The way businesses move money has changed completely in the last few years, with most transactions happening electronically. In fact, data shows that over 65,000 crore digital transactions have been completed in India over the past 6 years, with values exceeding Rs. 12,000 lakh crore.

Electronic Fund Transfer (EFT) offers a fast, secure, and cost-effective payment solution. It reduces friction from the payment process for businesses collecting payments from international clients or managing team payroll.

In this guide, we break down what EFT is, how it works, and the actual advantages it brings to your business. So, let’s get into it.

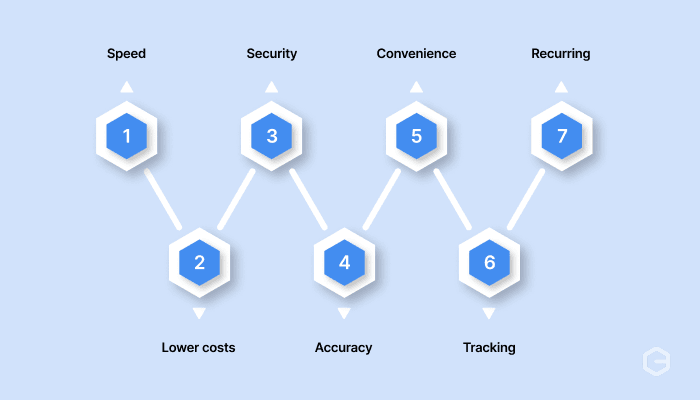

Fast processing: EFT transactions typically complete within hours or a few business days, much faster than traditional payment methods.

Lower costs: You avoid many fees associated with paper checks, wire transfers, or manual processing.

Better security: Electronic verification and encryption reduce the risk of theft, fraud, and lost payments.

Easy payment tracking: You can monitor transaction status in real time and maintain clear digital records.

Global reach: Collect payments from international clients and settle in your local currency with platforms like PayGlocal that handle multi-currency EFT transactions.

EFT stands for Electronic Fund Transfer. It's the digital movement of money from one bank account to another without using paper checks or cash.

When you transfer money through online banking, pay bills through an app, or receive your salary through direct deposit, you're using EFT. The system handles everything electronically through secure banking networks.

Common EFT methods include direct deposits, wire transfers, ATM transactions, card payments, and online payment systems. For example, when a client in the United States pays your invoice through a bank transfer and the money reaches your Indian business account, that's an EFT transaction.

The key difference from traditional methods is speed and automation. Instead of writing checks, mailing them, and waiting for bank clearance, EFT processes payments electronically. This makes it ideal for businesses that need to move money quickly and reliably across borders.

EFT offers several benefits that directly impact your business operations and profit potential. Here's a quick comparison of key EFT advantages:

Let’s take a detailed look at each of the main advantages:

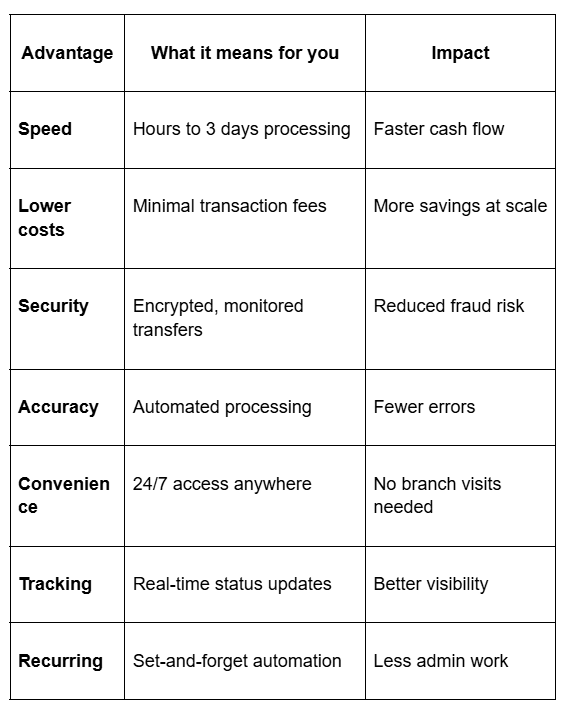

EFT transactions process much faster than traditional payment methods. Domestic transfers often complete within a few hours, while international payments typically take 1-3 business days instead of weeks.

