Most shoppers abandon their carts when they don't find their preferred payment method at checkout. Studies show that 10% of shoppers abandon their cart because of limited payment options.

Offering more payment options in your online store can significantly improve the checkout experience. The right e-commerce payment system builds trust, reduces friction, and increases the likelihood of your customers completing their purchases.

In this guide, we cover everything you need to know about e-commerce payment systems. Find out different types, their benefits, and how to choose the right one for your business.

An e-commerce payment system is the technology that processes online payments between customers and businesses. It handles the digital exchange of money when someone buys from your online store.

These systems securely capture payment information, verify funds availability, transfer money from the customer's account to yours, and provide confirmation to both parties.

For example, when someone buys from your online store using a credit card, the payment system communicates with the customer's bank, your bank, and card networks to complete the transaction in seconds.

Most e-commerce transactions follow the same basic steps regardless of the payment method used. Here's how a typical payment flows from start to finish:

Different payment methods suit different customer needs and shopping behaviors. Here's how the main options compare:

Let's take a detailed look at how each one of these e-commerce payment systems works:

Credit and debit cards remain the most widely accepted payment method globally. They offer immediate payment processing and are familiar to most customers. Major networks like Visa, Mastercard, American Express, and Discover provide coverage across most countries.

Key features include:

Cost: 2.9-3.5% per transaction plus fixed fees.

Best For: All business types and transaction sizes, especially international sales.

Digital wallets store payment information securely and enable faster checkout experiences. Popular options include PayPal, Google Pay, Apple Pay, and Amazon Pay. These services reduce checkout friction and add security layers.

Key features include:

Cost: 2.9-3.5% per transaction, similar to card processing.

Best For: Mobile commerce and repeat customers who value convenience.

Electronic Fund Transfer allows customers to pay directly from their bank accounts through various electronic banking methods. This includes wire transfers, ACH payments, and net banking, where customers log into their bank portals to authorize payments.

Key features include:

Cost: 0.5-1% per transaction or flat fees.

Best For: High-value transactions and B2B payments where speed isn't critical.

BNPL services allow customers to purchase items immediately and pay for them over time through scheduled payments. This payment method has grown rapidly, especially among younger consumers making larger purchases.

Key features include:

Cost: 3-6% per transaction, higher than traditional cards.

Best For: Fashion, electronics, and other higher-priced consumer goods.

Mobile payment methods use smartphones for transactions through apps, QR codes, and NFC technology. This includes UPI payments in India, mobile wallets, and contactless payment systems that are popular in markets with high smartphone adoption.

Key features include:

Cost: 1-3% per transaction, depending on the method.

Best For: Mobile-first businesses and markets with strong smartphone adoption.

Cash on Delivery allows customers to pay when they receive their products. This traditional method remains popular in markets where online payment trust is still developing.

Key features include:

Cost: Fixed fee per order plus logistics costs.

Best For: Emerging markets and customers hesitant about online payments.

Prepaid cards work like debit cards but are loaded with a specific amount of money in advance. They're popular among customers who want to control spending or don't have traditional bank accounts.

Key features include:

Cost: 2-4% per transaction plus card activation fees.

Best For: Budget-conscious customers and gift purchases.

The right payment system impacts every aspect of your online business, from customer experience to financial operations.

Selecting the right payment system requires balancing customer needs, business requirements, and cost considerations. Here are the main factors to evaluate:

* Integration complexity assessment: Consider how easily the system integrates with your existing e-commerce platform, accounting software, and other business tools you rely on.

E-commerce businesses using traditional payment systems often struggle with high fees, low success rates, and compliance challenges.

PayGlocal simplifies global payment acceptance by offering faster payment processing options with affordable and transparent pricing. Here's how PayGlocal solves common payment challenges:

Whether you're a growing SaaS company, an established exporter, or an enterprise expanding globally, PayGlocal provides the payment infrastructure you need to succeed internationally.

