoidance Agreement (DTAA) could reduce it to 10%. Always verify treaty rates and get proper documentation before calculating the final withholding amount.

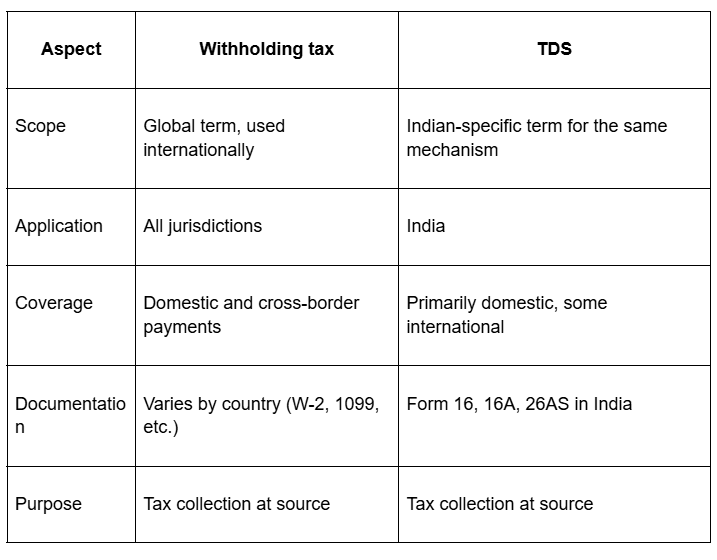

What is the Difference Between Withholding Tax and TDS?

Withholding tax and TDS (Tax Deducted at Source) are the same concept with different names. In India, TDS is the term used to refer to withholding tax on domestic transactions. Here's how they compare:

Both systems aim to collect tax before income reaches the recipient. The key difference is terminology and documentation. If you're dealing with international clients, you'll hear "withholding tax." If you're working within India, you'll come across "TDS."

For practical purposes, when a foreign client withholds tax from your payment, that's withholding tax. When an Indian company deducts tax before paying you, that's TDS. The tax credit mechanism works the same way. You claim what was withheld against your total tax liability.

One important distinction is that cross-border withholding tax may involve navigating two tax systems. You might face withholding in the payer's country and again when bringing funds into India, unless treaty provisions prevent double taxation.

How do You Claim Refunds on Withholding Tax?

Getting back excess withheld tax is straightforward if you have proper documentation and file returns accurately. Here's the process:

- Collect withholding certificates: Every entity that withholds tax from your payments should provide a certificate. In India, this is Form 16 (for salary) or Form 16A (for other payments). For international payments, you'll receive equivalent documents from foreign payers.

- Verify your Form 26AS: This consolidated statement shows all tax deducted on your behalf. Log in to the income tax portal and check that withheld amounts match your records. Discrepancies should be resolved before filing returns.

- Report withheld amounts when filing: When you file your Income Tax Return (ITR), include all withheld tax in the appropriate sections. The form automatically calculates if you've paid more tax than you owe.

- Claim the refund: If withholdings exceed your actual tax liability, the ITR will show a refund due. Submit your return, and the tax department will process the refund, typically within a few months.

- Track refund status: You can monitor refund processing through the income tax portal. Refunds are usually credited directly to your registered bank account.

For international withholding, you may need to file in multiple jurisdictions or use tax treaties to claim foreign tax credits. This can get complex, which is why having clear payment records and compliance documentation makes the process much smoother.

Simplify International Payment Management with PayGlocal

If you're handling international payments, withholding tax is just one piece of a complex puzzle. You need transparency, compliance, and speed without drowning in paperwork or losing money to hidden fees and unclear deductions.

PayGlocal is built for businesses like yours. Whether you're a freelancer receiving payments from global clients, an exporter shipping goods worldwide, or a service provider working across borders, PayGlocal makes international payment collection clear, compliant, and cost-effective.

Here's how PayGlocal helps you manage payments better:

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD, and globally in 33 currencies from 180+ countries. No need for multiple bank accounts or complex setups.

- Instant compliance documentation: Receive the Foreign Inward Remittance Certificate (FIRC) directly in your inbox after settlement. No chasing banks or waiting weeks for documents you need for tax filing.

- Transparent payment tracking: Get real-time notifications on fund status at every step. Know exactly when payments arrive, what's deducted, and where your money is.

- Zero fixed costs: Pay only when you transact. No setup fees, no platform charges, no monthly subscriptions. Just clear, predictable pricing.

- One unified platform: Manage all your international payments from a single dashboard. View transactions, download reports, and track compliance all in one place.

When withholding tax and compliance feel overwhelming, PayGlocal gives you clarity. You get paid faster, track every detail, and file taxes with confidence. No guesswork, no hidden surprises, just payments that work.

Final Thoughts

Withholding tax is part of doing business, especially when you're working internationally. It's not something to fear. It's a prepayment system that keeps you compliant and gives you credit against your annual tax liability. The key is knowing how it works, tracking what's withheld, and claiming your credits accurately.

Whether you're dealing with domestic TDS or cross-border withholding, having clear records and proper documentation makes everything easier. You can plan cash flow better, avoid surprises, and file returns with confidence when you know exactly what's been deducted and where.

If you're collecting payments from international clients, choosing the right payment platform matters. PayGlocal gives you transparent pricing, instant compliance documentation, and complete visibility into every transaction, so withholding tax becomes one less thing to worry about.

Get started with PayGlocal today and turn international payment complexity into your competitive advantage.