You don't wait for checks to arrive in the mail or clear through multiple banking stages. The electronic process cuts out intermediary steps, getting your money where it needs to go quickly. For instance, if a European client sends payment on Monday, you can often access those funds by Wednesday or Thursday.

This speed helps your cash flow. You can pay suppliers faster, meet payroll deadlines easily, and reinvest in your business sooner.

EFT reduces the expenses tied to payment processing. You skip costs for paper checks, postage, manual processing, and bank fees for depositing physical payments.

Many banks charge lower fees for electronic transfers compared to wire transfers or international checks. Some domestic EFT transactions come with minimal or no fees at all. For example, direct deposits for payroll costs cost businesses far less than printing and distributing paper checks.

When you process payments at scale, these savings add up significantly. A company processing hundreds of vendor payments monthly can save significant amounts in operational costs by switching to EFT.

Electronic systems protect your money better than physical payment methods. EFT uses encryption, secure banking networks, and multi-factor authentication to verify transactions.

You avoid risks like lost or stolen checks, forged signatures, or intercepted mail. Banks monitor EFT transactions for suspicious activity and can flag unusual patterns automatically.

Each transaction creates a digital record that's harder to alter or dispute compared to paper trails. For instance, when you receive payment through EFT, you get instant confirmation with transaction details that serve as proof of payment.

Automated electronic processing reduces human errors that happen with manual data entry. When payment details flow directly from your system to the bank's network, there's less chance of typos, wrong account numbers, or miscalculated amounts.

You avoid mistakes like misreading handwritten checks or entering payment information incorrectly into accounting systems. For example, setting up recurring EFT payments for rent or subscriptions ensures the correct amount goes to the right account every time without manual intervention.

This accuracy extends to your financial records. EFT transactions integrate smoothly with accounting software, keeping your books current and reducing reconciliation challenges.

You can initiate EFT payments anytime from anywhere with internet access. No need to visit bank branches during business hours or wait in line to deposit checks.

This flexibility matters when you're managing a business with clients in different time zones. You can process payments late at night or early morning, whatever fits your schedule. For instance, if a client sends payment confirmation at night, you can verify and track the transaction immediately through your banking portal.

The convenience extends to your customers and vendors, too. They can pay invoices or receive payments without geographical constraints, making business relationships smoother across borders.

EFT systems automatically maintain detailed digital records of every transaction. You can access payment history, track transaction status, and download statements whenever needed.

This transparency helps you answer questions quickly. When did that payment arrive? Has the vendor payment cleared? EFT records provide instant answers without digging through paper files.

For compliance and tax purposes, having organized digital records saves time during audits. You can search transactions by date, amount, or recipient and generate reports with a few clicks.

EFT makes automated recurring payments simple. Set up once, and the system handles regular payments for subscriptions, salaries, vendor contracts, or loan repayments automatically.

This automation reduces administrative work and prevents late payments. Your employees receive salaries on time every month without manual processing. Your software subscriptions renew without interruption.

For example, if you pay the same vendors monthly, EFT recurring payments ensure they get paid on schedule while you focus on running your business instead of processing individual transactions.

EFT operates through a straightforward electronic process that moves money between bank accounts securely. Here's what happens during an EFT transaction:

The entire process happens electronically without physical paperwork. Processing times vary based on the type of EFT, the countries involved, and the banking networks used. Some transfers complete in minutes, while others take a few business days, depending on cut-off times and banking schedules.

Here are some of the common types of EFT payment methods:

Let’s see in a bit more detail EFT payment method offers:

Each type offers different processing speeds, cost structures, and use cases. Choosing the right EFT method depends on your payment urgency, transaction size, and whether you're sending money domestically or internationally.