E-commerce payment systems form the foundation of successful online businesses. The right system enables customer trust, enables global expansion, and automates financial operations that scale with your growth.

Modern businesses need payment solutions that work globally, across different currencies and customer preferences. PayGlocal provides exactly this kind of payment solution, helping companies accept international payments without the usual complexity.

The global e-commerce market continues to expand, and businesses that can accept payments from anywhere have a significant competitive advantage. Get started with PayGlocal today and turn international payment challenges into growth opportunities that drive your business forward.

Offering more payment options in your online store can significantly improve the checkout experience. The right e-commerce payment system builds trust, reduces friction, and increases the likelihood of your customers completing their purchases.

In this guide, we cover everything you need to know about e-commerce payment systems. Find out different types, their benefits, and how to choose the right one for your business.

Key Takeaways:

- Payment method variety: E-commerce payment systems enable online businesses to accept a wide range of payment methods, including cards, digital wallets, and bank transfers.

- Customer preference matching: Different payment types serve different customer preferences, from credit cards for quick purchases to Buy Now Pay Later for larger transactions.

- Cart abandonment reduction: The right payment system reduces cart abandonment and increases customer trust through familiar payment options.

- Global payment capability: Modern solutions like PayGlocal offer multi-currency acceptance, global payment methods, and instant compliance documentation.

What is an e-commerce payment system?

An e-commerce payment system is the technology that processes online payments between customers and businesses. It handles the digital exchange of money when someone buys from your online store.

These systems securely capture payment information, verify funds availability, transfer money from the customer's account to yours, and provide confirmation to both parties.

For example, when someone buys from your online store using a credit card, the payment system communicates with the customer's bank, your bank, and card networks to complete the transaction in seconds.

How do e-commerce payment systems work?

Most e-commerce transactions follow the same basic steps regardless of the payment method used. Here's how a typical payment flows from start to finish:

- Customer initiates payment: The customer selects items, proceeds to checkout, and enters their payment information on your website or app.

- Payment data encryption: The system encrypts sensitive information like card numbers and sends it securely to the payment processor for verification.

- Authorization request: The payment processor contacts the customer's bank or card issuer to check if funds are available and the transaction is legitimate.

- Approval or decline decision: The bank approves or declines the transaction based on available funds, account status, and fraud detection algorithms.

- Transaction completion: If approved, money moves from the customer's account to your merchant account, and both parties receive confirmation.

- Settlement and reporting: Funds typically appear in your business bank account within 1-3 business days, along with transaction reports and fees deducted.

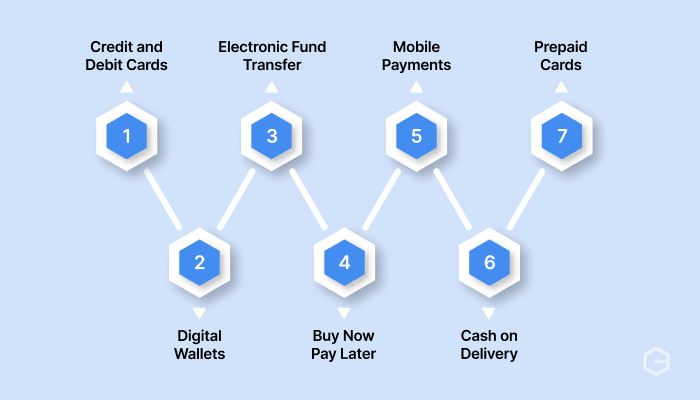

What are the types of e-commerce payment systems?

Different payment methods suit different customer needs and shopping behaviors. Here's how the main options compare:

Let's take a detailed look at how each one of these e-commerce payment systems works:

Credit and debit cards

Credit and debit cards remain the most widely accepted payment method globally. They offer immediate payment processing and are familiar to most customers. Major networks like Visa, Mastercard, American Express, and Discover provide coverage across most countries.

Key features include:

- Instant processing: Transactions complete within seconds of authorization.

- Universal acceptance: Accepted by virtually all online merchants worldwide.