Knowing how EFT compares to traditional payment methods helps you make better decisions for your business. Here's how they compare:

Traditional methods still work for certain situations, like small local transactions or customers who prefer physical payments. But for businesses processing multiple payments, working with international clients, or needing reliable payment tracking, EFT provides clear advantages.

The efficiency difference widens when you handle payments at scale. Processing 100 checks involves printing, signing, mailing, and tracking each one. Processing 100 EFT payments takes a few clicks and happens automatically.

Not all EFT systems work the same way. Picking the right platform for your business requires looking at several factors.

Compliance and documentation: For businesses handling international payments, automatic generation of compliance documents like FIRC (Foreign Inward Remittance Certificate) saves significant time and effort.

The right EFT solution should make payments simpler, not create new complications. Take time to evaluate options based on your specific business needs and transaction patterns.

International payments don't have to be complicated. If you're collecting from global clients, dealing with multiple currencies, or spending too much on transaction fees, you need a payment platform specifically built for global business.

PayGlocal helps businesses accept international payments and settle in INR with complete transparency and control. Here's how PayGlocal works for your business:

PayGlocal combines the advantages of EFT with specialized features for businesses working across countries. You get the speed and security of electronic payments plus the tools you need for easily handling international transactions.

EFT offers clear advantages over traditional payment methods. Speed, security, cost savings, and convenience make electronic fund transfers the standard for modern business payments.

When you're working with international clients, these advantages matter even more. You need reliable payment collection, transparent pricing, and systems that handle multiple currencies.

Ready to accept global payments fast, secure, and efficiently, in multiple currencies? Get started with PayGlocal today and experience payment collection that actually works for international business.

Electronic Fund Transfer (EFT) offers a fast, secure, and cost-effective payment solution. It reduces friction from the payment process for businesses collecting payments from international clients or managing team payroll.

In this guide, we break down what EFT is, how it works, and the actual advantages it brings to your business. So, let’s get into it.

Key takeaways

Fast processing: EFT transactions typically complete within hours or a few business days, much faster than traditional payment methods.

Lower costs: You avoid many fees associated with paper checks, wire transfers, or manual processing.

Better security: Electronic verification and encryption reduce the risk of theft, fraud, and lost payments.

Easy payment tracking: You can monitor transaction status in real time and maintain clear digital records.

Global reach: Collect payments from international clients and settle in your local currency with platforms like PayGlocal that handle multi-currency EFT transactions.

What is EFT?

EFT stands for Electronic Fund Transfer. It's the digital movement of money from one bank account to another without using paper checks or cash.

When you transfer money through online banking, pay bills through an app, or receive your salary through direct deposit, you're using EFT. The system handles everything electronically through secure banking networks.

Common EFT methods include direct deposits, wire transfers, ATM transactions, card payments, and online payment systems. For example, when a client in the United States pays your invoice through a bank transfer and the money reaches your Indian business account, that's an EFT transaction.

The key difference from traditional methods is speed and automation. Instead of writing checks, mailing them, and waiting for bank clearance, EFT processes payments electronically. This makes it ideal for businesses that need to move money quickly and reliably across borders.

What are the advantages of EFT?

EFT offers several benefits that directly impact your business operations and profit potential. Here's a quick comparison of key EFT advantages:

Let’s take a detailed look at each of the main advantages:

Speed and efficiency

EFT transactions process much faster than traditional payment methods. Domestic transfers often complete within a few hours, while international payments typically take 1-3 business days instead of weeks.

You don't wait for checks to arrive in the mail or clear through multiple banking stages. The electronic process cuts out intermediary steps, getting your money where it needs to go quickly. For instance, if a European client sends payment on Monday, you can often access those funds by Wednesday or Thursday.

This speed helps your cash flow. You can pay suppliers faster, meet payroll deadlines easily, and reinvest in your business sooner.

Lower transaction costs

EFT reduces the expenses tied to payment processing. You skip costs for paper checks, postage, manual processing, and bank fees for depositing physical payments.

Many banks charge lower fees for electronic transfers compared to wire transfers or international checks. Some domestic EFT transactions come with minimal or no fees at all. For example, direct deposits for payroll costs cost businesses far less than printing and distributing paper checks.

When you process payments at scale, these savings add up significantly. A company processing hundreds of vendor payments monthly can save significant amounts in operational costs by switching to EFT.

Better security and fraud prevention

Electronic systems protect your money better than physical payment methods. EFT uses encryption, secure banking networks, and multi-factor authentication to verify transactions.

You avoid risks like lost or stolen checks, forged signatures, or intercepted mail. Banks monitor EFT transactions for suspicious activity and can flag unusual patterns automatically.

Each transaction creates a digital record that's harder to alter or dispute compared to paper trails. For instance, when you receive payment through EFT, you get instant confirmation with transaction details that serve as proof of payment.

Improved accuracy

Automated electronic processing reduces human errors that happen with manual data entry. When payment details flow directly from your system to the bank's network, there's less chance of typos, wrong account numbers, or miscalculated amounts.

You avoid mistakes like misreading handwritten checks or entering payment information incorrectly into accounting systems. For example, setting up recurring EFT payments for rent or subscriptions ensures the correct amount goes to the right account every time without manual intervention.

This accuracy extends to your financial records. EFT transactions integrate smoothly with accounting software, keeping your books current and reducing reconciliation challenges.

Convenient and accessible

You can initiate EFT payments anytime from anywhere with internet access. No need to visit bank branches during business hours or wait in line to deposit checks.

This flexibility matters when you're managing a business with clients in different time zones. You can process payments late at night or early morning, whatever fits your schedule. For instance, if a client sends payment confirmation at night, you can verify and track the transaction immediately through your banking portal.

The convenience extends to your customers and vendors, too. They can pay invoices or receive payments without geographical constraints, making business relationships smoother across borders.

Easier payment tracking and record keeping

EFT systems automatically maintain detailed digital records of every transaction. You can access payment history, track transaction status, and download statements whenever needed.

This transparency helps you answer questions quickly. When did that payment arrive? Has the vendor payment cleared? EFT records provide instant answers without digging through paper files.

For compliance and tax purposes, having organized digital records saves time during audits. You can search transactions by date, amount, or recipient and generate reports with a few clicks.

Support for recurring payments

EFT makes automated recurring payments simple. Set up once, and the system handles regular payments for subscriptions, salaries, vendor contracts, or loan repayments automatically.

This automation reduces administrative work and prevents late payments. Your employees receive salaries on time every month without manual processing. Your software subscriptions renew without interruption.

For example, if you pay the same vendors monthly, EFT recurring payments ensure they get paid on schedule while you focus on running your business instead of processing individual transactions.

How does EFT work?

EFT operates through a straightforward electronic process that moves money between bank accounts securely. Here's what happens during an EFT transaction:

- You initiate the payment: This happens through online banking, a payment app, or an automated system. You provide the recipient's bank account details and the amount to transfer.

- Your bank verifies the transaction: The system checks transaction details and confirms you have sufficient funds. It encrypts your payment information for security.

- Transaction routes through a payment network: This could be ACH (Automated Clearing House) for domestic transfers in the US, NEFT or RTGS in India, or SWIFT for international payments. These networks act as secure intermediaries between banks.

- Recipient's bank receives and processes: The recipient's bank receives the transaction data and credits the funds to the recipient's account. Both parties get confirmation once the transfer completes.

The entire process happens electronically without physical paperwork. Processing times vary based on the type of EFT, the countries involved, and the banking networks used. Some transfers complete in minutes, while others take a few business days, depending on cut-off times and banking schedules.

What are the different types of EFT payments?