- Recurring payment support: Perfect for subscriptions and repeat billing.

- Chargeback protection: Customers can dispute fraudulent or incorrect charges.

Cost: 2.9-3.5% per transaction plus fixed fees.

Best For: All business types and transaction sizes, especially international sales.

Digital wallets

Digital wallets store payment information securely and enable faster checkout experiences. Popular options include PayPal, Google Pay, Apple Pay, and Amazon Pay. These services reduce checkout friction and add security layers.

Key features include:

- One-click checkout: Customers don't need to enter card details repeatedly.

- Enhanced security: Tokenization protects actual card numbers during transactions.

- Biometric authentication: Touch ID or Face ID adds extra security layers.

- Multi-device access: Works across phones, tablets, and computers.

Cost: 2.9-3.5% per transaction, similar to card processing.

Best For: Mobile commerce and repeat customers who value convenience.

Electronic Fund Transfer

Electronic Fund Transfer allows customers to pay directly from their bank accounts through various electronic banking methods. This includes wire transfers, ACH payments, and net banking, where customers log into their bank portals to authorize payments.

Key features include:

- Lower processing fees: They typically cost less than card payments.

- High transaction limits: Can handle very large payment amounts.

- Bank-grade security: Uses existing banking authentication systems.

- No chargebacks: Payments are final once processed.

Cost: 0.5-1% per transaction or flat fees.

Best For: High-value transactions and B2B payments where speed isn't critical.

Buy Now Pay Later (BNPL)

BNPL services allow customers to purchase items immediately and pay for them over time through scheduled payments. This payment method has grown rapidly, especially among younger consumers making larger purchases.

Key features include:

- Flexible payment plans: Split purchases into 2-4 installments.

- Instant approval: Quick credit decisions during checkout.

- No interest options: Many plans charge no interest if paid on time.

- Increased purchasing power: Customers can buy more expensive items.

Cost: 3-6% per transaction, higher than traditional cards.

Best For: Fashion, electronics, and other higher-priced consumer goods.

Mobile payments

Mobile payment methods use smartphones for transactions through apps, QR codes, and NFC technology. This includes UPI payments in India, mobile wallets, and contactless payment systems that are popular in markets with high smartphone adoption.

Key features include:

- UPI integration: Real-time payments through apps like Google Pay and PhonePe.

- NFC technology: Tap-to-pay functionality for contactless transactions.

- App-based processing: Integrated with popular mobile applications.

- Instant confirmation: Real-time payment notifications and confirmations.

Cost: 1-3% per transaction, depending on the method.

Best For: Mobile-first businesses and markets with strong smartphone adoption.

Cash on Delivery (COD)

Cash on Delivery allows customers to pay when they receive their products. This traditional method remains popular in markets where online payment trust is still developing.

Key features include:

- Payment upon delivery: No upfront payment required from customers.

- High customer trust: Familiar and comfortable for traditional shoppers.

- No payment processing: No digital transaction fees during checkout.

- Market penetration: Reaches customers without bank accounts or cards.

Cost: Fixed fee per order plus logistics costs.

Best For: Emerging markets and customers hesitant about online payments.

Prepaid cards

Prepaid cards work like debit cards but are loaded with a specific amount of money in advance. They're popular among customers who want to control spending or don't have traditional bank accounts.

Key features include:

- Spending control: Limited to a preloaded amount prevents overspending.

- No credit check: Available to customers with poor credit history.

- Gift card functionality: Often used for gifts and promotions.

- Wide availability: Sold at retail stores and online.

Cost: 2-4% per transaction plus card activation fees.

Best For: Budget-conscious customers and gift purchases.

What are the benefits of e-commerce payment systems?

The right payment system impacts every aspect of your online business, from customer experience to financial operations.

- Higher conversion rates: Offering preferred payment methods reduces cart abandonment.

- Global market access: Multi-currency and local payment method support lets you sell to customers worldwide without forcing them to use unfamiliar payment options.