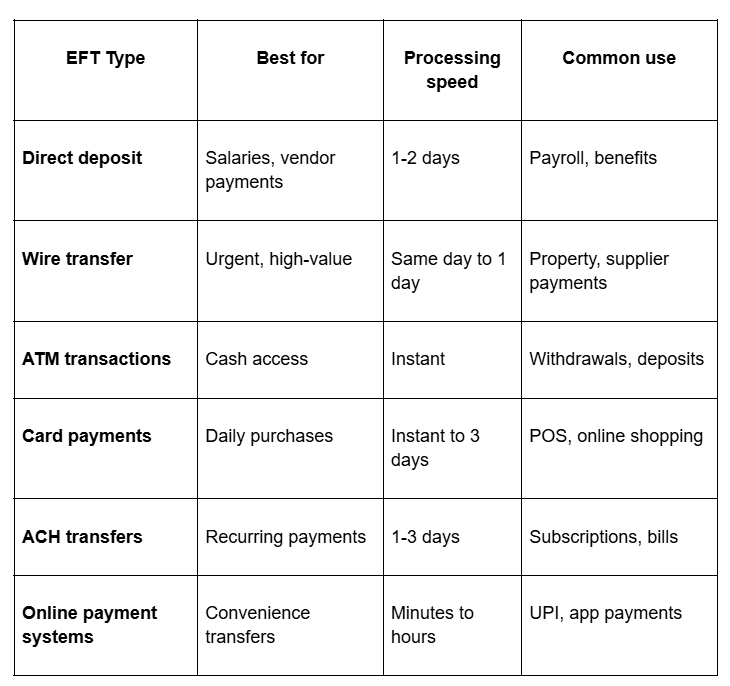

Here are some of the common types of EFT payment methods:

Let’s see in a bit more detail EFT payment method offers:

- Direct deposit: Money transfers directly from one account to another, commonly used for salaries, vendor payments, and government benefits. Your employer deposits your salary into your bank account automatically each month.

- Wire transfer: Fast electronic transfers that move larger amounts quickly, often used for urgent or high-value payments. For example, transferring funds for a property purchase or paying international suppliers with same-day requirements.

- ATM transactions: Electronic cash withdrawals and deposits through automated teller machines. When you use your debit card to withdraw cash or check your balance, you're using EFT technology.

- Card payments: Debit and credit card transactions at point-of-sale terminals or online. Swiping your card to pay for office supplies processes as an EFT transaction.

- ACH transfers: Batch-processed electronic payments are common in the US for direct deposits, bill payments, and B2B transactions. Many SaaS companies collect recurring subscription payments through ACH.

- Online payment systems: Digital platforms like UPI or bank-to-bank transfers initiated through mobile apps or websites. When you pay a client through your banking app, that's an online EFT payment.

Each type offers different processing speeds, cost structures, and use cases. Choosing the right EFT method depends on your payment urgency, transaction size, and whether you're sending money domestically or internationally.

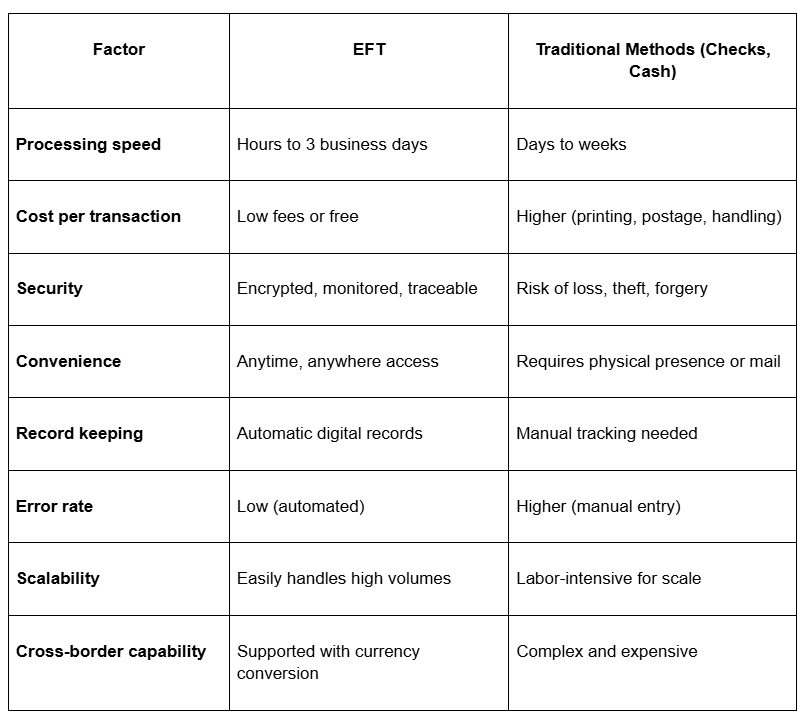

How do EFT and traditional payment methods compare?

Knowing how EFT compares to traditional payment methods helps you make better decisions for your business. Here's how they compare:

Traditional methods still work for certain situations, like small local transactions or customers who prefer physical payments. But for businesses processing multiple payments, working with international clients, or needing reliable payment tracking, EFT provides clear advantages.

The efficiency difference widens when you handle payments at scale. Processing 100 checks involves printing, signing, mailing, and tracking each one. Processing 100 EFT payments takes a few clicks and happens automatically.

What to consider when choosing EFT solutions?

Not all EFT systems work the same way. Picking the right platform for your business requires looking at several factors.

- Currency support: If you work with international clients, you need a system that handles multiple currencies smoothly. Check whether the platform offers competitive exchange rates and settles funds in your preferred currency.

- Processing speed: Different EFT networks have different timelines. Consider how quickly you need funds to arrive and whether same-day or next-day processing matters for your operations.

- Fee structure: Compare transaction fees, monthly charges, currency conversion costs, and any hidden charges. Some platforms charge per transaction while others offer volume-based pricing.

- Security features: Look for encryption standards, fraud monitoring, two-factor authentication, and compliance with banking regulations. Your payment platform should prioritize protecting your financial data.

- Integration capabilities: Check if the EFT solution connects with your accounting software, invoicing tools, or business management systems. Seamless integration saves time and reduces manual data entry.

- Payment tracking and reporting: You need visibility into transaction status, payment history, and detailed reporting for accounting and compliance. Good platforms provide real-time updates and downloadable reports.

- Customer support: When payment issues arise, you need quick help. Evaluate the provider's support availability, response times, and whether they offer assistance in your time zone.

Compliance and documentation: For businesses handling international payments, automatic generation of compliance documents like FIRC (Foreign Inward Remittance Certificate) saves significant time and effort.

The right EFT solution should make payments simpler, not create new complications. Take time to evaluate options based on your specific business needs and transaction patterns.

Move beyond payment complexity with PayGlocal

International payments don't have to be complicated. If you're collecting from global clients, dealing with multiple currencies, or spending too much on transaction fees, you need a payment platform specifically built for global business.

PayGlocal helps businesses accept international payments and settle in INR with complete transparency and control. Here's how PayGlocal works for your business:

- Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD. Your international clients can pay you like a local business.

- Global payment methods: Support 40+ local payment methods that customers in different regions prefer, increasing trust and conversion rates.

- Real-time tracking: Monitor payment status at every step with instant notifications and transparent dashboards showing exactly where your funds are.

- Recurring payments: Set up automated collection for subscriptions, retainers, or regular services with network-compliant recurring payment processing.

- Zero fixed costs: Pay only when you transact. No setup fees, no platform charges, no documentation fees.

PayGlocal combines the advantages of EFT with specialized features for businesses working across countries. You get the speed and security of electronic payments plus the tools you need for easily handling international transactions.

Final thoughts

EFT offers clear advantages over traditional payment methods. Speed, security, cost savings, and convenience make electronic fund transfers the standard for modern business payments.

When you're working with international clients, these advantages matter even more. You need reliable payment collection, transparent pricing, and systems that handle multiple currencies.

Ready to accept global payments fast, secure, and efficiently, in multiple currencies? Get started with PayGlocal today and experience payment collection that actually works for international business.