- Better customer trust: Recognizable payment brands and secure checkout processes build confidence, especially for first-time buyers.

- Automated financial processes: Modern systems handle invoicing, recurring billing, and financial reporting automatically, reducing manual work.

- Stronger security protection: Built-in fraud detection, encryption, and compliance features protect both you and your customers from financial risks.

- Improved cash flow management: Faster settlement times and automated reconciliation improve your working capital and financial planning.

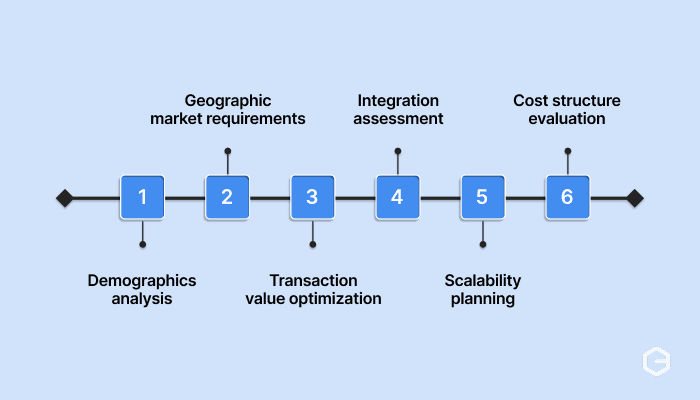

How do you choose the right e-commerce payment system?

Selecting the right payment system requires balancing customer needs, business requirements, and cost considerations. Here are the main factors to evaluate:

- Customer demographics analysis: Younger customers prefer digital wallets and BNPL, while older customers often stick to cards. Research your audience's payment preferences before making decisions.

- Geographic market requirements: Payment preferences vary significantly by country. Credit cards dominate in the US, while bank transfers are common in Europe, and mobile payments lead in Asia.

- Transaction value optimization: High-value purchases benefit from bank transfers or BNPL options, while small transactions work well with digital wallets that reduce checkout friction.

* Integration complexity assessment: Consider how easily the system integrates with your existing e-commerce platform, accounting software, and other business tools you rely on.

- Scalability planning: Choose systems that can handle growth in transaction volume and geographic expansion without requiring complete rebuilds.

- Cost structure evaluation: Compare transaction fees, setup costs, monthly fees, and currency conversion charges across different providers to find the best fit.

Collect payments from 180+ countries easily with PayGlocal

E-commerce businesses using traditional payment systems often struggle with high fees, low success rates, and compliance challenges.

PayGlocal simplifies global payment acceptance by offering faster payment processing options with affordable and transparent pricing. Here's how PayGlocal solves common payment challenges:

- Multi-currency payment collection: Accept payments in 33+ currencies from 180+ countries while settling in your preferred currency.

- Global payment method support: Offer 40+ local payment methods including cards, digital wallets, bank transfers, and regional favorites that customers trust.

- Instant compliance documentation: Automatic FIRC (Foreign Inwards Remittance Certificate) generation handling saves time and ensures you meet compliance requirements.

- One platform management: Monitor all payments, generate reports, and manage operations from a single dashboard instead of juggling multiple providers.

- Transparent pricing structure: Pay-per-transaction model with no setup fees, fixed monthly charges, or hidden costs that affect your profit margins.

Whether you're a growing SaaS company, an established exporter, or an enterprise expanding globally, PayGlocal provides the payment infrastructure you need to succeed internationally.

Final thoughts

E-commerce payment systems form the foundation of successful online businesses. The right system enables customer trust, enables global expansion, and automates financial operations that scale with your growth.

Modern businesses need payment solutions that work globally, across different currencies and customer preferences. PayGlocal provides exactly this kind of payment solution, helping companies accept international payments without the usual complexity.

The global e-commerce market continues to expand, and businesses that can accept payments from anywhere have a significant competitive advantage. Get started with PayGlocal today and turn international payment challenges into growth opportunities that drive your business forward.